Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

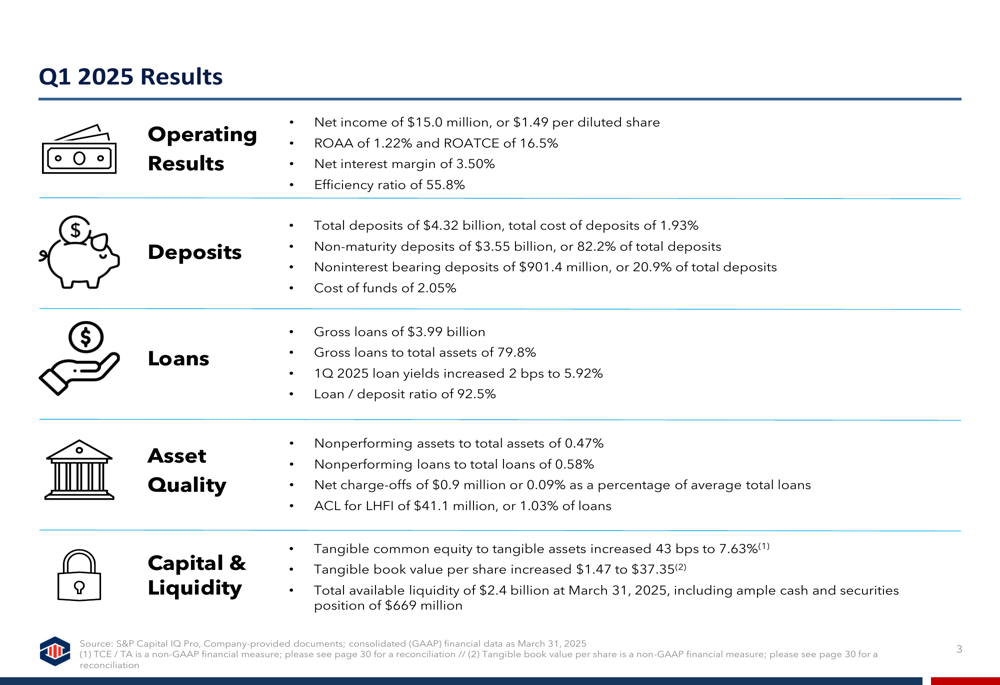

Peoples Financial Services Corp. (NASDAQ:PFIS), the holding company for Peoples Security Bank & Trust, recently presented its Q1 2025 investor results, showcasing continued growth following its merger with FNCB Bancorp. The Pennsylvania-based community bank reported net income of $15.0 million, or $1.49 per diluted share, maintaining its position as the second-largest bank by deposit market share in the Scranton MSA.

The bank’s stock has shown positive momentum recently, with shares trading at $49.77, up 2.47% in the latest session, and currently trading within its 52-week range of $38.90 to $59.70.

Quarterly Performance Highlights

Peoples Financial delivered solid financial results for Q1 2025, demonstrating strong profitability metrics and continued growth momentum. The company reported a return on average assets (ROAA) of 1.22% and return on average tangible common equity (ROATCE) of 16.5%, reflecting efficient capital utilization.

The bank’s net interest margin stood at 3.50%, while maintaining an efficiency ratio of 55.8%. These metrics indicate the company’s ability to generate revenue while controlling expenses in a challenging interest rate environment.

As shown in the following comprehensive overview of key Q1 2025 metrics:

Balance Sheet Growth and Asset Quality

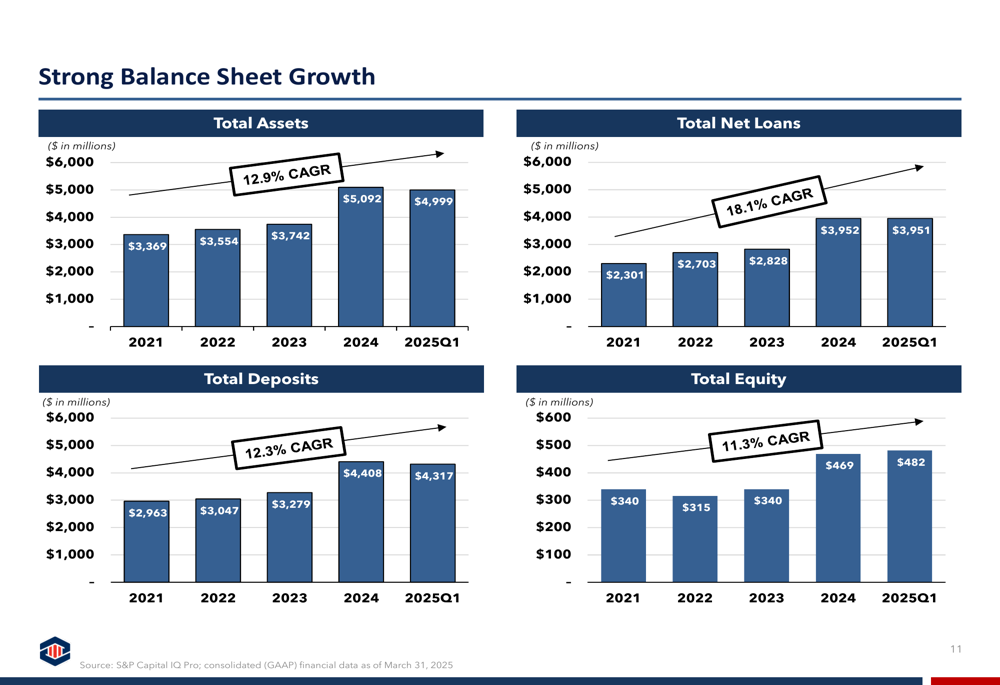

Peoples Financial has demonstrated impressive balance sheet growth over recent years. Total (EPA:TTEF) assets reached $5.00 billion in Q1 2025, representing a 12.9% compound annual growth rate (CAGR) since 2021. Net loans grew at an even faster pace of 18.1% CAGR, reaching $3.95 billion, while total deposits increased to $4.32 billion, reflecting a 12.3% CAGR.

The following chart illustrates this consistent growth trajectory across key balance sheet components:

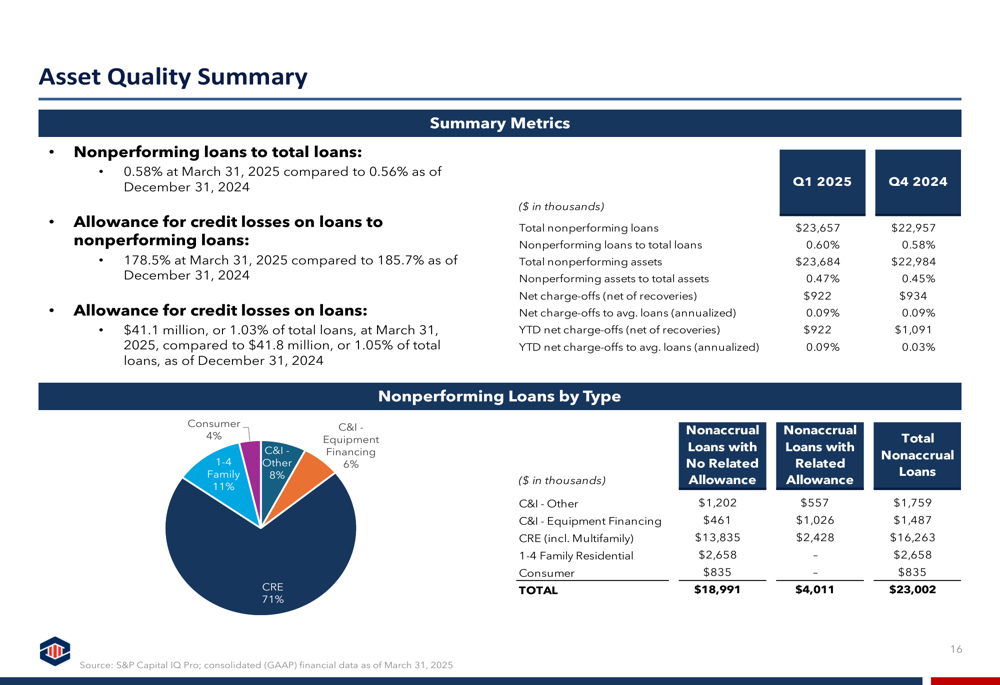

Asset quality remains stable, with nonperforming assets to total assets at 0.47% and nonperforming loans to total loans at 0.58% as of March 31, 2025. The allowance for credit losses on loans stood at $41.1 million, representing 1.03% of total loans and providing 178.5% coverage of nonperforming loans.

The bank’s loan portfolio is well-diversified, with commercial real estate (CRE) comprising the largest segment at 35.0% of total loans, followed by 1-4 family residential (19.1%), commercial and industrial (17.6%), and multifamily (10.4%).

The following asset quality summary provides a detailed breakdown of the bank’s credit metrics:

Deposit Base and Funding

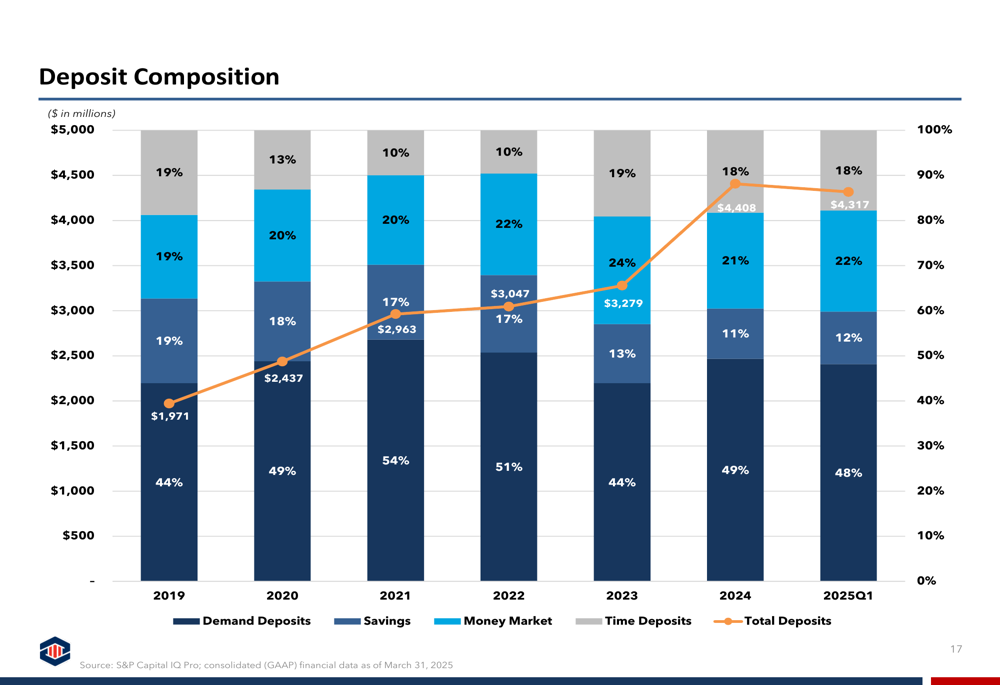

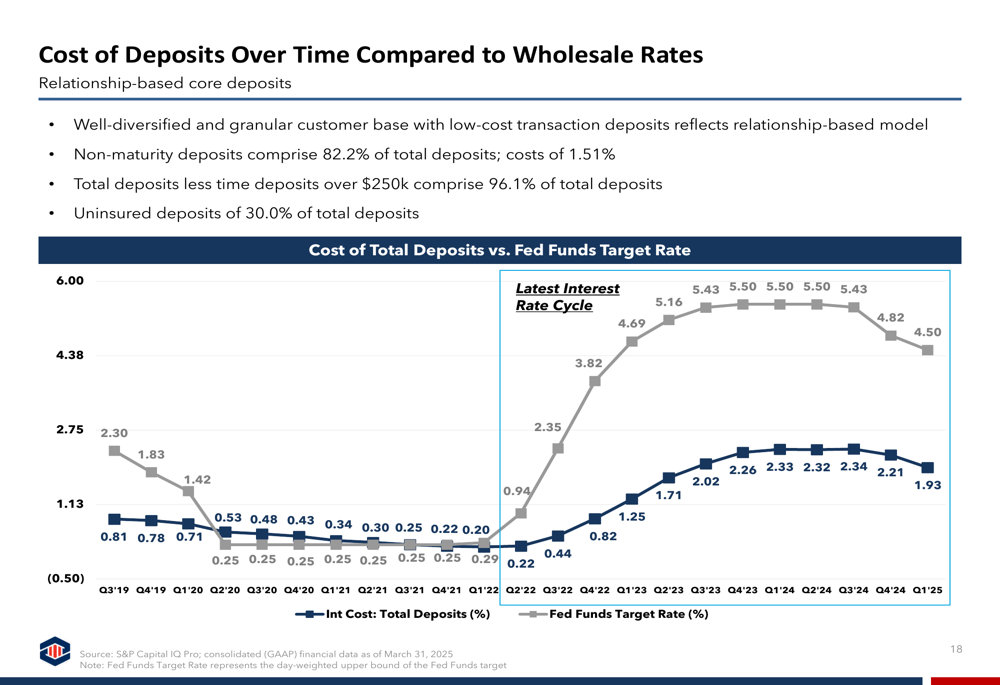

Peoples Financial maintains a strong deposit franchise built over its 100+ year history. As of Q1 2025, non-maturity deposits comprised 82.2% of total deposits, with noninterest-bearing deposits accounting for 20.9% of the total. The bank’s cost of deposits was 1.93%, while the overall cost of funds stood at 2.05%.

The company highlighted that its cost of funds (1.99%) compares favorably to the median of all Pennsylvania banks (2.14%), demonstrating its ability to attract and retain lower-cost deposits through relationship banking.

The following chart shows the evolution of the bank’s deposit composition over time:

The bank has also effectively managed its deposit costs relative to wholesale rates, as illustrated in this comparison:

Strategic Positioning and Market Presence

Peoples Financial holds a strong competitive position in its core markets. The bank ranks second in deposit market share (16.1%) in the Scranton-Wilkes-Barre MSA, which accounts for approximately 57% of its deposit franchise. It maintains a dominant position in Susquehanna County with a 65% market share and is expanding its presence in the fast-growing Lehigh Valley region.

The company’s recent merger with FNCB has strengthened its market position and contributed to improved profitability. Management noted that Q1 2025 results reflect successful execution of merger initiatives, including realization of cost savings and purchase accounting accretion.

The following overview highlights the bank’s principal markets and competitive positioning:

Forward-Looking Statements

Peoples Financial appears well-positioned for continued growth, supported by its strong market presence, experienced management team (with over 375 years of combined banking experience), and robust capital position. The bank’s tangible common equity to tangible assets ratio increased 43 basis points to 7.63%, while tangible book value per share grew by $1.47 to $37.35.

The company’s liquidity position remains strong, with total available liquidity of $2.4 billion as of March 31, 2025, including cash and securities of $669 million. This provides ample flexibility to support future loan growth and navigate potential economic challenges.

While the presentation highlights numerous strengths, investors should note that rising deposit costs (from 0.27% in 2021 to 1.93% in Q1 2025) could pressure margins if interest rates remain elevated. Additionally, the slight increase in nonperforming assets warrants monitoring, though current levels remain manageable.

Overall, Peoples Financial’s Q1 2025 presentation portrays a community bank with solid fundamentals, strategic growth initiatives, and the financial strength to capitalize on opportunities in its expanding market footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.