Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Perseus Mining Ltd (ASX:PRU) delivered its June 2025 Quarter Report Webinar on July 28, 2025, highlighting how surging gold prices have significantly boosted the company’s financial performance despite relatively flat production. The gold producer, with operations across West Africa, has capitalized on favorable market conditions while maintaining disciplined cost management and advancing key growth projects.

The company’s share price has reflected this strong performance, trading near AU$4.87 as of October 14, 2025, close to its 52-week high of AU$5.04 and significantly above its 52-week low of AU$2.45.

Quarterly Performance Highlights

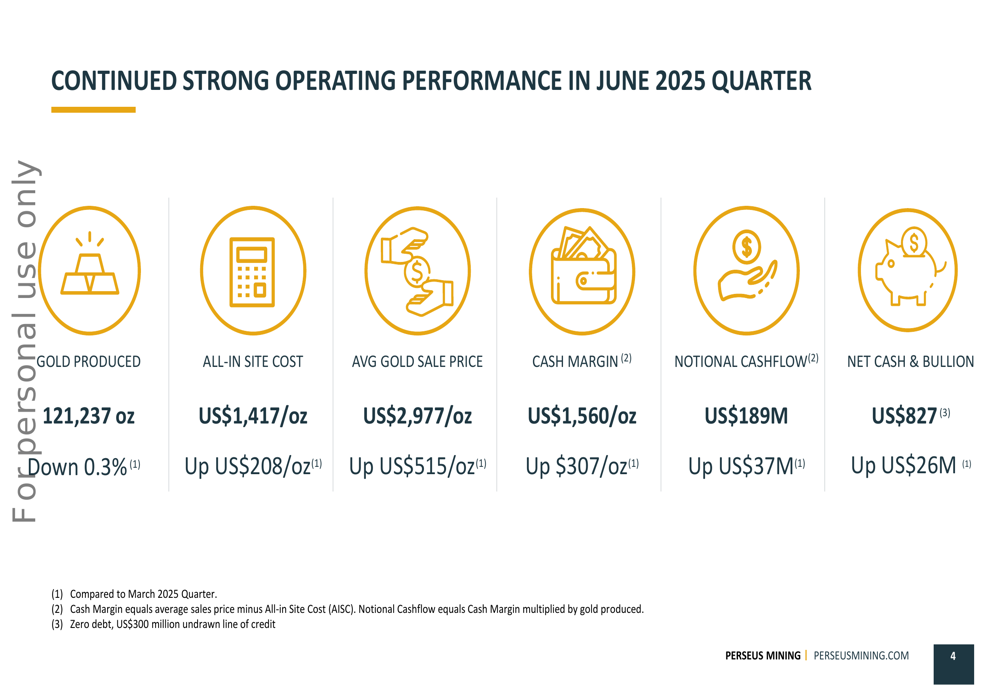

Perseus reported gold production of 121,237 ounces for the June 2025 quarter, representing a marginal decrease of 0.3% compared to the March 2025 quarter. However, the company’s financial metrics showed substantial improvement due to rising gold prices.

As shown in the following chart detailing quarterly performance:

The average gold sale price reached US$2,977 per ounce, up US$515 per ounce from the previous quarter, driving cash margins to US$1,560 per ounce (up US$307). This translated into notional cashflow of US$189 million for the quarter, a US$37 million increase over the March quarter.

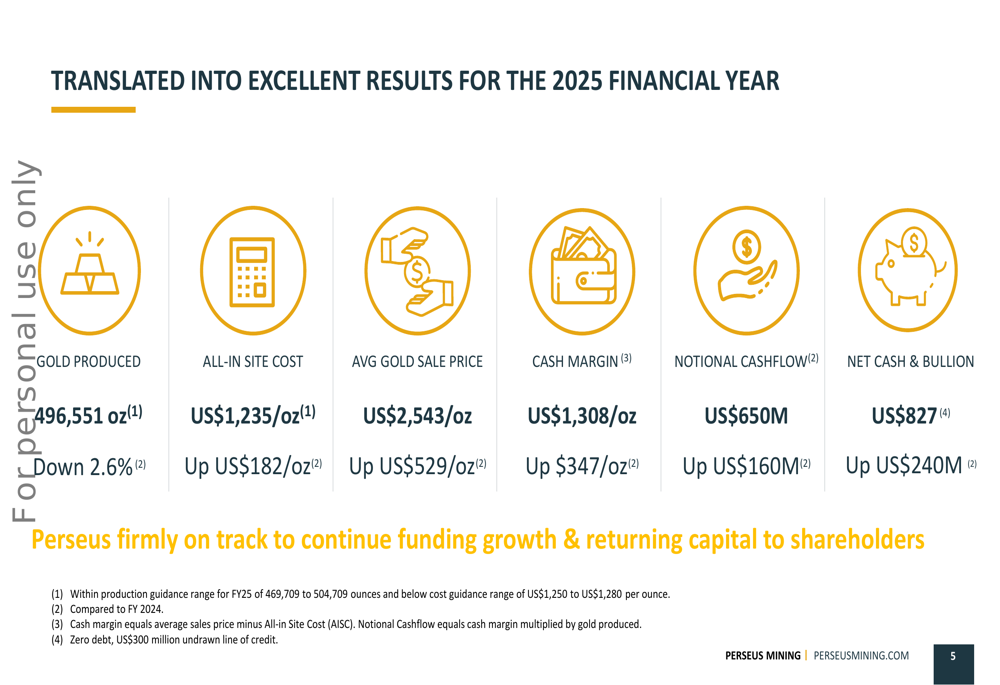

For the full 2025 financial year, Perseus delivered 496,551 ounces of gold, slightly below the previous year but within the company’s guidance range:

The company’s all-in site cost (AISC) for FY2025 was US$1,235 per ounce, up from US$1,053 per ounce in FY2024, but still below the guidance range of US$1,250-1,280 per ounce. The average gold sale price for the year was US$2,543 per ounce, generating a healthy cash margin of US$1,308 per ounce and notional cashflow of US$650 million.

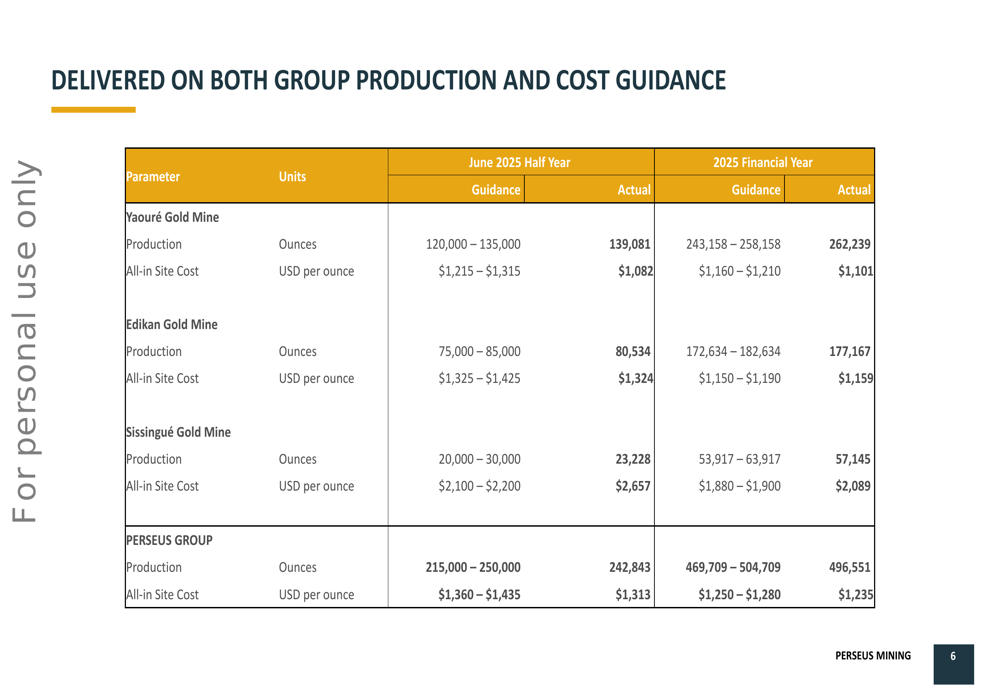

Perseus successfully met both its production and cost guidance across all three operating mines (Yaouré, Edikan, and Sissingué) for both the half-year and full-year periods:

Financial Position and Shareholder Returns

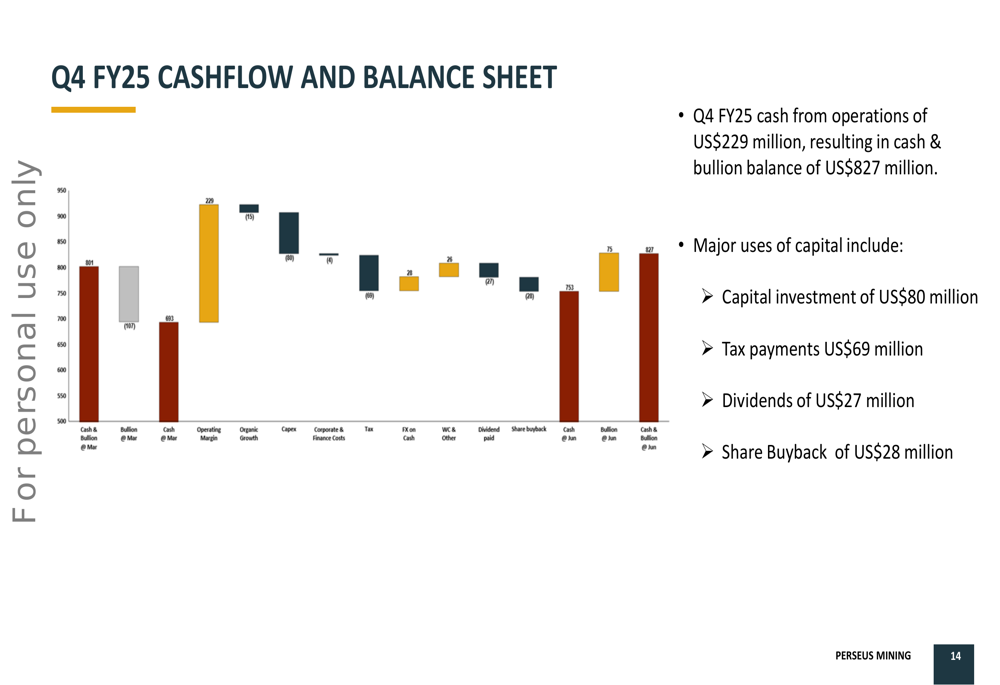

Perseus’s financial position strengthened considerably during the quarter, with net cash and bullion increasing to US$827 million, up US$26 million from the March quarter and US$240 million from the previous year. The company maintains zero debt and has an undrawn credit facility of US$300 million, providing substantial financial flexibility.

The following chart illustrates the company’s Q4 FY25 cashflow:

Major uses of capital during the quarter included US$80 million in capital investments, US$69 million in tax payments, US$27 million in dividends, and US$28 million for the share buyback program.

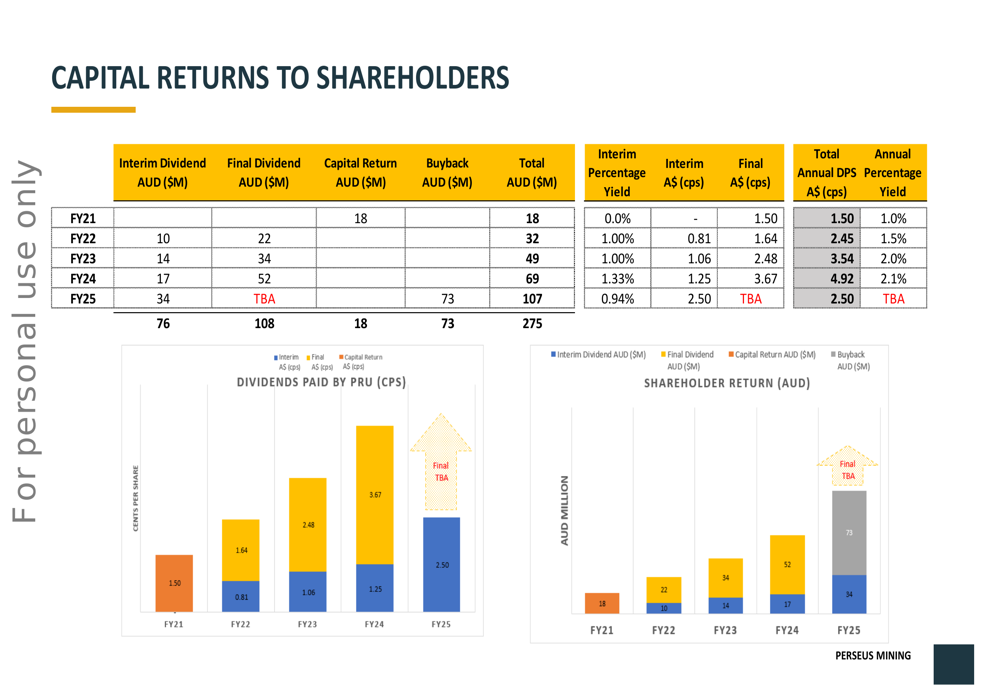

Perseus has maintained a strong focus on returning capital to shareholders, with total returns of A$107 million in FY2025 and A$275 million since FY2021:

The company’s ongoing share buyback program has reached 73% of its A$100 million target as of July 11, 2025, with 22.9 million shares repurchased at an average price of A$3.17.

Growth Projects

Perseus is advancing two major growth projects that will support future production: the Nyanzaga Gold Project in Tanzania and the CMA Underground mine at Yaouré in Côte d’Ivoire.

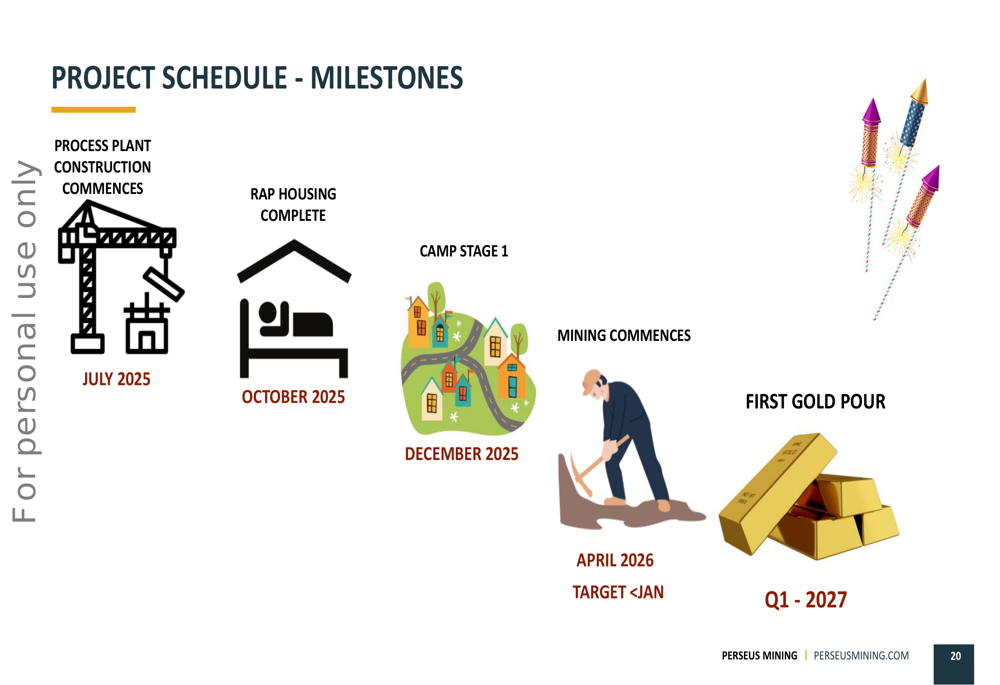

The Nyanzaga project is progressing toward first gold production in early 2027, with key milestones outlined below:

Construction of the process plant is scheduled to commence in July 2025, with mining operations starting in April 2026 and first gold pour expected in Q1 2027. Once operational, Nyanzaga is projected to produce 725,000-750,000 ounces over its first five years at an AISC of US$1,230-1,330 per ounce, making it Perseus’s lowest-cost asset.

The CMA Underground mine development received final investment decision approval in January 2025, with underground mining activities scheduled to begin in Q1 FY26. However, commencement of work on cutting portals is contingent on formal granting of an Arrêté (presidential decree) setting out mining regulations, as Côte d’Ivoire currently lacks specific legislation governing underground mining.

Forward Outlook

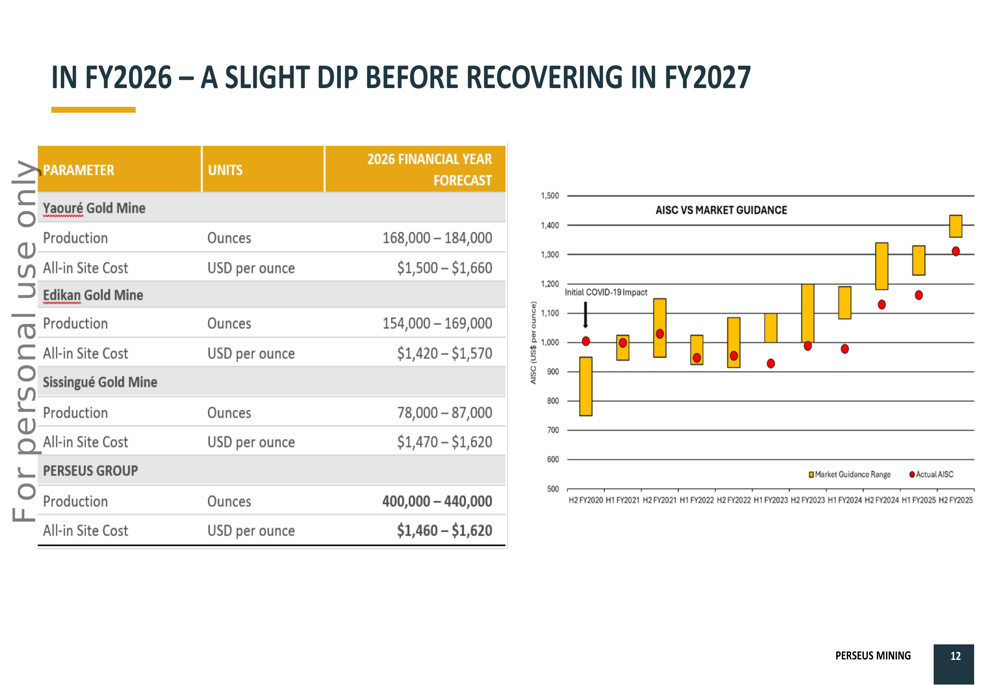

Perseus’s production guidance for FY2026 indicates a temporary dip to 400,000-440,000 ounces at an AISC of US$1,460-1,620 per ounce before recovering in FY2027:

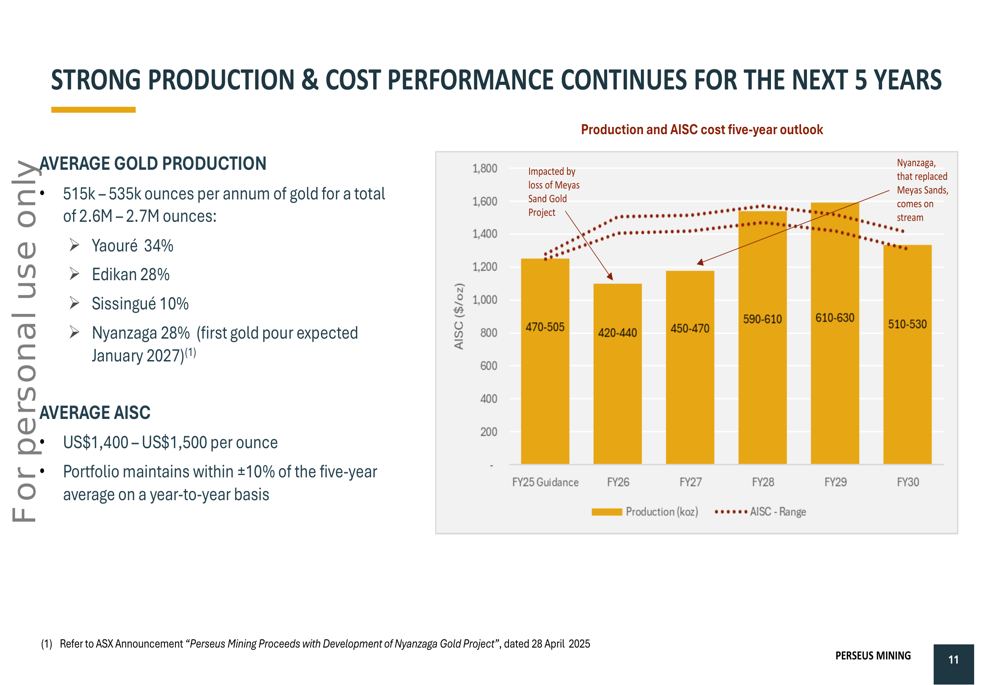

However, the company’s five-year outlook remains strong, with projected average annual gold production of 515,000-535,000 ounces from FY2025 to FY2030:

This production profile includes contributions from Yaouré (34%), Edikan (28%), Sissingué (10%), and Nyanzaga (28% once operational). The portfolio is expected to maintain costs within ±10% of the five-year average AISC of US$1,400-1,500 per ounce on a year-to-year basis.

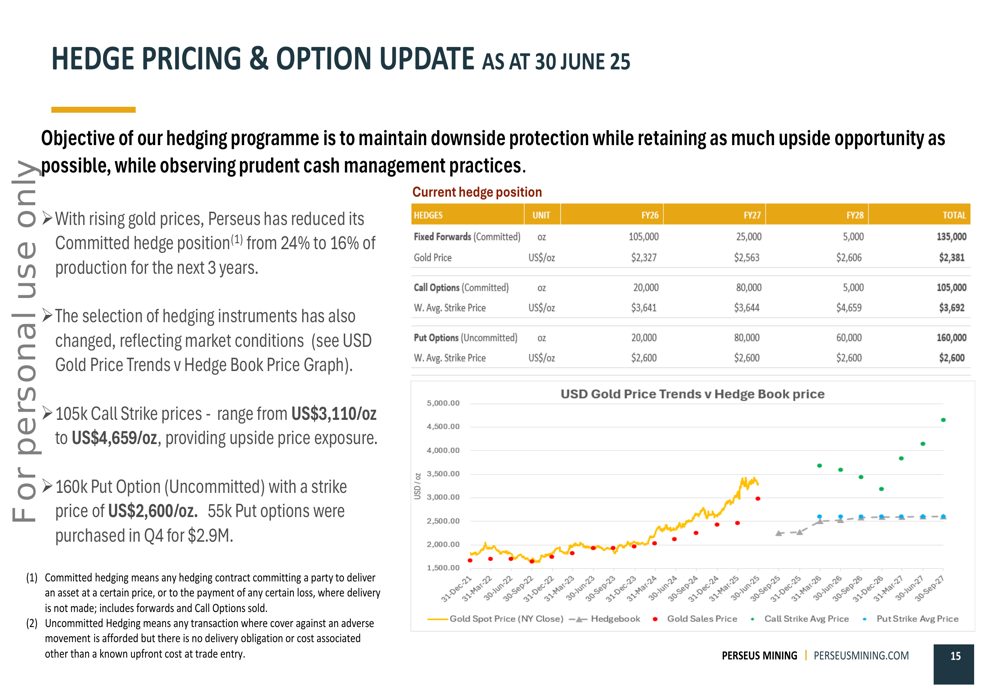

Perseus has also adjusted its hedging strategy in response to rising gold prices, reducing its committed hedge position from 24% to 16% of production for the next three years:

The current hedge position includes 135,000 ounces in fixed forwards at US$2,381 per ounce, 105,000 ounces in call options at US$3,692 per ounce, and 160,000 ounces in uncommitted put options at US$2,600 per ounce.

With its strong cash position, disciplined cost management, and clear growth strategy, Perseus Mining appears well-positioned to navigate the temporary production dip in FY2026 while continuing to deliver value to shareholders through both growth investments and capital returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.