Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Polska Grupa Energetyczna (PGE) released its Q2 and H1 2025 financial results on September 9, 2025, highlighting continued progress in its energy transition strategy despite significant impairment charges affecting bottom-line results. The Polish energy giant reported strong EBITDA performance while maintaining a solid financial position to support its ongoing capital investments in gas-fired generation and renewable energy projects.

The presentation comes after PGE reported record EBITDA in Q1 2025, continuing the company’s momentum in operational performance despite challenging market conditions. The company’s stock has shown impressive performance year-to-date, with a 116.67% return according to recent market data.

Quarterly Performance Highlights

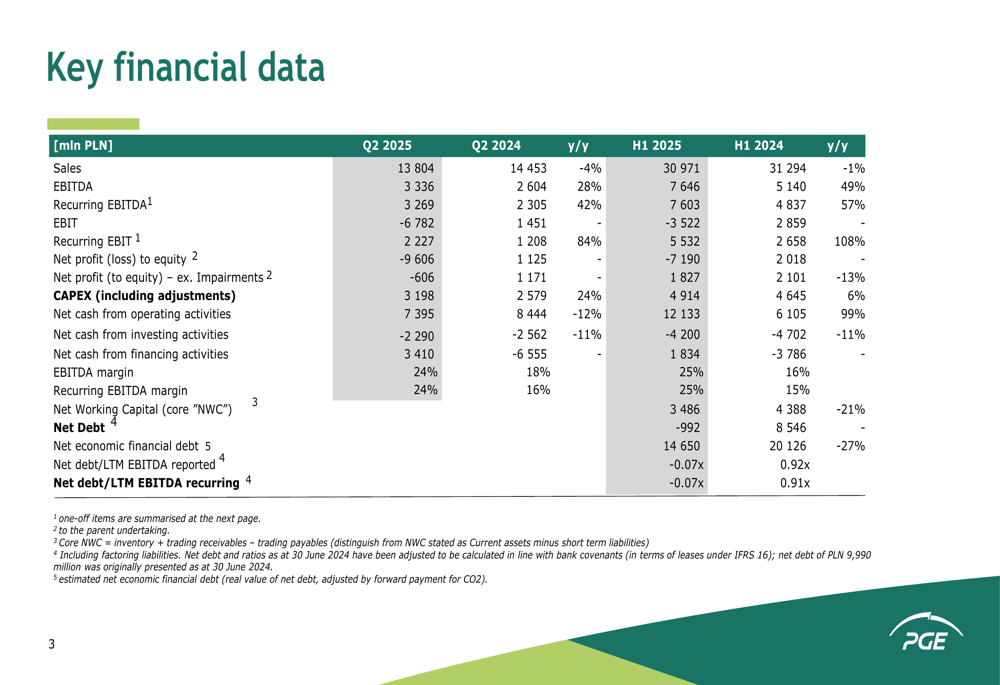

PGE reported Q2 2025 sales of 13,804 million PLN, with EBITDA reaching 3,336 million PLN (reported) and 3,269 million PLN (recurring), representing a solid 24% EBITDA margin. However, significant impairment charges led to a reported EBIT of -6,782 million PLN and a net loss of 9,606 million PLN for the quarter. Excluding impairments, the adjusted net loss was substantially reduced to 606 million PLN.

For the first half of 2025, the company achieved sales of 30,971 million PLN and EBITDA of 7,646 million PLN (reported) and 7,603 million PLN (recurring), maintaining a strong 25% EBITDA margin. Despite the positive operational performance, H1 reported net loss stood at 7,190 million PLN, though excluding impairments, the company would have posted a net profit of 1,827 million PLN.

As shown in the following comprehensive financial overview:

Detailed Financial Analysis

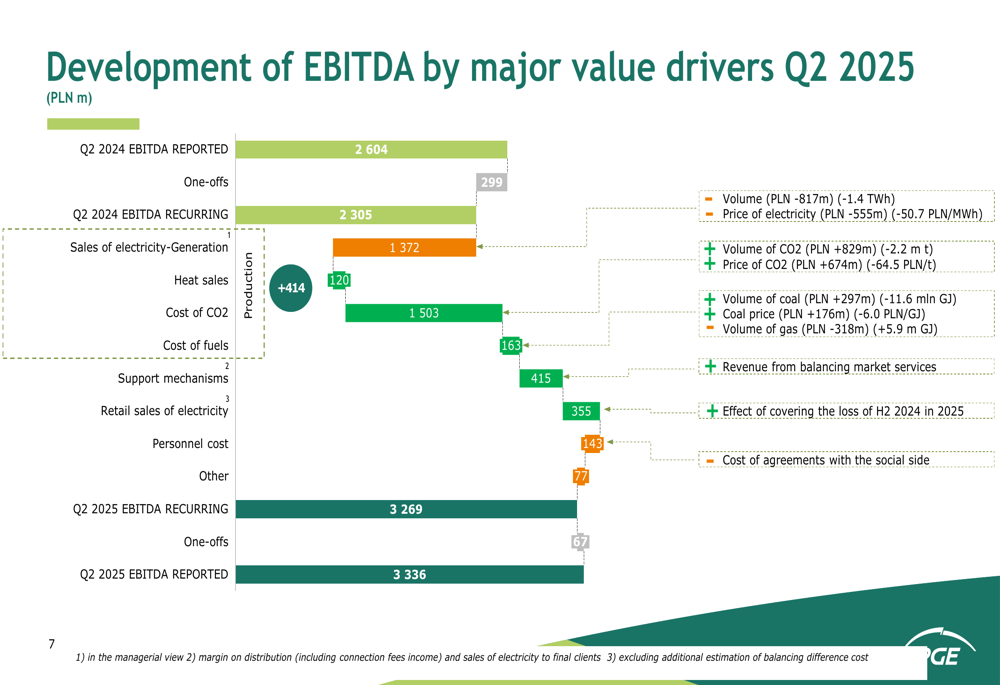

The development of PGE’s EBITDA in Q2 2025 was driven by several key factors, including improved electricity generation margins, heat sales, and retail electricity sales, partially offset by increased personnel costs and other expenses. The company’s recurring EBITDA reached 3,269 million PLN, with one-off items adding 67 million PLN to reach the reported EBITDA of 3,336 million PLN.

The following chart illustrates the major value drivers affecting EBITDA performance in Q2 2025:

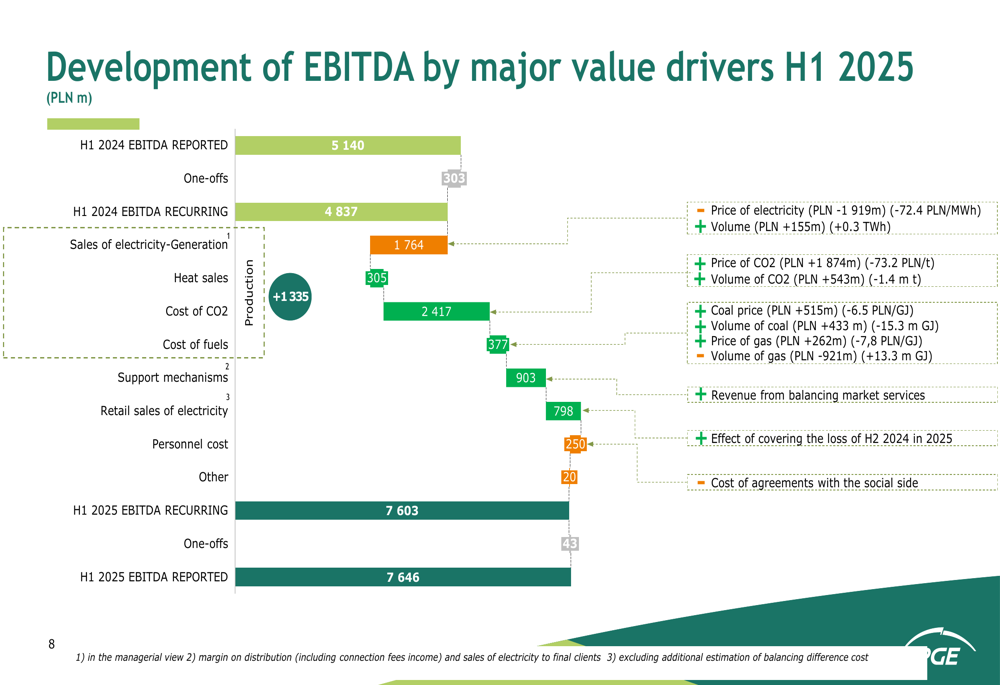

For the first half of 2025, similar trends were observed, with recurring EBITDA reaching 7,603 million PLN and one-off items contributing an additional 43 million PLN to the reported EBITDA of 7,646 million PLN:

PGE’s segment performance reflects its ongoing energy transition, with Distribution contributing the largest share (35%) of H1 2025 recurring EBITDA, followed by Supply (16%), District Heating (16%), and Renewables (13%). The Coal Energy segment represented only 5% of recurring EBITDA, highlighting the company’s shift away from coal-based generation.

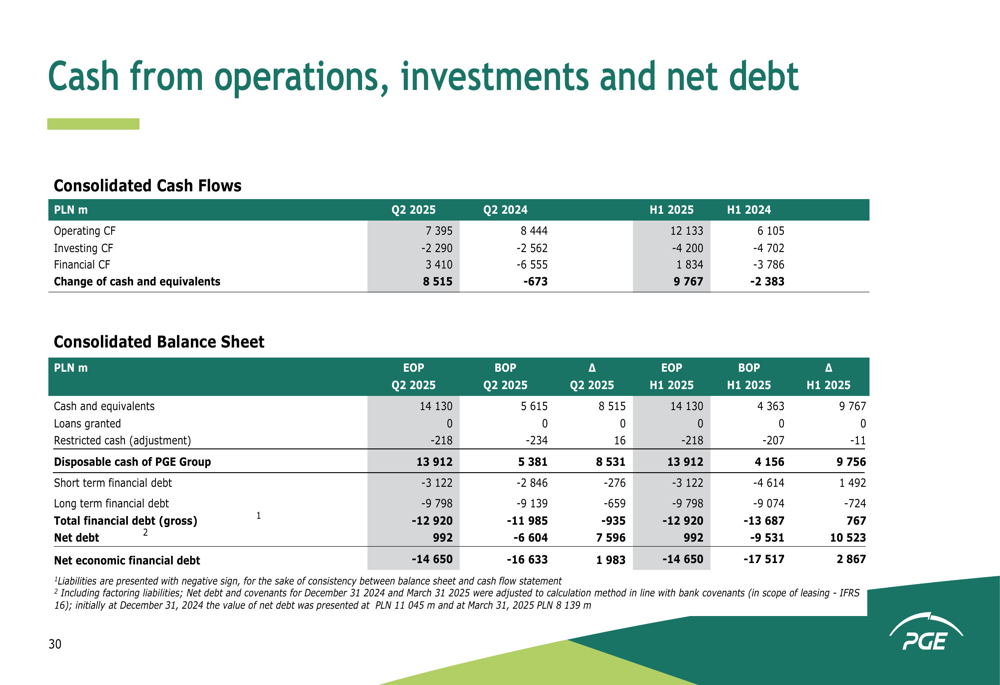

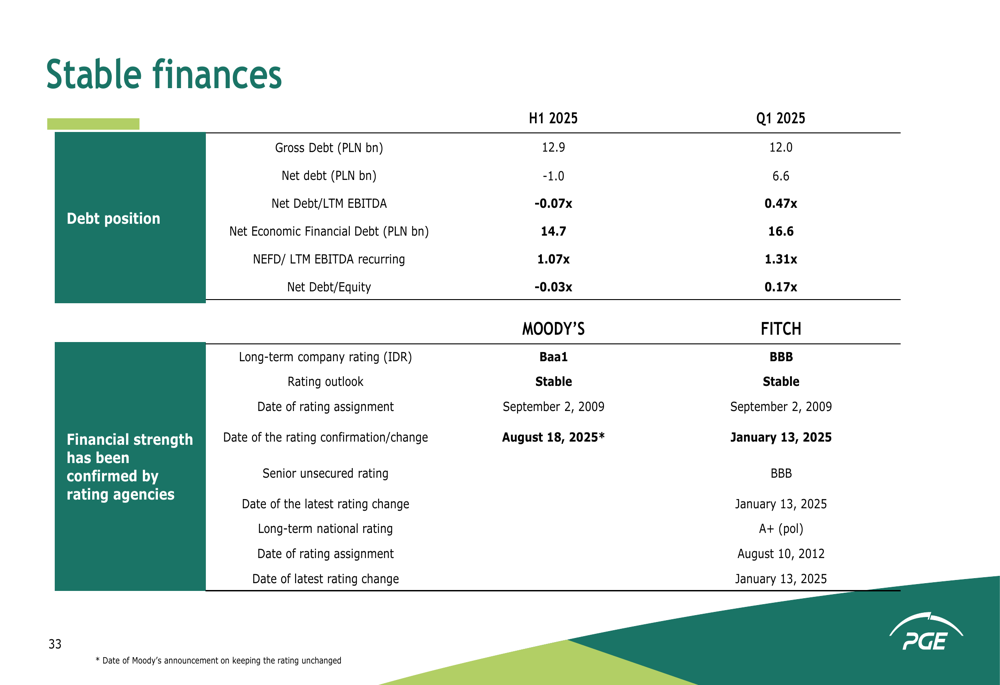

The company’s cash flow performance remained strong, with net cash from operating activities reaching 7,395 million PLN in Q2 2025 and 12,133 million PLN in H1 2025. PGE maintained a solid financial position with a negative net debt of 992 million PLN, indicating a net cash position, though net economic financial debt stood at 14,650 million PLN.

The following table provides a detailed breakdown of cash flows and debt position:

PGE’s stable financial position is further evidenced by its credit ratings and debt metrics:

Strategic Initiatives

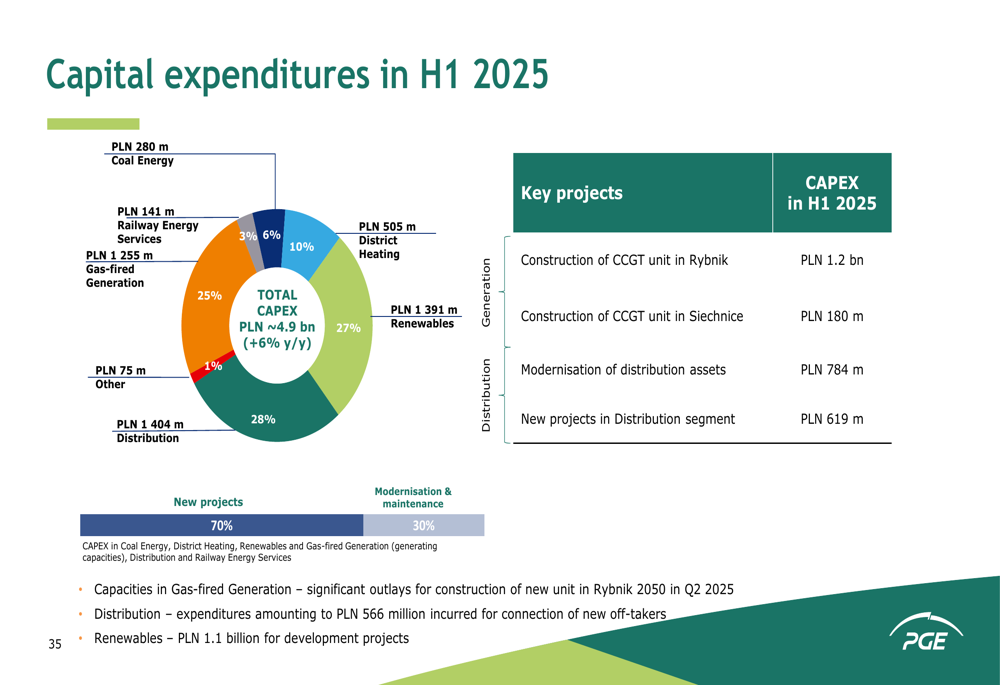

Capital expenditures in H1 2025 totaled approximately 4.9 billion PLN, representing a 6% increase year-over-year. The company allocated 70% of CAPEX to new projects and 30% to modernization and maintenance activities. Major investments included the construction of CCGT units in Rybnik (1.2 billion PLN) and Siechnice (180 million PLN), as well as modernization of distribution assets (784 million PLN).

The capital expenditure breakdown reflects PGE’s strategic focus on transitioning from coal to gas-fired generation and renewables:

On an accrual basis, capital expenditures were distributed across segments, with significant investments in Gas-fired Generation, Distribution, and Renewables, underscoring the company’s commitment to its energy transition strategy.

Operational Performance

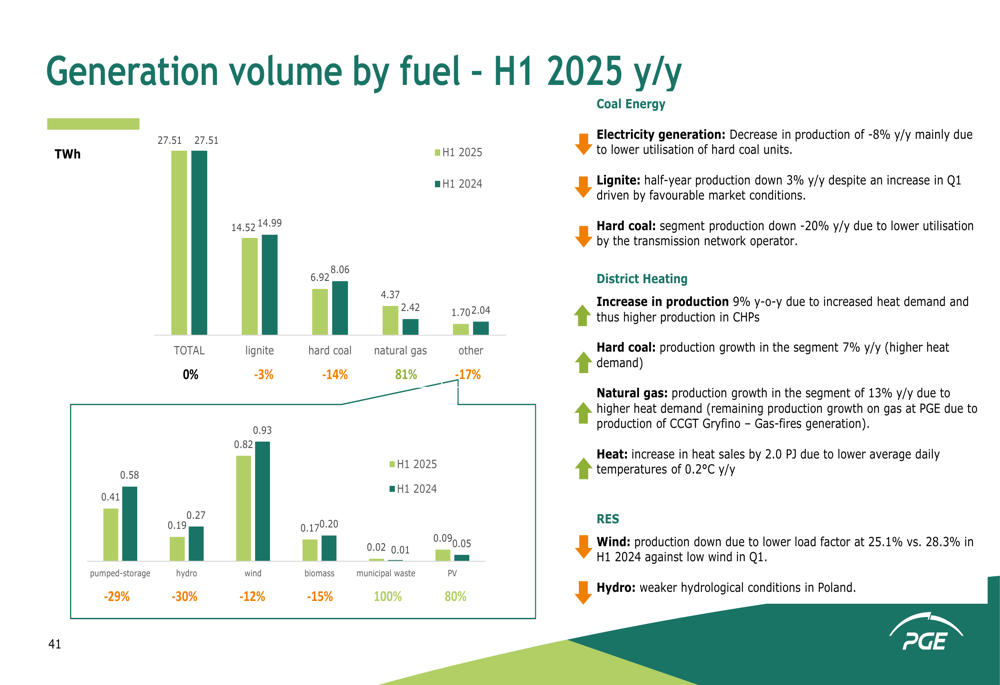

PGE’s operational performance in H1 2025 showed mixed results, with electricity generation volumes declining year-over-year, particularly in coal-based generation. The company’s generation mix continued to shift toward cleaner sources, with increased contribution from renewables and gas-fired generation.

The following chart illustrates the generation volume by fuel type for H1 2025 compared to H1 2024:

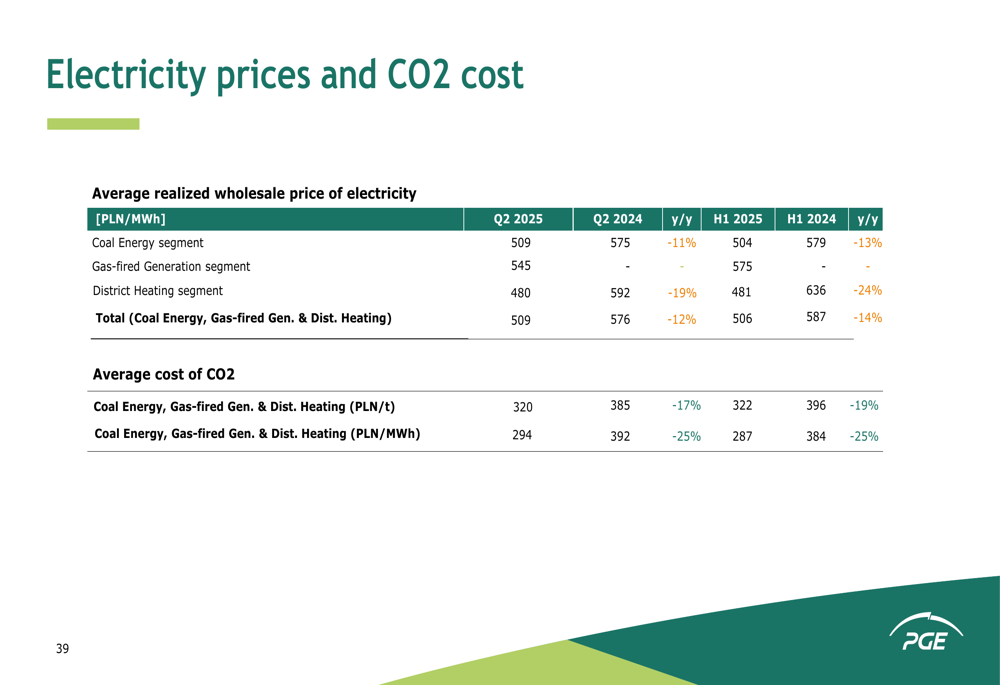

Electricity prices and CO2 costs remained key factors affecting PGE’s performance, with the average realized wholesale price of electricity varying across segments:

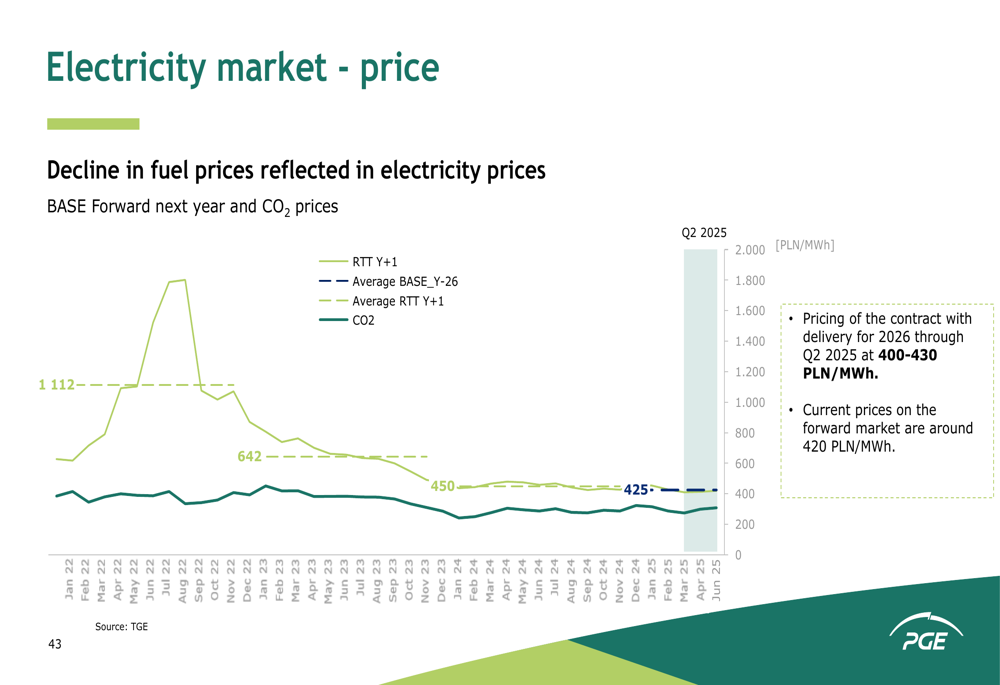

The electricity market showed pricing for 2026 delivery contracts at 400-430 PLN/MWh during Q2 2025, with CO2 and fuel prices influencing the overall market dynamics:

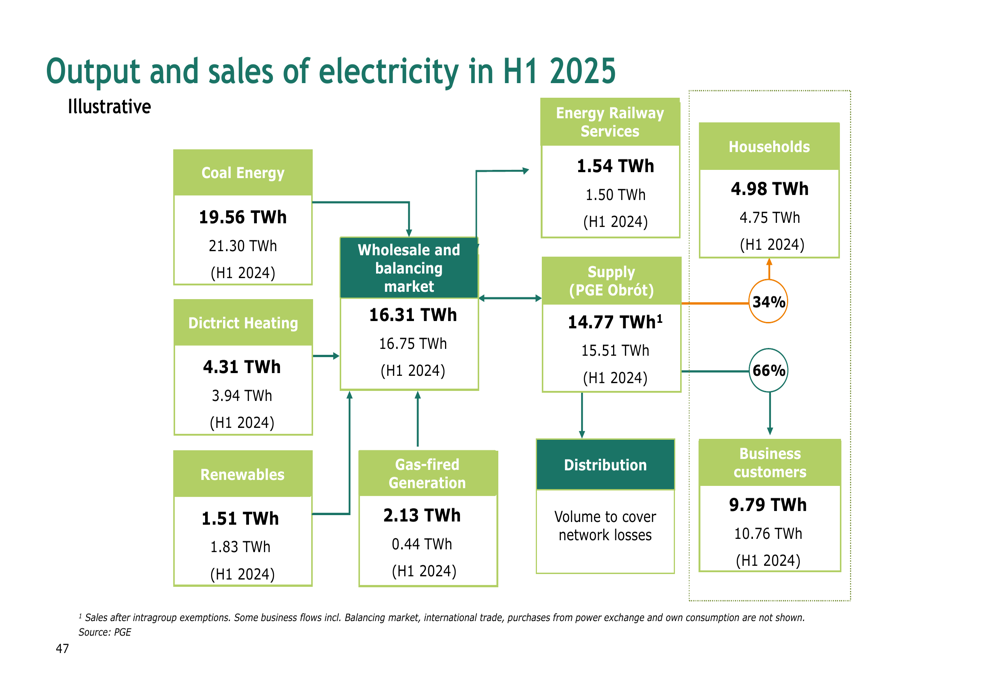

PGE’s electricity output and sales flow in H1 2025 demonstrates the company’s integrated business model, from generation through wholesale markets to final customers:

Forward-Looking Statements

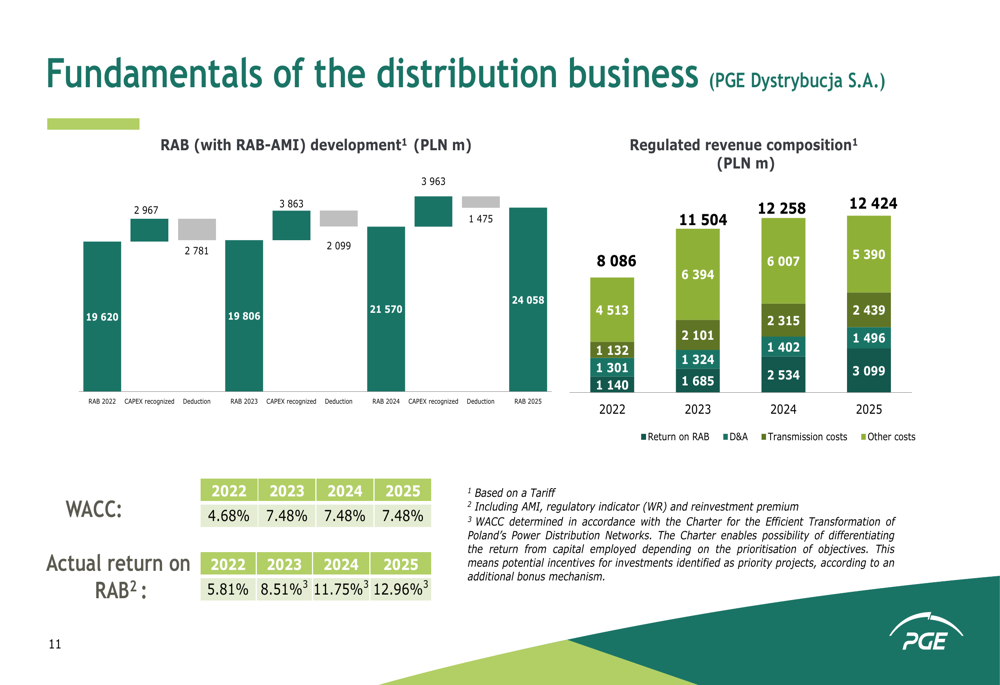

Looking ahead, PGE continues to focus on its energy transition strategy, with ongoing investments in gas-fired generation, renewables, and distribution infrastructure. The company’s distribution business remains a key contributor to earnings, with regulated asset base (RAB) growth and improving returns on investment.

The fundamentals of PGE’s distribution business show positive trends in regulated revenue composition and returns:

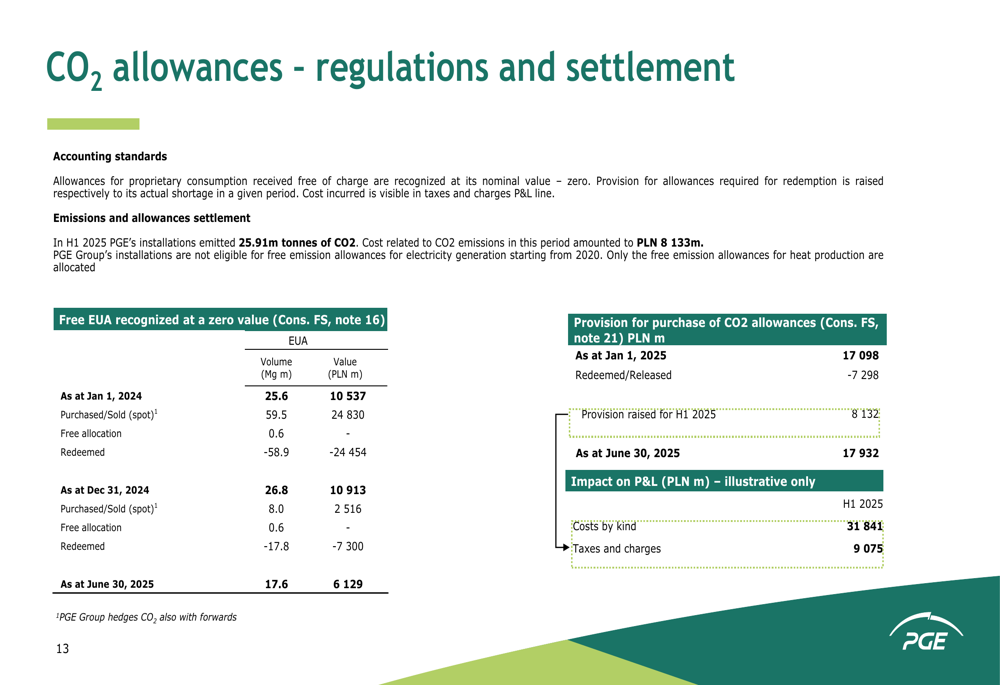

CO2 allowances and their regulatory treatment remain an important factor for PGE’s financial performance, with the company actively managing its exposure:

While PGE faces challenges such as market volatility and regulatory pressures, its strategic investments and financial discipline position it well for future growth. The company’s energy transition strategy continues to advance, with increasing focus on renewables and gas-fired generation to replace coal-based capacity over time.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.