China AI: Bernstein sees chipmakers benefiting from Nvidia scrutiny

Introduction & Market Context

Phathom Pharmaceuticals (NASDAQ:PHAT) presented its first quarter 2025 earnings results in May, highlighting continued adoption of its VOQUEZNA (vonoprazan) product while outlining a strategic path to profitability. The company’s stock has shown recent signs of recovery, trading at $10.90 in the aftermarket session on June 18, 2025, up 3.81% from its previous close of $10.50, though still well below its 52-week high of $19.71.

The specialty pharmaceutical company, focused on gastrointestinal diseases, reported steady prescription growth for VOQUEZNA despite seasonal headwinds, while emphasizing cost-reduction initiatives aimed at achieving profitable operations by 2026 without requiring additional financing.

Quarterly Performance Highlights

Phathom reported Q1 2025 net revenue of $28.5 million, slightly below the $29.7 million achieved in Q4 2024 but significantly higher than the $1.9 million reported in Q1 2024. The company beat analyst expectations, with earnings per share of -$1.07 compared to forecasts of -$1.11.

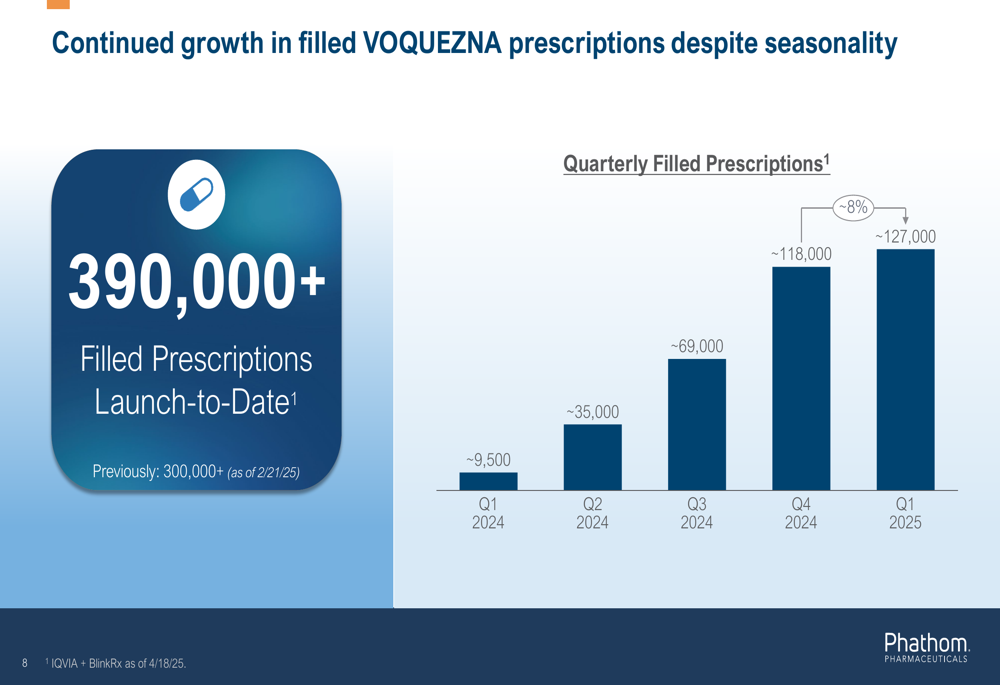

VOQUEZNA prescriptions continued to grow, with the company reporting over 390,000 total filled prescriptions since launch (as of April 18, 2025), up from 300,000+ as of February 21, 2025. The quarterly filled prescriptions showed consistent growth from launch through Q1 2025.

As shown in the following chart of quarterly prescription growth:

The Q1 2025 prescription volume reached approximately 127,000, representing an 8% increase from Q4 2024 despite typical seasonal challenges in the first quarter. This growth trajectory demonstrates continued market penetration for VOQUEZNA, which the company positions as a rapid, potent, and durable treatment option.

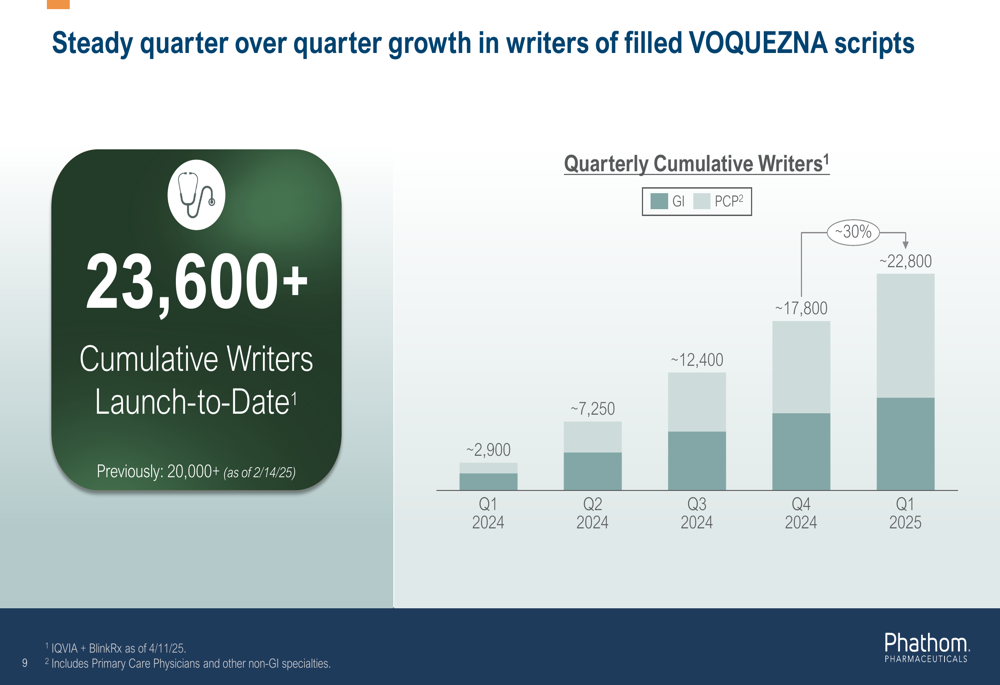

Equally impressive was the expansion of the prescriber base, with cumulative writers reaching 23,600+ as of April 11, 2025, up from 20,000+ in mid-February. The prescriber growth rate actually accelerated compared to prescription volume, with a 30% quarter-over-quarter increase.

The prescriber growth is illustrated in this detailed breakdown between gastroenterologists (GI) and primary care physicians (PCP):

This prescriber expansion is particularly significant as it suggests potential for sustained future growth, with both specialist gastroenterologists and primary care physicians increasingly adopting VOQUEZNA into their treatment protocols.

Strategic Initiatives

Phathom outlined four key strategic focus areas aimed at achieving profitable operations by 2026:

The company’s strategic roadmap emphasizes continued prescription growth while implementing significant cost reductions to reach quarterly operating expenses below $55 million by Q4 2025 (excluding stock-based compensation). This represents a substantial reduction from the $103.7 million in total operating expenses reported for Q1 2025.

CEO Steve Bosta emphasized during the earnings call that the company is at "an inflection point for FAVEN, transitioning from an early-stage company to a stable, profitable organization." He further reassured stakeholders that the company’s priorities would remain serving patients, the team, and investors.

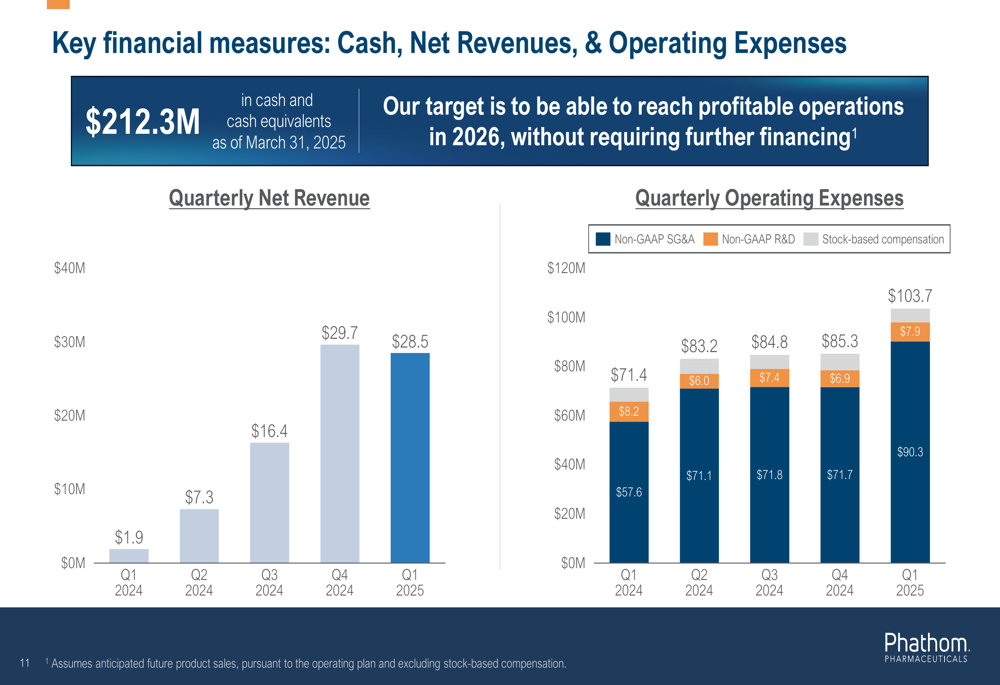

The strategy also focuses on maintaining the strength of the sales organization while mitigating financing risk. With $212.3 million in cash and cash equivalents as of March 31, 2025, management believes the company has sufficient resources to reach profitability without additional financing.

Detailed Financial Analysis

Phathom’s financial results revealed both progress and challenges. While prescription growth continued, revenue slightly declined quarter-over-quarter. The company maintained a strong gross margin of 87%, indicating effective cost management for its product.

The comprehensive financial picture is illustrated in this chart showing revenue and operating expenses:

Operating expenses for Q1 2025 totaled $103.7 million, with non-GAAP SG&A expenses accounting for $90.3 million, non-GAAP R&D at $6.9 million, and stock-based compensation at $7.9 million. The company’s focus on cost reduction is evident in its target to reduce quarterly operating expenses to below $55 million by Q4 2025.

Despite the earnings beat, Phathom’s stock faced pressure in the market following the earnings announcement, declining 1.4% in premarket trading on the day of the release. This suggests investor concerns about the company’s path to profitability despite the positive prescription trends.

Forward-Looking Statements

Phathom’s presentation emphasized its commitment to achieving profitable operations by 2026 without requiring additional financing. The company’s strategy hinges on balancing continued prescription growth with aggressive cost-cutting measures.

Management confirmed during the Q&A session that there would be no reductions in the sales force, indicating confidence in the market potential for VOQUEZNA. However, they remained flexible about the exact timing of achieving profitability in 2026.

Potential challenges highlighted in the earnings report include continued net losses impacting investor confidence, a high gross-to-net discount rate pressuring margins, and market competition, particularly the potential entry of competitor product Sabella.

With a solid cash position of $212.3 million and growing prescription trends, Phathom appears positioned to execute its strategic plan, though investors will be closely monitoring the company’s progress toward its ambitious profitability target in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.