SoftBank Group Q2 profit blows past expectations; sells Nvidia stake for $5.8 bln

Introduction & Market Context

Philip Morris International Inc (NYSE:PM) reported strong second-quarter 2025 results on July 22, showcasing accelerated growth in its smoke-free product portfolio and raising its full-year earnings guidance. Despite the impressive performance, the stock faced pressure in premarket trading, down 5.45% to $170.65, following a 0.98% gain in the previous session.

The tobacco giant continues its transformation into a smoke-free company, with smoke-free products now representing a significant portion of its business and driving margin expansion across the board.

Quarterly Performance Highlights

PMI delivered robust financial results for both Q2 and the first half of 2025, with growth across all key metrics. The company reported Q2 adjusted diluted earnings per share of $1.91, representing a 20.1% increase including currency effects, while net revenues grew 7.1% to $10.1 billion.

As shown in the following comprehensive financial data:

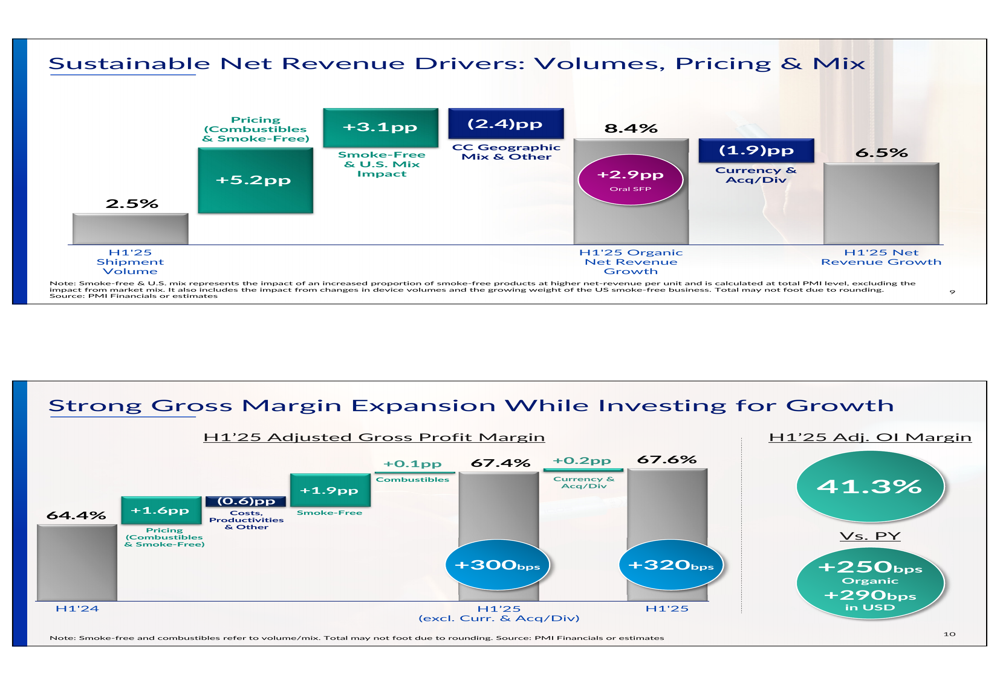

For the first half of 2025, PMI’s adjusted operating income increased by 14.5% to $8.0 billion, with an impressive operating income margin of 41.3%, representing an expansion of 250 basis points organically. This performance demonstrates the company’s ability to drive both top-line growth and margin improvement simultaneously.

Smoke-Free Products Growth

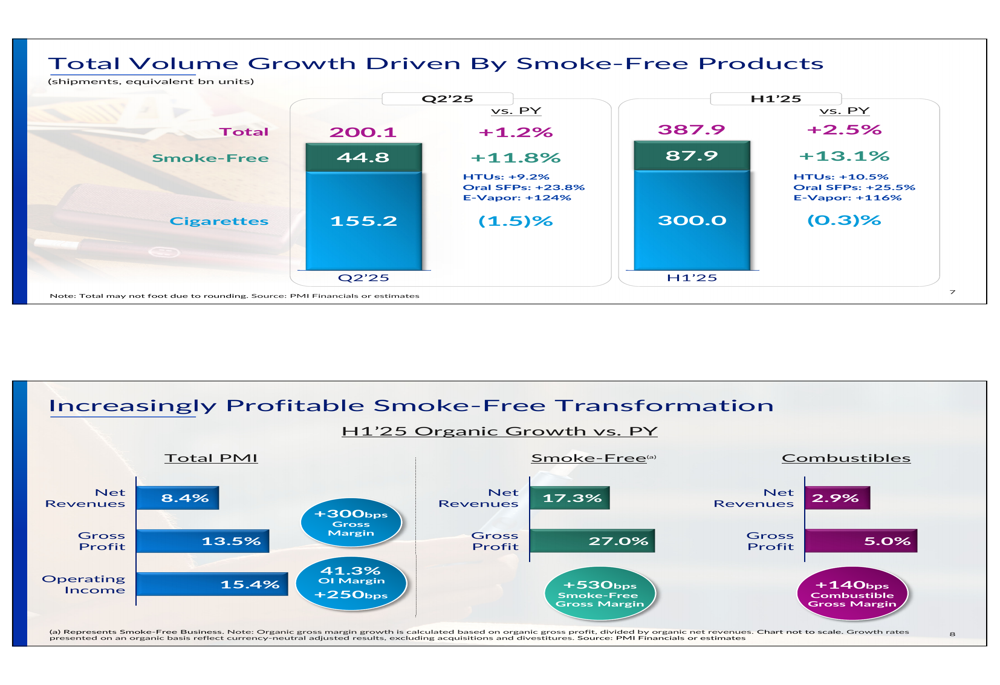

The company’s smoke-free product portfolio continues to be the primary growth engine, with total smoke-free product users reaching approximately 41.5 million by the end of H1 2025, up from 39.0 million at the end of 2024. This includes approximately 34 million IQOS users, 6.5 million oral product users, and over 1 million VEEV users.

PMI’s smoke-free product shipment volumes increased by 11.8% in Q2 2025, with heated tobacco units growing 9.2%, oral smoke-free products up 23.8%, and e-vapor products surging by 124%. The company’s total smoke-free net revenues exceeded $4 billion for the quarter.

The following chart illustrates the strong volume growth across product categories:

ZYN nicotine pouches continue to show exceptional momentum, particularly in the U.S. market. Shipment volumes reached 190.2 million cans in Q2 2025, representing a 41% increase compared to the prior year. International nicotine pouch volumes grew even faster at 65% year-over-year, and an impressive 179% when excluding the Nordic markets.

The following data highlights the remarkable growth trajectory of ZYN and VEEV:

VEEV, the company’s e-vapor product, has shown consistent quarter-over-quarter growth, with shipment volumes more than doubling year-over-year to 858 million equivalent units in Q2 2025.

Regional Performance

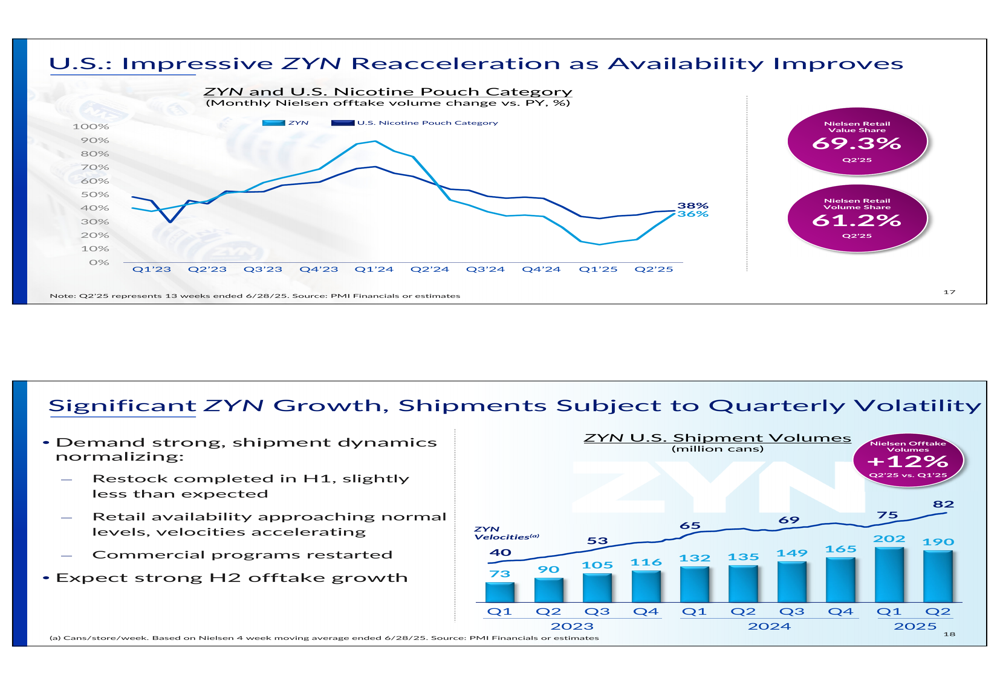

In Europe, PMI’s smoke-free product portfolio demonstrated strong performance, with combined IQOS, ZYN, and VEEV shipment growth of 13.5% in Q2 2025. IQOS adjusted in-market sales grew 9.1% in Q2, while ZYN shipments increased 31% and VEEV shipments more than doubled with 115% growth.

The following regional performance data illustrates this growth:

In Japan, a key market for heated tobacco products, PMI continues to gain market share. The heated tobacco category now represents 48% of the total tobacco market, up 3 percentage points year-over-year, with PMI’s heated tobacco unit share reaching 31.7%, an increase of 2.3 percentage points.

The U.S. market remains a significant growth opportunity for ZYN, with Nielsen data showing 38% year-over-year growth in Q2 2025. ZYN maintains a dominant position in the U.S. nicotine pouch category with a 69.3% retail value share and 61.2% retail volume share.

The following chart demonstrates ZYN’s continued growth trajectory in the U.S. market:

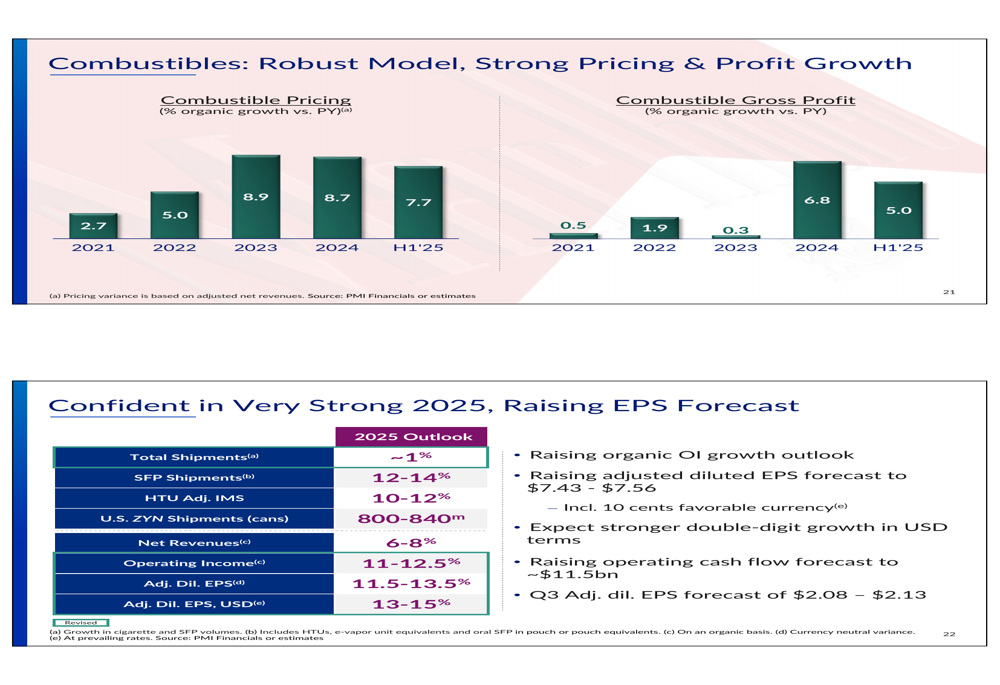

Combustible Business Resilience

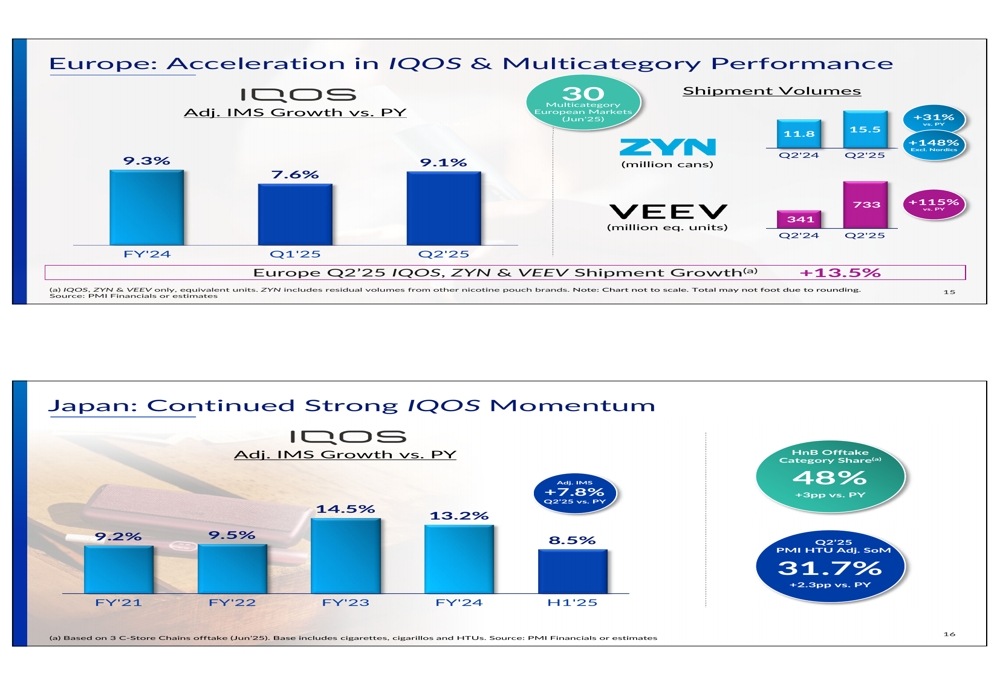

While PMI continues its transition to smoke-free products, its combustible cigarette business remains resilient and continues to generate significant cash flow. Combustible pricing grew 7.7% organically in the first half of 2025, driving a 5.0% increase in combustible gross profit.

The following data shows the consistent pricing power in the combustible business:

This pricing power has enabled PMI to offset volume declines in cigarettes, which were down 1.5% in Q2 2025, while continuing to invest in its smoke-free product portfolio.

Forward-Looking Statements

Based on its strong first-half performance, PMI has raised its full-year 2025 adjusted diluted EPS growth forecast to 13-15% in USD terms, up from the previous guidance of 11.5-13.5% provided after Q1 results.

For the full year 2025, the company expects:

- Total (EPA:TTEF) shipment volume growth of approximately 1%

- Smoke-free product shipment growth of 12-14%

- Heated tobacco unit adjusted in-market sales growth of 10-12%

- U.S. ZYN shipments of 800-840 million cans

- Net revenue growth of 6-8% organically

- Operating income growth of 11-12.5% organically

The company’s ability to deliver consistent, best-in-class growth compared to consumer packaged goods peers underscores the success of its smoke-free transformation strategy and its strong execution across markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.