How are energy investors positioned?

Introduction & Market Context

Philippine Seven Corporation (SEVN), the exclusive operator of 7-Eleven convenience stores in the Philippines, presented its Q1 2025 investor briefing on May 20, highlighting a period of mixed financial performance. The company reported revenue growth despite facing headwinds in same-store sales, while continuing its aggressive store expansion strategy.

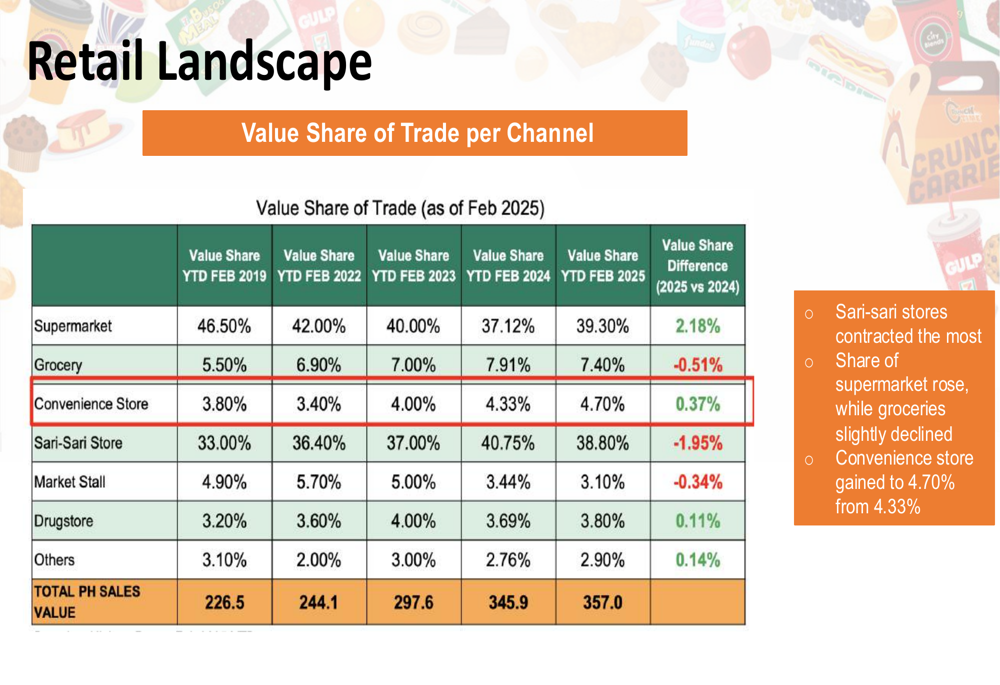

The company operates within a shifting retail landscape in the Philippines, where convenience stores have steadily increased their market share over the past six years. According to the presentation, the convenience store channel’s value share of trade has grown from 3.80% in 2019 to 4.70% in 2025, while traditional supermarkets have seen their share decline from 46.50% to 39.30% during the same period.

As shown in the following retail landscape analysis, Sari-Sari stores have significantly increased their market share to 38.80%, representing the most direct competition to 7-Eleven’s convenience model:

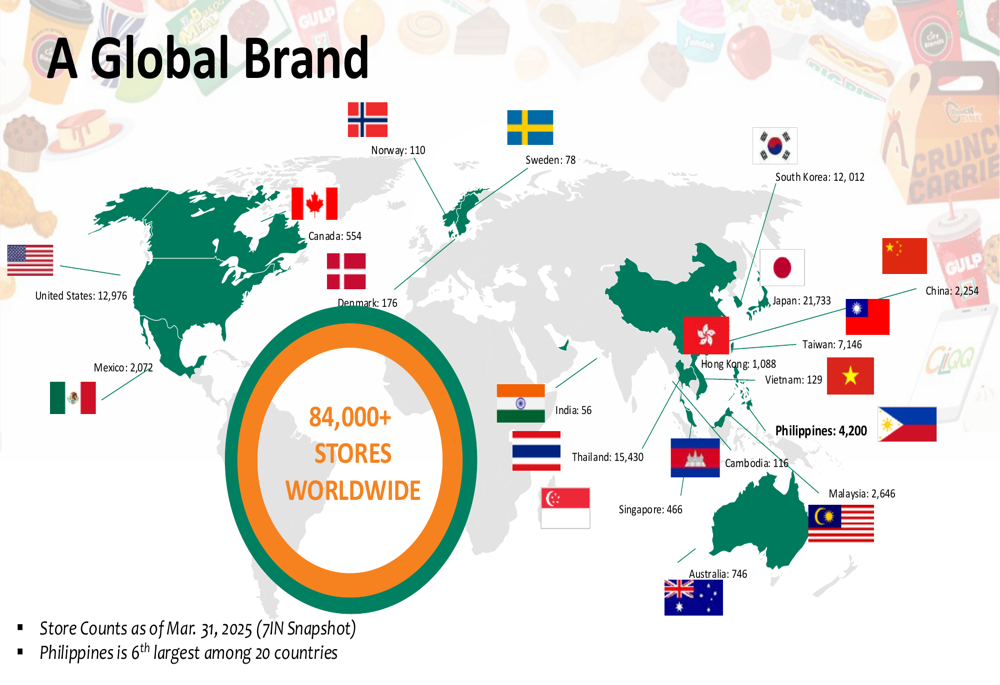

On the global stage, 7-Eleven maintains a substantial presence with over 84,000 stores worldwide. The Philippines ranks as the 6th largest market among 20 countries with 4,200 stores as of March 31, 2025, behind Japan (21,733), Thailand (15,430), the United States (12,976), South Korea (12,012), and Taiwan (7,146).

The following map illustrates 7-Eleven’s global footprint:

Quarterly Performance Highlights

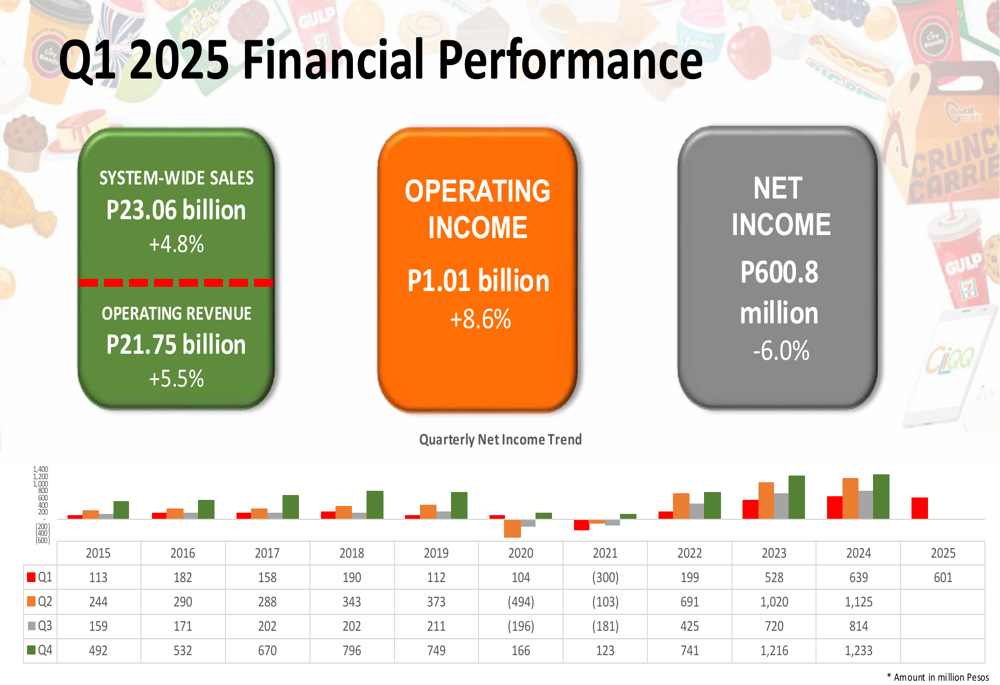

Philippine Seven reported mixed financial results for Q1 2025, with system-wide sales reaching P23.06 billion, a 4.8% increase year-over-year. Operating revenue grew by 5.5% to P21.75 billion, while operating income rose 8.6% to P1.01 billion. However, net income declined by 6.0% to P600.8 million compared to the same period last year.

The company’s quarterly performance is illustrated in the following chart, showing the net income trend from 2015 to 2025:

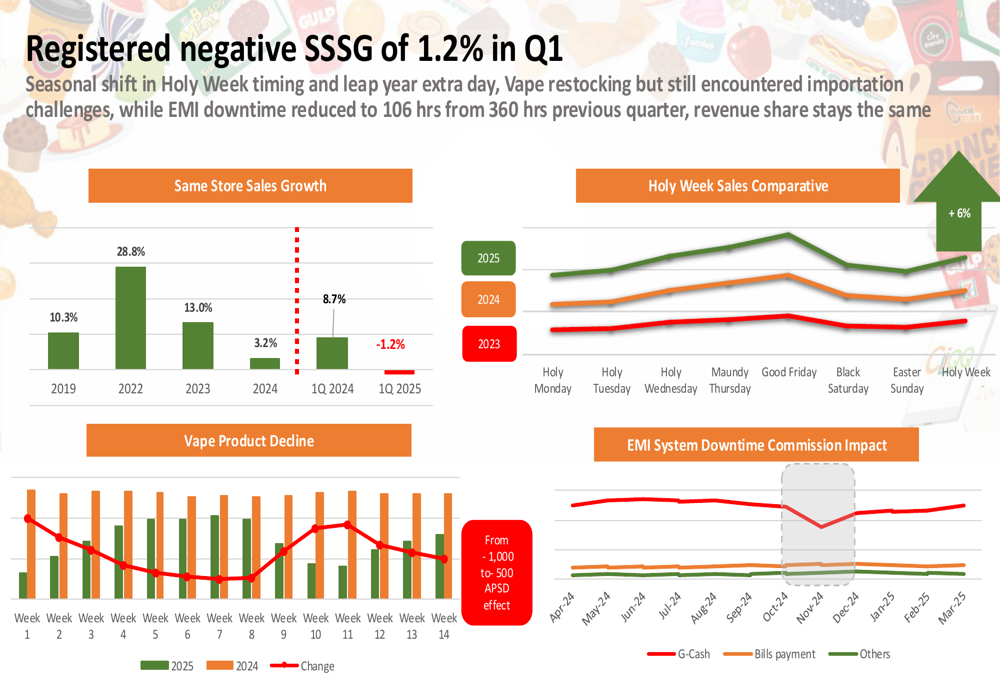

A key challenge in Q1 was the negative Same Store Sales Growth (SSSG) of -1.2%, breaking a streak of positive growth since the pandemic recovery. The company attributed this decline to several factors, including the timing of Holy Week, the impact of an extra day in February due to the leap year, and challenges with vape product importation.

The following chart details the sales performance analysis and factors affecting SSSG:

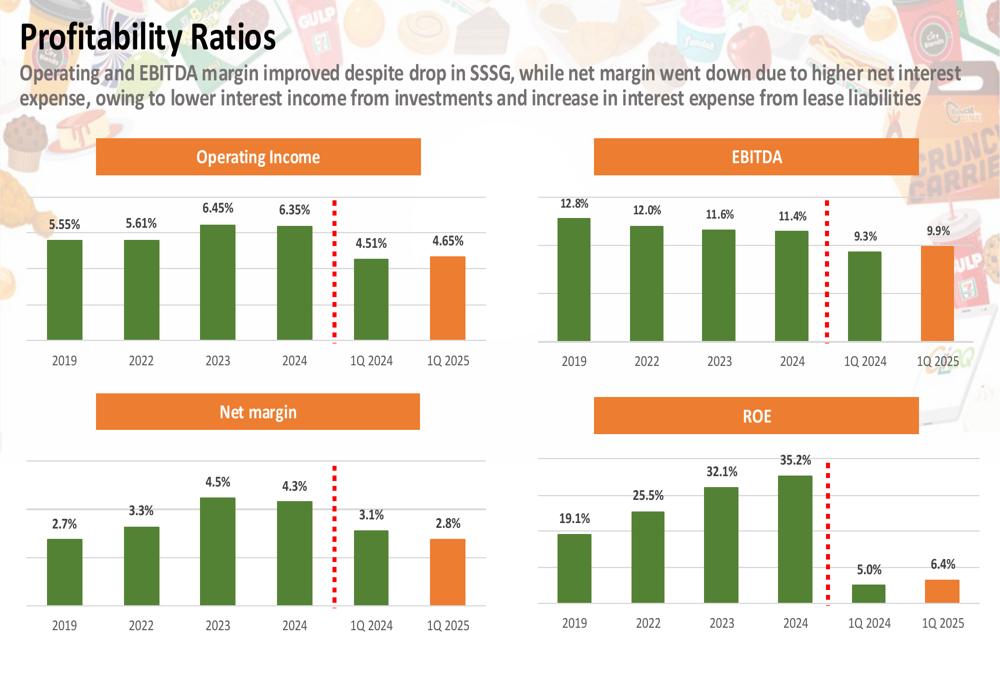

Despite these challenges, Philippine Seven maintained healthy profitability ratios. Operating margin improved to 4.65% and EBITDA margin reached 9.9% in Q1 2025, though net margin decreased to 2.8% due to higher net interest expenses. Return on equity (ROE) stood at 6.4%.

The profitability trends are illustrated in this chart:

Store Expansion Strategy

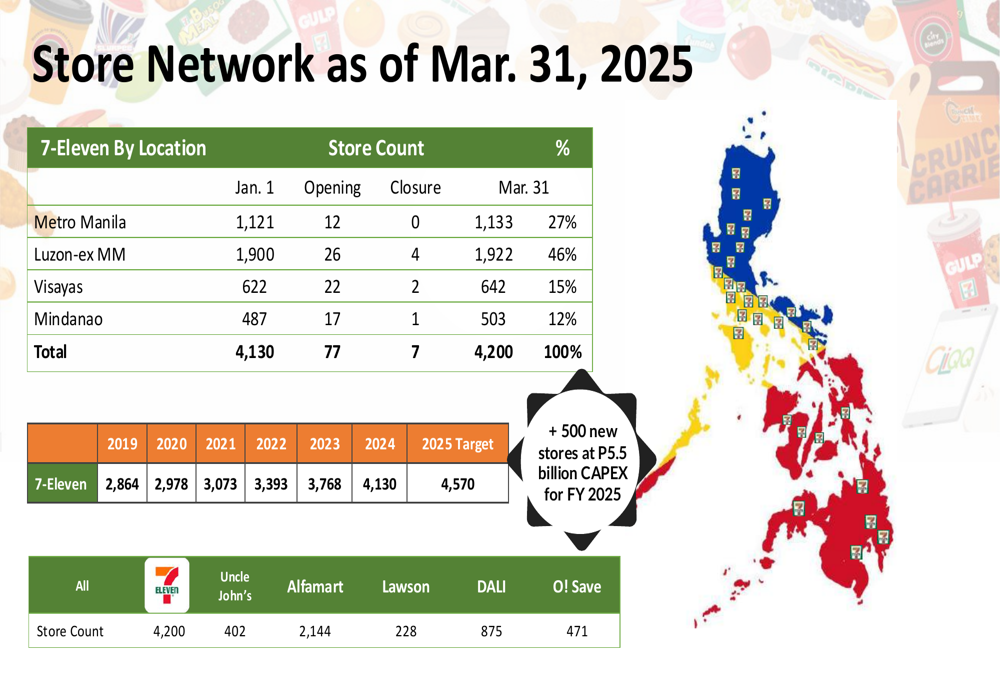

Philippine Seven continues its aggressive expansion strategy, targeting 4,570 stores by the end of 2025 with a planned capital expenditure of P5.5 billion. As of March 31, 2025, the company operated 4,200 stores across the Philippines, with 1,133 in Metro Manila, 1,922 in Luzon (excluding Metro Manila), 642 in Visayas, and 503 in Mindanao.

During Q1 2025, the company opened 77 new stores while closing 7 underperforming locations, resulting in a net addition of 70 stores. A significant milestone was reached with the opening of the 500th store in Mindanao, demonstrating the company’s commitment to expanding beyond traditional urban centers.

The following chart shows the current store network and competitive landscape:

In terms of store ownership structure, corporate-owned stores represent 51% of the network, while franchised stores make up the remaining 49% (44% FC1 and 5% FC2 & FC3). The store locations are strategically distributed across various clusters, with residential areas (39%) and transit locations (23%) representing the largest segments.

Financial Position and Outlook

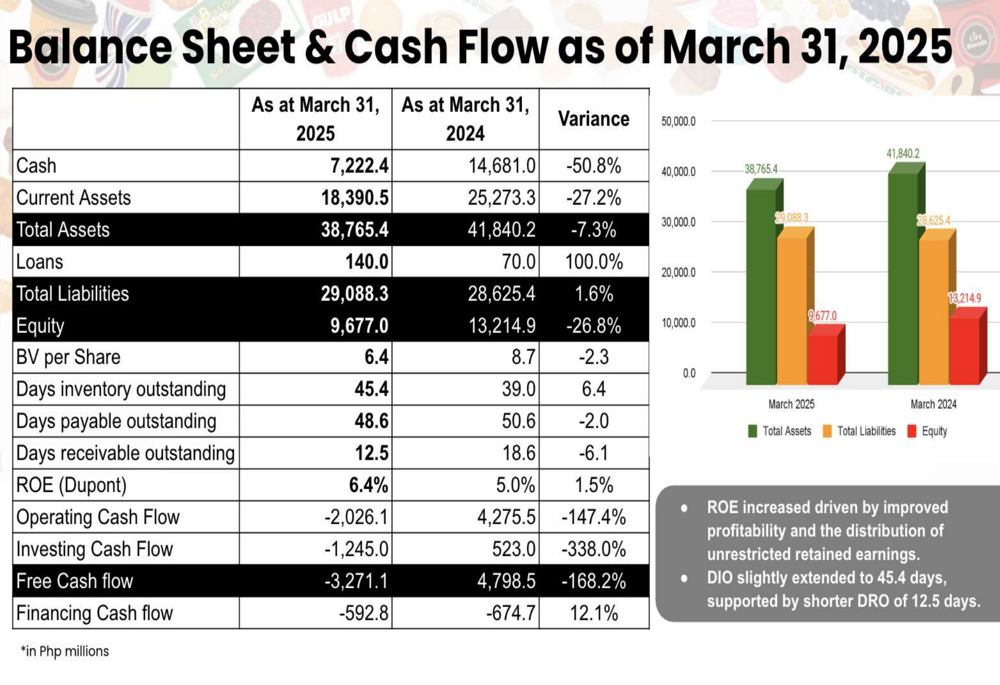

Philippine Seven’s balance sheet showed some concerning trends, with cash decreasing significantly from P14,681.0 million in March 2024 to P7,222.4 million in March 2025. Total (EPA:TTEF) assets decreased by 7.3% year-over-year to P38,765.4 million, while total liabilities increased slightly to P29,088.3 million. Equity decreased by 26.8% to P9,677.0 million.

The company reported negative operating cash flow of P2,026.1 million and negative investing cash flow of P1,245.0 million, resulting in negative free cash flow of P3,271.1 million. Days inventory outstanding slightly increased to 45.4 days, while days payable outstanding stood at 48.6 days.

The balance sheet summary is shown in the following chart:

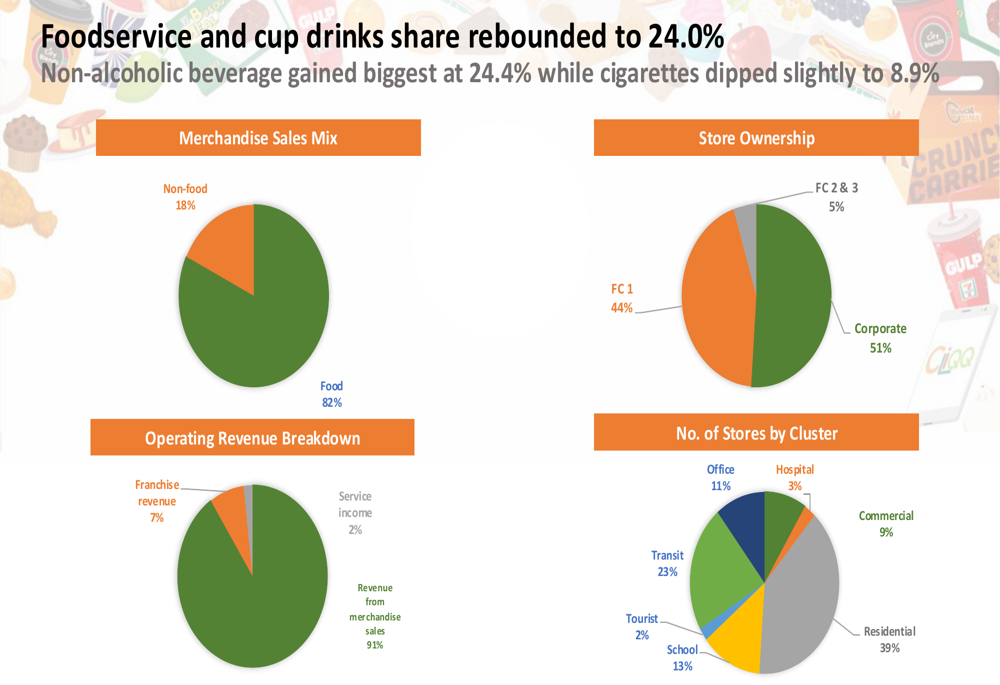

Despite these cash flow challenges, Philippine Seven’s merchandise mix remains heavily weighted toward food products, which account for 82% of sales, with non-food items making up the remaining 18%. Revenue from merchandise sales contributes 91% of total revenue, with franchise revenue at 7% and service income at 2%.

Competitive Industry Position

Philippine Seven faces competition from various convenience store chains in the Philippines, including All Day, Uncle John’s, Alfamart, Lawson, DALI, and O! Save. However, with 4,200 stores, 7-Eleven maintains the largest network among convenience store operators in the country.

The company has received several global recognitions, including the "Industry Leader of the Year Award" from Asian Convenience and being awarded "Highest Same Store Sales Growth in 2018." Additionally, Victor Paterno, the company’s leader, was named 2023-24 NACS Chairman, further cementing Philippine Seven’s position as a leader in the convenience store industry.

Looking ahead, Philippine Seven faces the dual challenge of maintaining profitability while funding its ambitious expansion plans amid cash flow pressures. The company’s ability to reverse the negative same-store sales trend while continuing to open new stores will be crucial for its performance throughout the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.