JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Philips ( AMS (VIE:AMS2):PHIA) presented its first quarter 2025 results on May 6, revealing a challenging start to the year with comparable sales declining 2% amid significant regional disparities. The healthcare technology company maintained its full-year sales growth outlook but revised down its margin and cash flow guidance, primarily due to anticipated tariff impacts.

The company’s stock closed at €22.55 on May 5, down 0.66% ahead of the earnings presentation, and has been trading in a 52-week range of €19.54 to €30.12.

CEO Roy Jakobs and CFO Charlotte Hanneman highlighted the company’s resilience in most markets, with strong performance in North America offsetting a double-digit decline in China. The results come after Philips paid a €1 billion settlement related to the Respironics recall while maintaining its leverage ratio at 2.2x.

Quarterly Performance Highlights

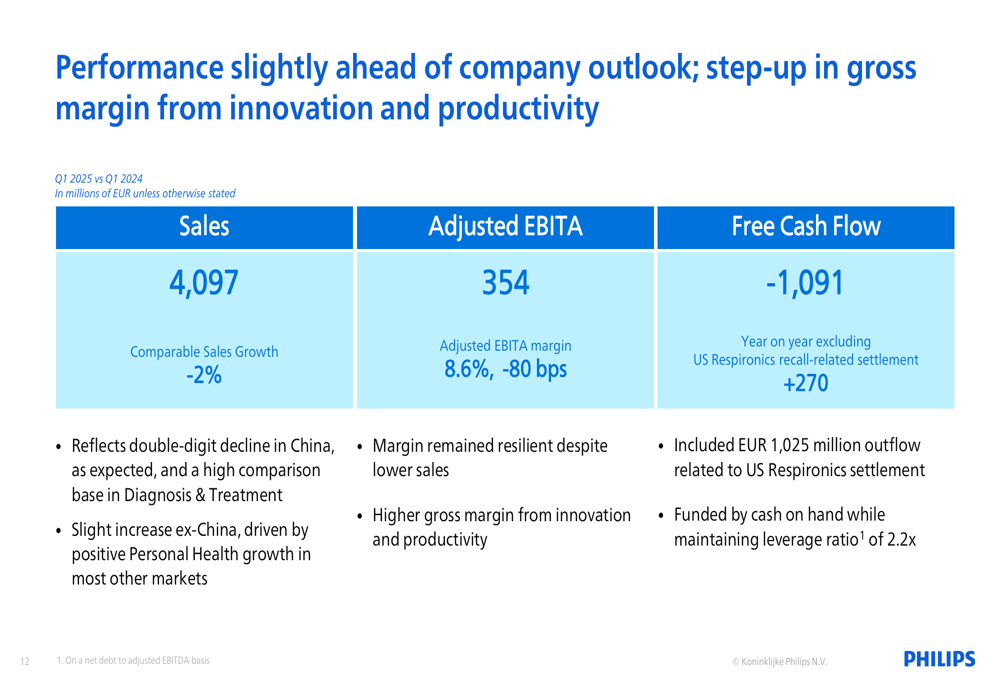

Philips reported Q1 2025 sales of €4,097 million with a comparable sales decline of 2%. The adjusted EBITA reached €354 million, resulting in an 8.6% margin, down 80 basis points year-over-year. Free cash flow was negative at €1,091 million, primarily due to the Respironics settlement payment, but showed a €270 million improvement year-on-year when excluding this one-time outflow.

As shown in the following overall financial performance summary:

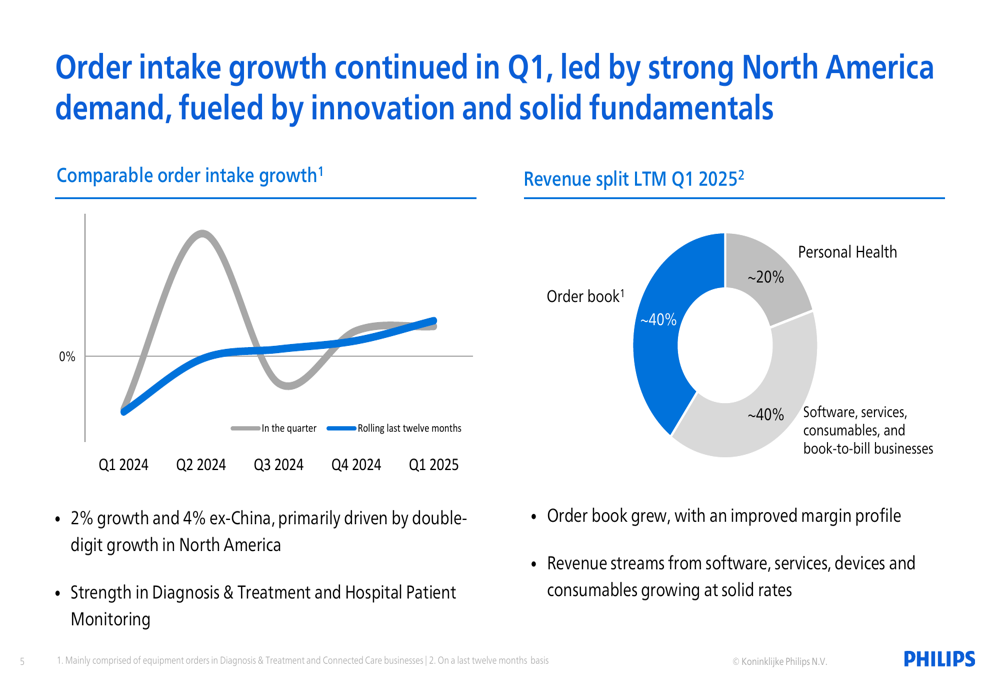

Order intake showed growth, primarily driven by strength in North America, which helped offset the significant decline in China. The company’s order book grew with an improved margin profile, while revenue streams from software, services, devices, and consumables continued to grow at solid rates.

The revenue split for the last twelve months ending Q1 2025 demonstrates the company’s diversified business model:

Segment Performance

The Diagnosis & Treatment segment reported sales of €1,965 million, representing a 4% comparable sales decline compared to Q1 2024. Despite lower sales, the adjusted EBITA margin improved to 9.5% from 9.2% a year earlier. The segment’s performance was marked by strong results in Image Guided Therapy, which were more than offset by declines in Precision Diagnosis, particularly due to weakness in China.

Connected Care delivered flat comparable sales growth with revenues of €1,182 million. However, the segment’s adjusted EBITA margin decreased significantly to 3.5% from 6.4% in Q1 2024, mainly due to mix and cost phasing, partially offset by productivity measures and innovation. Hospital Patient Monitoring sales grew, driven by higher installations in North America and Europe.

The Personal Health segment showed resilience with sales of €811 million and 1% comparable sales growth. The adjusted EBITA margin remained stable at 15.2%. Double-digit growth in Europe and growth markets, along with slight growth in the US, largely offset the expected decline in China. Consumer sentiment remained strong in Europe and growth markets.

Strategic Initiatives

Philips continues to focus on AI-driven innovations, which the company reports are fueling 50% of its sales. Recent product launches include Visual Patient Avatar, SmartSpeed Precise, Elevate Ultrasound, and several other AI-enabled diagnostic and treatment solutions.

The following image showcases some of these recently launched AI innovations:

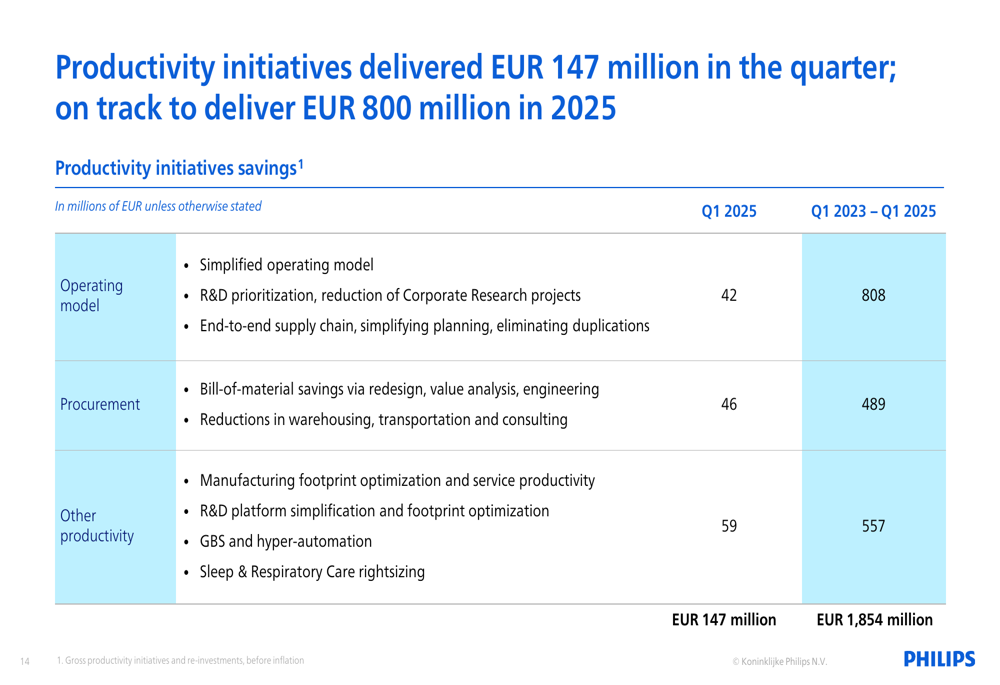

The company also reported solid progress on its execution priorities, including strengthening patient safety and quality culture, improving supply chain quality and velocity, and simplifying its operating model. Productivity initiatives delivered €147 million in savings during Q1 2025, contributing to a total of €1,854 million since Q1 2023.

Philips detailed its productivity savings across different initiatives:

Revised 2025 Outlook

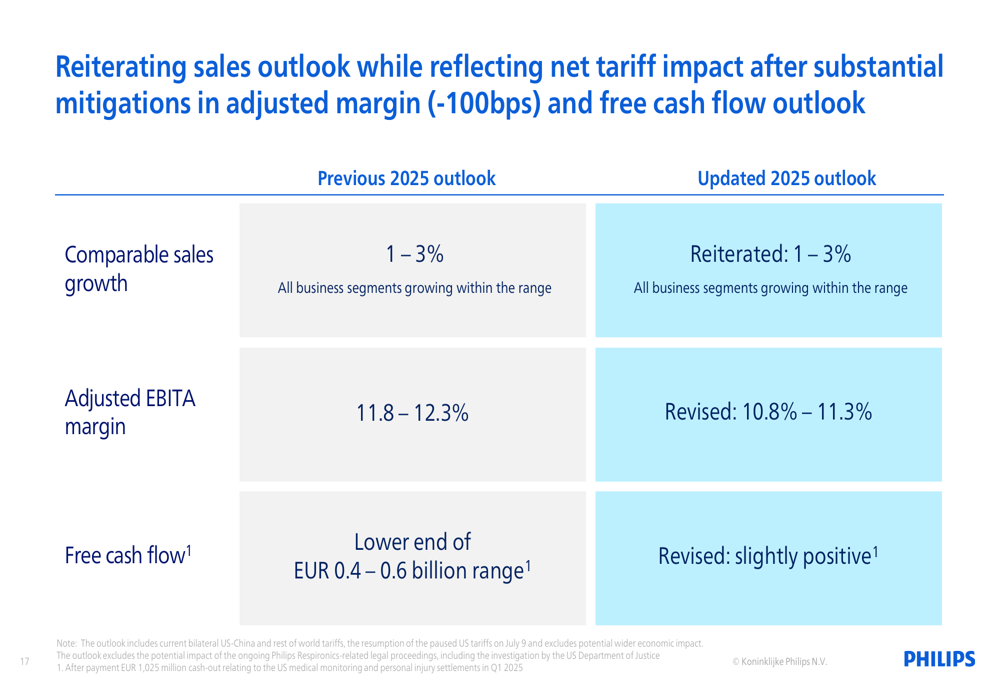

In response to anticipated tariff impacts, Philips has revised its 2025 financial outlook. While the company maintained its comparable sales growth forecast of 1-3%, it reduced its adjusted EBITA margin guidance to 10.8-11.3% from the previous 11.8-12.3%. Free cash flow expectations were also lowered to "slightly positive" from the "lower end of €0.4-0.6 billion range."

The company estimates a net tariff impact of €250-300 million after substantial mitigations. Philips outlined several mitigation strategies, including supplier management and network optimization, inventory management, accelerated regionalization, pursuing exemptions, cost management, select pricing actions, and advocacy efforts.

The updated financial outlook compared to previous guidance is illustrated here:

Financial Analysis

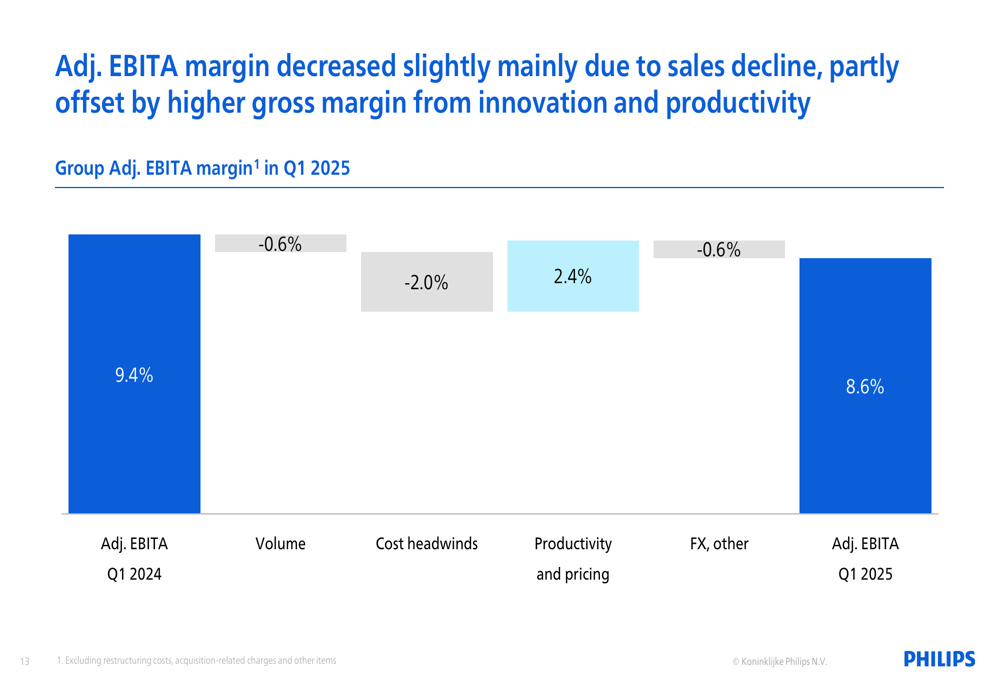

The adjusted EBITA margin decline of 80 basis points year-over-year to 8.6% was driven by several factors. Volume impact (-0.6%), cost headwinds (-2.0%), and foreign exchange effects (-0.6%) were partially offset by productivity and pricing improvements (+2.4%).

This breakdown of factors affecting the EBITA margin provides insight into the company’s operational challenges and responses:

Despite the challenges, Philips maintained a solid gross margin, supported by innovation value and productivity measures. The company’s working capital management and debt profile remain stable, with an average tenor of long-term debt at 6.2 years and €1 billion in committed credit facilities.

The company’s regional performance varied significantly, with North America showing solid demand, Europe experiencing slight improvement, China facing subdued demand due to anti-corruption programs and regulatory changes, and Rest of World markets demonstrating strong performance driven by infrastructure investments and digitalization.

As Philips navigates these mixed market conditions, its focus on productivity initiatives, AI innovations, and strategic mitigations will be crucial to achieving its revised 2025 financial targets while managing the impact of tariffs and regional challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.