BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

Royal Philips ( AMS (VIE:AMS2):PHIA) presented its second quarter 2025 results on July 29, showing a return to sales growth and significant margin improvement after a challenging first quarter. The company’s stock closed at €22.04 on July 28, down 0.5% ahead of the earnings presentation.

The presentation, delivered by CEO Roy Jakobs and CFO Charlotte Hanneman, highlighted improved performance across key metrics and an upgraded outlook for the full year, despite ongoing challenges in certain segments and regions.

Quarterly Performance Highlights

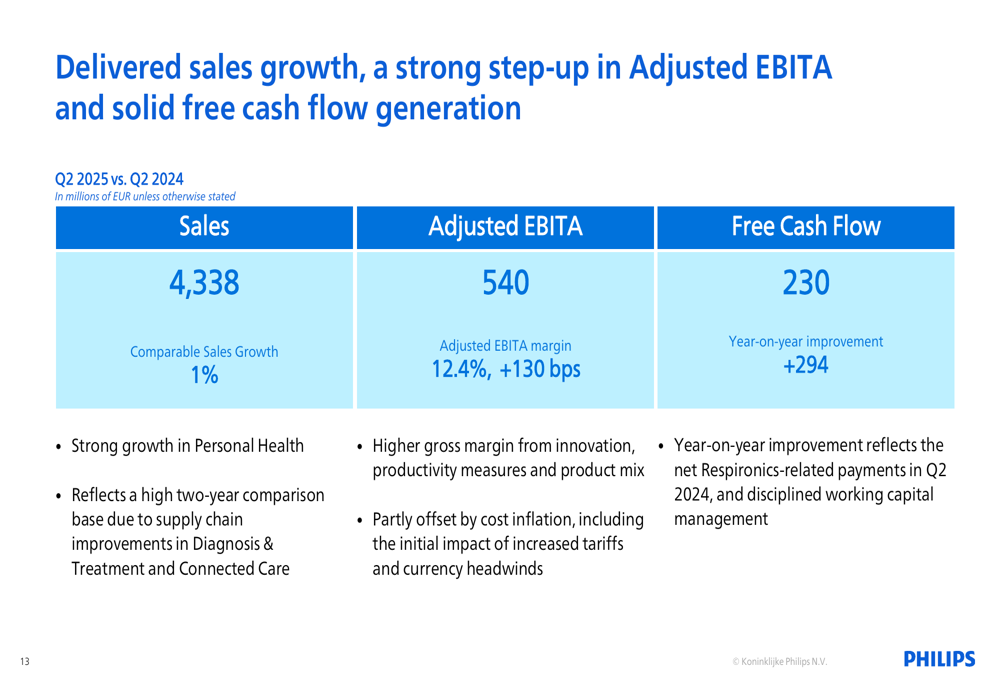

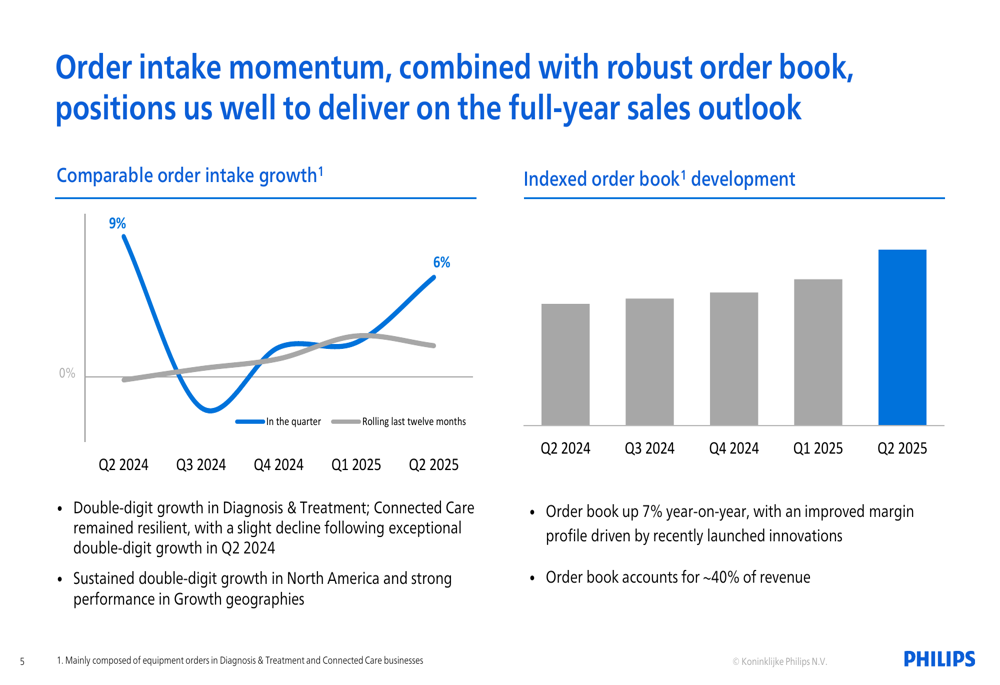

Philips reported Q2 2025 sales of €4,338 million, representing 1% comparable growth year-over-year, a notable improvement from the 2% decline seen in Q1. The company’s order intake increased by 6%, with the order book growing 7% compared to the previous year, now accounting for approximately 40% of revenue.

As shown in the following financial summary:

Adjusted EBITA reached €540 million, with the margin expanding 130 basis points to 12.4% compared to Q2 2024. Free cash flow showed a dramatic improvement to €230 million, representing a €294 million year-on-year increase. This recovery follows the significant cash outflow in Q1 2025 that was impacted by a €1 billion settlement related to the Respironics litigation.

The company’s order intake growth has been particularly strong in the Diagnosis & Treatment segment, which saw double-digit growth:

Segment Performance Analysis

Performance varied significantly across Philips’ three main business segments, with Personal Health emerging as the clear growth driver.

The Personal Health segment delivered 6% comparable sales growth, reaching €862 million in Q2 2025, with an adjusted EBITA margin of 15.2%. The company attributed this strong performance to innovation-led growth across most geographies, showcasing products like the i9000 Shaver, OneBlade 360, and AI-powered Avent baby monitors.

The following image highlights Philips’ innovations in the Personal Health segment:

In contrast, the Diagnosis & Treatment segment experienced a 1% sales decline to €2,084 million, which the company attributed to a high two-year comparison base. Despite this, the segment maintained a solid adjusted EBITA margin of 13.5%, driven by improved gross margins.

Similarly, the Connected Care segment saw a 1% sales decrease to €1,272 million, with low single-digit growth in Enterprise Informatics offset by a decline in Monitoring. The segment posted an adjusted EBITA margin of 10.4%.

Productivity and Margin Improvement

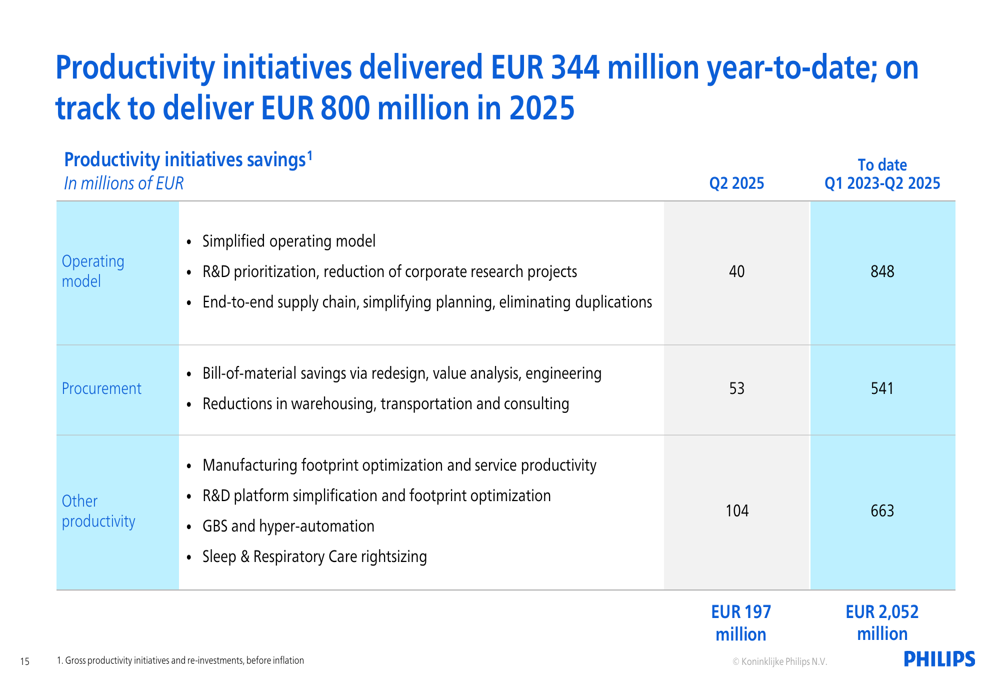

A key driver of Philips’ improved profitability has been its productivity initiatives, which delivered €344 million in savings year-to-date. Since Q1 2023, these initiatives have generated cumulative savings of €2,052 million.

The following chart breaks down the productivity savings by category:

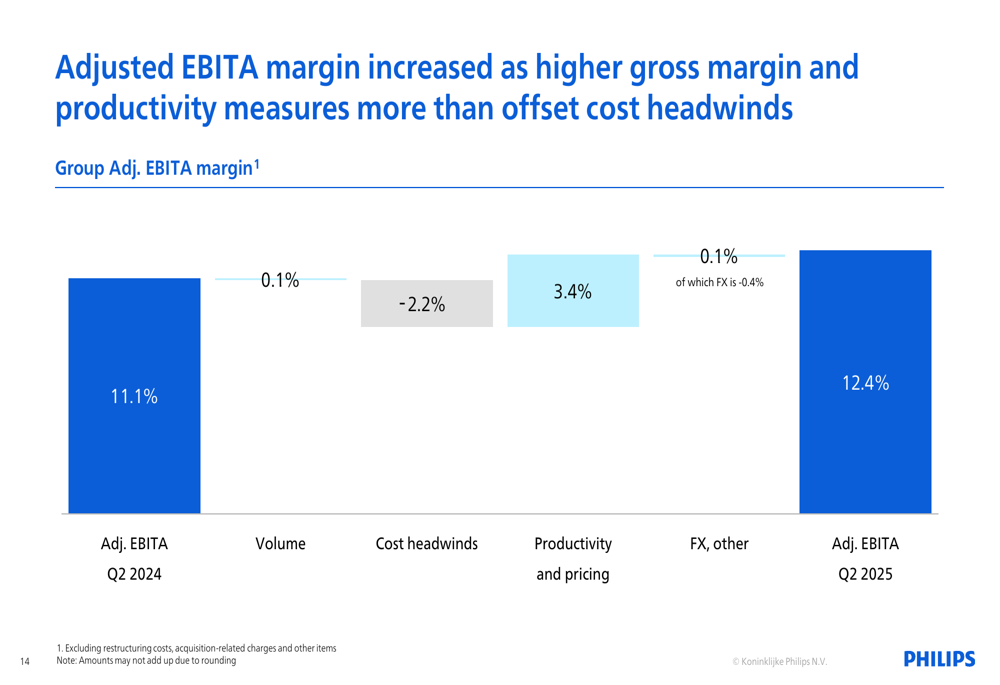

The company’s adjusted EBITA margin improvement of 130 basis points (from 11.1% in Q2 2024 to 12.4% in Q2 2025) was primarily driven by productivity and pricing improvements, which contributed 3.4 percentage points, more than offsetting cost headwinds of 2.2 percentage points:

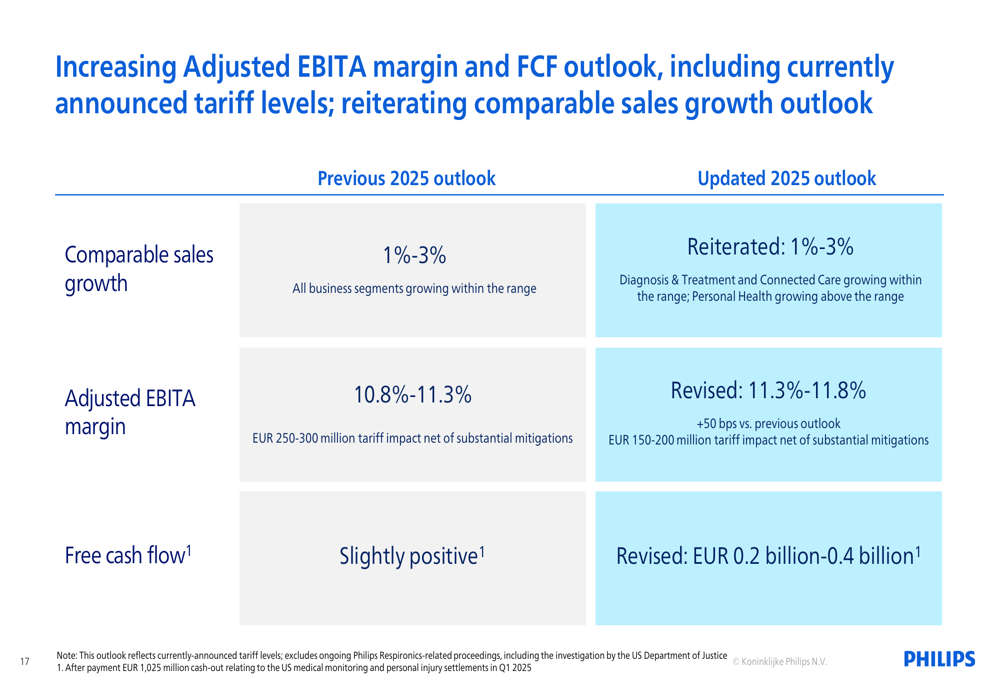

Updated 2025 Outlook

Based on the stronger-than-expected performance in Q2, Philips has upgraded its full-year 2025 outlook. While the company maintained its comparable sales growth projection of 1-3%, it raised its adjusted EBITA margin target by 50 basis points to 11.3-11.8%.

Additionally, Philips significantly improved its free cash flow guidance from "slightly positive" to €0.2-0.4 billion. The company also reduced its expected tariff impact from €250-300 million to €150-200 million.

The following slide details these outlook changes:

This updated outlook represents a notable improvement from the guidance provided after Q1 2025, when the company projected an adjusted EBITA margin between 10.8% and 11.3%.

Market Conditions and Regional Performance

Philips provided insights into market conditions across different regions, noting varied performance. North American health systems remain solid, with productivity and consolidation as key drivers. Europe shows slight improvement, while Greater China demonstrates strong underlying demand despite being influenced by anti-corruption programs and regulatory changes.

The Personal Health segment is performing particularly well in Europe and Rest of World markets, while remaining stable in North America and subdued in Greater China, reflecting broader consumer sentiment trends in these regions.

Conclusion

Philips’ Q2 2025 results indicate a recovery from the challenges faced in the first quarter, with a return to sales growth and significant margin improvement. The company’s focus on productivity initiatives and innovation-led growth, particularly in the Personal Health segment, appears to be yielding results.

The upgraded outlook for adjusted EBITA margin and free cash flow suggests growing confidence in the company’s ability to navigate ongoing market challenges. However, the varied performance across segments and regions highlights the uneven nature of the recovery, with Diagnosis & Treatment and Connected Care segments still facing headwinds.

As Philips continues to implement its strategic initiatives and productivity measures, investors will be watching closely to see if the positive momentum can be maintained through the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.