Stock market today: S&P 500 drops for fifth day as focus shifts to Powell’s speech

Introduction & Market Context

Phillips 66 (NYSE:PSX) released its second-quarter 2025 earnings presentation on July 25, showcasing a significant improvement in financial performance driven primarily by a strong rebound in its refining segment. The company reported adjusted earnings of $973 million, a substantial recovery from a $368 million loss in the first quarter, highlighting the cyclical nature of the refining business and the company’s operational improvements.

The presentation emphasized Phillips 66’s ability to capitalize on favorable refining market conditions while maintaining focus on its long-term strategic priorities, including cost reduction initiatives and midstream growth. However, the company’s increased debt levels and reduced cash position suggest ongoing challenges in balancing growth investments with financial discipline.

Quarterly Performance Highlights

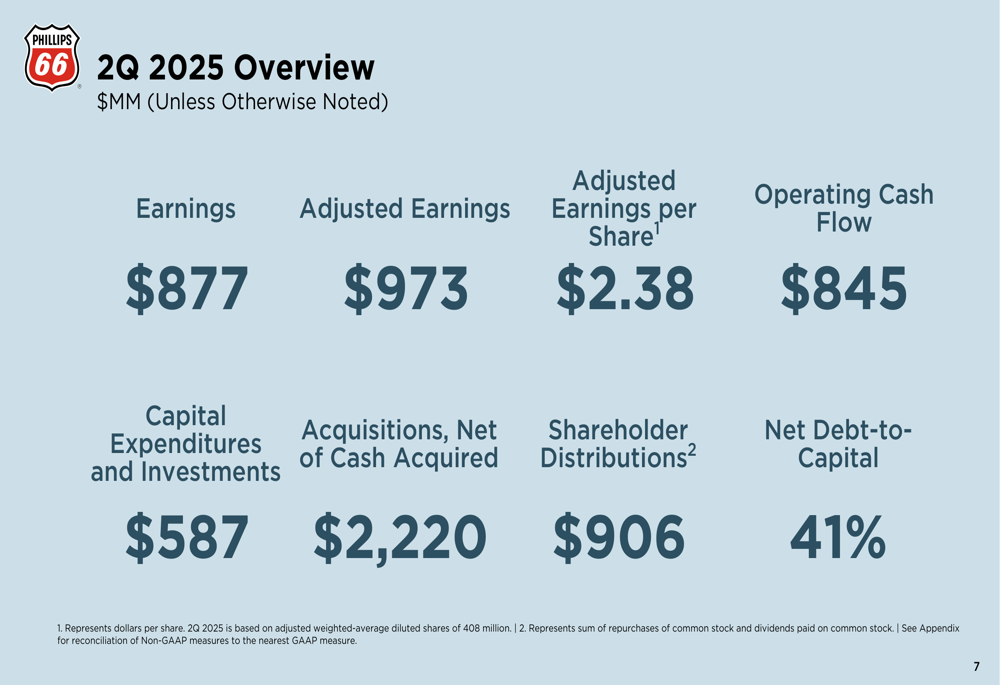

Phillips 66 reported second-quarter earnings of $877 million, with adjusted earnings of $973 million, translating to $2.38 per share based on 408 million weighted-average diluted shares. The company generated $845 million in operating cash flow while allocating $587 million to capital expenditures and investments.

As shown in the following financial overview slide, Phillips 66 returned $906 million to shareholders through dividends and share repurchases, demonstrating its commitment to shareholder returns despite significant acquisition spending of $2.22 billion during the quarter:

The company’s net debt-to-capital ratio stood at 41% at quarter-end, reflecting increased leverage compared to previous periods. This metric remains significantly above the company’s long-term target of below 30%, indicating potential financial flexibility challenges ahead.

Segment Analysis

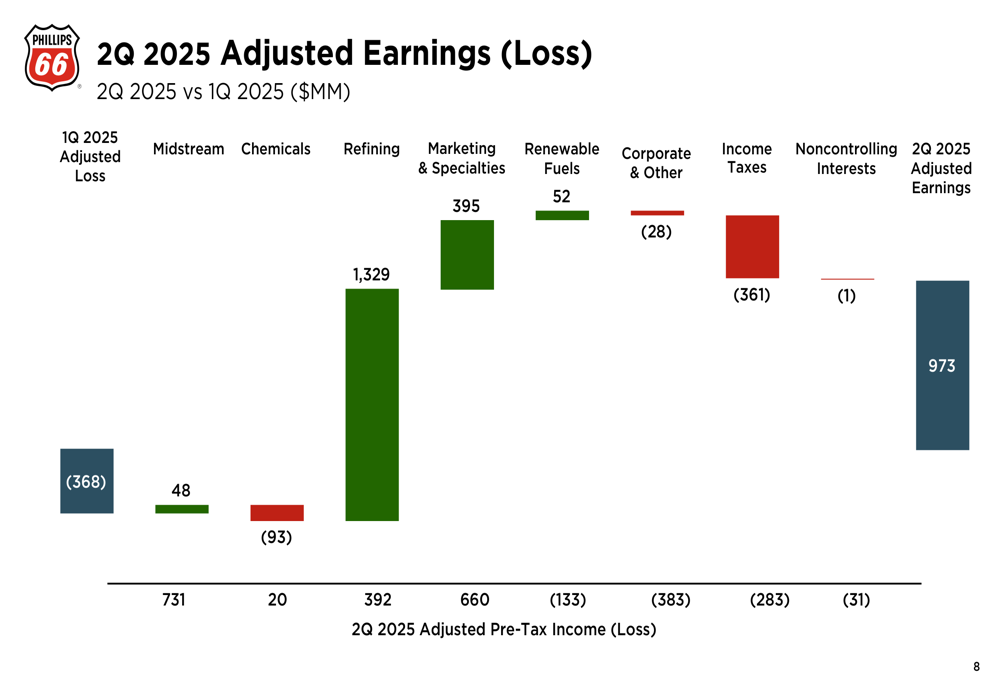

Phillips 66’s second-quarter performance showed dramatic variations across business segments, with Refining emerging as the clear standout contributor to the company’s profitability turnaround.

As illustrated in the following segment breakdown, Refining delivered $1,329 million in adjusted earnings, compared to just $392 million in the first quarter, while other segments showed mixed results:

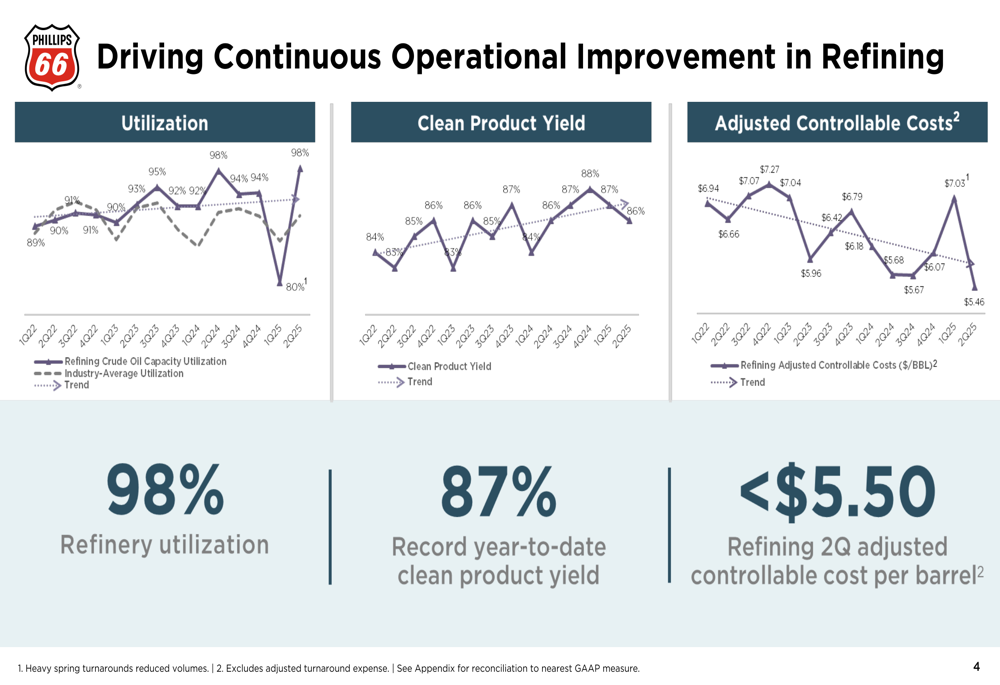

The Refining segment’s strong performance was driven by improved utilization rates, higher margins, and lower costs. The company achieved 98% crude utilization, 86% clean product yield, and 99% market capture during the quarter, demonstrating operational excellence in this core business.

As shown in the following operational metrics chart, Phillips 66 has consistently outperformed industry averages in refinery utilization while driving down controllable costs:

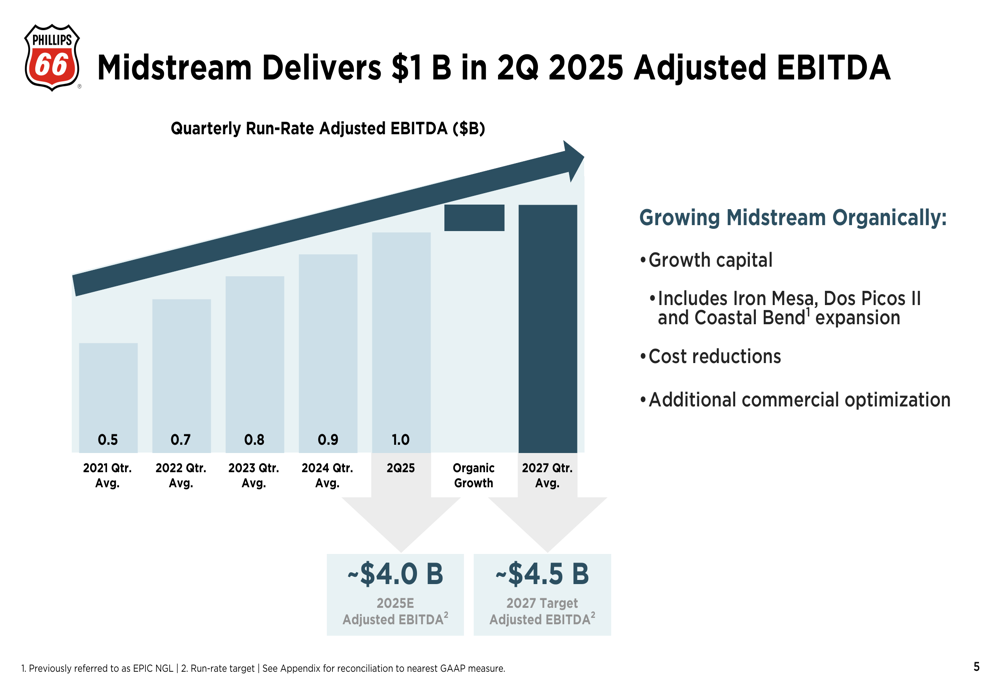

The Midstream segment contributed $20 million to adjusted earnings, a significant decrease from $731 million in the first quarter. Despite this quarterly decline, the segment delivered $1 billion in adjusted EBITDA, supporting the company’s long-term growth strategy in this area.

The following chart illustrates the Midstream segment’s growth trajectory and future targets:

The Chemicals segment reported a loss of $93 million, reversing from a $48 million profit in the previous quarter, while Marketing & Specialties earnings declined to $395 million from $660 million. Renewable Fuels showed improvement, posting a $52 million profit compared to a $133 million loss in Q1.

Cash Flow and Capital Structure

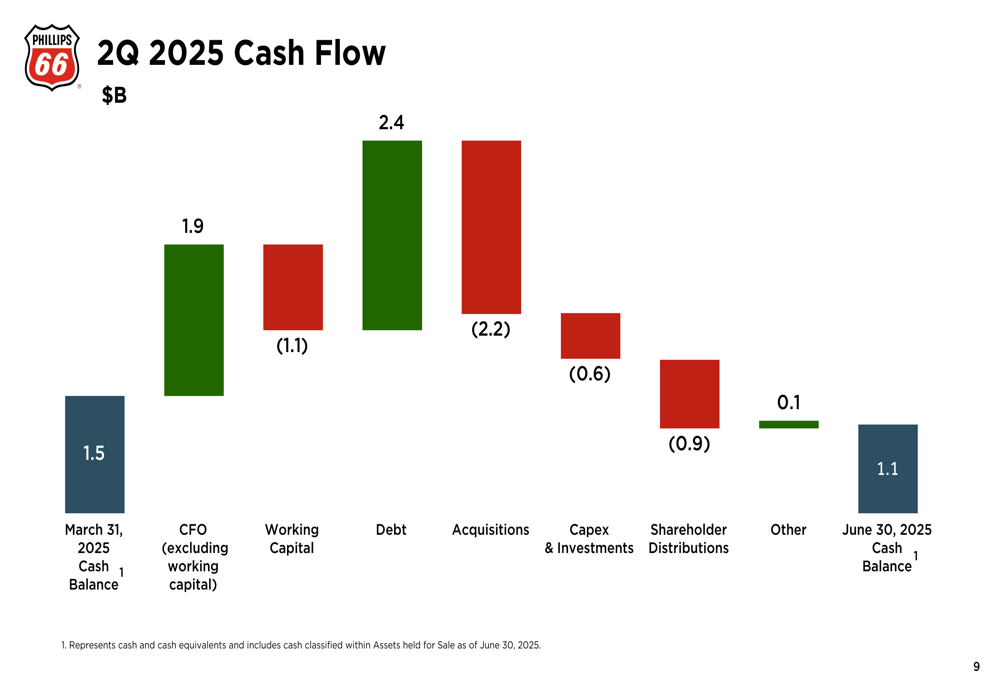

Phillips 66’s cash position decreased from $1.5 billion at the end of Q1 to $1.1 billion by June 30, 2025. This reduction was primarily driven by significant acquisition spending of $2.2 billion, partially offset by new debt issuance of $2.4 billion.

The following cash flow waterfall chart provides a comprehensive view of the quarter’s cash movements:

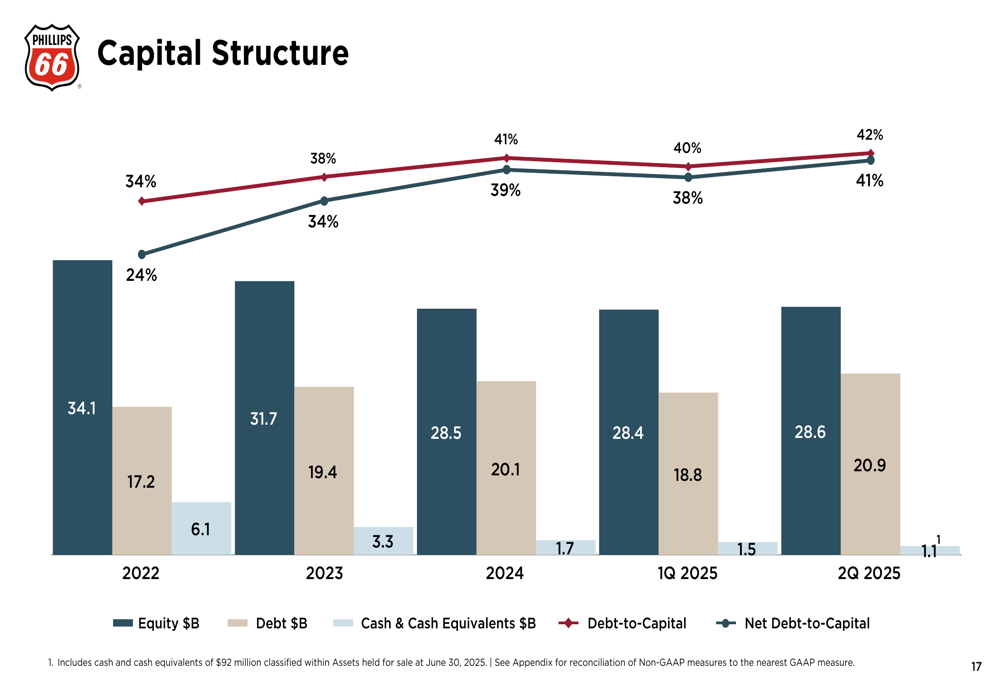

The company’s capital structure has evolved significantly over recent years, with total debt increasing to $20.9 billion in Q2 2025 from $18.8 billion in the previous quarter. This trend reflects Phillips 66’s aggressive investment strategy, particularly in acquisitions and midstream growth projects.

As illustrated in the following capital structure chart, the company’s debt-to-capital ratio has increased to 42%, with net debt-to-capital at 41%:

This leverage level represents a significant deviation from the company’s stated long-term target of below 30% net debt-to-capital, suggesting that debt reduction may become a priority in coming quarters.

Strategic Outlook and 2027 Priorities

Looking ahead to the third quarter of 2025, Phillips 66 provided guidance indicating continued operational strength. The company expects refining crude utilization in the low to mid-90% range, with global olefins and polyolefins utilization in the mid-90% range. Refining turnaround expenses are projected at $50-60 million, while Corporate & Other costs are estimated at $350-370 million.

Phillips 66 outlined its investment rationale and strategic priorities through 2027, emphasizing operational excellence, cost reduction, disciplined growth, and shareholder returns. The following slide details these strategic objectives:

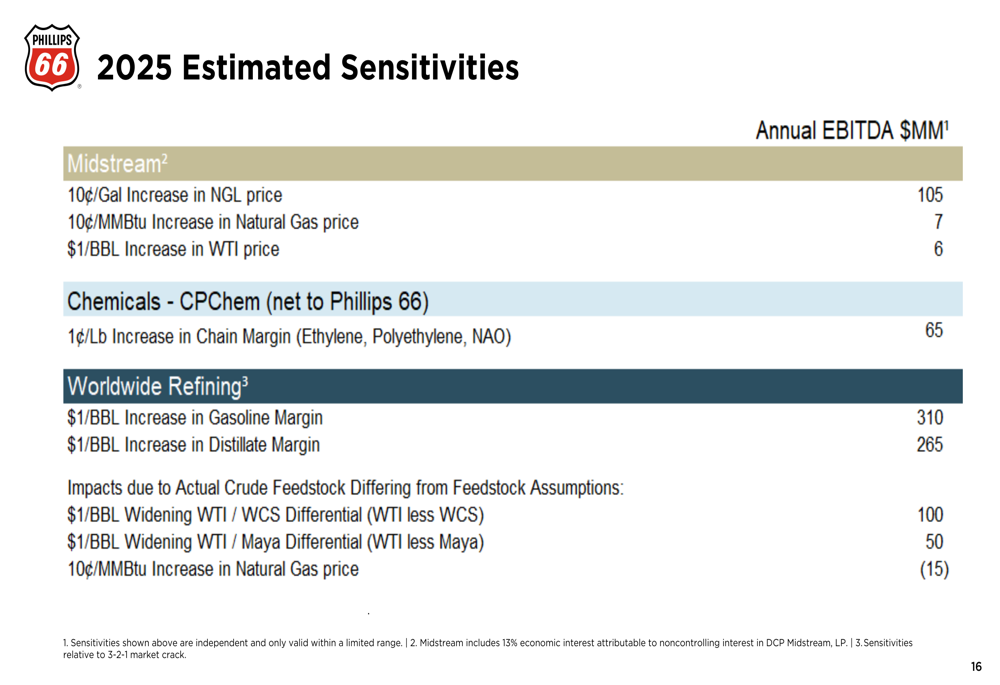

A key component of Phillips 66’s strategy involves understanding and managing market sensitivities. The company provided detailed estimates of how various market factors could impact its 2025 EBITDA, offering investors insight into potential risks and opportunities:

These sensitivities highlight the company’s significant exposure to refining margins, with a $1/BBL increase in gasoline and distillate margins potentially adding $310 million and $265 million to annual EBITDA, respectively.

Phillips 66’s presentation demonstrates a company in transition, balancing short-term operational improvements with long-term strategic initiatives while managing an elevated debt profile. The strong refining performance in Q2 2025 provided welcome relief after a challenging first quarter, but sustainable profitability will depend on continued operational excellence across all segments and disciplined execution of the company’s strategic priorities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.