Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Ping An Insurance Group presented its interim results for the first half of 2025, highlighting resilient performance across its diversified business segments despite challenging market conditions. The company reported steady growth in its core financial metrics while emphasizing its strategic pivot toward integrated health and senior care services.

The presentation, delivered by senior executives including Group CFO Fu Xin and Co-CEOs Xie Yonglin and Michael Guo, outlined how Ping An’s strategic transformation is beginning to yield tangible results, particularly in new business value growth.

Executive Summary

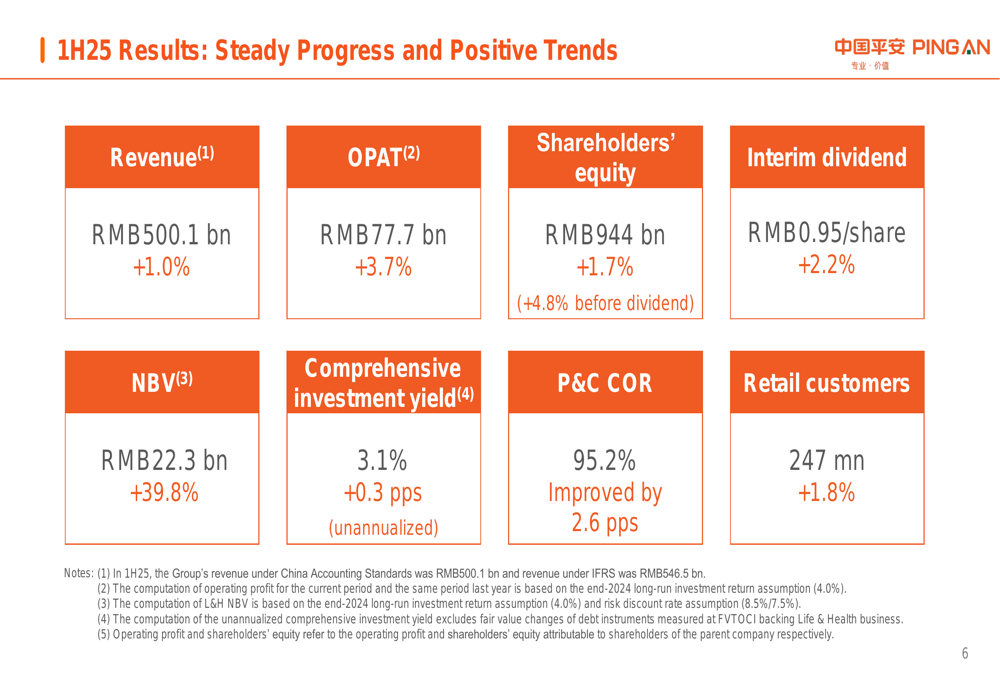

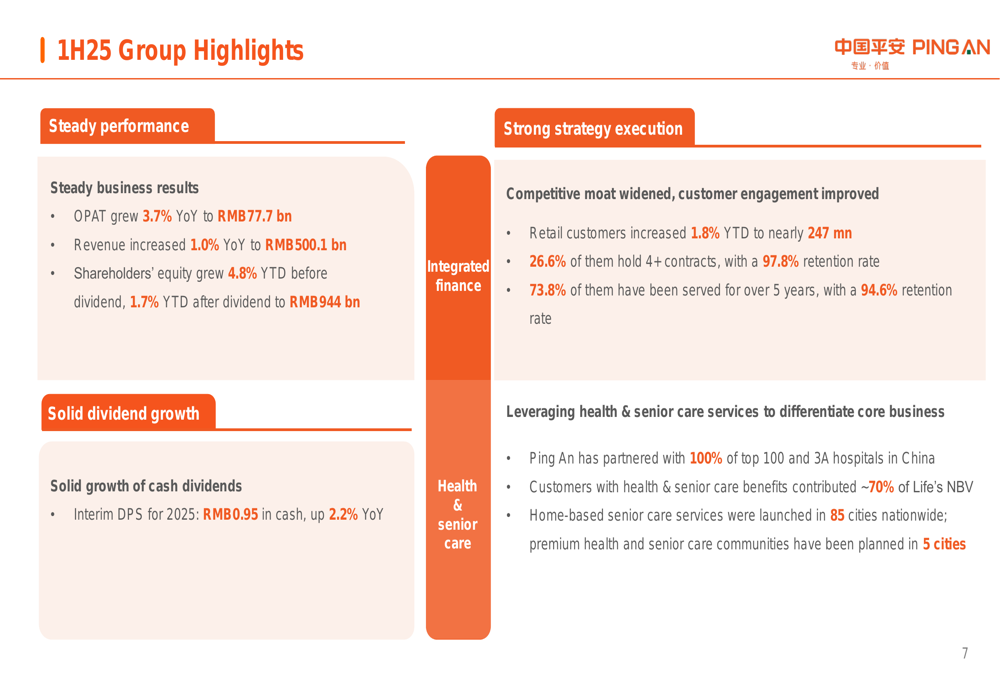

Ping An reported a 3.7% year-over-year increase in Operating Profit Attributable to shareholders (OPAT) to RMB77.7 billion for the first half of 2025, while revenue grew modestly by 1.0% to RMB500.1 billion. The standout metric was New Business Value (NBV), which surged 39.8% to RMB22.3 billion, reflecting the company’s successful pivot toward higher-margin products and distribution channels.

As shown in the following comprehensive results summary, the company maintained growth across most key performance indicators:

Shareholders’ equity increased by 1.7% year-to-date (4.8% before dividend) to RMB944 billion, and the company announced an interim dividend of RMB0.95 per share, up 2.2% year-over-year, demonstrating its commitment to shareholder returns despite market headwinds.

Strategic Initiatives

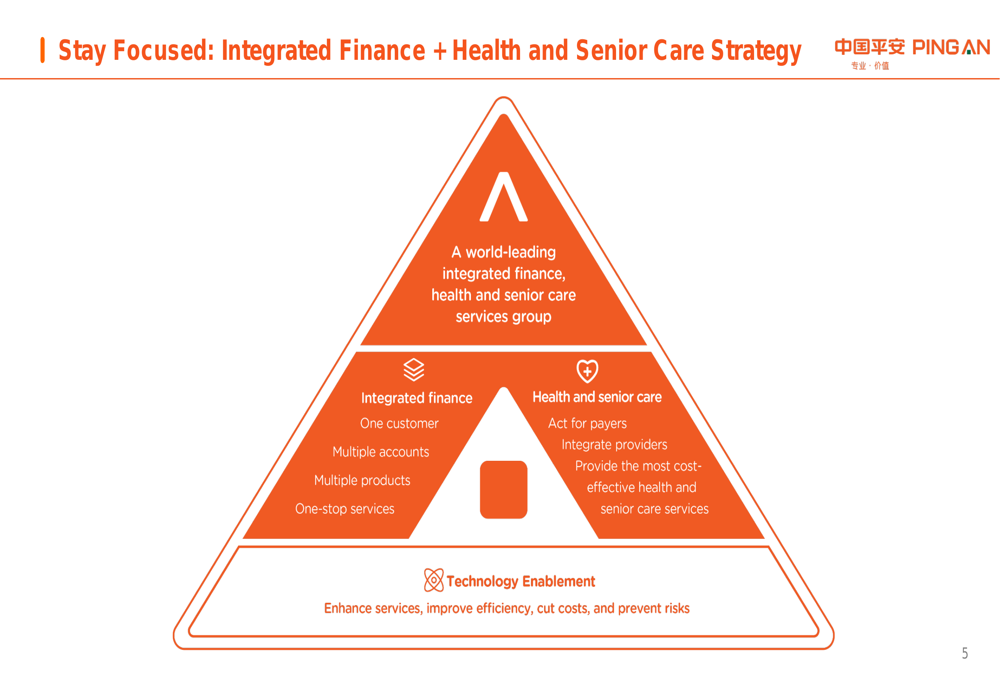

Ping An’s presentation emphasized its strategic focus on "Integrated Finance + Health and Senior Care," positioning the company as "a world-leading integrated finance, health and senior care services group." This strategy is built around three key pillars as illustrated below:

The company has made significant progress in implementing this strategy, particularly in the health and senior care segment. Ping An has established partnerships with 100% of China’s top 100 and 3A hospitals, launched home-based senior care services in 85 cities nationwide, and planned premium health and senior care communities in five major cities.

This strategic focus is already showing results, with customers holding health and senior care benefits contributing approximately 70% of Life’s NBV. The company’s ability to differentiate its core insurance offerings through these value-added services appears to be driving both customer acquisition and retention.

As shown in the following slide detailing the company’s strategic execution metrics:

Ping An’s customer-centric approach has yielded impressive retention rates, with 26.6% of customers holding four or more contracts maintaining a 97.8% retention rate. Additionally, 73.8% of customers have been with the company for over five years, with a 94.6% retention rate, demonstrating strong customer loyalty.

Quarterly Performance Highlights

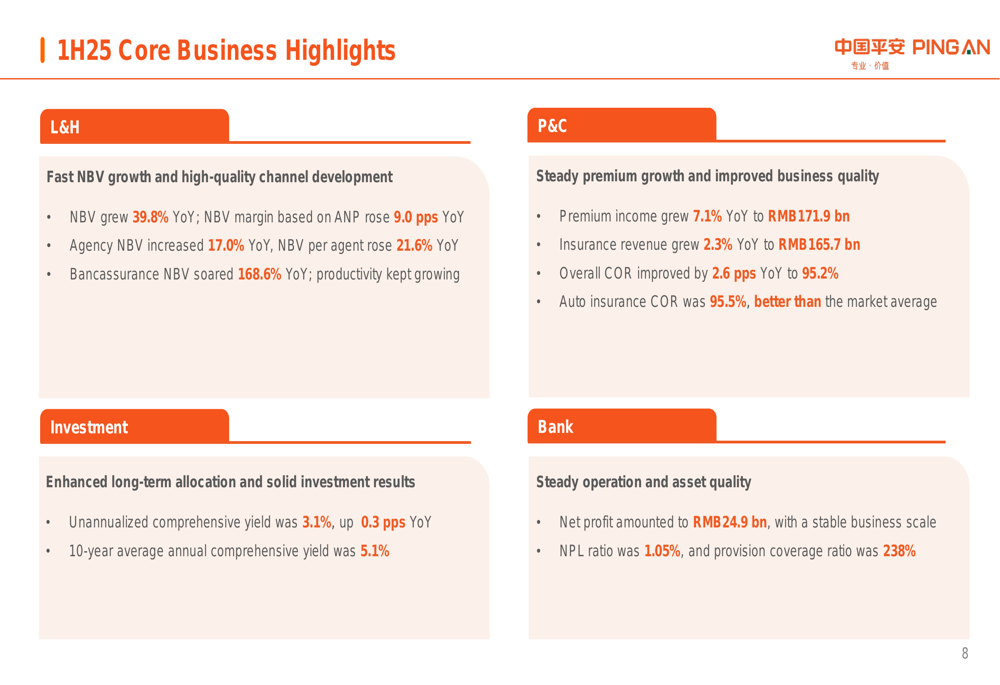

Ping An’s core business segments showed varied performance, with particularly strong results in the Life & Health (L&H) and Property & Casualty (P&C) insurance divisions, as detailed in the following business highlights:

The L&H segment demonstrated robust growth, with NBV increasing by 39.8% year-over-year. Agency NBV grew by 17.0%, with NBV per agent rising 21.6%, indicating improved agent productivity. Most notably, bancassurance NBV soared by 168.6% year-over-year, reflecting successful channel optimization strategies.

The P&C segment also performed well, with premium income growing 7.1% year-over-year to RMB171.9 billion and insurance revenue increasing 2.3% to RMB165.7 billion. The combined operating ratio (COR) improved by 2.6 percentage points to 95.2%, with auto insurance COR at 95.5%, better than the market average, indicating enhanced underwriting discipline.

Investment performance was solid, with an unannualized comprehensive yield of 3.1%, up 0.3 percentage points year-over-year, while the 10-year average annual comprehensive yield remained strong at 5.1%.

Detailed Financial Analysis

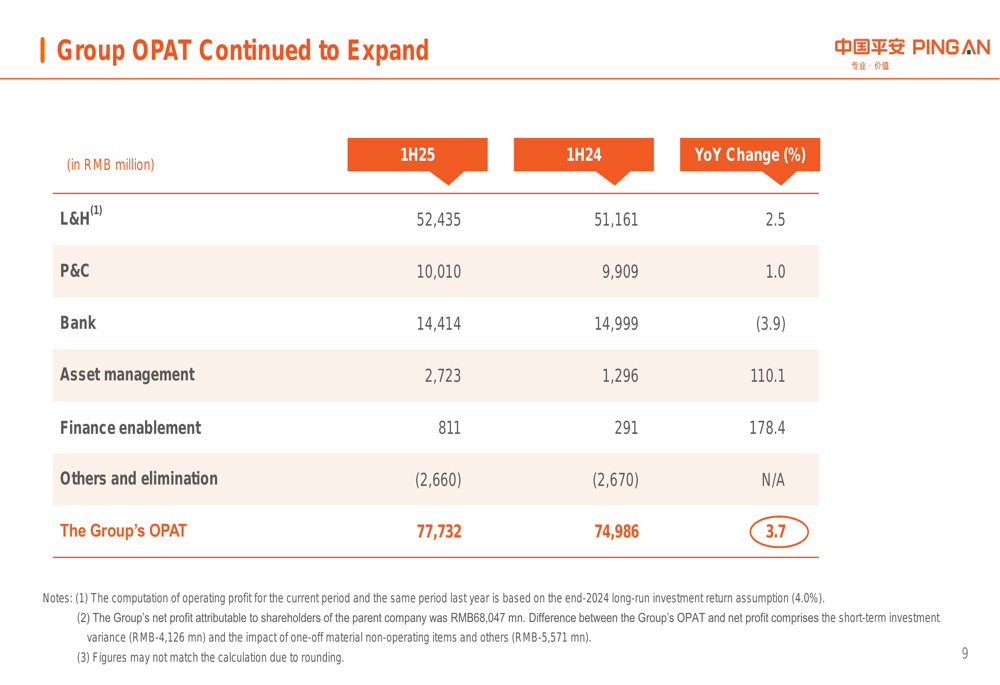

Breaking down the Group’s OPAT by business segment reveals the diversified nature of Ping An’s earnings and the relative contribution of each division:

The L&H segment remained the largest contributor to group OPAT at RMB52,435 million, growing 2.5% year-over-year. The banking segment, despite a 3.9% decline in OPAT to RMB14,414 million, remained the second-largest contributor. Notable growth came from the Asset Management segment, which saw OPAT more than double with 110.1% growth, and the Finance Enablement segment, which grew by 178.4%.

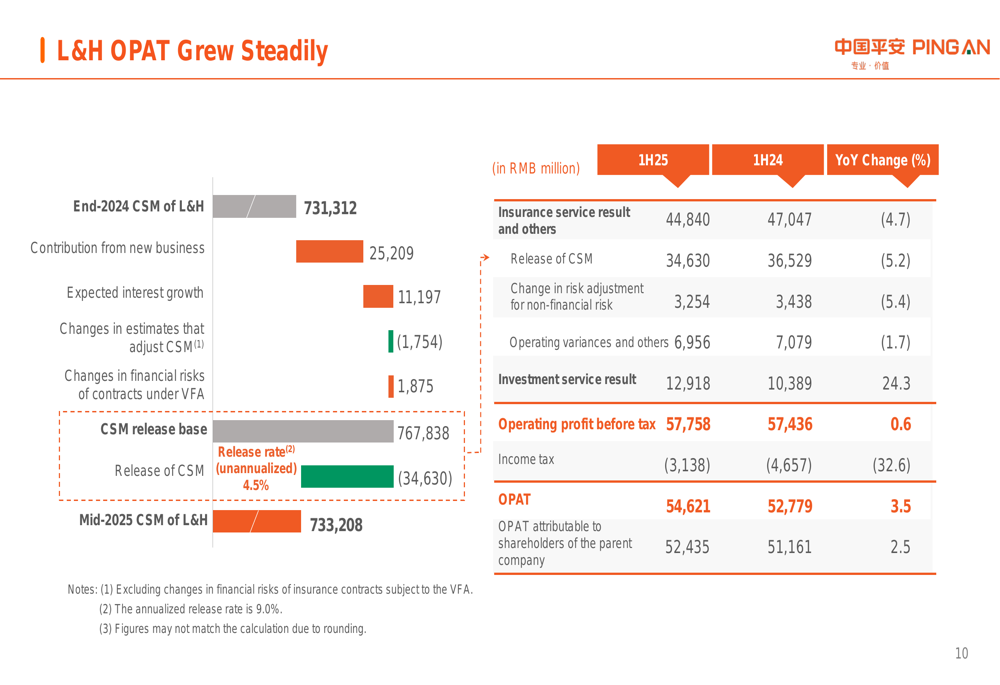

The drivers of L&H OPAT growth are further detailed in the following waterfall chart:

The chart illustrates how new business contributed RMB25,209 million to the Contractual Service Margin (CSM), while expected interest growth added RMB11,197 million. After accounting for various adjustments and the release of CSM, the mid-2025 CSM of L&H stood at RMB733,208 million, providing a strong foundation for future profit recognition.

Forward-Looking Statements

While Ping An’s presentation painted a positive picture of its current performance and strategic direction, the company included standard cautionary language regarding forward-looking statements. The company faces ongoing challenges in China’s financial services sector, including regulatory changes, economic headwinds, and intense competition.

The success of Ping An’s strategic pivot toward health and senior care services will depend on continued execution and the ability to monetize these offerings effectively. While early results are promising, particularly in driving NBV growth, the long-term profitability of this strategy remains to be proven.

Nevertheless, Ping An’s diversified business model, strong capital position, and innovative approach to integrating financial services with health and senior care position the company well to navigate market challenges and capitalize on China’s aging population and growing demand for comprehensive financial and healthcare solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.