Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Pitney Bowes Inc (NYSE:PBI) reported significant profitability improvements despite revenue challenges in its second quarter earnings presentation on July 30, 2025. The company’s shares dipped slightly in aftermarket trading, down 0.73% to $10.91, following a year-to-date surge of over 54%.

Quarterly Performance Highlights

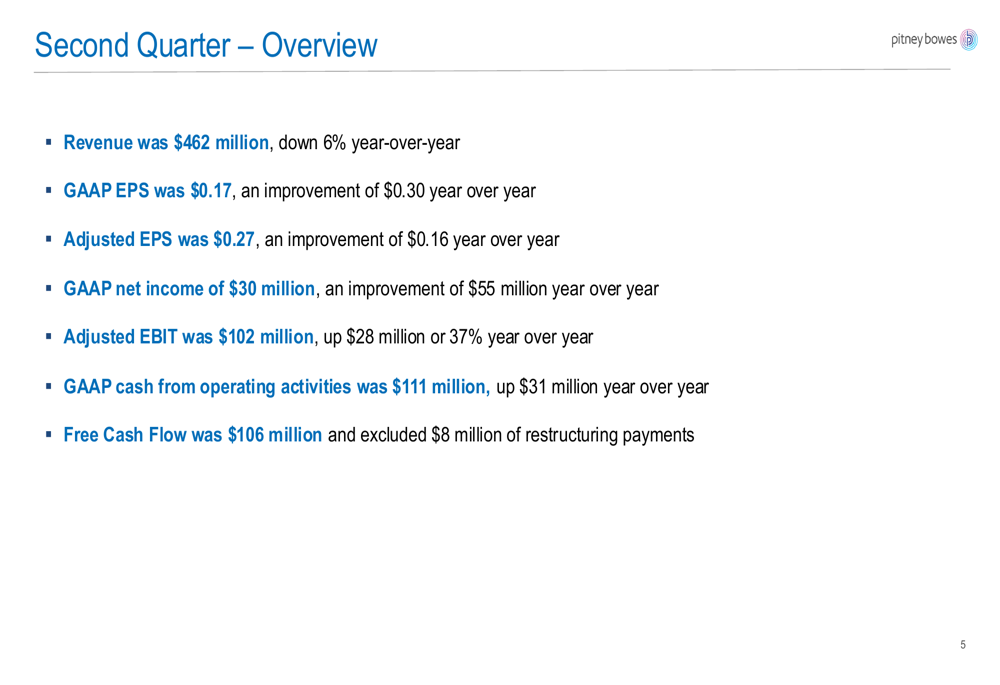

Pitney Bowes delivered strong bottom-line results in Q2 2025 despite top-line pressure. The company reported revenue of $462 million, down 6% year-over-year, while achieving substantial gains in profitability metrics.

"Change has been a huge catalyst for value creation at Pitney Bowes," CEO Kurt Wolff emphasized during the earnings call, highlighting the company’s transformation efforts.

As shown in the following quarterly overview:

The company’s GAAP EPS reached $0.17, a $0.30 improvement year-over-year, while adjusted EPS climbed to $0.27, up $0.16 from the prior year. GAAP net income surged to $30 million, representing a $55 million improvement, and adjusted EBIT rose 37% to $102 million.

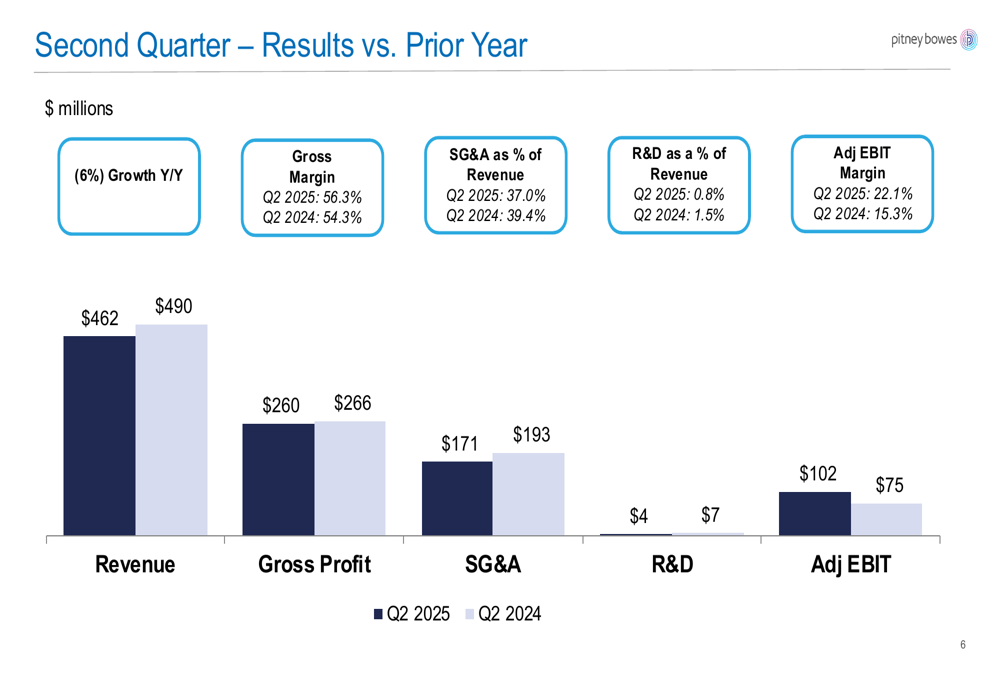

The company’s margin expansion was particularly noteworthy, as illustrated in this comparative analysis:

Gross margin improved to 56.3% from 54.3% in the prior year, while adjusted EBIT margin expanded significantly to 22.1% from 15.3%. These improvements came as the company reduced both SG&A and R&D expenses as a percentage of revenue, demonstrating effective cost management.

Segment Analysis

Pitney Bowes operates through two primary business segments: SendTech Solutions and Presort Services, each showing distinct performance trends.

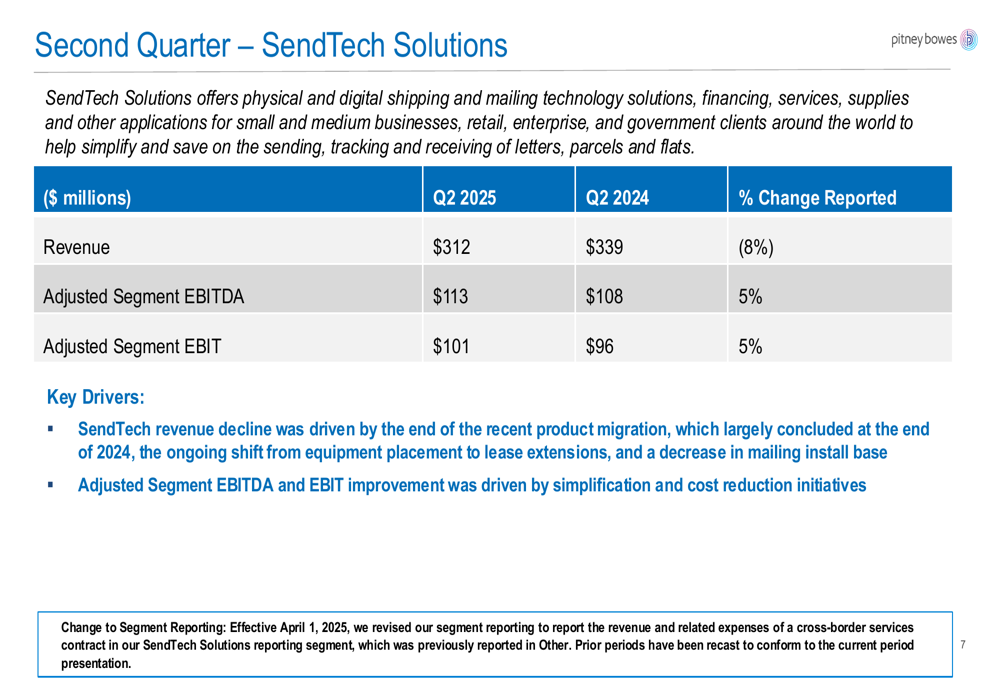

The SendTech Solutions segment, which includes mailing equipment and related services, experienced an 8% revenue decline to $312 million. However, profitability improved with adjusted segment EBIT rising 5% to $101 million.

The revenue decline in SendTech was attributed to the conclusion of a recent product migration cycle, ongoing shifts from equipment placement to lease extensions, and a decreasing mailing install base. Despite these challenges, cost reduction initiatives drove profitability improvements.

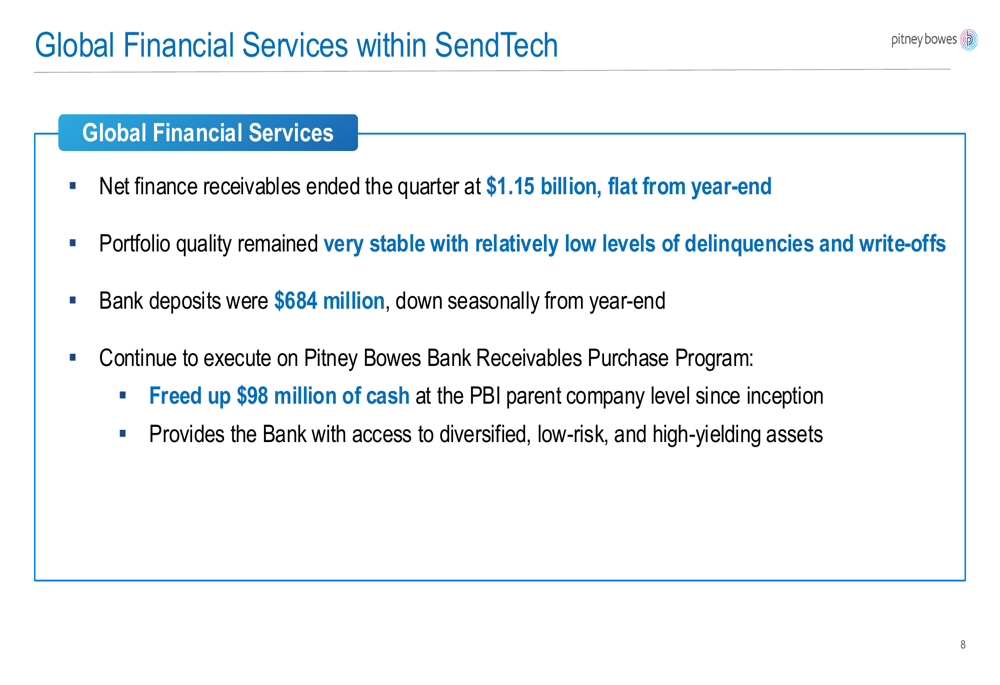

Within SendTech, the Global Financial Services operation maintained stability:

Net finance receivables remained flat at $1.15 billion, with the portfolio maintaining low delinquency and write-off levels. The company’s Bank Receivables Purchase Program has freed up $98 million in cash at the parent company level since inception.

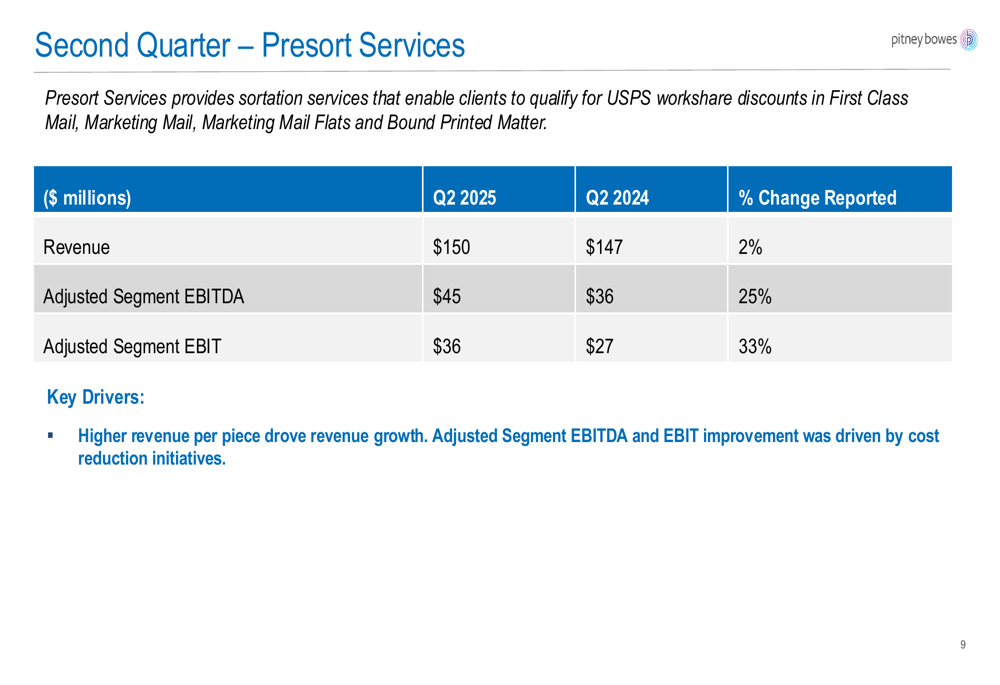

Meanwhile, the Presort Services segment showed modest revenue growth of 2% to $150 million, while delivering impressive profit gains:

Adjusted segment EBIT for Presort Services jumped 33% to $36 million, driven by higher revenue per piece and cost reduction initiatives. This segment’s strong margin performance demonstrates the company’s ability to extract greater profitability from its mail processing operations.

Guidance and Strategic Direction

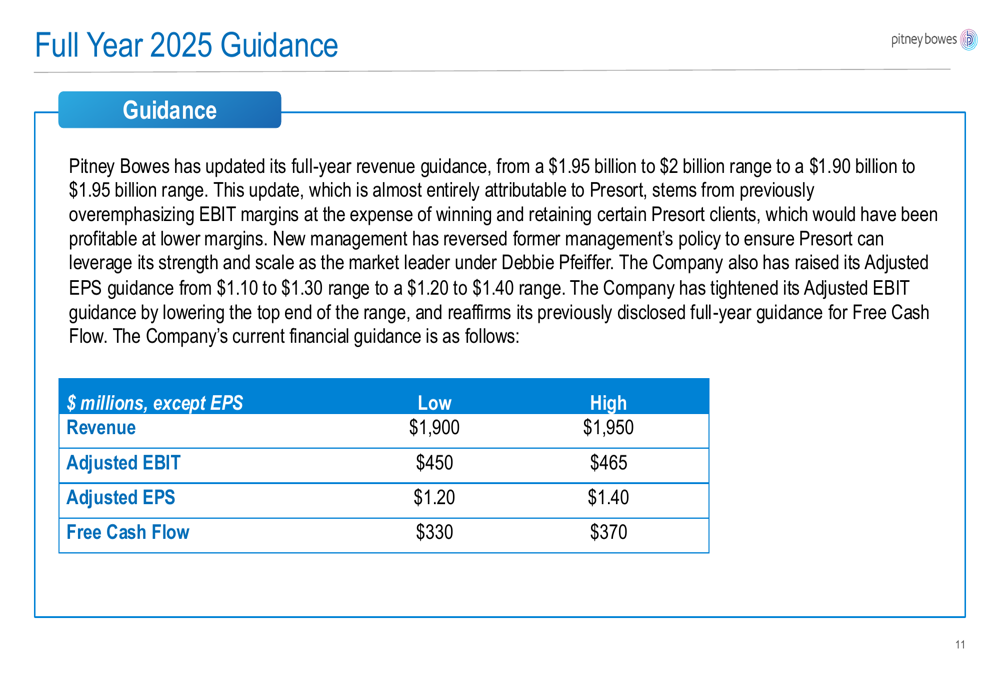

Despite the strong profitability performance, Pitney Bowes adjusted its full-year 2025 guidance, reflecting both challenges and opportunities:

The company reduced its revenue guidance to $1.90-1.95 billion, a $50 million reduction primarily attributed to the Presort segment. This adjustment stems from what the company described as "previously overemphasizing EBIT margins at the expense of winning and retaining certain Presort clients."

CFO Paul Evans highlighted the company’s perceived undervaluation during the earnings call, stating, "I think it’s an incredibly undervalued asset and the opportunity we have to bring value to our shareholders."

Despite the revenue guidance reduction, Pitney Bowes maintained its adjusted EBIT outlook of $450-465 million and increased its EPS guidance by $0.10, now projecting $1.20-1.40 per share. Free cash flow is expected to range between $330-370 million for the full year.

The company also expanded its share repurchase authorization from $150 million to $400 million, signaling confidence in its financial position and commitment to returning value to shareholders.

Financial Position

Pitney Bowes has been actively managing its debt profile, as evidenced by significant changes between December 2024 and June 2025. The company has restructured its debt with new term loans at varying interest rates, while reducing or eliminating certain existing obligations.

Cash flow performance was strong, with GAAP cash from operating activities reaching $111 million, up $31 million year-over-year. Free cash flow totaled $106 million, excluding $8 million in restructuring payments.

The company faces several challenges moving forward, including ongoing revenue declines in its traditional mailing business, customer attrition in the Presort segment, and the need to balance margin optimization with customer retention. However, its improved profitability metrics and cash generation capabilities provide financial flexibility as it navigates these challenges.

With shares having surged over 54% year-to-date, investors appear to be recognizing the value of Pitney Bowes’ transformation efforts, though the stock’s slight aftermarket decline suggests some caution regarding the reduced revenue guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.