Stock market today: S&P 500 rides Apple-led tech rally to close higher

Plains All American Pipeline , L.P. (NASDAQ:PAA) reported solid first quarter 2025 results, highlighting continued execution of its efficient growth strategy through bolt-on acquisitions and operational improvements. The company’s presentation, delivered on May 9, 2025, showcased steady financial performance and reaffirmed full-year guidance while emphasizing its commitment to shareholder returns.

Executive Summary

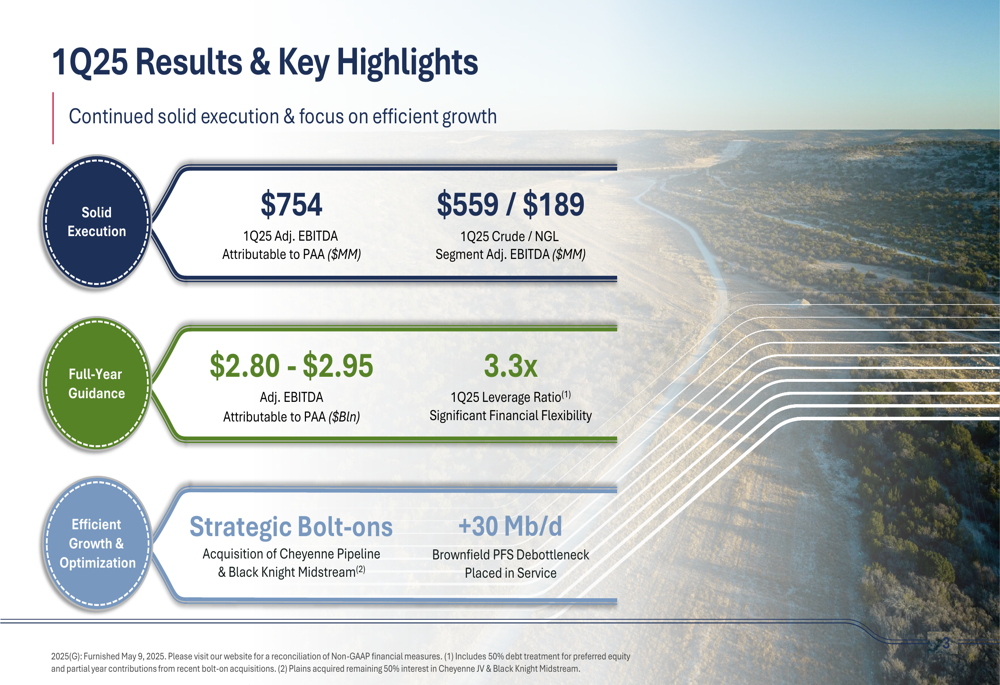

Plains reported Adjusted EBITDA attributable to PAA of $754 million for Q1 2025, with the Crude Oil segment contributing $559 million and the NGL segment delivering $189 million. The company reaffirmed its full-year 2025 guidance for Adjusted EBITDA of $2.80-$2.95 billion, positioning it for continued growth compared to previous years.

As shown in the following quarterly results summary:

The company highlighted recent acquisitions of Cheyenne Pipeline and Black Knight (BMV:BKIN) Midstream as part of its bolt-on strategy, along with the completion of a brownfield debottlenecking project that added 30,000 barrels per day of capacity. Plains maintained a leverage ratio of 3.3x, within its target range of 3.25x-3.75x.

Quarterly Performance Highlights

The Crude Oil segment’s Adjusted EBITDA increased slightly from $553 million in Q1 2024 to $559 million in Q1 2025. This modest growth was driven by higher pipeline tariff volumes, tariff escalation, and contributions from bolt-on acquisitions, which collectively added $24 million. However, these gains were partially offset by $18 million in higher operating expenses related to environmental accruals and remediation costs.

The NGL segment showed stronger performance, with Adjusted EBITDA rising from $159 million in Q1 2024 to $189 million in Q1 2025. This 19% increase was primarily attributed to higher weighted average frac spreads and increased NGL sales volumes, which contributed $29 million to the year-over-year improvement.

Sequentially, the Crude Oil segment experienced a slight decline from $569 million in Q4 2024 to $559 million in Q1 2025, as bolt-on contributions of $13 million were more than offset by $23 million in lower volumes and higher operating expenses. Conversely, the NGL segment improved from $154 million in Q4 2024 to $189 million in Q1 2025, benefiting from higher frac spreads, increased sales volumes, and lower operating expenses.

Strategic Growth Initiatives

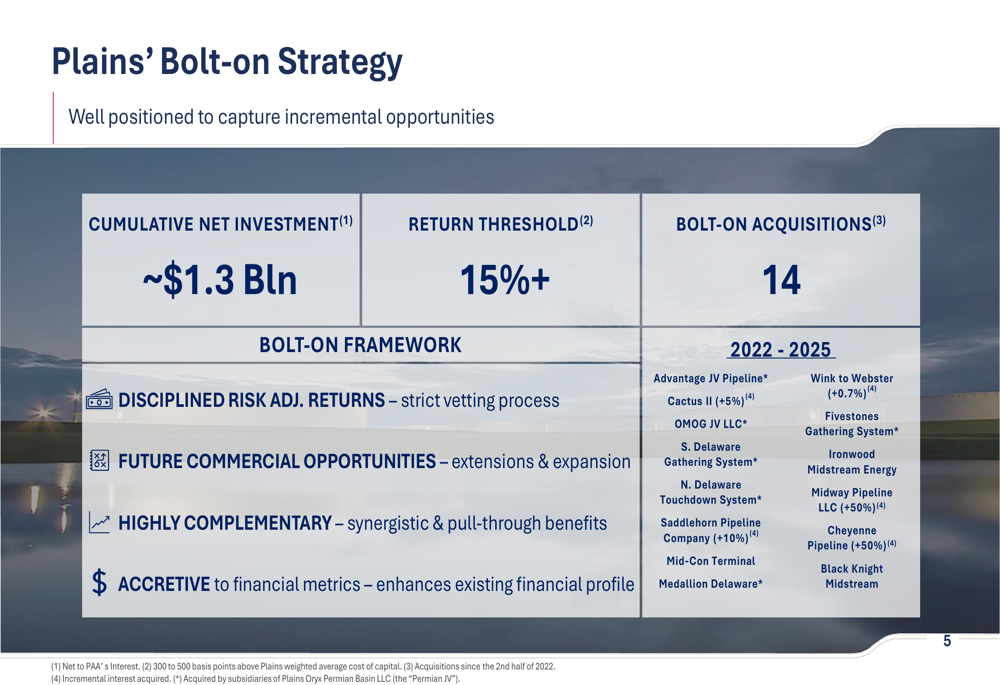

Plains has implemented a disciplined bolt-on acquisition strategy, completing 14 transactions since the second half of 2022 with a cumulative net investment of approximately $1.3 billion. The company targets a minimum 15% return threshold for these acquisitions, focusing on assets that complement its existing infrastructure and provide synergistic benefits.

The company’s bolt-on acquisition framework is illustrated in the following slide:

This strategy emphasizes disciplined risk-adjusted returns, future commercial opportunities, complementary assets with synergistic benefits, and accretive financial metrics. Recent acquisitions include Ironwood Midstream Energy, Midway Pipeline LLC, Cheyenne Pipeline, and Black Knight Midstream, among others.

Plains positions itself for resilience through market cycles by maintaining financial flexibility with a leverage ratio at the lower end of its target range, enabling it to capitalize on acquisition opportunities while ensuring strong distribution coverage.

Financial Outlook

For 2025, Plains projects Adjusted EBITDA attributable to PAA of $2.80-$2.95 billion, with the Crude Oil segment contributing approximately $2.41 billion and the NGL segment adding around $450 million. The company expects to generate Distributable Cash Flow available to Common Unitholders of $1.875 billion, resulting in a Common Unit Distribution Coverage Ratio of 175%.

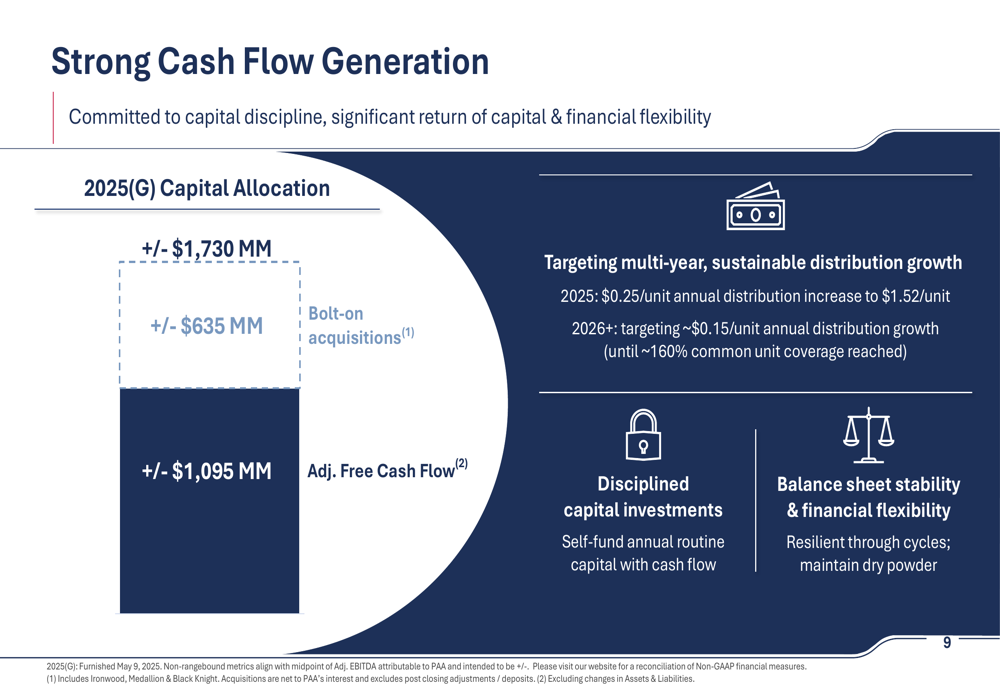

Plains anticipates Adjusted Free Cash Flow (excluding changes in Assets & Liabilities) of approximately $1.095 billion for 2025, providing significant financial flexibility for both bolt-on acquisitions and shareholder returns. The company’s capital allocation strategy is outlined in the following slide:

The company is targeting multi-year, sustainable distribution growth, with a $0.25 per unit annual increase in 2025 and approximately $0.15 per unit annual growth starting in 2026. Plains remains committed to disciplined capital investments, self-funding annual routine capital needs with cash flow, and maintaining balance sheet stability and financial flexibility.

Long-term Value Creation

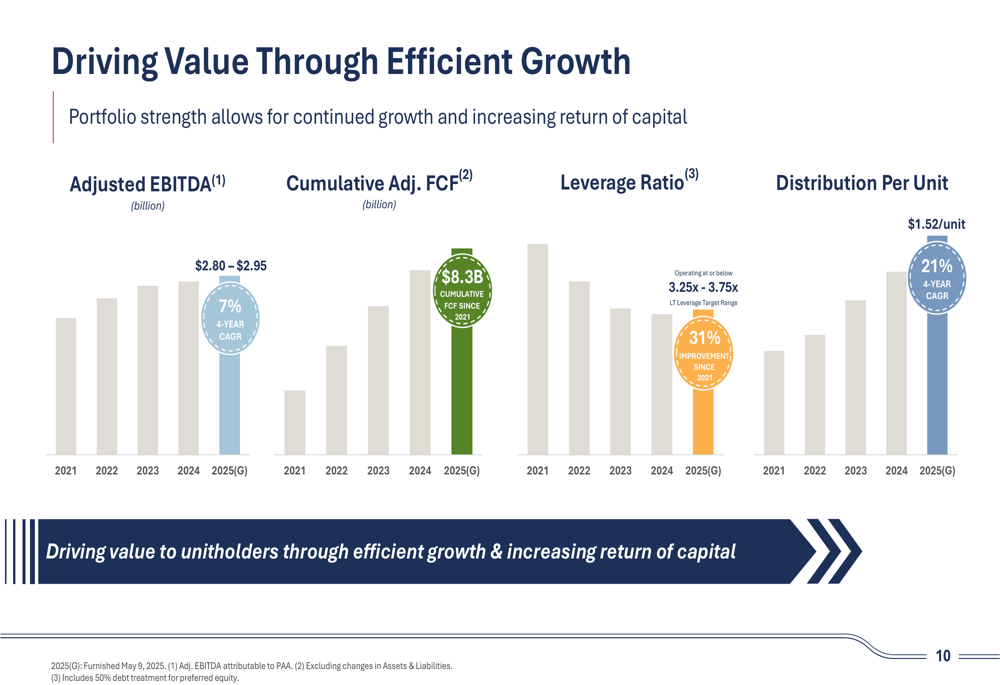

Plains has demonstrated consistent progress in driving value through efficient growth, as illustrated in the following performance metrics:

Since 2021, the company has achieved a 7% four-year compound annual growth rate (CAGR) in Adjusted EBITDA, accumulated $8.3 billion in free cash flow, improved its leverage ratio by 31%, and delivered a 21% four-year CAGR in distribution per unit. These metrics highlight Plains’ successful execution of its strategy to balance growth investments with shareholder returns.

Segment Analysis

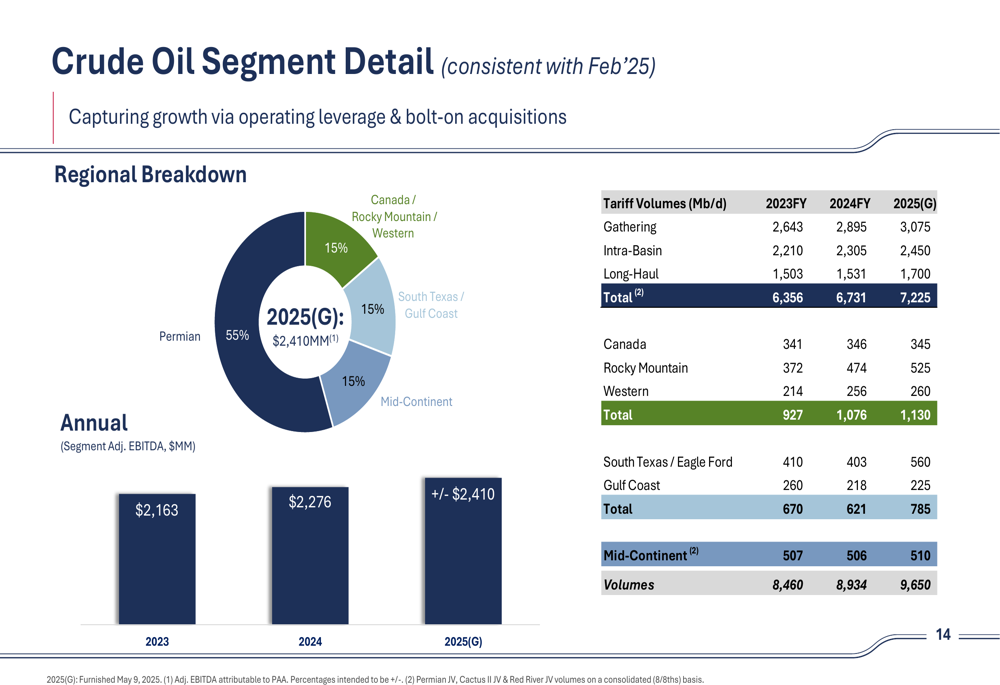

The Crude Oil segment, which accounts for approximately 84% of Plains’ total Adjusted EBITDA, is diversified across multiple regions with the Permian Basin representing the largest share at 55%. The company’s pipeline tariff volumes are projected to reach 7,225 thousand barrels per day (Mb/d) in 2025, as shown in the following segment breakdown:

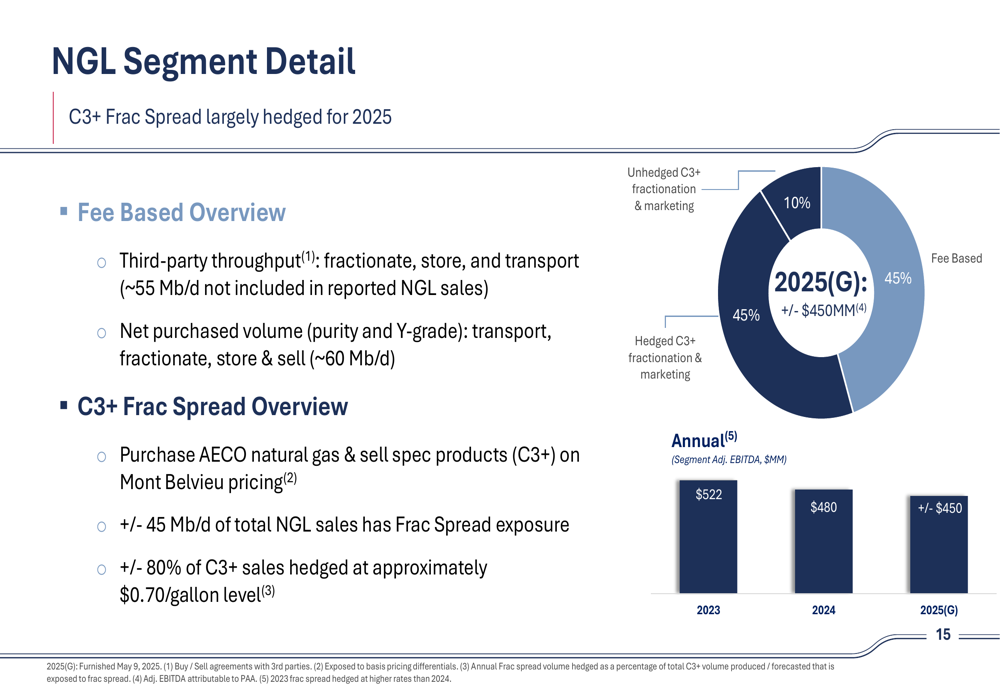

For the NGL segment, Plains has structured its operations to provide stability through a balanced approach, with 45% of the business being fee-based, 45% hedged C3+ fractionation and marketing, and only 10% unhedged. This strategy helps mitigate volatility in the NGL market while allowing for some upside potential.

The company’s NGL segment structure is illustrated below:

Approximately 80% of Plains’ C3+ sales are hedged at approximately $0.70 per gallon for 2025, providing earnings stability for this segment. The composition of spec products is predominantly propane (70%) and butane (25%), with condensate accounting for the remaining 5%.

Market Context and Outlook

Plains acknowledges the current market environment characterized by short-term uncertainty and volatility, with trade tariffs creating global economic uncertainty and OPEC+ dissension adding surplus supply to the market. However, the company maintains a constructive long-term view based on population growth, improving living standards supporting demand, and diminishing long-lead project additions increasing reliance on U.S. shale production.

For 2025, Plains assumes Permian Basin production growth of 200-300 thousand barrels per day, consistent with previous projections. The company’s guidance reflects the lower half of its range in a $60-$65 per barrel WTI price environment, demonstrating a conservative approach to financial planning.

According to the previous earnings call from Q3 2024, Plains was expecting adjusted EBITDA for 2024 at the upper end of the $2.725-$2.775 billion range. The Q1 2025 guidance of $2.80-$2.95 billion represents continued growth, aligning with the company’s long-term trajectory.

Plains GP Holdings (NASDAQ:PAGP) closed at $18.24 on May 8, 2025, with a 1.28% increase on the day. In pre-market trading on May 9, the stock was up an additional 0.6% to $18.35, suggesting a positive market reaction ahead of the earnings presentation.

With a strong balance sheet featuring investment grade ratings (BBB/BBB/Baa2), committed liquidity of $2.6 billion, and a disciplined approach to capital allocation, Plains appears well-positioned to execute its strategy of efficient growth while delivering increasing returns to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.