Street Calls of the Week

Introduction & Market Context

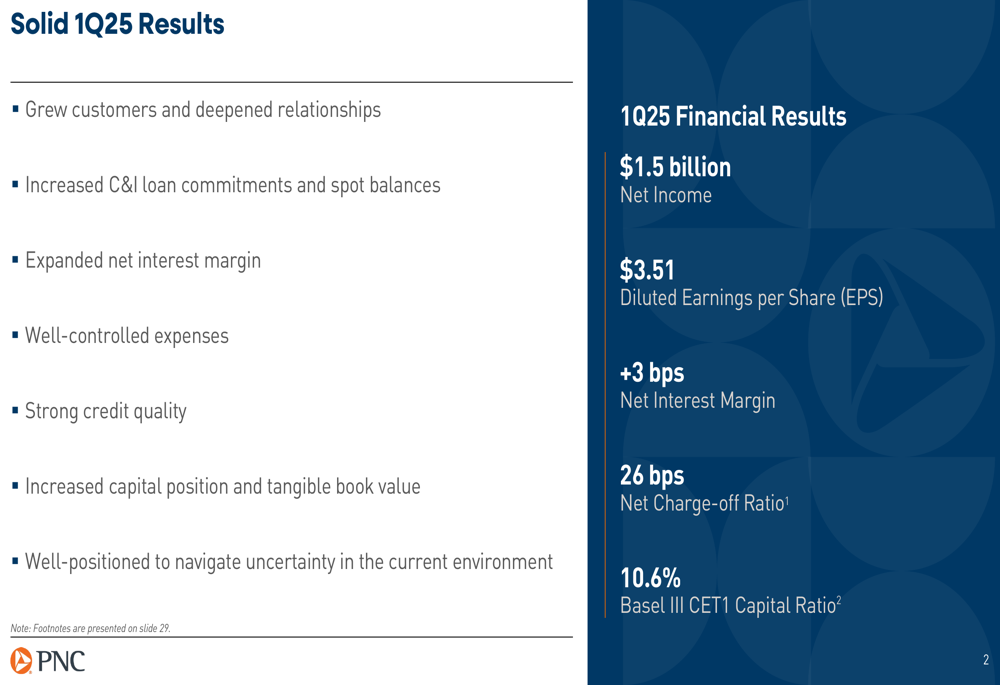

PNC Financial Services Group (NYSE:PNC) reported its first-quarter 2025 results on April 15, 2025, showcasing solid performance with improving net interest margins and credit metrics despite a slight revenue decline. The company’s stock price rose 2.01% to $158.44 following the earnings announcement, reflecting positive investor sentiment about the results and outlook.

PNC reported earnings per share (EPS) of $3.51, exceeding analyst expectations of $3.39, despite revenue coming in slightly below forecasts at $5.45 billion. The company’s strong capital position, improving credit quality, and positive outlook for the remainder of 2025 helped drive the favorable market reaction.

Quarterly Performance Highlights

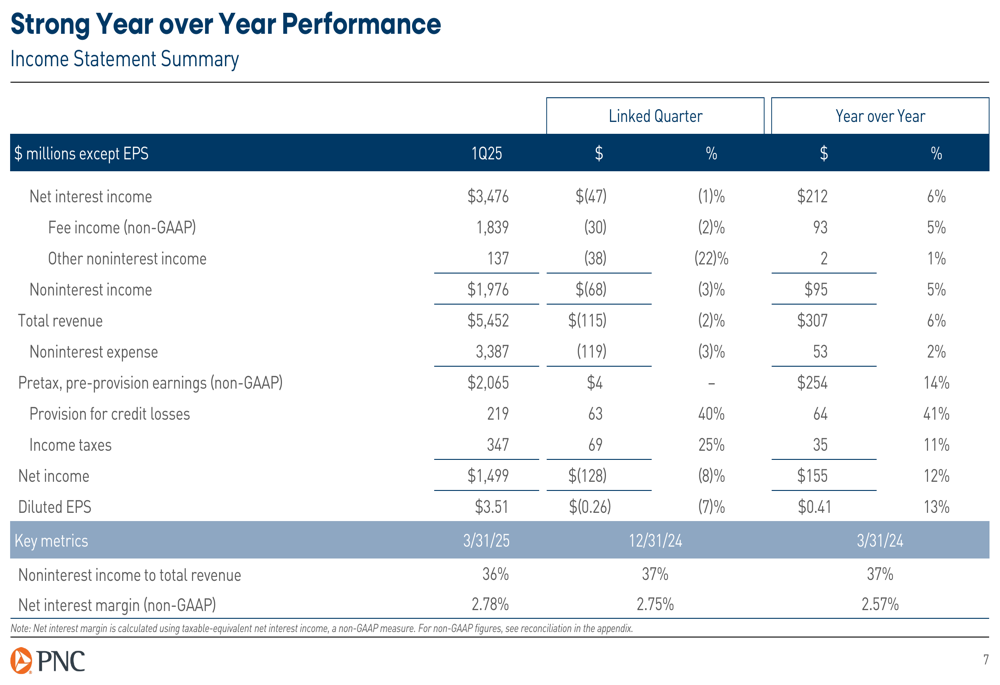

PNC delivered net income of $1.5 billion for Q1 2025, representing a 12% increase year-over-year, though down 8% from the previous quarter. The company’s net interest margin expanded to 2.78%, up from 2.75% in Q4 2024 and 2.57% in Q1 2024, demonstrating continued improvement in core profitability.

As shown in the following income statement summary, PNC achieved strong year-over-year growth across key metrics:

Total (EPA:TTEF) revenue reached $5.45 billion, up 6% year-over-year, with net interest income increasing by 6% and noninterest income growing by 5%. The company’s pretax, pre-provision earnings grew by an impressive 14% compared to the same period last year, highlighting the underlying strength of PNC’s core operations.

Fee income, which accounts for 36% of total revenue, showed solid performance at $1.84 billion, with notable growth in asset management and brokerage (up 7% year-over-year) and capital markets and advisory (up 18% year-over-year).

Detailed Financial Analysis

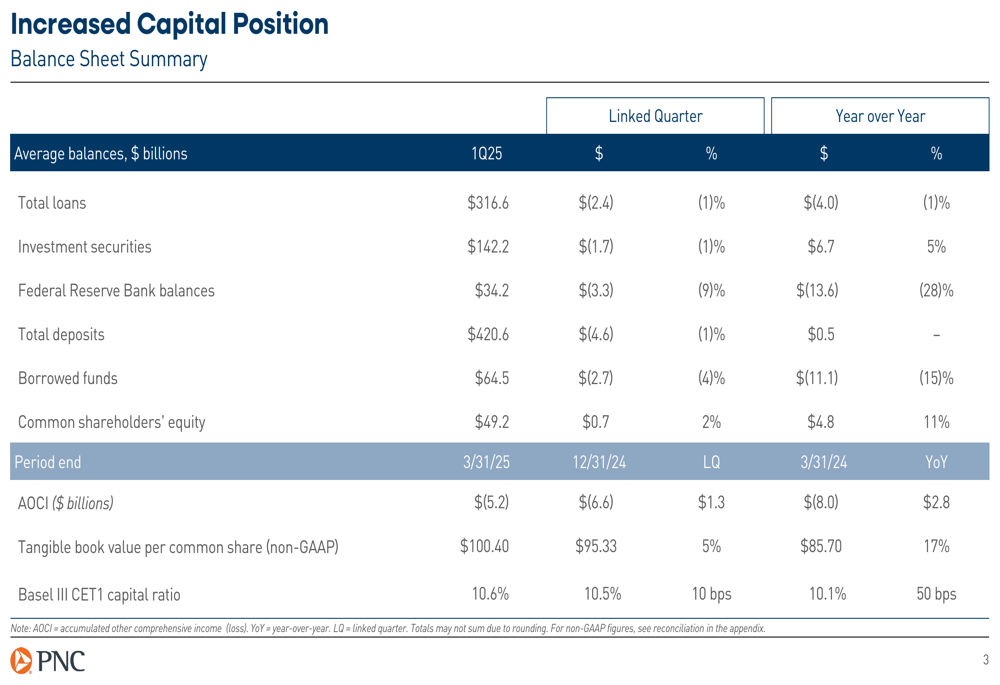

PNC’s balance sheet remained strong, with total assets of $554.96 billion as of March 31, 2025. The company’s capital position continued to improve, with the Common Equity Tier 1 (CET1) ratio increasing to 10.6%, up from 10.5% at the end of 2024 and 10.1% a year ago.

The following slide illustrates PNC’s balance sheet summary, highlighting the year-over-year improvement in capital position:

While average loans declined by 1% both quarter-over-quarter and year-over-year to $316.6 billion, spot loans showed encouraging growth of $2.4 billion or 1% during the quarter. This growth was primarily driven by C&I loans, which increased by $4.7 billion, partially offset by declines in commercial real estate and consumer loans.

As illustrated in the loan trends slide below, C&I loan utilization increased by approximately 80 basis points during the quarter, a positive sign for future loan growth:

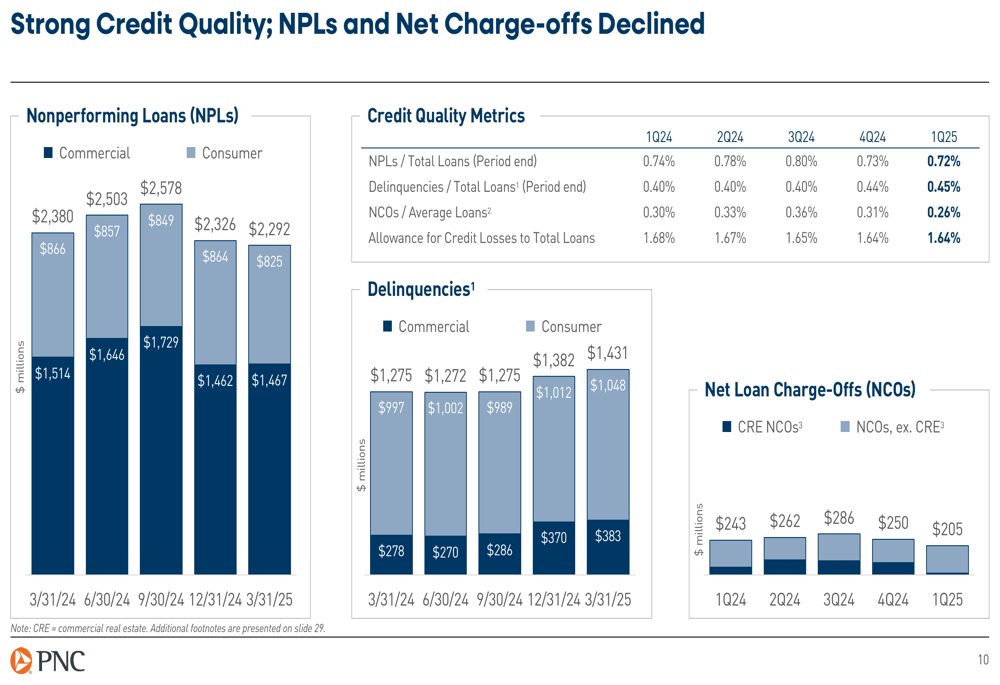

Credit quality showed improvement, with nonperforming loans (NPLs) and net charge-offs both declining during the quarter. Net charge-offs decreased to $205 million or 0.26% of average loans, down from 0.31% in the previous quarter and 0.30% a year ago.

The following slide details the improving credit quality metrics:

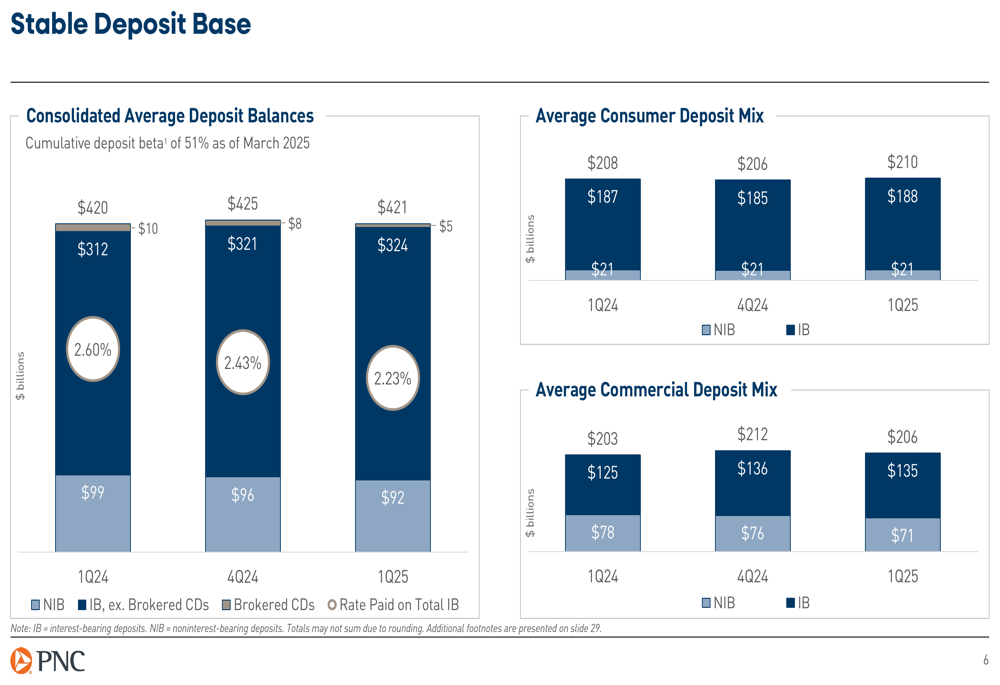

PNC maintained a stable deposit base of $420.6 billion, down 1% from the previous quarter but essentially flat year-over-year. The company’s cumulative deposit beta stood at 51% as of March 2025, reflecting disciplined deposit pricing in a high-rate environment.

Strategic Initiatives

During the earnings call, PNC’s Chairman and CEO Bill Demchak emphasized the company’s focus on organic growth opportunities and the strength of its balance sheet, client selection, interest rate risk positioning, diversified business mix, and technology investments.

A significant development was the appointment of Mark Wiedemann as President, bringing extensive financial services experience from his time at BlackRock (NYSE:BLK). Demchak clarified that this appointment does not signal a change in strategy but rather adds complementary skills to the existing management team.

The company continues to invest in its national expansion strategy, which is driving growth across all lines of business. According to management comments in the earnings call, new markets are outproducing legacy markets on a relative basis, contributing significantly to customer growth and net inflows in wealth management.

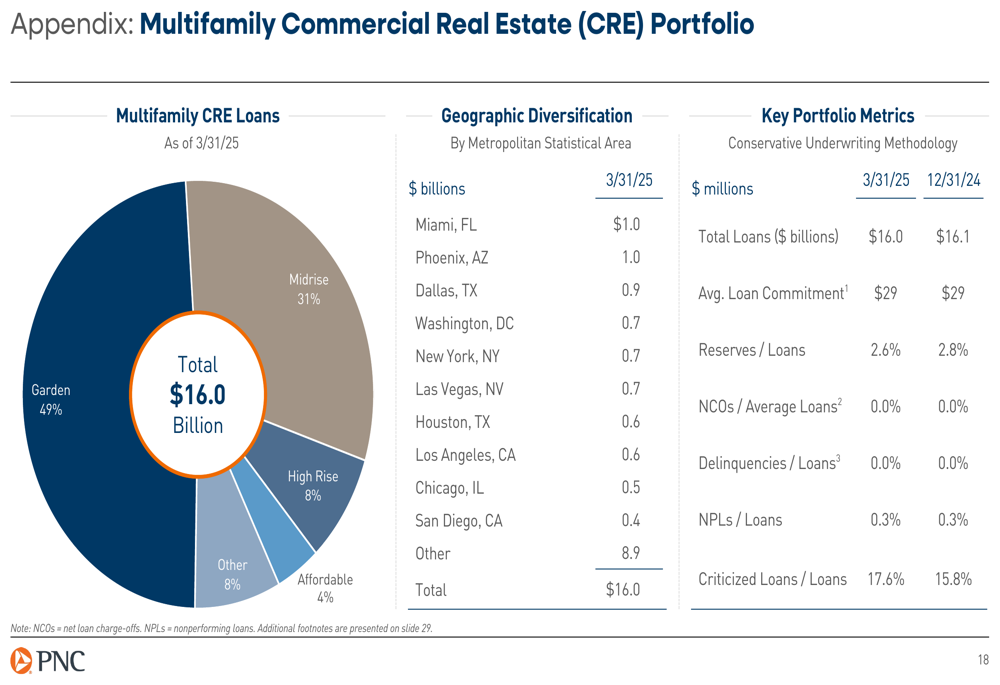

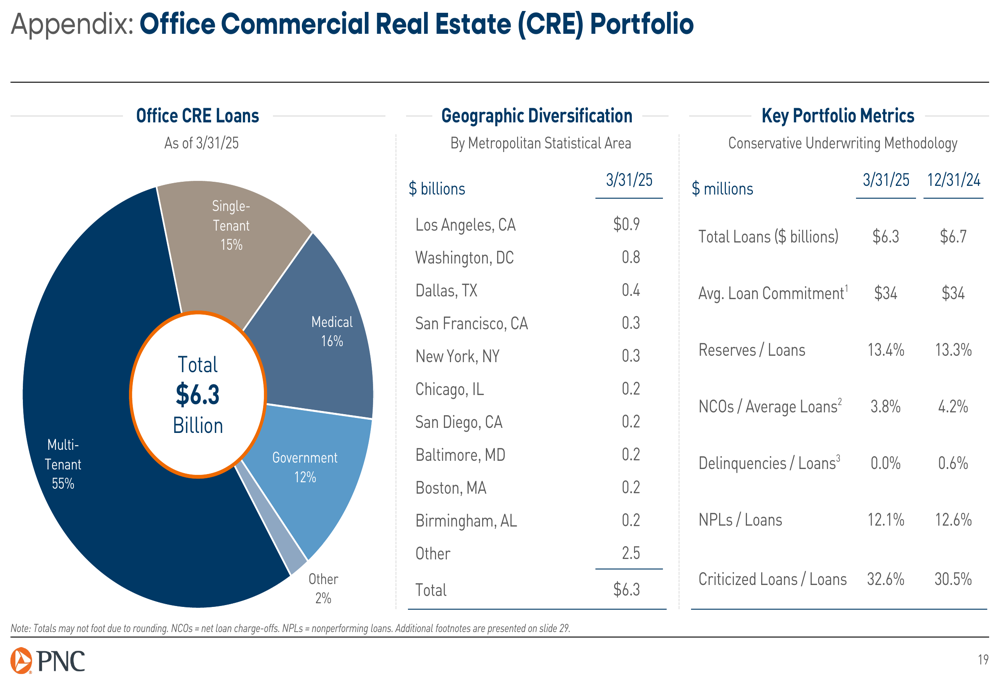

Office CRE Portfolio Management

PNC continues to actively manage its commercial real estate portfolio, particularly the office segment, which faces ongoing challenges. The office CRE portfolio represents 2.0% of total loans at $6.3 billion, with a high nonperforming loan ratio of 12.1% and substantial reserves at 13.4% of loans.

The following slide provides details on the office CRE portfolio composition:

The multi-tenant segment, which represents 55% of the office portfolio, shows the highest stress with a criticized ratio of 53.5% and NPL/Loans ratio of 21.3%. However, PNC has built significant reserves against this exposure, with reserves to loans at 18.7% for this segment.

Forward-Looking Statements

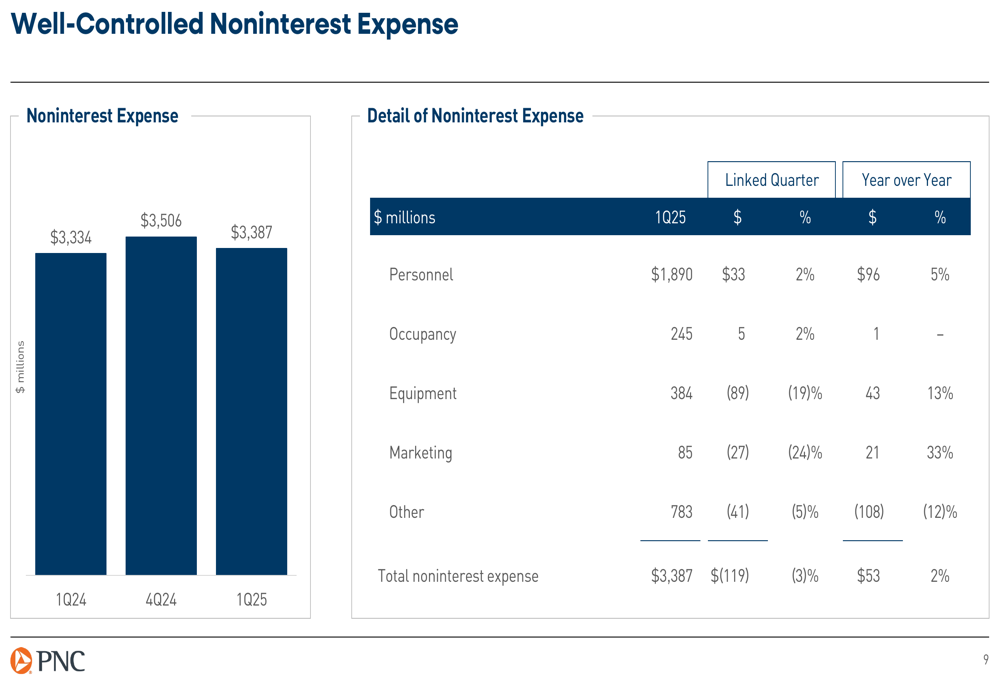

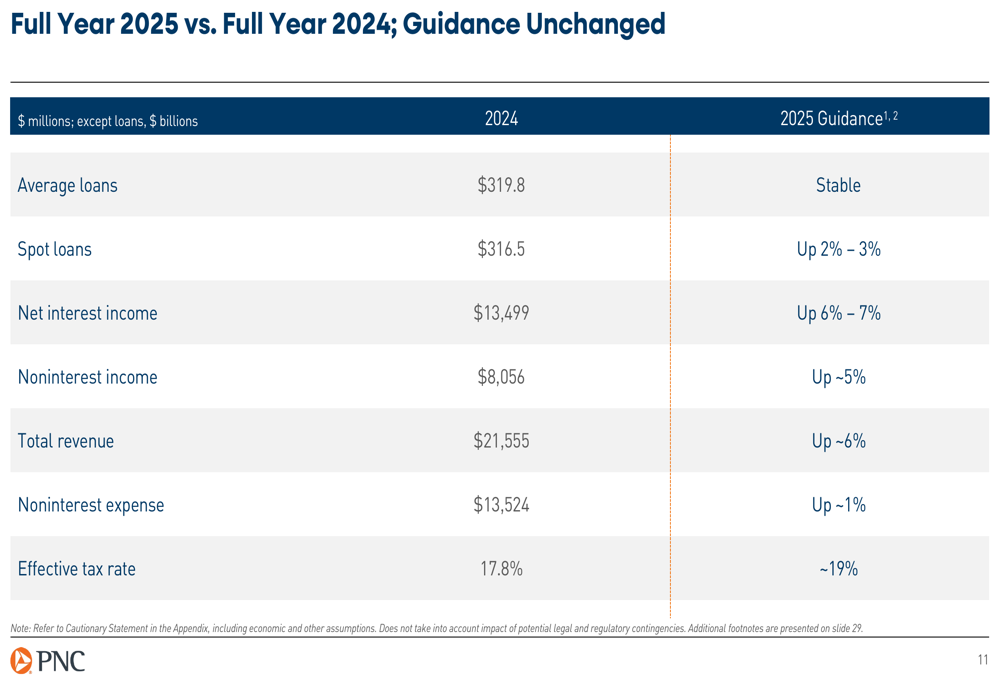

PNC maintained its full-year 2025 guidance, projecting net interest income growth of 6-7%, noninterest income growth of approximately 5%, and total revenue growth of approximately 6%. The company expects noninterest expenses to increase by only about 1%, demonstrating continued focus on expense management.

The following slide summarizes PNC’s full-year 2025 guidance:

For the second quarter of 2025, PNC expects average loans to increase by approximately 1%, net interest income to grow by 1-2%, and fee income to rise by 1-3%. Total revenue is projected to increase by 1-3% compared to the first quarter, while noninterest expenses are expected to remain stable.

During the earnings call, CFO Rob Reilly indicated that PNC’s net interest margin could approach 2.90% by the fourth quarter of 2025, continuing the positive trend seen in recent quarters. The company also plans to increase share repurchases in the coming quarters while still building capital, reflecting confidence in its financial position and outlook.

In conclusion, PNC’s first quarter results demonstrate solid performance with improving profitability metrics and credit quality, despite modest revenue pressure. The company’s strong capital position, expanding net interest margin, and return to spot loan growth provide positive momentum for the remainder of 2025, supporting management’s optimistic outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.