Intel surges more than 8% after chipmaker’s profits top expectations

Introduction & Market Context

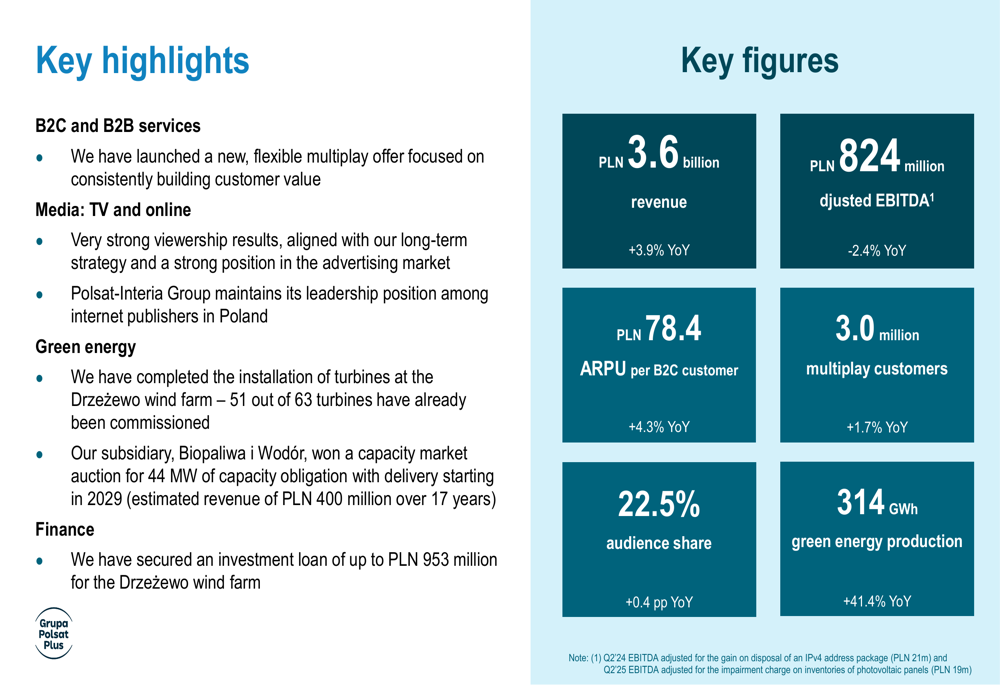

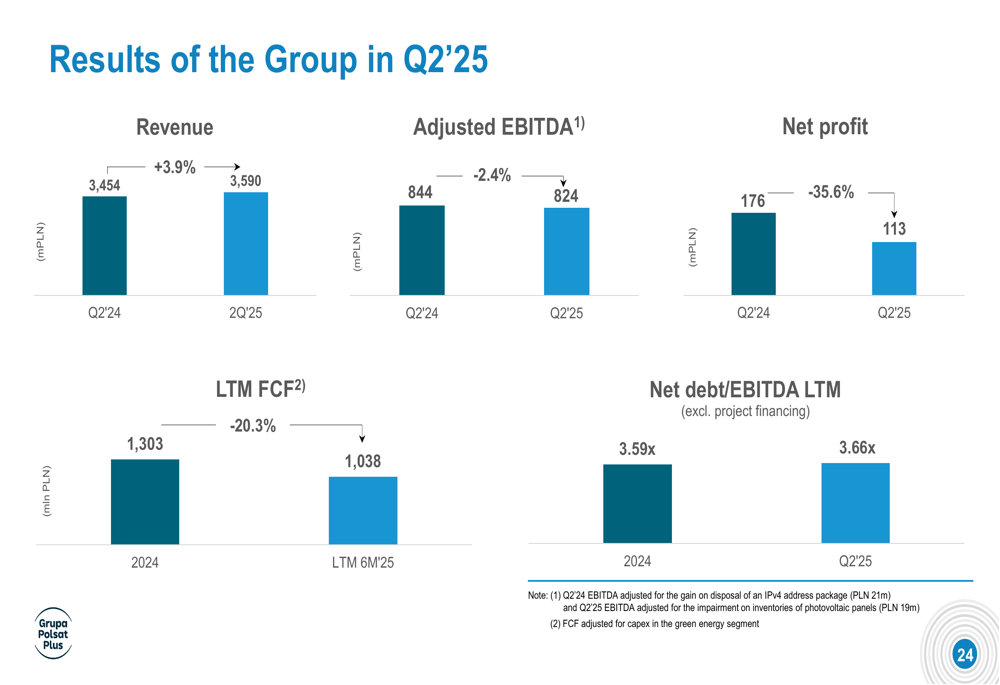

Grupa Polsat Plus (WSE:CPS) presented its Q2 2025 financial results on August 21, 2025, revealing a mixed performance characterized by revenue growth but declining profitability. The Polish media and telecommunications conglomerate reported a 3.9% year-over-year increase in revenue to PLN 3.6 billion, while adjusted EBITDA decreased by 2.4% to PLN 824 million. The company maintained its leadership position in Poland’s media landscape with a 22.5% audience share and continued to expand its green energy segment.

Quarterly Performance Highlights

Polsat Plus achieved several key milestones in the second quarter, despite facing profitability challenges. The company’s net profit declined significantly by 35.6% year-over-year to PLN 113 million, while maintaining revenue growth across multiple business segments.

As shown in the following comprehensive overview of the quarter’s performance:

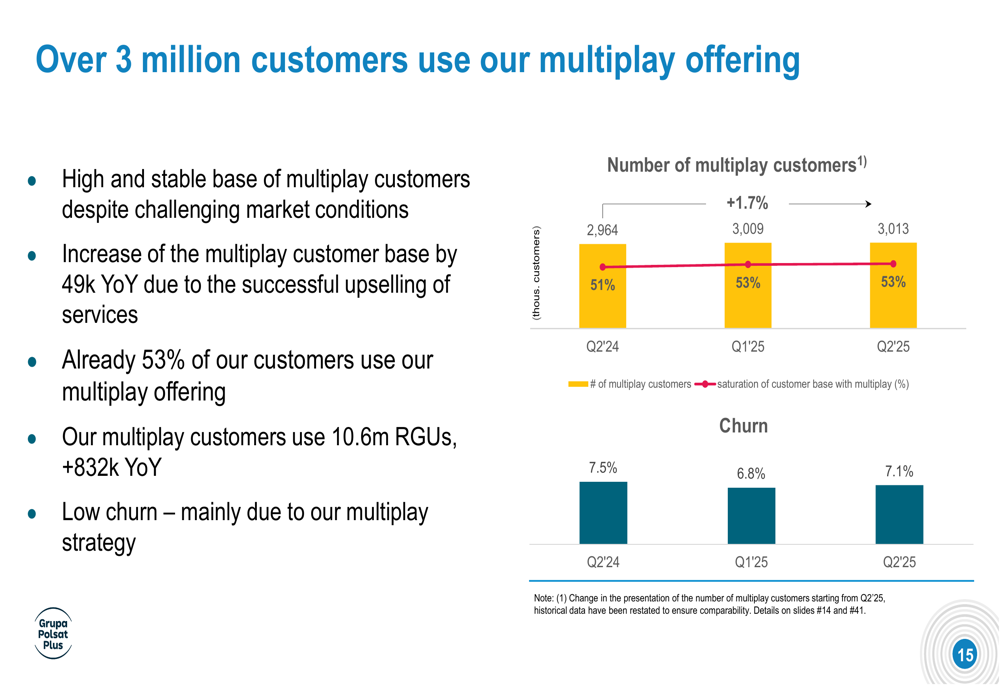

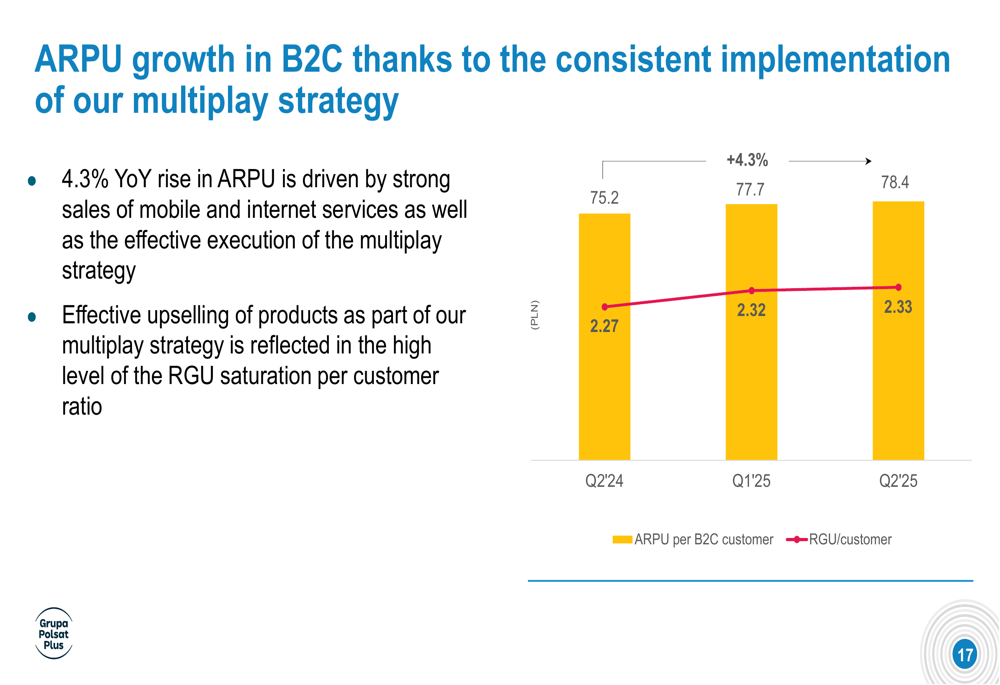

The company’s ARPU (average revenue per user) per B2C customer increased by 4.3% year-over-year to PLN 78.4, demonstrating the effectiveness of its multiplay strategy. The multiplay customer base grew by 1.7% to 3.0 million customers, representing 53% of the total customer base.

The following chart illustrates the steady growth in multiplay customers:

The company’s ARPU growth has been a consistent bright spot, as shown in this chart:

Segment Performance Analysis

Media Segment

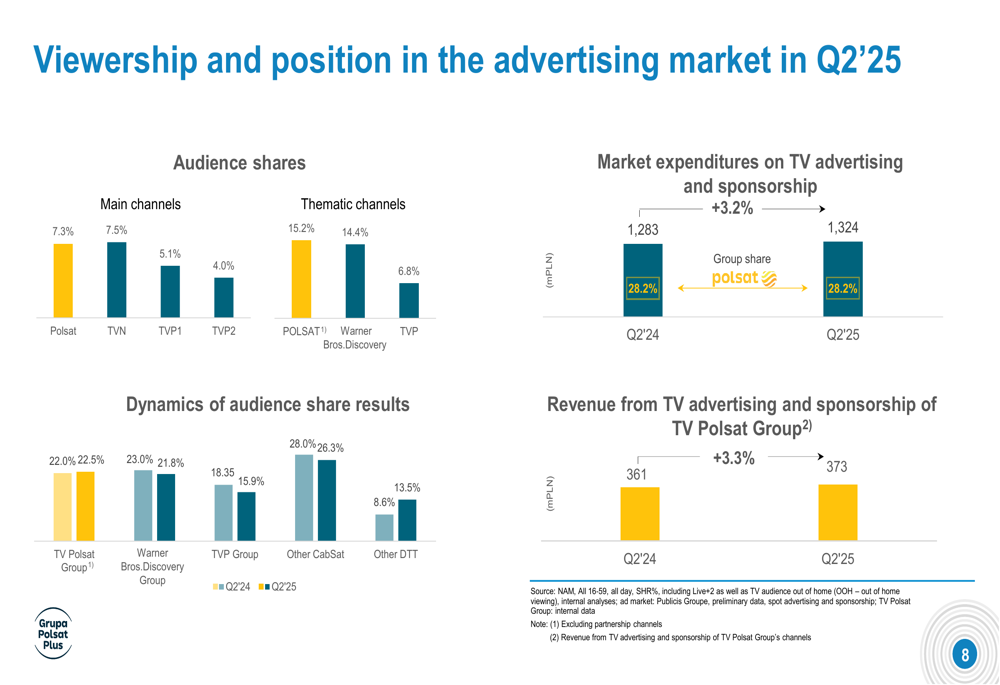

In the media segment, Polsat Plus maintained its strong position in the Polish television market with a 22.5% audience share, up 0.4 percentage points year-over-year. The company outperformed TVP Group (15.9%) and remained competitive with Warner Bros. Discovery (NASDAQ:WBD) Group (21.8%).

The following chart details the company’s viewership and advertising market position:

The Polish TV advertising market grew by 3.2% to PLN 1,324 million in Q2 2025, with Polsat Plus maintaining its market share at 28.2%. The company’s revenue from TV advertising and sponsorship increased by 3.3% to PLN 373 million.

B2C and B2B Services

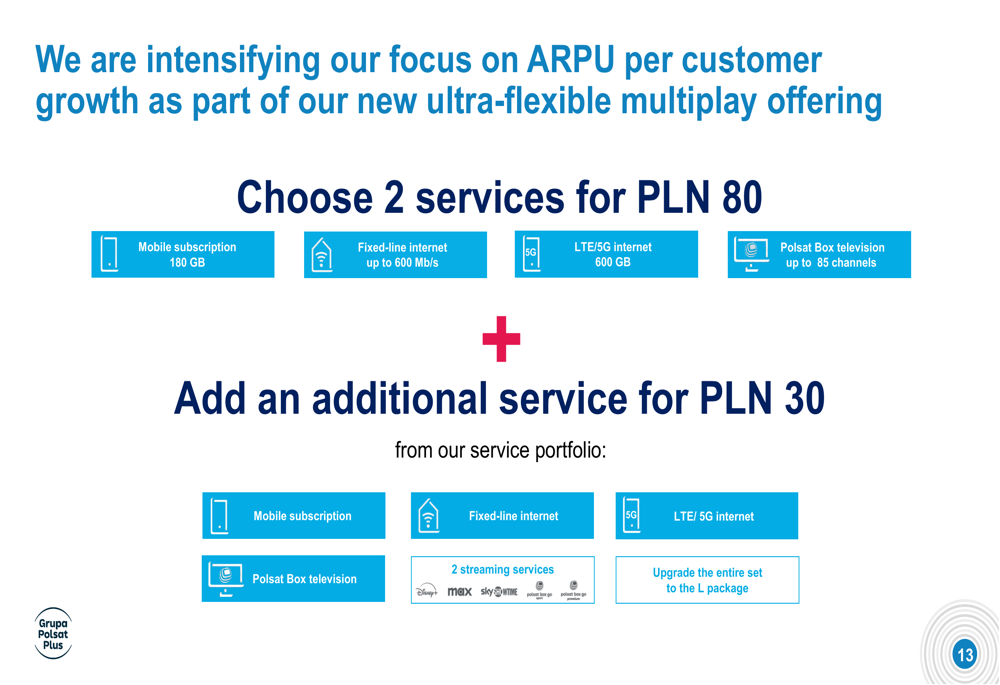

The B2C and B2B services segment introduced a new ultra-flexible multiplay offering, allowing customers to choose two services for PLN 80 with the option to add additional services for PLN 30 each.

The new offering is illustrated here:

The company has also redefined its multiplay customer definition to include any customer using at least two services from any company within the Group, resulting in over 3 million multiplay customers.

Green Energy Segment

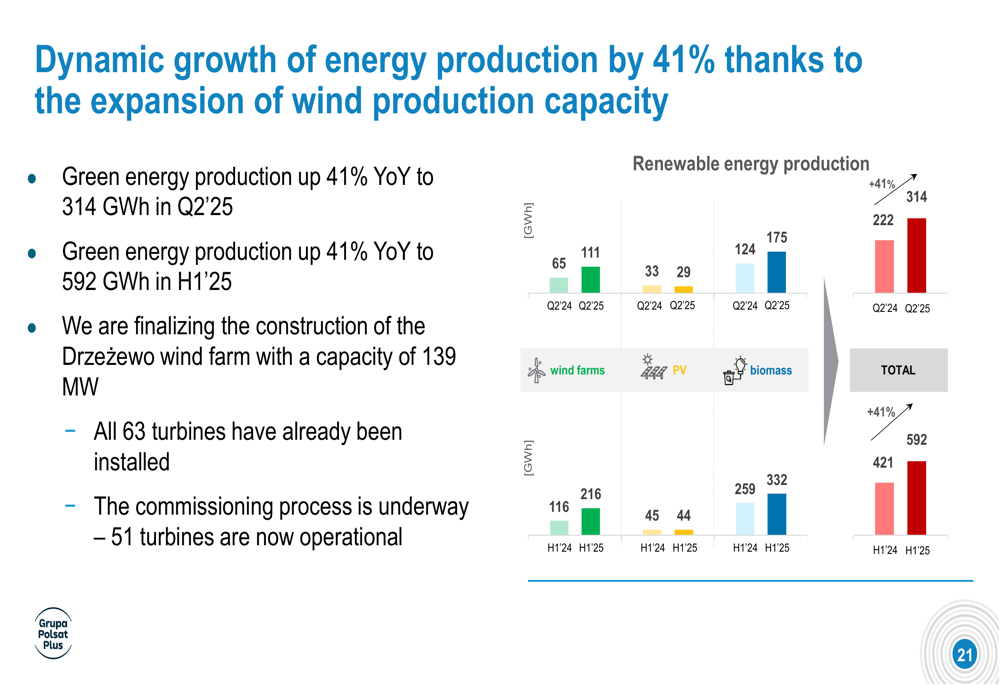

The green energy segment showed impressive growth, with production increasing by 41.4% year-over-year to 314 GWh in Q2 2025. This growth was primarily driven by increased production from wind farms (+71%) and biomass (+41%).

The following chart shows the breakdown of renewable energy production:

Despite the significant increase in production, EBITDA from the green energy segment slightly decreased by 7% to PLN 66 million in Q2 2025.

Financial Analysis

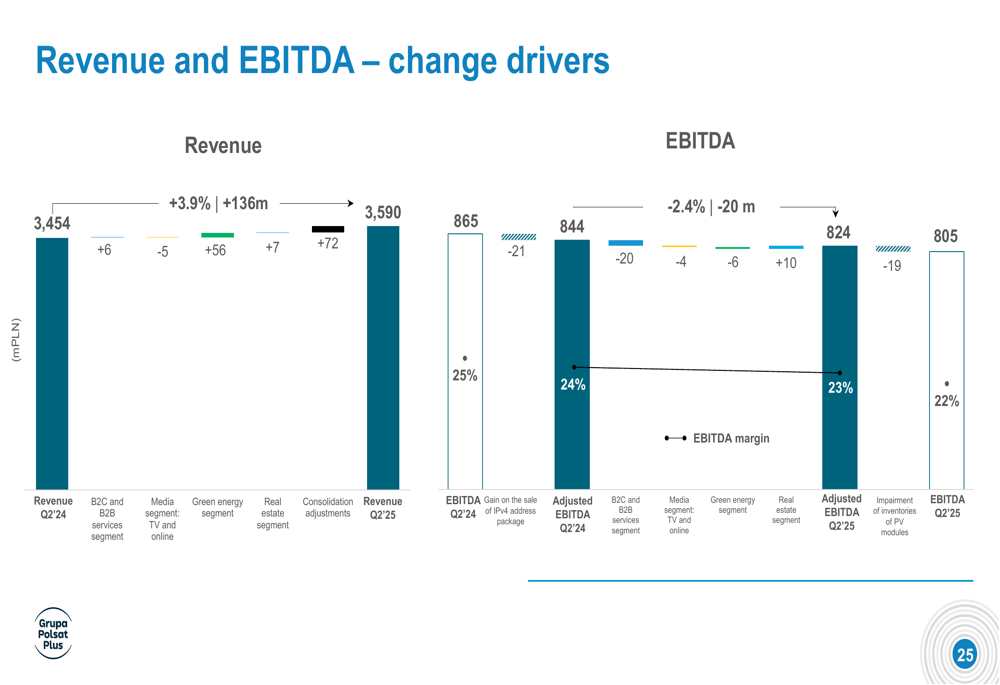

The company’s revenue growth of 3.9% was primarily driven by the green energy segment (+PLN 56 million) and consolidation adjustments (+PLN 72 million), while the B2C segment remained flat and the media segment slightly declined.

The following chart breaks down the revenue and EBITDA change drivers:

The adjusted EBITDA decline of 2.4% was attributed to the absence of a one-time gain on the sale of IPv4 addresses (-PLN 21 million) and an impairment charge on inventories of photovoltaic panels (-PLN 19 million).

The company’s overall financial results show the revenue growth alongside profit pressure:

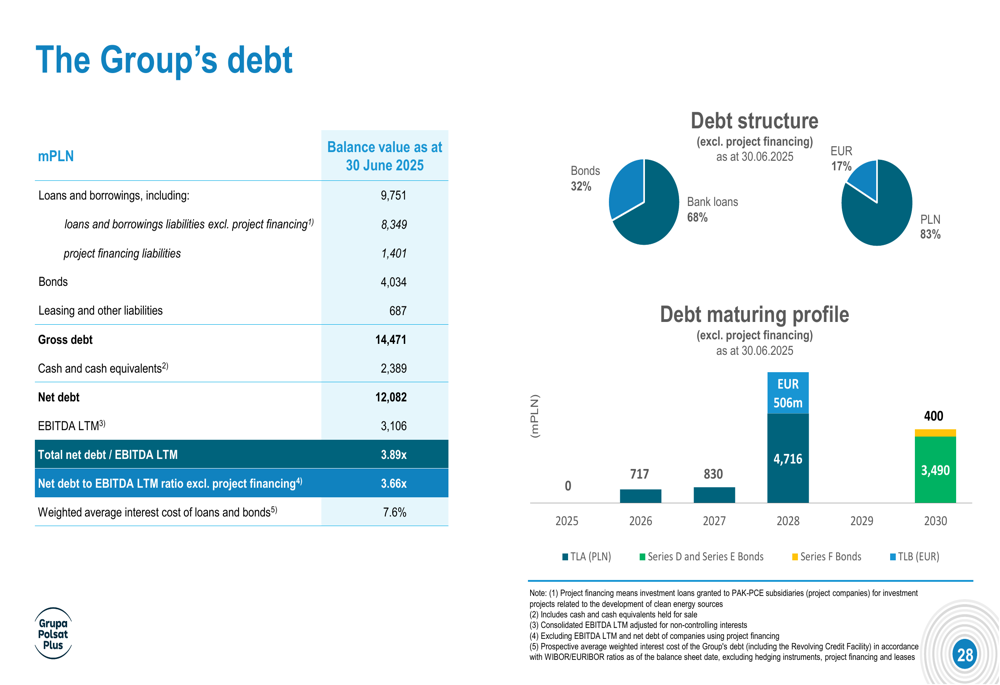

Polsat Plus maintained its debt levels with a net debt to EBITDA LTM ratio of 3.66x (excluding project financing), slightly up from 3.62x reported in Q1 2025. The weighted average interest cost of loans and bonds was 7.6%.

The debt structure and maturity profile is illustrated here:

Strategic Initiatives and Outlook

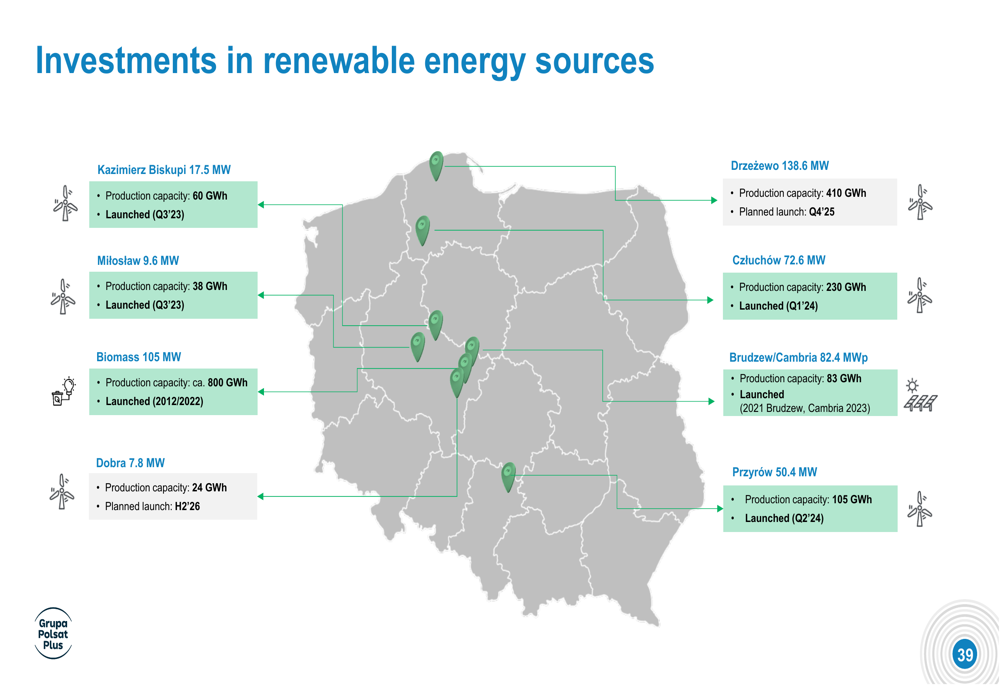

Polsat Plus continues to focus on its multiplay strategy and expansion of its green energy portfolio. The company is finalizing construction of the Drzeżewo wind farm and has secured project financing for this initiative.

The company’s renewable energy investments are spread across Poland, with multiple wind farms, biomass plants, and solar installations:

Management highlighted good operating and financial results for Q2 2025 despite the profit decline, emphasizing the strategic importance of the green energy segment and the enhanced multiplay offering as key drivers for future growth.

The company faces challenges from high interest costs, which impacted its free cash flow generation. However, Polsat Plus demonstrated continued cash generation capacity with an adjusted FCF LTM after interest of PLN 978 million (excluding green energy capex).

While the Q2 results show some pressure on profitability compared to the 5% EBITDA growth reported in Q1 2025, the company’s strategic positioning in both telecommunications and renewable energy provides diversification as it navigates a competitive market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.