Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Pool Corporation (NASDAQ:POOL) reported modest growth in its second quarter 2025 earnings presentation on July 24, showing signs of stabilization after a challenging first quarter. The swimming pool supplies distributor posted a 1% increase in net sales and a 4% rise in earnings per share, with strong performance in maintenance products offsetting continued weakness in discretionary spending categories.

Introduction & Market Context

Pool Corp ’s stock jumped 7.34% in premarket trading following the earnings release, signaling investor relief after the company’s disappointing Q1 results when it missed EPS expectations and saw its stock drop over 7%. The Q2 results suggest the company is successfully navigating a challenging environment where high interest rates continue to pressure new pool construction and renovation activities.

The company’s performance represents a notable improvement from Q1 2025, when Pool Corp reported a 4% year-over-year revenue decline and missed analyst EPS expectations with $1.32 versus the forecasted $1.48.

Quarterly Performance Highlights

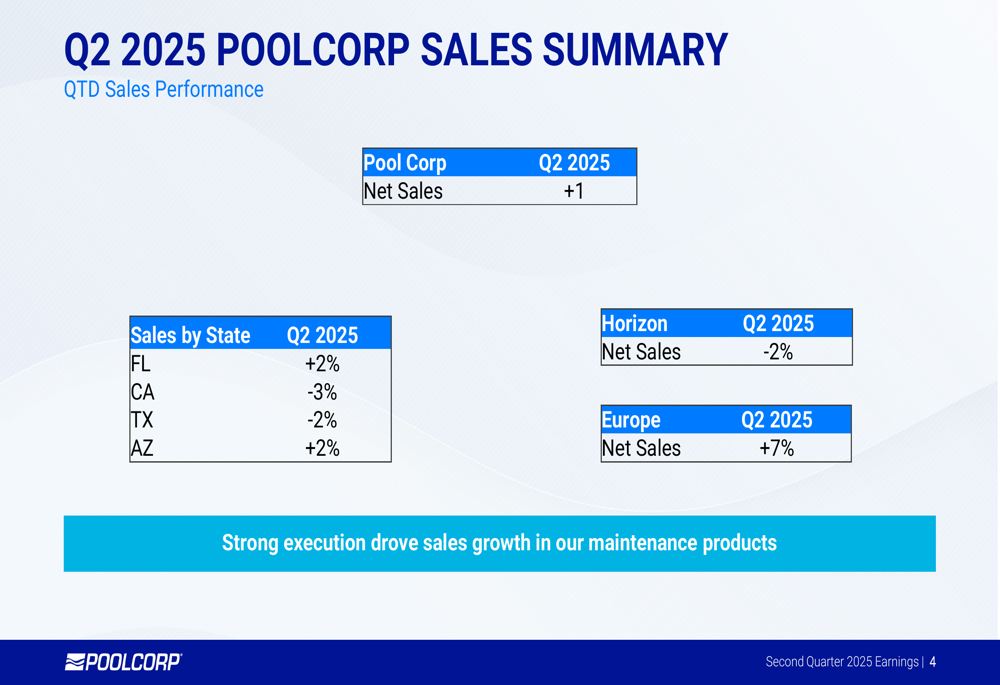

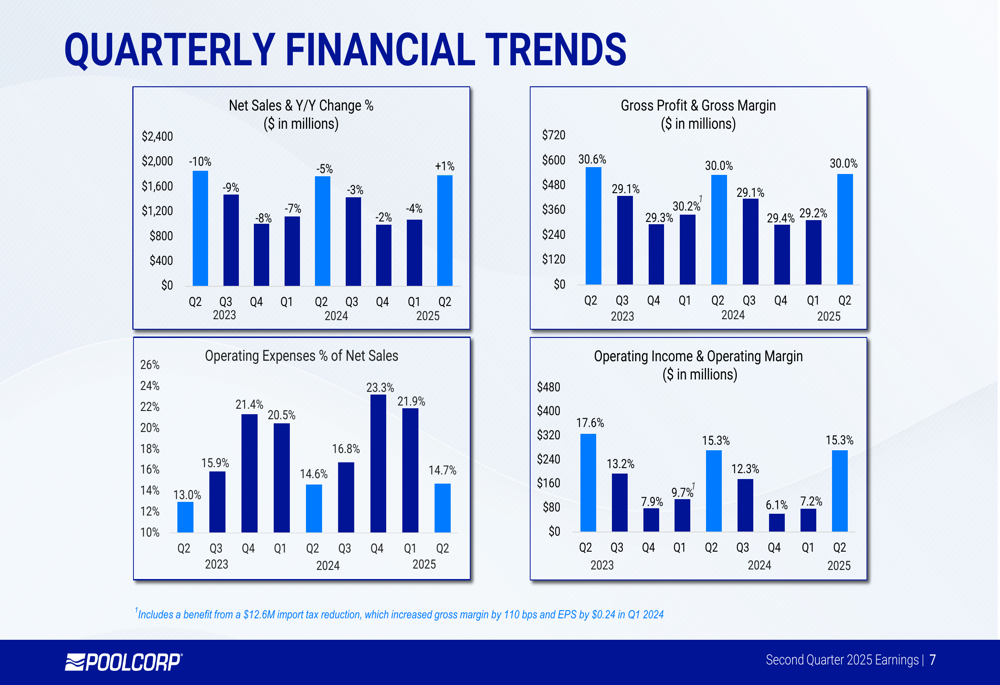

For Q2 2025, Pool Corp reported net sales of $1,784.5 million, a 1% increase compared to the same period in 2024. Operating income reached $272.7 million, up $1.2 million year-over-year, while maintaining an operating margin of 15.3%. Diluted earnings per share grew 4% to $5.17.

As shown in the following summary of quarterly results:

Gross profit increased by $5.0 million to $535.2 million, with gross margin holding steady at 30.0%. This stability in margins demonstrates the company’s ability to manage pricing and costs effectively despite inflationary pressures.

The company’s performance was driven by what it described as "strong execution" in maintenance products, which helped offset continued weakness in discretionary categories like new pool construction and remodeling.

Segment and Regional Performance

Pool Corp’s performance varied significantly by region and product category. Florida and Arizona each saw 2% growth, while California and Texas experienced declines of 3% and 2%, respectively. European operations were a bright spot with 7% net sales growth, while the company’s Horizon business segment declined by 2%.

The following breakdown illustrates these regional variations:

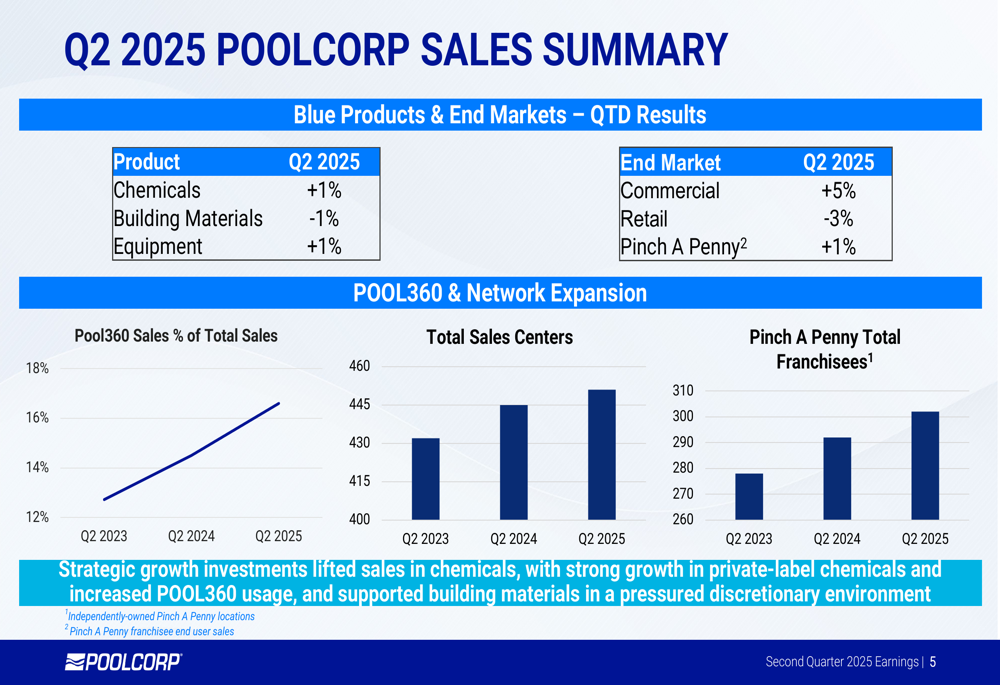

By product category, chemicals and equipment each grew by 1%, while building materials declined by 1%. The commercial segment showed strong 5% growth, contrasting with a 3% decline in retail. The company’s Pinch A Penny franchise business grew by 1%.

Pool Corp’s digital transformation continues to gain traction, with sales through its POOL360 platform increasing from approximately 12% of total sales in Q2 2023 to 16% in Q2 2025. The company also expanded its physical presence, growing from 435 total sales centers in Q2 2023 to 450 in Q2 2025, while Pinch A Penny franchisees increased from 270 to 290 over the same period.

The following chart illustrates these product and strategic growth trends:

Detailed Financial Analysis

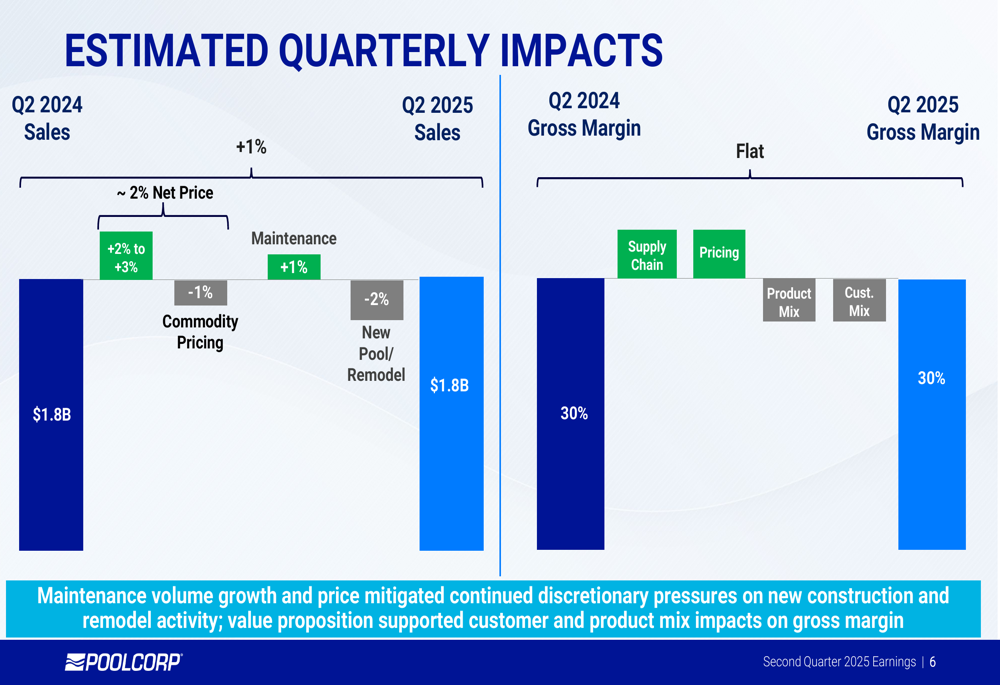

Pool Corp’s quarterly results were influenced by several factors. While the company implemented approximately 2% net price increases, this was partially offset by commodity pricing declines of 1% and a 2% decrease in new pool construction and remodel activity. Maintenance product sales grew by 1%, helping to balance these pressures.

The following chart breaks down these impacts on quarterly performance:

The company’s quarterly financial trends show a seasonal pattern typical of the pool industry, with performance improving from Q4 2023 through Q2 2025. This follows the challenging comparison to 2023, when the company was still benefiting from the post-pandemic pool boom.

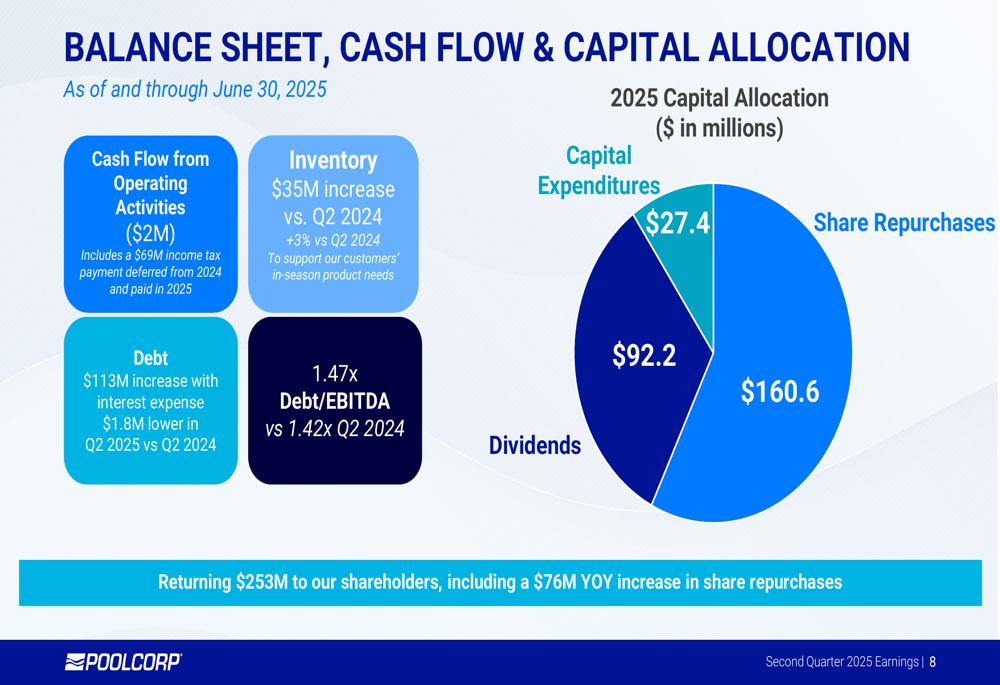

Balance Sheet and Capital Allocation

Pool Corp reported negative cash flow from operating activities of $2 million, which included a $69 million income tax payment deferred from 2024. Inventory increased by $35 million or 3% compared to Q2 2024, which the company attributed to supporting in-season product needs.

The company’s debt increased by $113 million, resulting in a debt-to-EBITDA ratio of 1.47x compared to 1.42x in Q2 2024. Despite the higher debt level, interest expense was $1.8 million lower in Q2 2025 compared to the same period last year.

Pool Corp continued to return significant capital to shareholders, with $160.6 million in share repurchases and $92.2 million in dividends during the quarter, as illustrated in the following capital allocation breakdown:

In total, the company returned $253 million to shareholders, including a $76 million year-over-year increase in share repurchases, demonstrating confidence in its long-term prospects despite near-term market challenges.

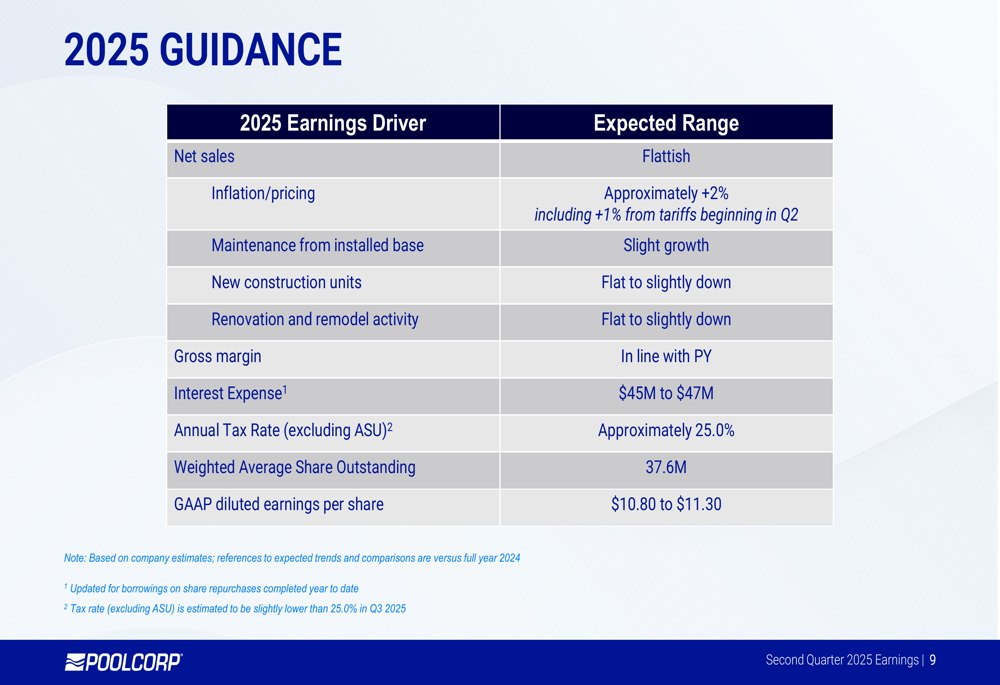

Forward Guidance

Looking ahead, Pool Corp maintained a cautious outlook for the remainder of 2025. The company expects "flattish" net sales for the full year, with approximately 2% inflation/pricing benefit, including 1% from tariffs that began in Q2. Maintenance from the installed base is projected to see slight growth, while new construction units and renovation/remodel activity are expected to be flat to slightly down.

The company provided the following detailed guidance for 2025:

Pool Corp narrowed its full-year diluted EPS guidance to $10.80-$11.30, compared to the $11.1-$11.6 range provided in its Q1 earnings call. This adjustment likely reflects both the Q2 performance and continued caution about discretionary spending in the second half of the year.

The company expects gross margins to remain in line with the prior year, with an annual tax rate of approximately 25.0% and weighted average shares outstanding of 37.6 million.

Despite the challenging environment for new pool construction and renovations, Pool Corp’s Q2 results demonstrate the resilience of its business model, particularly in the maintenance segment which provides recurring revenue. The company’s strategic investments in digital capabilities, network expansion, and private-label products position it well for when discretionary spending eventually recovers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.