S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Popular Inc . (NASDAQ:BPOP) released its second quarter 2025 investor presentation on July 23, showing substantial improvement across key financial metrics and prompting management to raise guidance for the full year. The Puerto Rico-based financial institution reported net income of $210 million, an 18% increase from both the previous quarter and the same period last year, as the bank capitalized on expanding interest margins and improved credit quality.

The results build on the positive momentum seen in Q1 2025, when the company beat earnings expectations with an EPS of $2.56. Popular’s stock has performed strongly in 2025, trading near its 52-week high of $116.80, reflecting investor confidence in the company’s execution and financial strength.

Quarterly Performance Highlights

Popular delivered impressive results across its key performance indicators for Q2 2025. Earnings per share reached $3.09, up significantly from $2.56 in Q1 2025 and $2.47 in Q2 2024. The bank’s return on tangible common equity (ROTCE) improved to 13.26%, compared to 11.36% in the previous quarter.

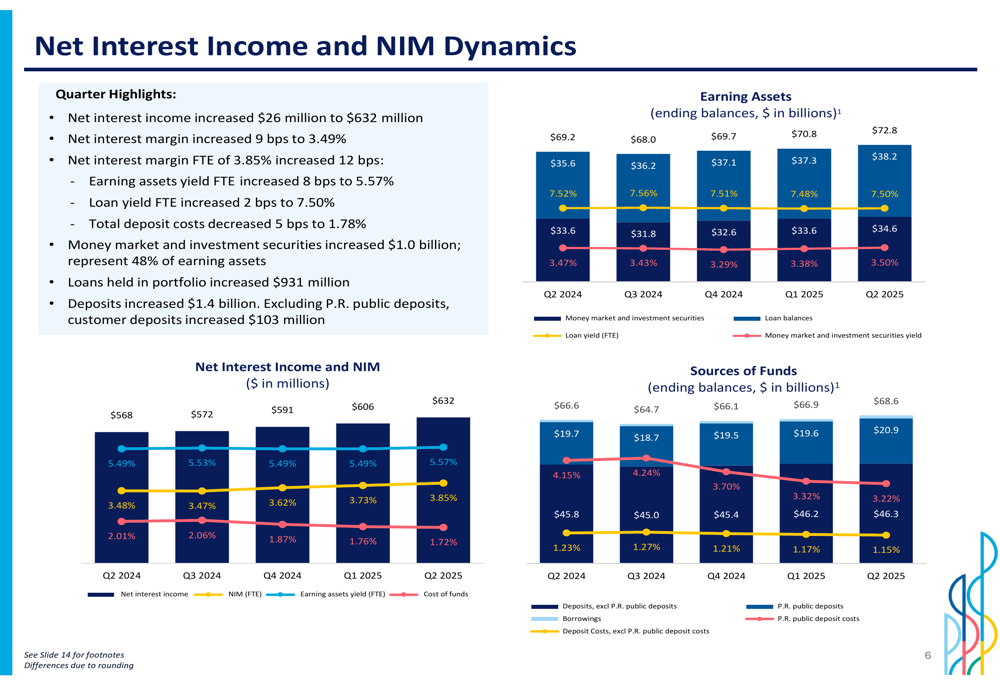

Net interest margin, a crucial profitability metric for banks, expanded 9 basis points to 3.49%, while the fully taxable equivalent NIM increased 12 basis points to 3.85%. This expansion was driven by higher yields on earning assets and lower deposit costs, which decreased 5 basis points during the quarter.

As shown in the following chart detailing net interest income and NIM dynamics, Popular has achieved consistent improvement in these metrics over recent quarters:

Loan growth remained robust, with the portfolio increasing by $931 million or 2.5% during the quarter, primarily driven by commercial and construction loans at both the Puerto Rico and U.S. operations. Total (EPA:TTEF) deposits grew by $1.4 billion or 2.1%, with public deposits in Puerto Rico accounting for most of the increase.

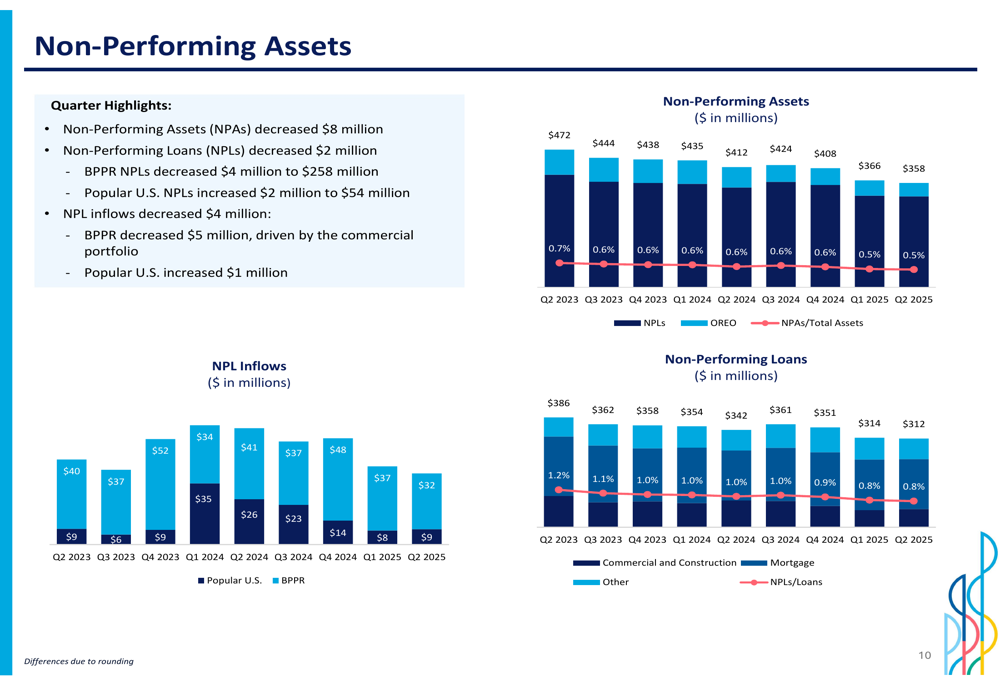

Credit quality metrics showed notable improvement, with non-performing loans decreasing to $312 million (0.82% of total loans) from $314 million (0.84%) in the previous quarter. The net charge-off ratio improved to 0.45% from 0.53% in Q1 2025.

Detailed Financial Analysis

Popular’s financial performance was strong across both its Puerto Rico (BPPR) and U.S. mainland operations. BPPR saw loans increase by $681 million, with growth across all major categories including commercial, construction, mortgage, auto, and credit card portfolios. The segment’s net interest margin improved 5 basis points to 3.68%.

The U.S. operation experienced loan growth of $251 million, primarily in commercial and construction loans, while its NIM expanded 19 basis points to 2.93%. The following breakdown illustrates the performance by region:

Non-interest income increased to $168.5 million in Q2 2025 from $152.1 million in Q1 2025, with improvements across multiple fee categories as shown in the following chart:

Operating expenses rose to $492.8 million from $471.0 million in the previous quarter. Despite the increase, the bank’s efficiency metrics remained solid, with strong revenue growth offsetting higher costs.

Popular maintains a robust capital position, with a Common Equity Tier 1 ratio of 15.91% as of Q2 2025, well above regulatory requirements, though slightly down from 16.11% in the previous quarter due to share repurchases and balance sheet growth. The following chart details the capital ratios across the organization:

Strategic Initiatives & Forward Guidance

Based on the strong first-half performance, Popular has revised its full-year 2025 guidance upward in several key areas. The company now expects net interest income to grow 10-11% year-over-year, up from the original projection of 7-9%. Net charge-offs are now forecast at 45-65 basis points annualized, an improvement from the initial guidance of 70-90 basis points.

The company also raised its outlook for non-interest income to the higher end of its original $155-160 million quarterly range, while slightly increasing its operating expense growth projection to 4-5% for the year, up from 4% previously. The following chart details the updated guidance:

Popular continues to focus on its position as a market leader in Puerto Rico, leveraging its substantial capital base and diversified deposit structure. The company’s U.S. mainland operations provide important geographic diversification, while initiatives to transform the company’s technology and customer service capabilities remain priorities.

Capital Management & Shareholder Returns

Popular demonstrated its commitment to shareholder returns through significant capital actions announced during the quarter. The company repurchased $112 million in common stock at an average price of $98.54 per share during Q2 2025.

On July 16, 2025, Popular announced a new common stock repurchase program of up to $500 million, with approximately $32.8 million still available under the previous 2024 repurchase program as of July 15, 2025. Additionally, the company increased its quarterly common stock dividend from $0.70 to $0.75 per share, effective with the dividend payable in the fourth quarter of 2025, subject to board approval.

The bank’s tangible book value per share increased $3.39 to $75.41 during the quarter, reflecting continued value creation for shareholders. The following chart shows the improvement in non-performing assets, which has contributed to the bank’s strong performance:

Popular’s deposit composition remains a strength, with a diversified funding base that includes significant public deposits in Puerto Rico. The following chart illustrates the deposit composition and cost trends:

With its strong capital position, improving profitability metrics, and positive guidance revisions, Popular appears well-positioned to continue delivering value to shareholders while maintaining its leadership position in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.