Stock market today: Stocks fall as investors rotate out of tech into Jackson Hole

Introduction & Market Context

Portillo’s Inc (NASDAQ:PTLO) released its first quarter 2025 earnings presentation on May 6, 2025, revealing 6.4% revenue growth but showing signs of margin pressure. The Chicago-based fast-casual restaurant chain known for its hot dogs, Italian beef sandwiches, and chocolate cake saw its stock decline 4.62% to $9.92 following the release, despite reporting improved same-restaurant sales growth.

The presentation comes after a strong fourth quarter 2024 performance that had previously driven the stock up 9.58%, highlighting the market’s shifting sentiment as investors digest the latest financial metrics and expansion plans.

Quarterly Performance Highlights

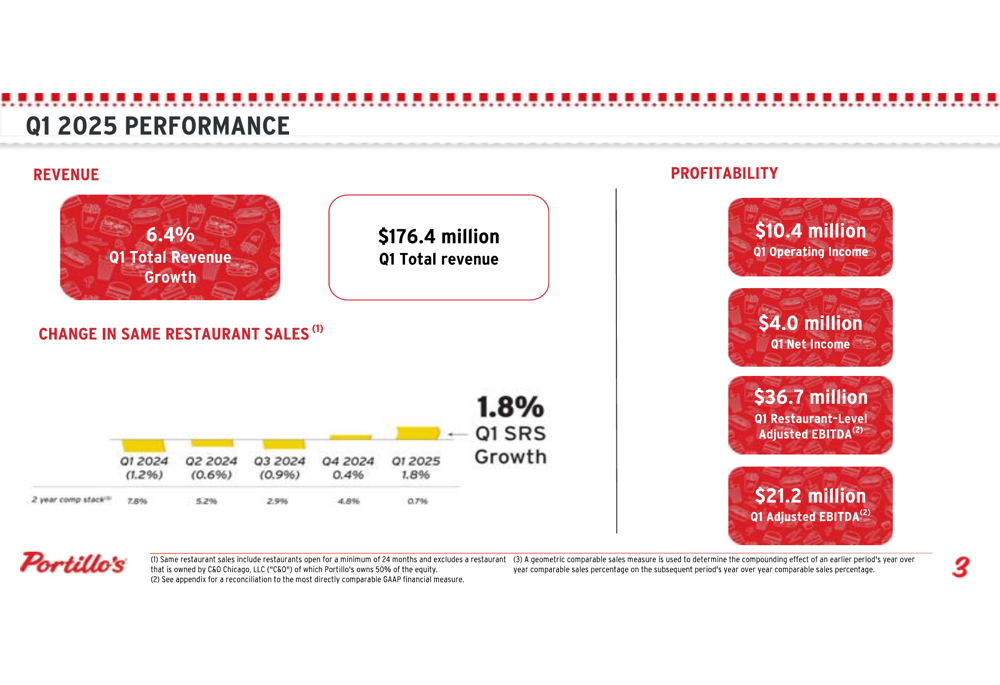

Portillo’s reported total revenue of $176.4 million for Q1 2025, representing a 6.4% year-over-year increase from $165.8 million in Q1 2024. Same-restaurant sales growth rebounded to 1.8%, a significant improvement from the -1.2% reported in the same quarter last year.

As shown in the following performance highlights:

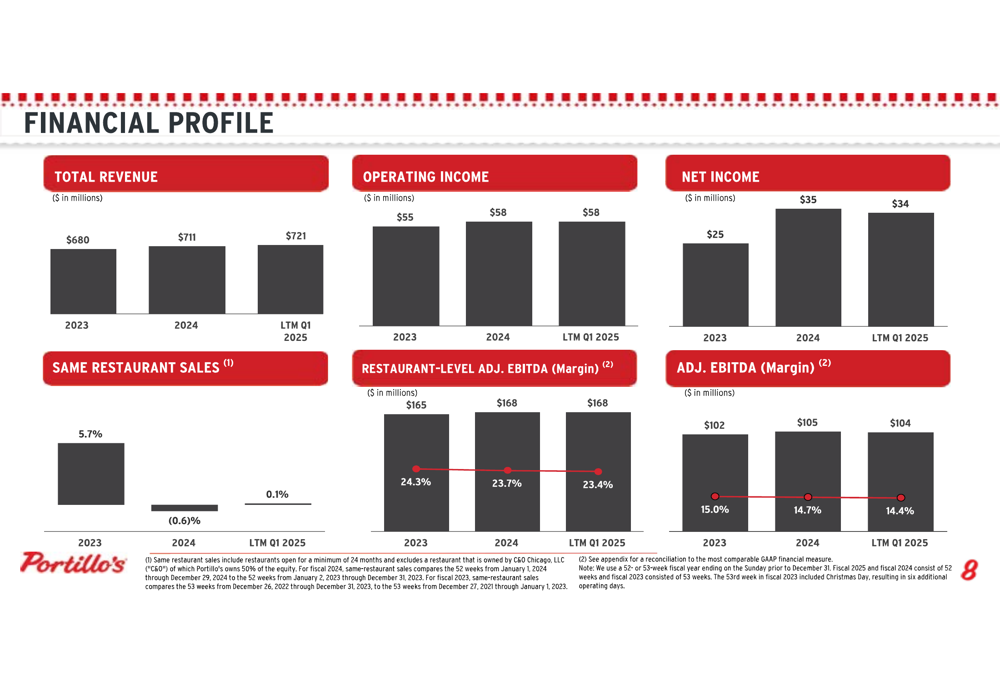

Despite the revenue growth, Portillo’s experienced margin compression during the quarter. Operating income reached $10.4 million (5.9% margin), slightly up from $10.1 million (6.1% margin) in Q1 2024. Net income declined to $4.0 million (2.3% margin) from $5.3 million (3.2% margin) in the prior-year period.

Restaurant-Level Adjusted EBITDA was $36.7 million with a margin of 20.8%, compared to $36.4 million with a margin of 21.9% in Q1 2024. Similarly, Adjusted EBITDA decreased to $21.2 million (12.0% margin) from $21.8 million (13.1% margin).

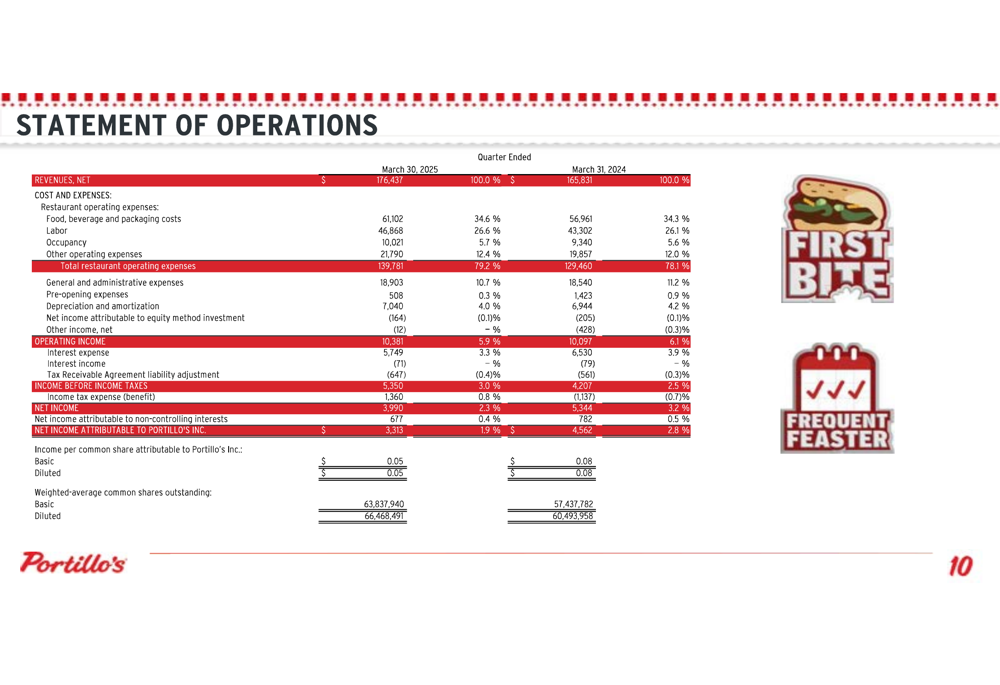

The company’s detailed statement of operations reveals the financial performance comparison:

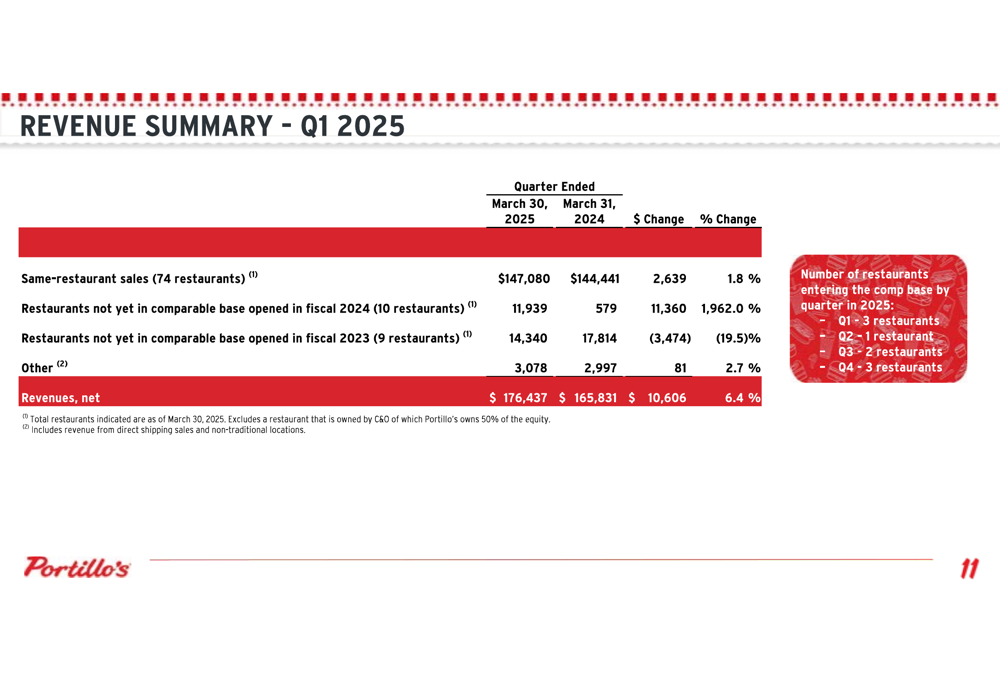

A closer examination of Portillo’s revenue sources shows that the 74 restaurants in the comparable base generated $147.1 million, up 1.8% year-over-year, while the 10 restaurants opened in fiscal 2024 contributed $11.9 million:

Expansion Plans

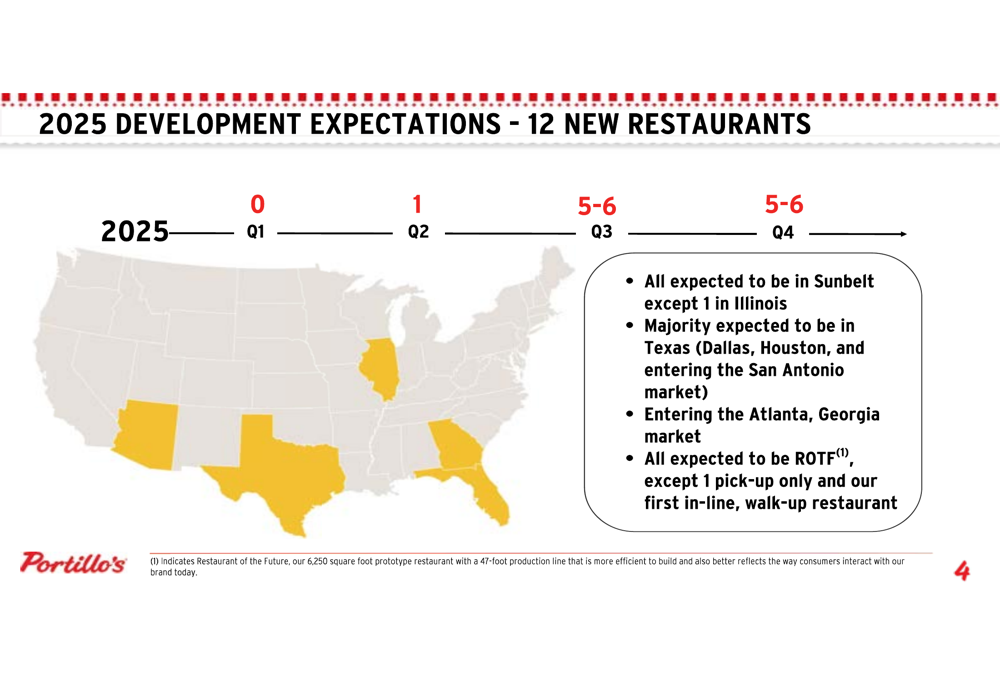

Portillo’s ambitious growth strategy is centered on opening 12 new restaurants in 2025, with the majority planned for the second half of the year. The expansion is heavily focused on the Sunbelt region, particularly Texas, where the company is strengthening its presence in Dallas and Houston while entering the San Antonio market. Additionally, Portillo’s will enter the Atlanta, Georgia market for the first time.

The company’s development expectations are illustrated in this geographic expansion map:

Most new locations will feature the company’s "Restaurant of the Future" (ROTF) format, with the exception of one pick-up only location and the company’s first in-line, walk-up restaurant. This diversification of formats demonstrates Portillo’s adaptation to changing consumer preferences and urban environments.

Financial Targets and Long-Term Strategy

For fiscal year 2025, Portillo’s has set specific financial targets including same-restaurant sales growth of 1% to 3% and overall revenue growth of 10% to 12%. The company expects to face commodity inflation of 3% to 5% and labor inflation of 3% to 4%, challenging its margin management.

The detailed financial targets for 2025 include:

Looking beyond 2025, Portillo’s outlined its long-term growth algorithm targeting annual unit growth of 12% to 15%, low single-digit same-restaurant sales growth, and mid-teens revenue growth. The company aims to achieve low-teens adjusted EBITDA growth over the long term.

The company’s financial profile shows steady revenue growth over recent years, with total revenue increasing from $680 million in 2023 to $711 million in 2024, and $721 million for the last twelve months ending Q1 2025:

Challenges and Outlook

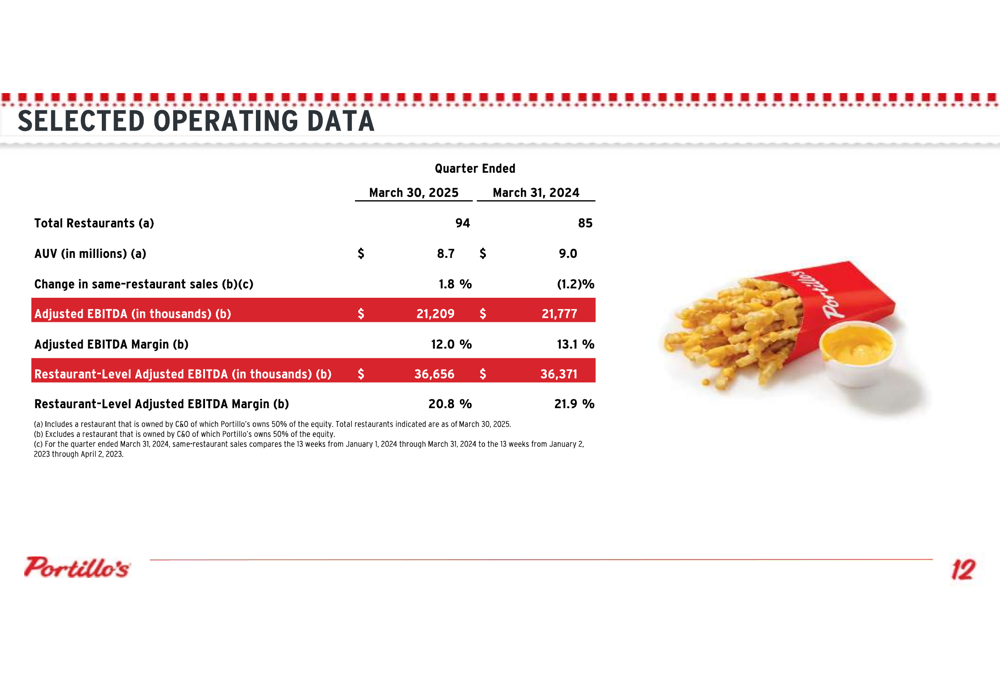

While Portillo’s is demonstrating revenue growth and ambitious expansion plans, the company faces several challenges. The decline in average unit volume (AUV) from $9.0 million in Q1 2024 to $8.7 million in Q1 2025 suggests potential cannibalization or operational challenges in newer markets.

The company’s selected operating data highlights these metrics:

Margin compression remains a concern as both Restaurant-Level Adjusted EBITDA Margin and Adjusted EBITDA Margin declined year-over-year. The company will need to navigate rising commodity and labor costs effectively to achieve its targeted Restaurant-Level Adjusted EBITDA Margin of 22.5% to 23% for 2025, up from the 20.8% reported in Q1.

Portillo’s strategic pillars focus on running world-class operations, innovating the customer experience, developing restaurants with industry-leading returns, and taking care of its teams. The success of these initiatives will be crucial as the company accelerates its expansion into new markets where brand awareness may be lower than in its Midwest stronghold.

With capital expenditures projected at $97-$100 million for 2025 and pre-opening expenses of $11-$12 million, Portillo’s is making significant investments in its growth strategy. Investors will be watching closely to see if these investments translate into improved profitability and sustained same-restaurant sales growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.