U.S. stocks lower as investors rotate out of tech ahead of Jackson Hole

Introduction & Market Context

Poste Italiane (BIT:PST) presented its Q2 and H1 2025 financial results on July 22, 2025, revealing record performance across all business segments. The company’s stock has been trading near the middle of its 52-week range, with the latest results potentially providing further momentum following the strong Q1 performance reported earlier this year.

The Italian postal and financial services giant reported record H1 revenues of €6.46 billion, continuing the positive trajectory established in Q1 when the company achieved its highest first-quarter revenue in history. The results reflect Poste Italiane’s successful diversification strategy and its growing presence in financial services, insurance, and digital payments.

Executive Summary

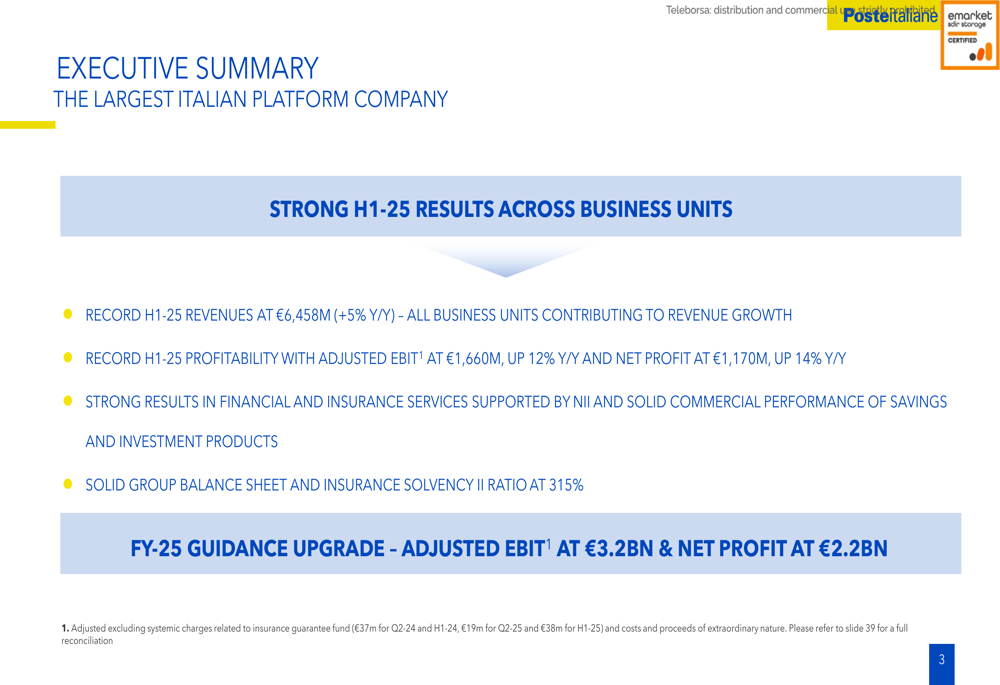

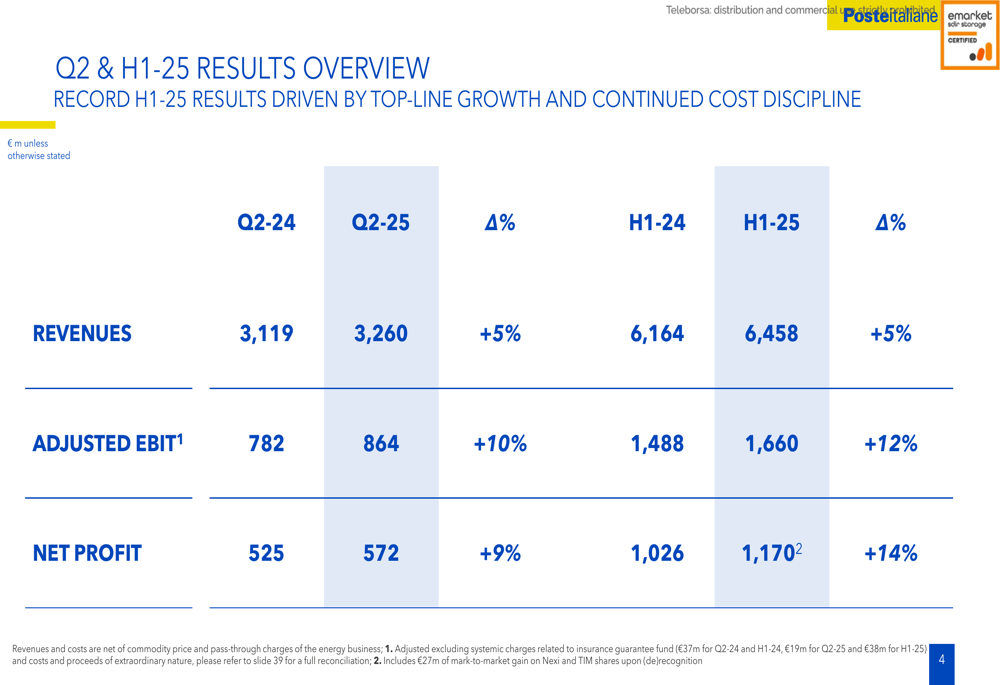

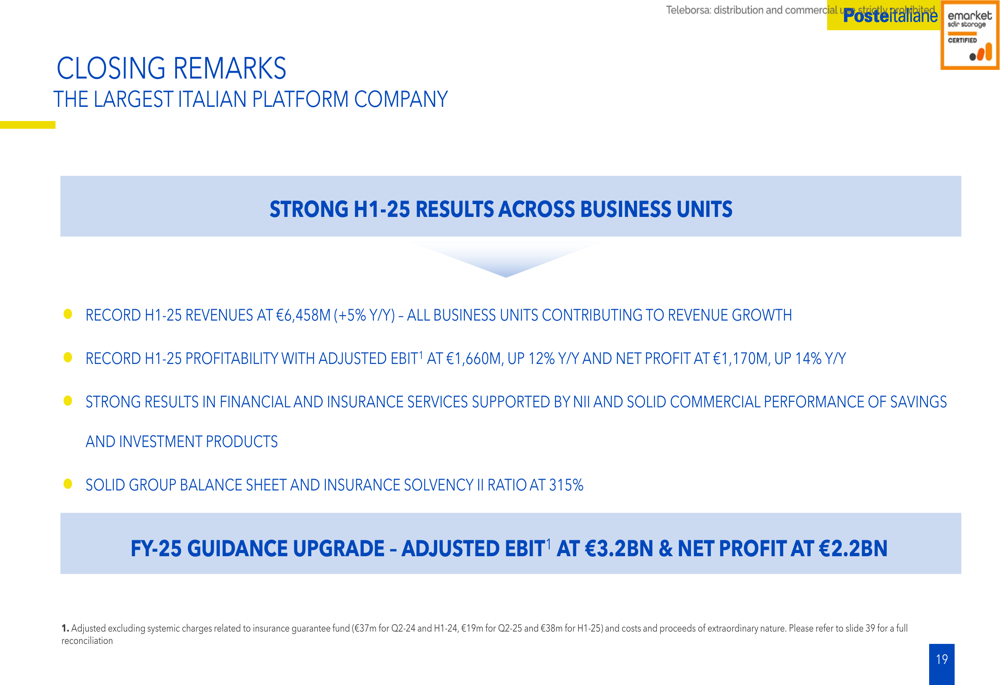

Poste Italiane delivered exceptional financial performance in the first half of 2025, with all business units contributing to growth. The company achieved record H1 revenues of €6,458 million, representing a 5% increase year-over-year, while adjusted EBIT surged 12% to €1,660 million and net profit rose 14% to €1,170 million.

As shown in the following comprehensive results overview:

The strong performance has prompted Poste Italiane to upgrade its full-year 2025 guidance, with adjusted EBIT now expected to reach €3.2 billion and net profit projected at €2.2 billion. This upgrade builds on the momentum established in Q1 2025, when the company reported a 13% year-on-year increase in adjusted EBIT to €796 million.

The detailed breakdown of Q2 and H1 results shows consistent growth across key metrics:

Detailed Financial Analysis

Revenue by Business Unit

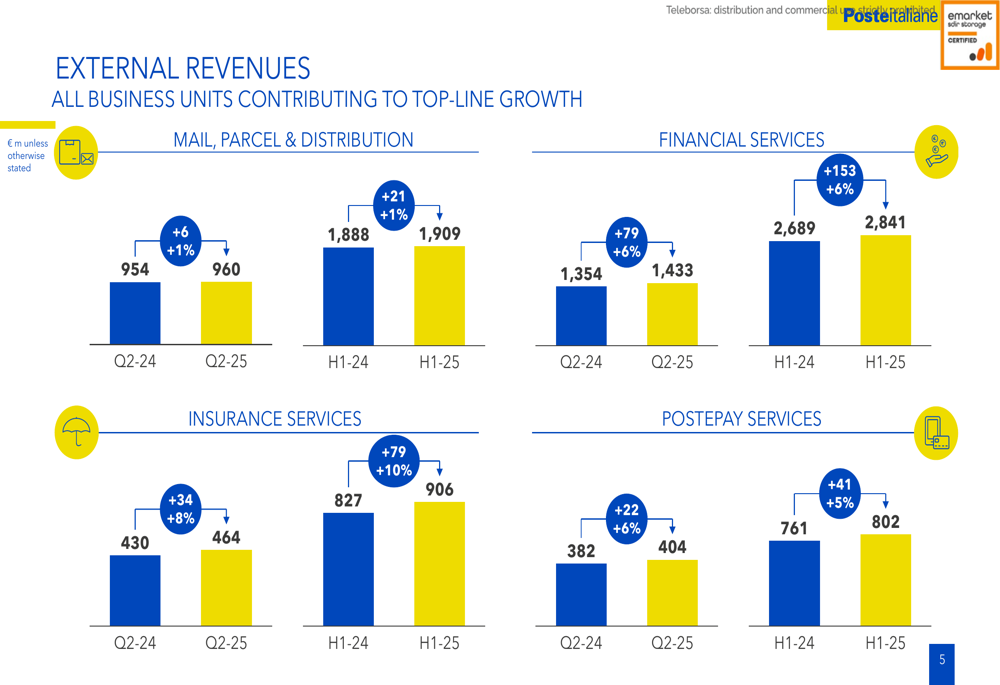

All four of Poste Italiane’s business segments contributed to revenue growth in H1 2025. Financial Services remained the largest contributor with €2,841 million (+6% Y/Y), followed by Mail, Parcel & Distribution with €1,909 million (+1% Y/Y), Insurance Services with €906 million (+10% Y/Y), and Postepay Services with €802 million (+5% Y/Y).

The following chart illustrates the revenue contribution by business unit:

Segment Profitability

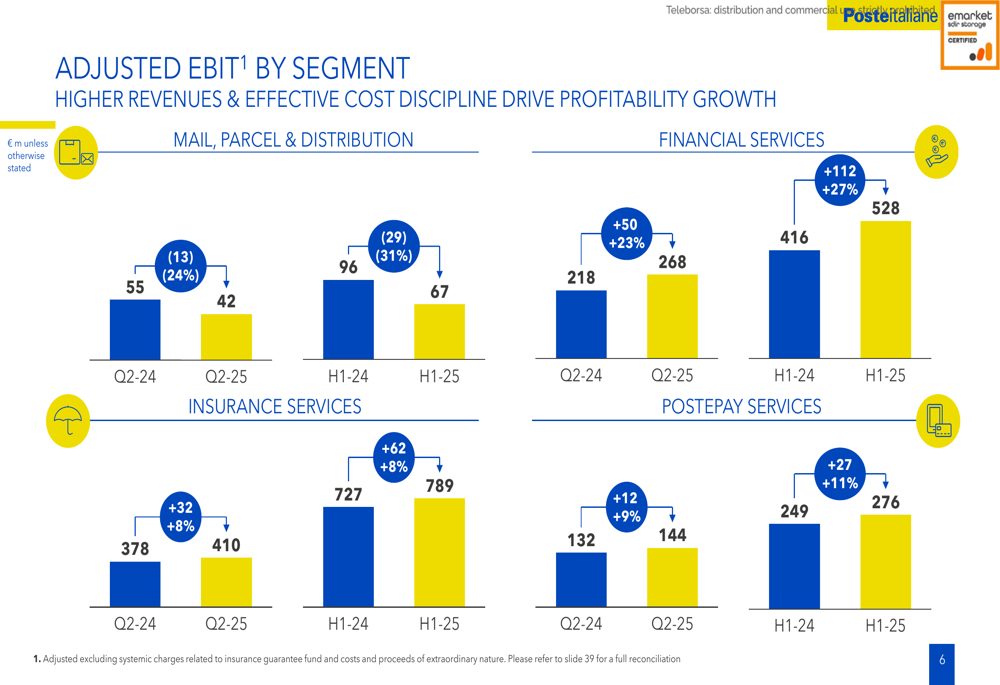

While all segments contributed to revenue growth, profitability varied across business units. Financial Services showed the strongest EBIT growth, increasing by 27% year-over-year to €528 million in H1 2025. Insurance Services EBIT grew by 9% to €789 million, and Postepay Services EBIT rose by 11% to €276 million. However, Mail, Parcel & Distribution EBIT declined to €67 million from €96 million in H1 2024.

The following chart details adjusted EBIT by segment:

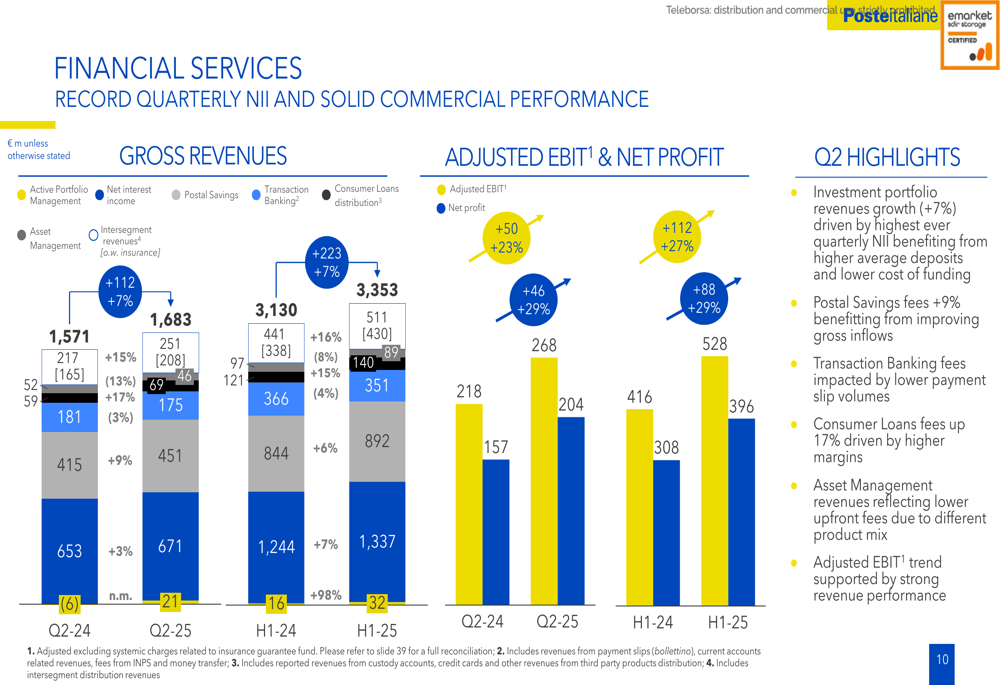

Financial Services Performance

The Financial Services segment delivered particularly strong results, driven by record net interest income and improved commercial performance. Gross revenues increased across all categories, with active portfolio management, net interest income, and postal savings all showing significant growth.

As illustrated in the detailed breakdown of Financial Services performance:

The segment benefited from the highest ever quarterly net interest income, supported by higher average deposits and lower cost of funding. Postal savings fees increased by 9%, reflecting improving gross inflows, while consumer loans fees grew by 17% due to higher margins.

Insurance Services

Insurance Services continued to show strong commercial performance and profitability across Life & Protection products. The segment benefited from positive net flow trends, driven by strong gross written premiums (+20% Y/Y) with an increased share of multiclass products.

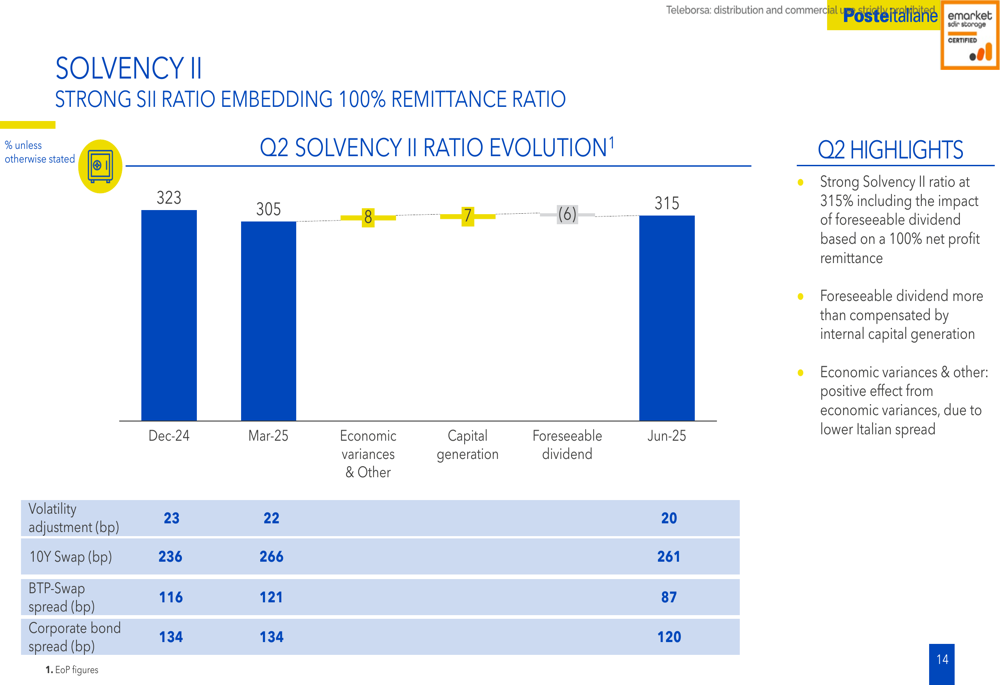

The company maintains a strong Solvency II ratio of 315%, providing a solid foundation for future growth:

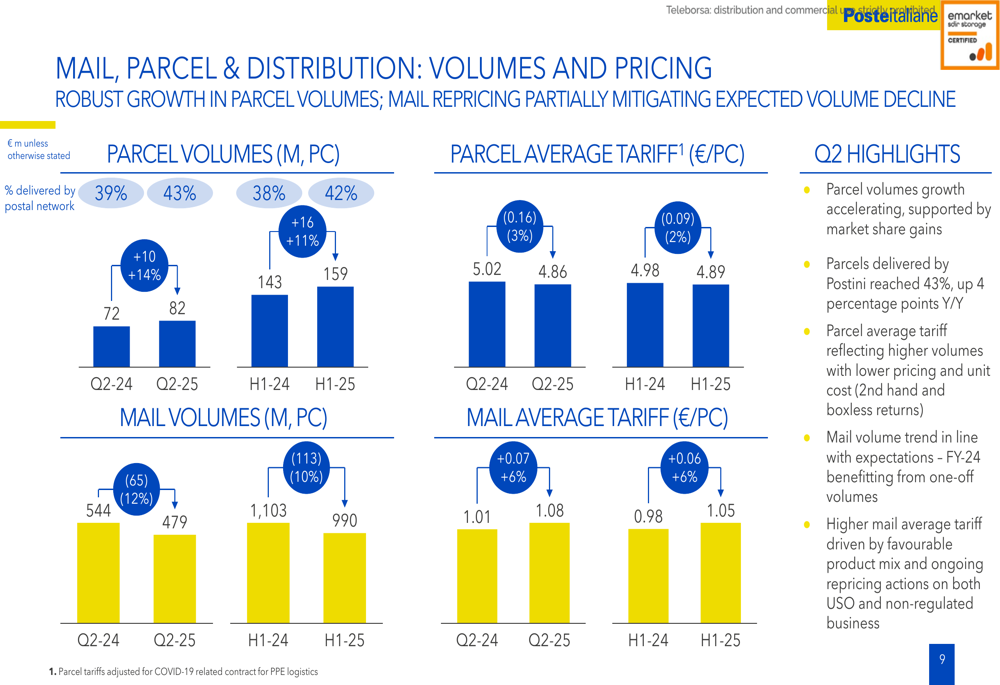

Mail, Parcel & Distribution

The Mail, Parcel & Distribution segment showed mixed results. While parcel volumes growth accelerated, supported by market share gains, mail volumes continued their expected decline. The segment’s adjusted EBIT was impacted by lower distribution rebates, though management indicated it was progressing in line with FY-25 guidance.

Parcel volumes and pricing trends show the evolving nature of this business:

Parcels delivered by Postini (postal carriers) reached 43% in Q2 2025, up 4 percentage points year-over-year, demonstrating the company’s continued focus on last-mile delivery optimization. The parcel average tariff reflected higher volumes with lower pricing and unit cost, particularly in second-hand and boxless returns.

Strategic Initiatives

A key strategic development for Poste Italiane is its investment in TIM ( Telecom Italia (BIT:TLIT)). The company now holds a 24.8% shareholding in TIM’s ordinary share capital, representing 17.8% of total share capital. This investment, valued at €1,278 million as of June 30, 2025, aligns with the strategic market consolidation efforts mentioned in the Q1 earnings report.

The TIM investment is accounted for using the equity method, with TIM’s pro-rata net result accounted below EBIT in the Mail, Parcel & Distribution segment. This strategic positioning in telecommunications could provide synergies with Poste Italiane’s existing services and create additional growth opportunities.

Forward-Looking Statements

Based on the strong H1 2025 performance, Poste Italiane has upgraded its full-year guidance, now projecting adjusted EBIT of €3.2 billion and net profit of €2.2 billion. This represents a significant increase from previous projections and builds on the company’s Q1 guidance, which anticipated parcel revenues reaching €1.8 billion (growth of 10-16%) and insurance premiums between €1.1 billion and €1.2 billion.

The company’s closing remarks highlight the key achievements and outlook:

Poste Italiane maintains a solid group balance sheet with strong cash generation and ample liquidity. The company’s BancoPosta division shows a solid capital position with a Total (EPA:TTEF) Capital Ratio of 22.7% as of June 2025, providing a strong foundation for continued growth and shareholder returns.

While the mail market continues to face long-term volume declines, Poste Italiane’s diversified business model and strategic investments position it well for sustainable growth. The integration and realization of synergies from the TIM investment will be a key area to watch, as will the company’s ability to maintain momentum in its financial and insurance services segments amid changing market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.