Jamaica’s outlook revised to stable by Fitch after hurricane

Introduction & Market Context

Poste Italiane (BIT:PST) presented its second quarter and first half 2025 financial results on July 22, showcasing record performance across its diversified business portfolio. The company, which positions itself as "the largest Italian platform company," reported strong growth in revenues and profitability, leading to an upgrade in its full-year guidance.

The stock responded positively to the results, with shares rising 0.89% to €11.36 following the announcement. Currently trading at $22.06, the stock offers a 3.82% dividend yield but remains 11.7% below its 52-week high of $25.04, suggesting potential upside for investors.

Executive Summary

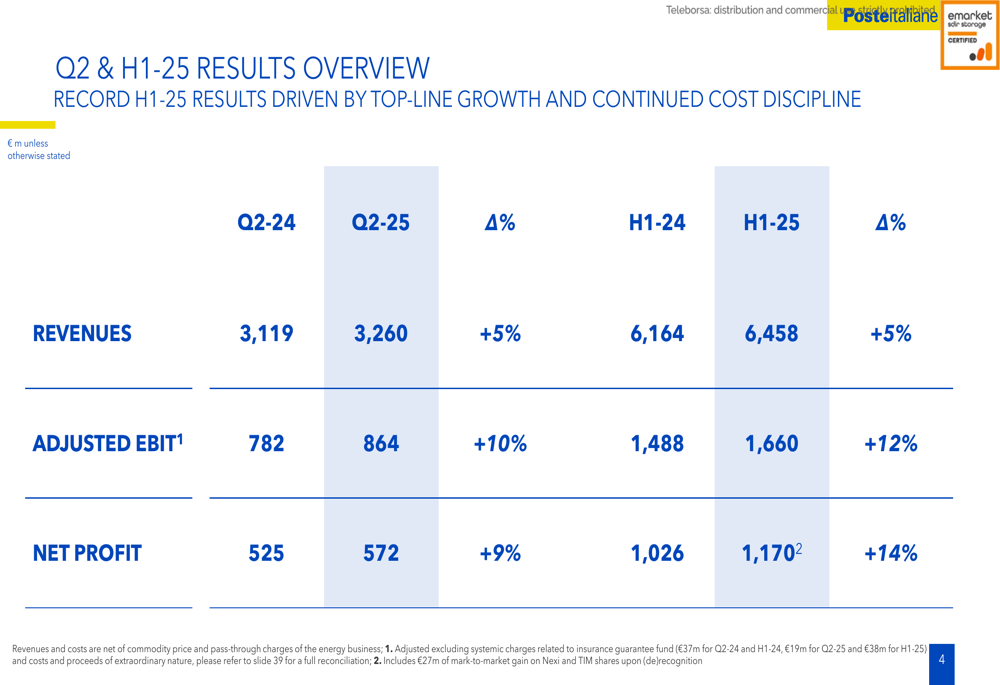

Poste Italiane delivered exceptional financial results for H1 2025, with record revenues of €6,458 million, representing a 5% year-over-year increase. This growth was complemented by a 12% rise in adjusted EBIT to €1,660 million and a 14% increase in net profit to €1,170 million.

The strong performance was driven by contributions from all business units, with particularly robust results in Financial and Insurance Services. These results have enabled the company to upgrade its full-year guidance, with adjusted EBIT now expected to reach €3.2 billion and net profit projected at €2.2 billion.

As shown in the following comprehensive financial overview:

Quarterly Performance Highlights

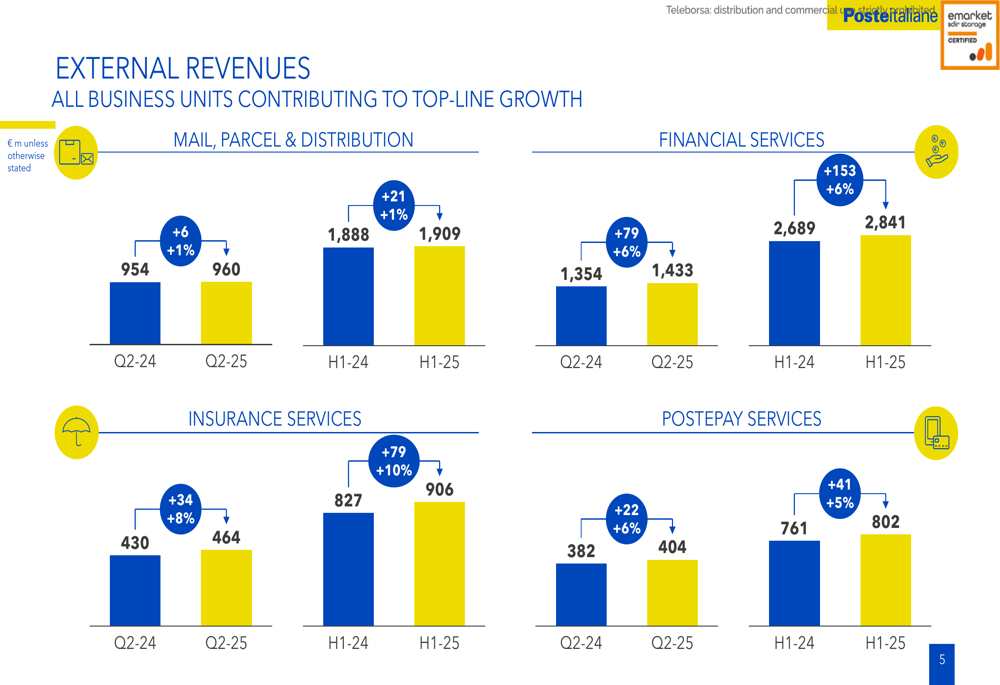

The company's diversified business model demonstrated its strength, with all segments contributing to revenue growth. External revenues by business unit showed positive trends across the board, with Insurance Services leading the way with a 10% increase in H1 2025 compared to the same period last year.

The breakdown of external revenues by business unit illustrates the balanced growth across Poste Italiane's operations:

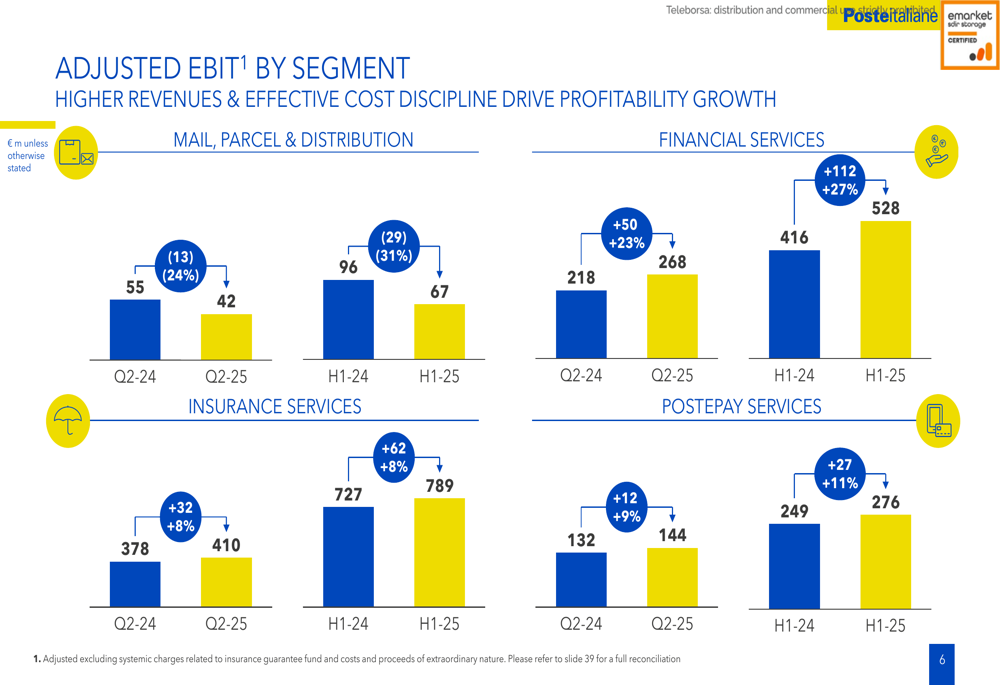

While revenues grew across all segments, profitability varied. Financial Services and Insurance Services were standout performers, with adjusted EBIT growth of 27% and 8% respectively in H1 2025. However, the Mail, Parcel & Distribution segment experienced a 31% decline in adjusted EBIT, reflecting challenges in the traditional postal business.

The following chart details the adjusted EBIT performance by segment:

Detailed Financial Analysis

Mail, Parcel & Distribution

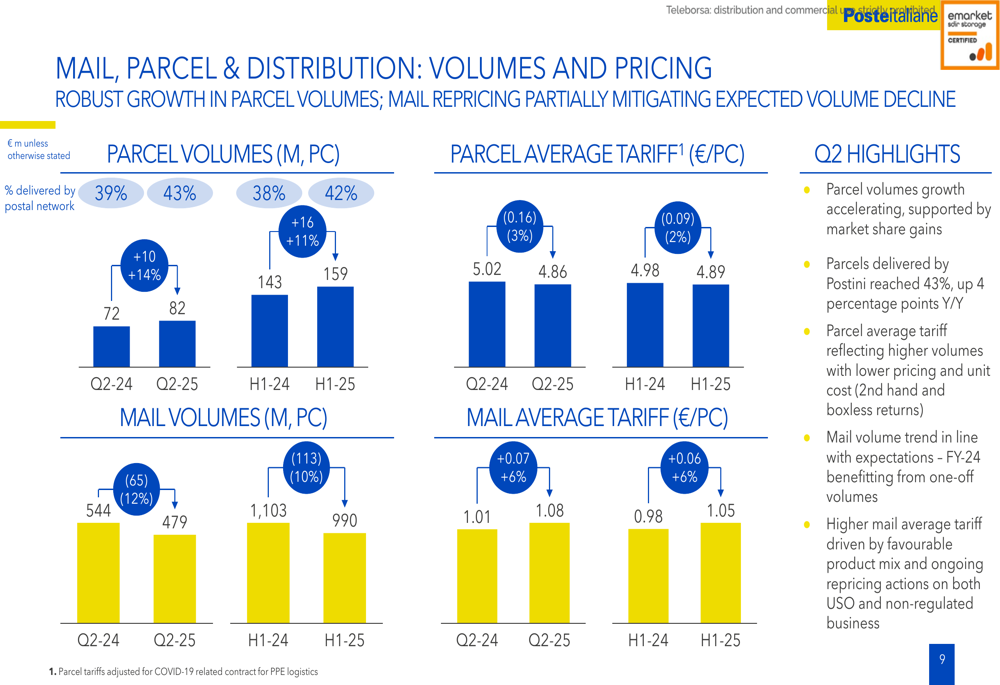

The Mail, Parcel & Distribution segment reported a modest 1% increase in external revenues for H1 2025, reaching €1,909 million. However, adjusted EBIT declined by 31% to €67 million. This reflects the ongoing structural decline in mail volumes, partially offset by growth in the parcel business.

Parcel volumes showed robust growth, with volumes increasing and the business now representing 42% of the segment in H1 2025, up from 38% in the same period last year. Meanwhile, mail volumes declined from 1,103 million pieces in H1 2024 to 990 million in H1 2025, though this was partially mitigated by an increase in the average tariff from €0.98 to €1.05 per piece.

The following chart illustrates the volume and pricing trends in the Mail, Parcel & Distribution segment:

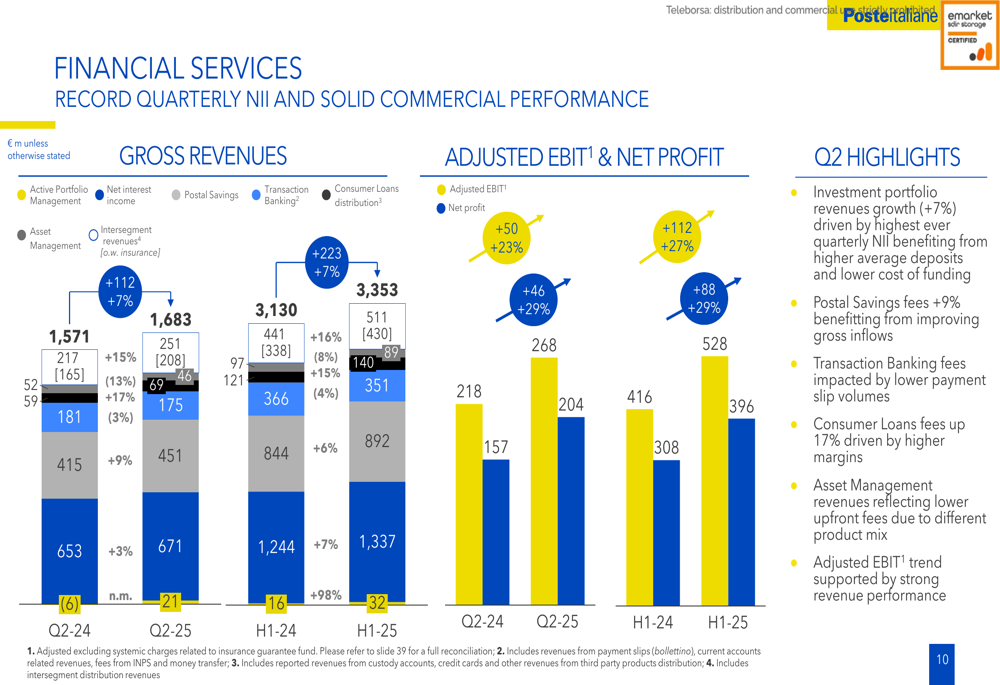

Financial Services

The Financial Services segment delivered outstanding results, with external revenues increasing by 6% to €2,841 million in H1 2025. Adjusted EBIT showed even stronger growth, rising 27% to €528 million.

This performance was driven by record quarterly net interest income and solid commercial performance across investment products. The segment benefited from active portfolio management, with revenues from this area growing by 16% in H1 2025.

The detailed breakdown of Financial Services revenues and profitability is shown below:

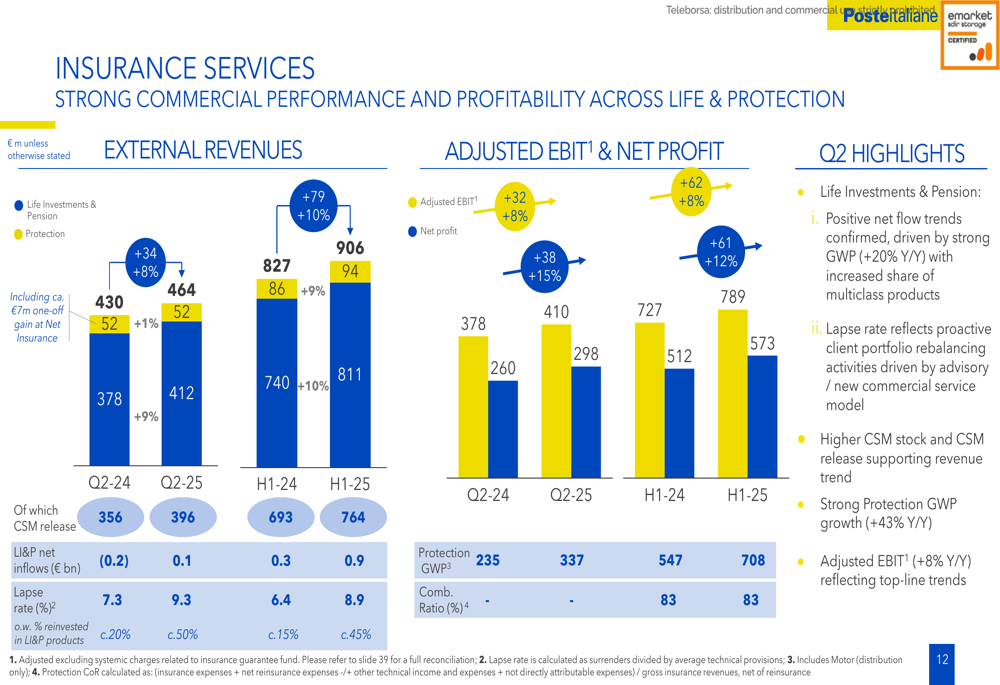

Insurance Services

The Insurance Services segment demonstrated strong commercial performance and profitability across both Life & Protection products. External revenues increased by 10% to €906 million in H1 2025, while adjusted EBIT grew by 8% to €789 million.

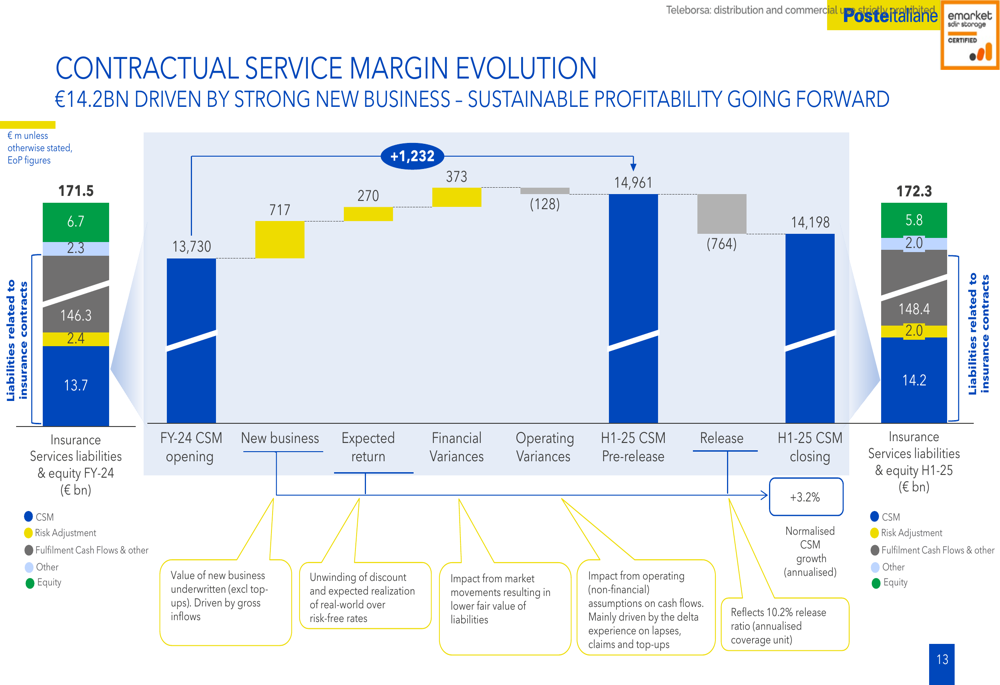

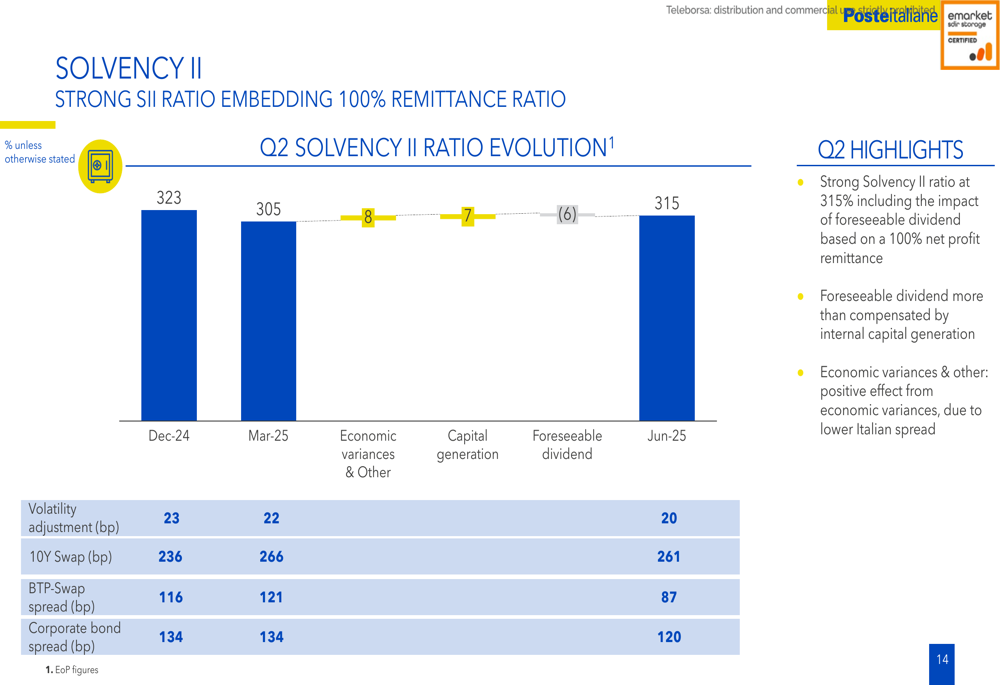

The segment's Contractual Service Margin (CSM) reached €14.2 billion, driven by strong new business, indicating sustainable profitability going forward. The company also maintained a robust Solvency II ratio of 315%, providing a solid foundation for future growth.

The following chart details the performance of the Insurance Services segment:

The evolution of the Contractual Service Margin provides insight into the future profitability of the Insurance business:

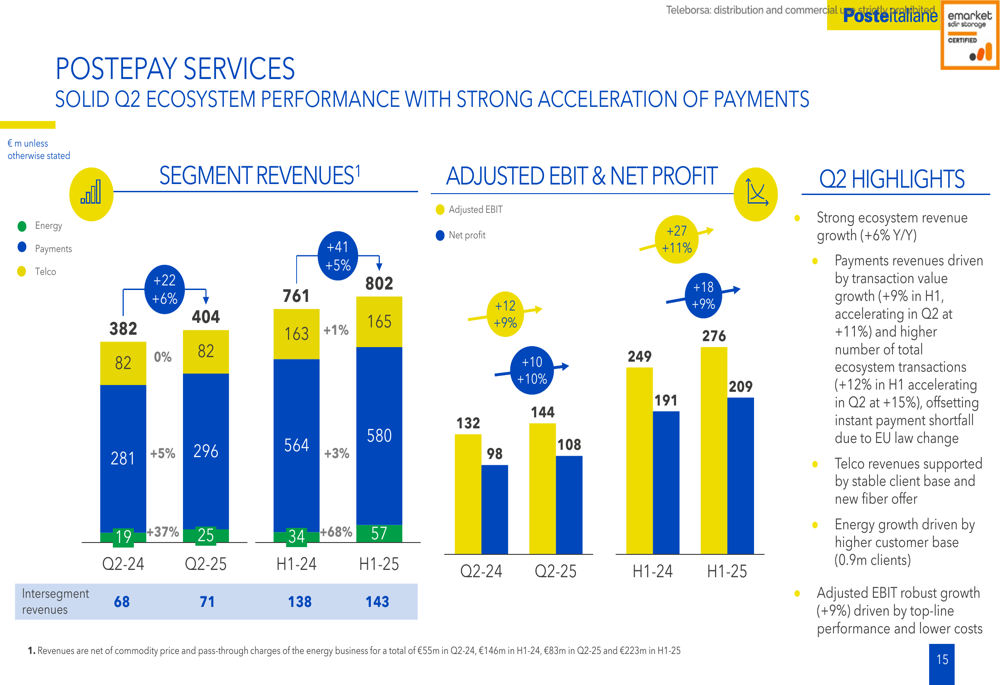

Postepay Services

The Postepay Services segment continued its solid performance, with external revenues growing by 5% to €802 million in H1 2025. Adjusted EBIT increased by 11% to €276 million, demonstrating the strength of the company's payments ecosystem.

The segment showed strong acceleration in payments, contributing to the overall digital transformation strategy of Poste Italiane:

Strategic Initiatives & Forward-Looking Statements

Poste Italiane's strong performance across all business units has enabled the company to upgrade its full-year guidance. The company now expects adjusted EBIT to reach €3.2 billion, up from the previous forecast of €3.1 billion, and net profit to reach €2.2 billion, increased from €2.1 billion.

The company's unique business model, combining traditional postal services with financial, insurance, and digital payment offerings, positions it well for sustained profitable growth in all market conditions. As CEO Matteo Del Fante emphasized, "We continue to build upon our solid momentum with a clear commitment to generate long-term value for our stakeholders."

The company's strong balance sheet and insurance solvency position provide a solid foundation for future growth:

Poste Italiane's digital transformation efforts continue to yield significant results, with 9 million app users reported during the earnings call. The company plans to maintain its focus on cost and capital expenditure discipline while expanding its digital and energy customer base.

Despite challenges such as declining mail volumes and rising HR costs, Poste Italiane's diversified business model and strategic initiatives position it well to navigate the evolving market landscape and deliver continued value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.