Can anything shut down the Gold rally?

PotlatchDeltic Corporation (NASDAQ:PCH) reported a significant decline in second-quarter performance during its earnings presentation on July 29, 2025, with total Adjusted EBITDDA falling 18% quarter-over-quarter to $52.0 million. The timber and wood products company’s stock closed down 3.29% at $41.94 ahead of the earnings release, reflecting market concerns about the challenging operating environment.

Quarterly Performance Highlights

PotlatchDeltic’s Q2 2025 results showed a marked deterioration from its strong first quarter, with net income dropping to $7.4 million ($0.09 per diluted share) from $25.8 million ($0.33 per diluted share) in Q1. This represents a substantial decline from the company’s Q1 performance, which had significantly exceeded analyst expectations.

The company’s presentation highlighted its diversified business model, with Timberlands providing stability, while the Wood Products segment faced significant headwinds. The Real Estate segment continued to deliver solid results.

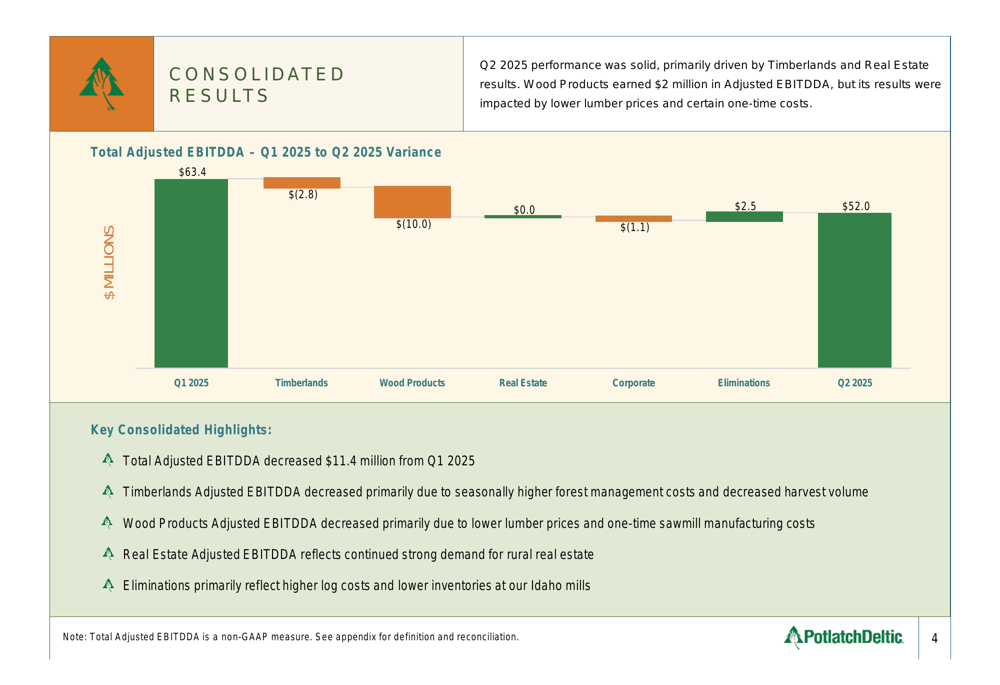

As shown in the following consolidated results chart:

Total (EPA:TTEF) Adjusted EBITDDA decreased by $11.4 million from Q1 2025, with the Wood Products segment accounting for the largest portion of the decline (-$10.0 million). Timberlands decreased by $2.8 million, and Real Estate decreased by $1.1 million, while eliminations improved by $2.5 million.

Detailed Financial Analysis

The Timberlands segment, which typically provides stability to PotlatchDeltic’s business model, posted Adjusted EBITDDA of $39.6 million, down from $42.4 million in Q1. This decrease was primarily driven by increased forest management costs due to seasonal activity and lower Southern harvest volumes.

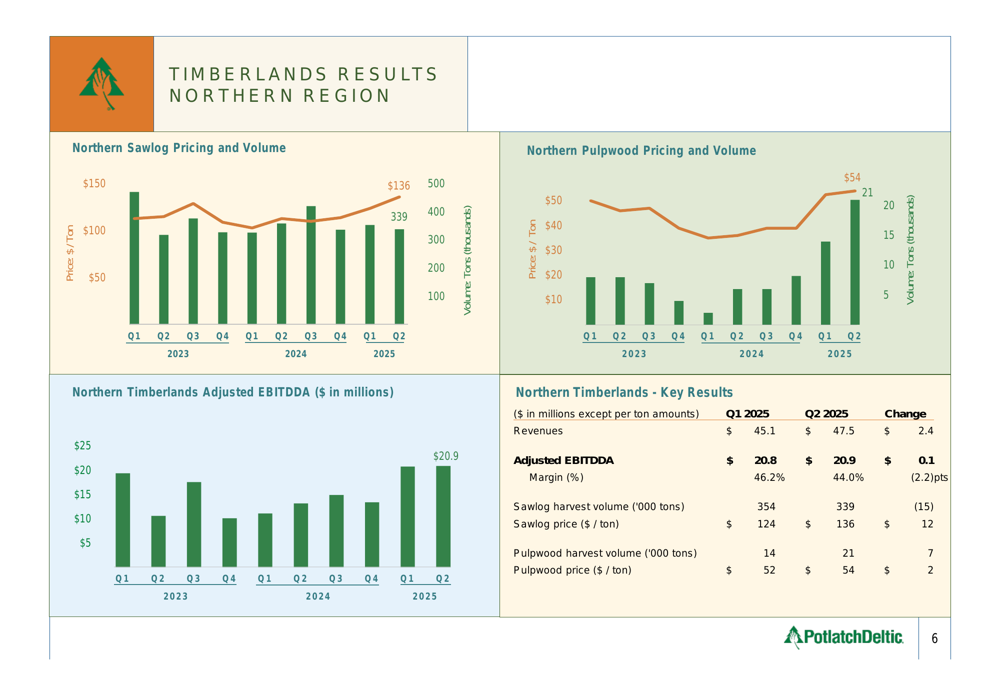

The Northern Region saw improved sawlog pricing, with average prices increasing from $124 to $136 per ton, as illustrated in the following chart:

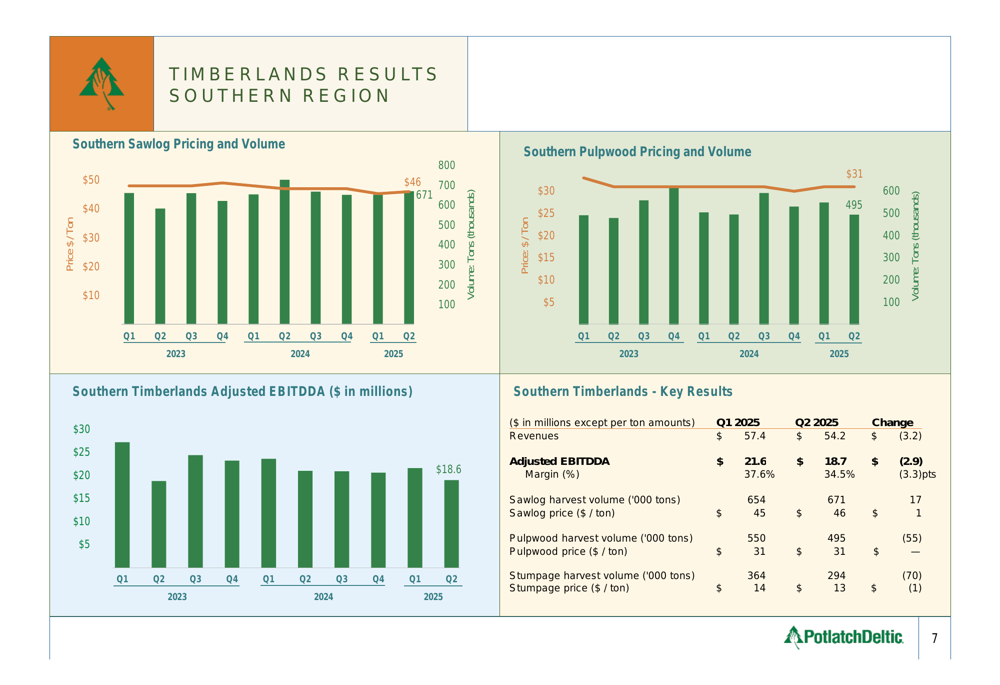

Meanwhile, the Southern Region experienced a more significant decline in performance, with Adjusted EBITDDA falling from $21.6 million to $18.7 million:

The Wood Products segment faced the most significant challenges, with Adjusted EBITDDA plummeting to $1.7 million from $11.7 million in Q1 2025. This dramatic decline occurred despite achieving a quarterly record in shipment volume of 303 MMBF.

The following chart illustrates the factors contributing to this decline:

Key factors impacting the Wood Products segment included a 1% decrease in average lumber prices to $450 per MBF, increased log costs in Idaho, a higher lumber inventory charge, and operational issues at the St. Maries and Waldo facilities.

The Real Estate segment remained relatively stable, with Adjusted EBITDDA of $22.7 million. The company sold 7,457 rural acres at an average price of $3,108 per acre and 18 residential lots at an average price of $102,222 per lot.

Strategic Initiatives & Capital Allocation

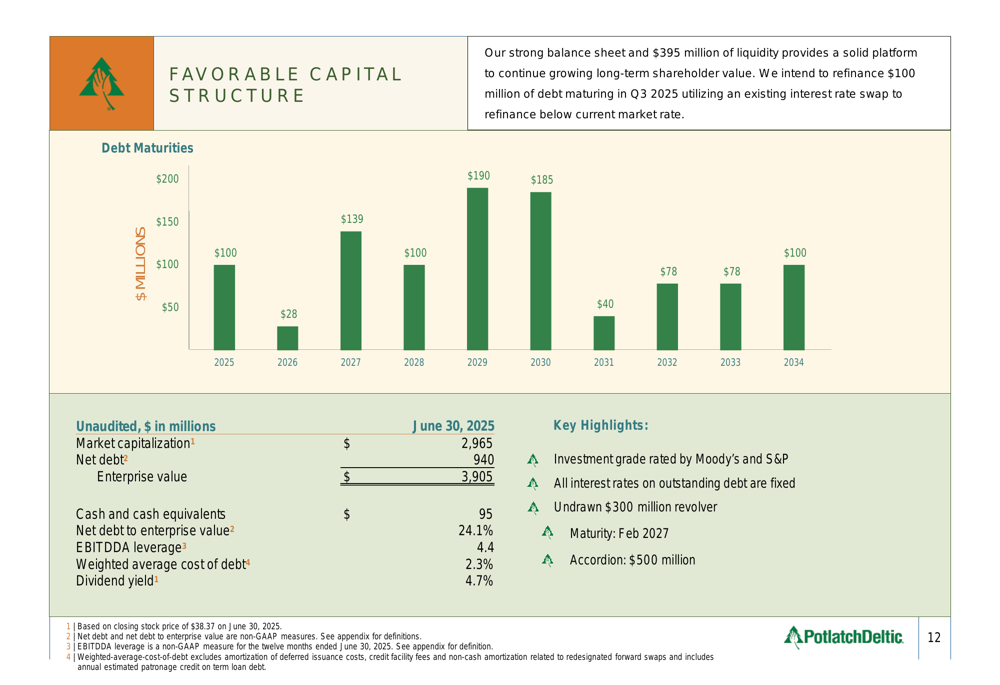

Despite the challenging quarter, PotlatchDeltic maintained its focus on shareholder returns and capital allocation priorities. The company highlighted its strong financial position and commitment to returning cash to shareholders:

Key capital allocation highlights include:

- $139 million annual dividend run rate (4.7% yield)

- $60 million in share repurchases year-to-date at an average price of $40 per share

- $33 million in capital expenditures spent year-to-date, with $60-$65 million planned for full-year 2025

- Plans to refinance $100 million of debt maturing in Q3 2025

- Strong liquidity position of $395 million

- Net debt to enterprise value ratio of 24.1%

The company also emphasized its environmental commitments, including 6.4 million metric tons of net CO2e removals and targets for 42% reduction in scope 1 & 2 emissions by 2030 and Net Zero scope 1 & 2 by 2050.

Forward-Looking Statements

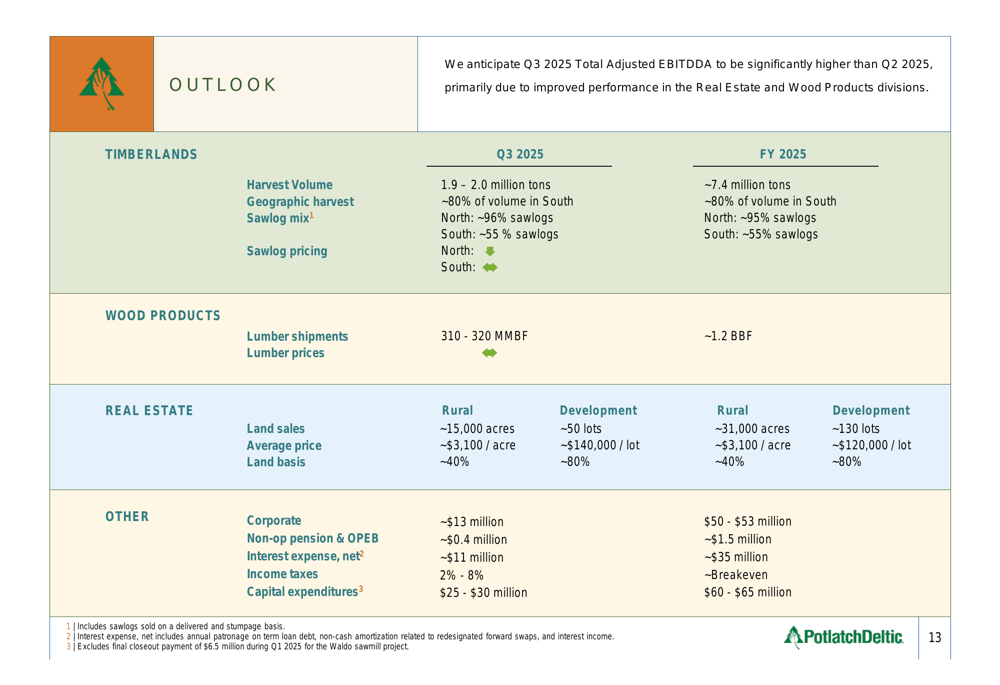

Despite the Q2 challenges, management provided an optimistic outlook for the third quarter and full year 2025:

The company anticipates Q3 2025 Total Adjusted EBITDDA will be "significantly higher" than Q2 2025, driven by:

- Increased harvest volumes of 1.9-2.0 million tons in Timberlands

- Higher lumber shipments of 310-320 MMBF in Wood Products

- Substantial increase in Real Estate sales, with approximately 15,000 rural acres and 50 residential lots expected to close in Q3

For the full year 2025, PotlatchDeltic projects:

- Total harvest volume of approximately 7.4 million tons

- Lumber shipments of approximately 1.2 billion board feet

- Rural real estate sales of approximately 31,000 acres at an average price of $3,100 per acre

- Development sales of approximately 130 lots at an average price of $120,000 per lot

- Capital expenditures of $60-$65 million

This outlook aligns with management’s comments during the Q1 earnings call, where they had anticipated seasonal factors would lead to lower Q2 EBITDA but projected improvement in the second half of the year.

Market Context

PotlatchDeltic’s Q2 results come amid ongoing volatility in lumber markets and broader economic uncertainty. The company’s performance reflects the challenges facing the wood products industry, including fluctuating lumber prices and increased operational costs.

The stock’s 3.29% decline ahead of the earnings release suggests investors were anticipating disappointing results. With the company projecting a significant improvement in Q3 performance, market attention will likely focus on whether PotlatchDeltic can deliver on this optimistic outlook amid continuing industry headwinds.

The company’s diversified business model, strong balance sheet, and consistent dividend policy (currently yielding 4.7%) may provide some stability for investors during this period of volatility in the timber and wood products sectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.