Tesla’s Samsung order shift unlikely to hurt TSMC: Morgan Stanley

PPG Industries (NYSE:PPG) presented its second quarter 2025 financial results on July 29, showing modest organic sales growth of 2% driven primarily by strength in its Performance Coatings segment, while the company’s architectural business continued to face headwinds in Europe. The company reported adjusted earnings per share of $2.22 and narrowed its full-year guidance.

Quarterly Performance Highlights

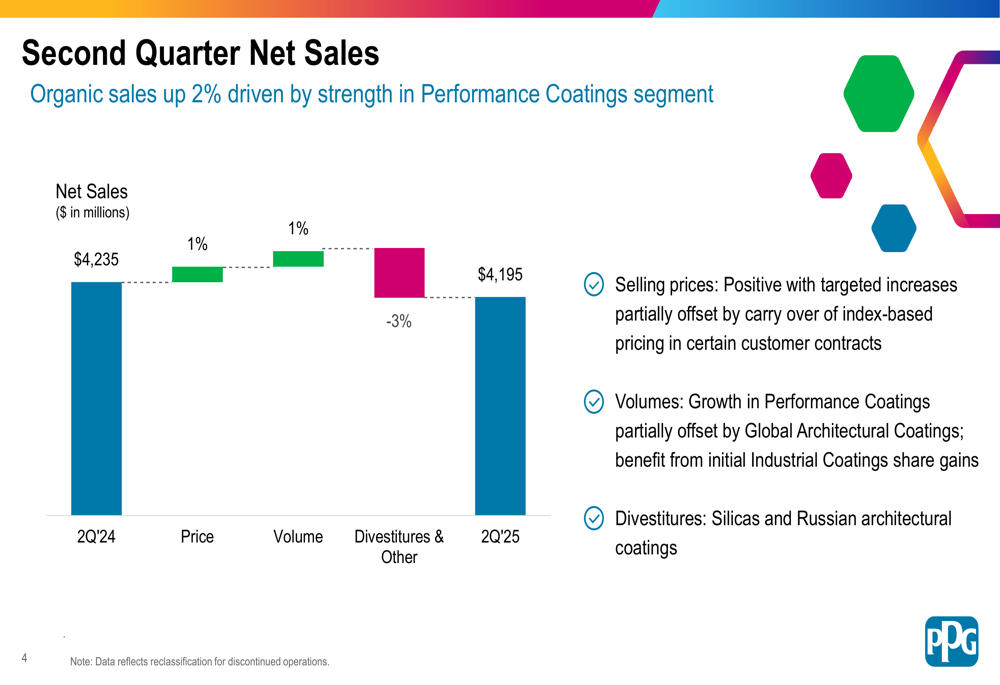

PPG (WA:IBSP) reported net sales of $4.2 billion for the second quarter, representing a 2% organic sales increase compared to the same period last year. This growth was achieved despite a 3% negative impact from divestitures, including the company’s silicas business and Russian architectural coatings operations.

"Our second quarter results demonstrate continued momentum in key sectors like aerospace, protective and marine, and packaging, which helped offset challenges in other areas of our business," the company noted in its presentation.

The quarter’s adjusted earnings per share came in at $2.22, showing sequential improvement from the $1.72 reported in Q1 2025. The company maintained a segment EBITDA margin of 20.3% and deployed approximately $150 million for share repurchases during the quarter.

As shown in the following chart detailing the components of net sales performance:

Segment Analysis

PPG’s performance varied significantly across its three main business segments, with Performance Coatings emerging as the clear standout.

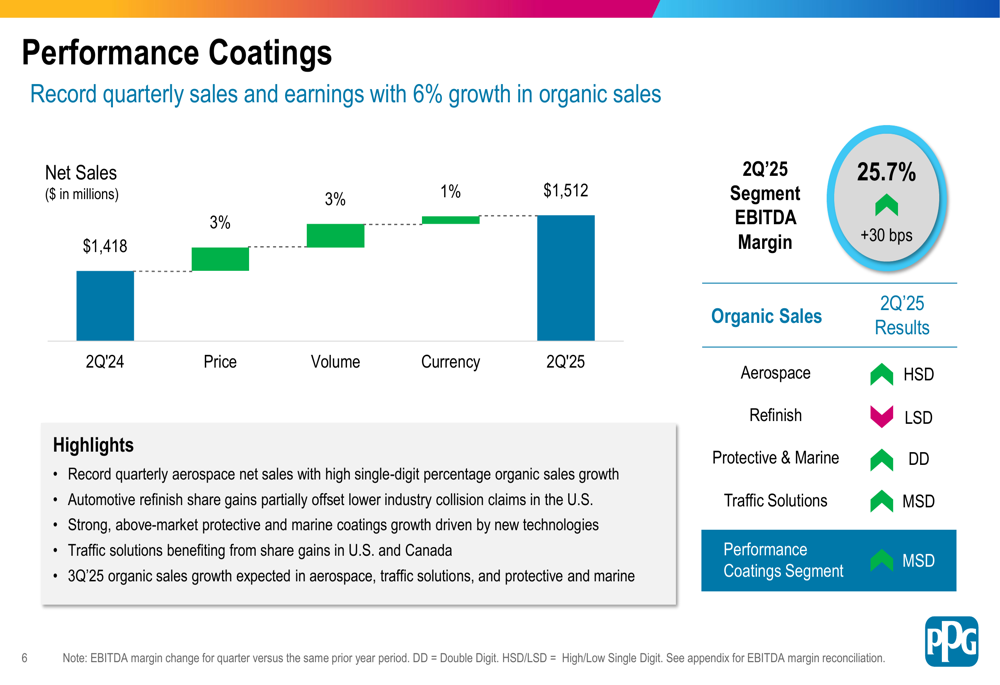

The Performance Coatings segment delivered record quarterly sales and earnings with 6% organic sales growth. Net sales increased from $1,418 million in Q2 2024 to $1,512 million in Q2 2025, driven by both price (+3%) and volume (+3%) improvements. The segment achieved an EBITDA margin of 25.7%, up 30 basis points year-over-year.

Key drivers included record quarterly aerospace sales with high single-digit percentage organic growth, automotive refinish share gains (partially offset by lower collision claims in the U.S.), and strong growth in protective and marine coatings driven by new technologies.

The following chart illustrates the Performance Coatings segment’s strong results:

In contrast, the Global Architectural Coatings segment faced continued challenges, particularly in Europe. Net sales declined from $1,070 million in Q2 2024 to $1,018 million in Q2 2025, with volume down 2% and a 4% negative impact from divestitures. The segment’s EBITDA margin fell 370 basis points to 18.4%.

"Tepid demand in EMEA persisted, though we saw slight improvement in Mexico," the company noted. "Lower volume and inflation negatively impacted margins, but we expect sales growth to resume in Latin America."

The Industrial Coatings segment reported flat volume as growing benefits from share gains offset end-market declines. Net sales decreased from $1,747 million to $1,665 million, primarily due to divestitures (-5%) and slightly negative pricing (-1%). The segment’s EBITDA margin declined 130 basis points to 16.6%.

Strategic Initiatives

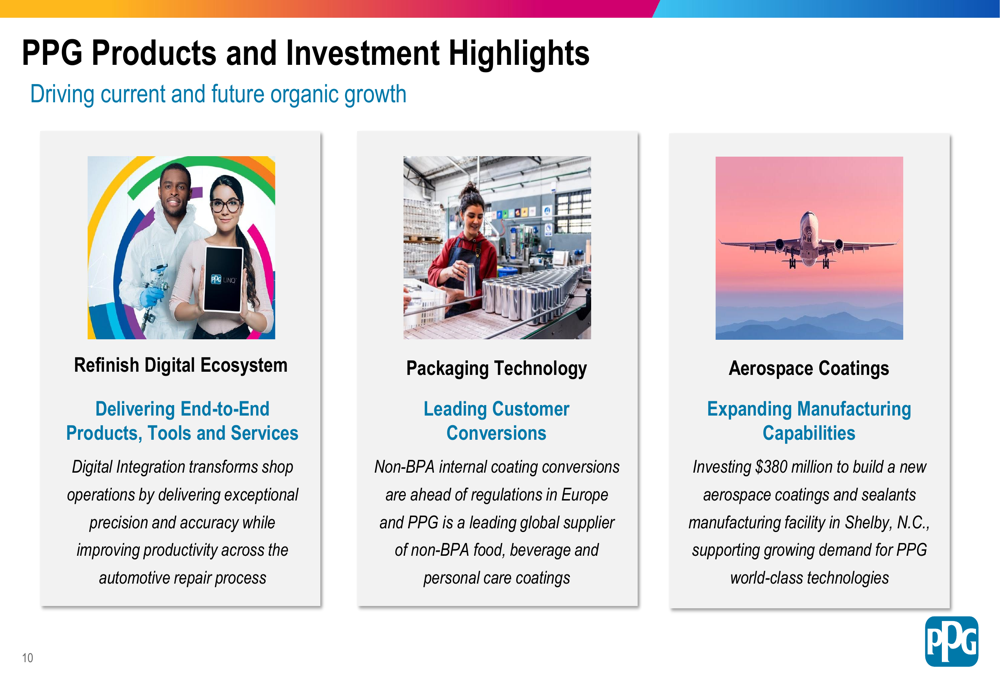

PPG highlighted several strategic initiatives aimed at driving long-term growth and competitive advantage. The company is investing $380 million to build a new aerospace coatings and sealants manufacturing facility in Shelby, North Carolina, supporting growing demand for its aerospace technologies.

Additionally, PPG is advancing its Refinish Digital Ecosystem, which transforms shop operations through digital integration, and expanding its packaging technology leadership with non-BPA internal coatings that are ahead of regulatory requirements in Europe.

These strategic investments align with the company’s focus on maintaining leadership positions across all coatings verticals while driving organic and inorganic growth opportunities.

The following image showcases these key strategic initiatives:

Financial Position & Outlook

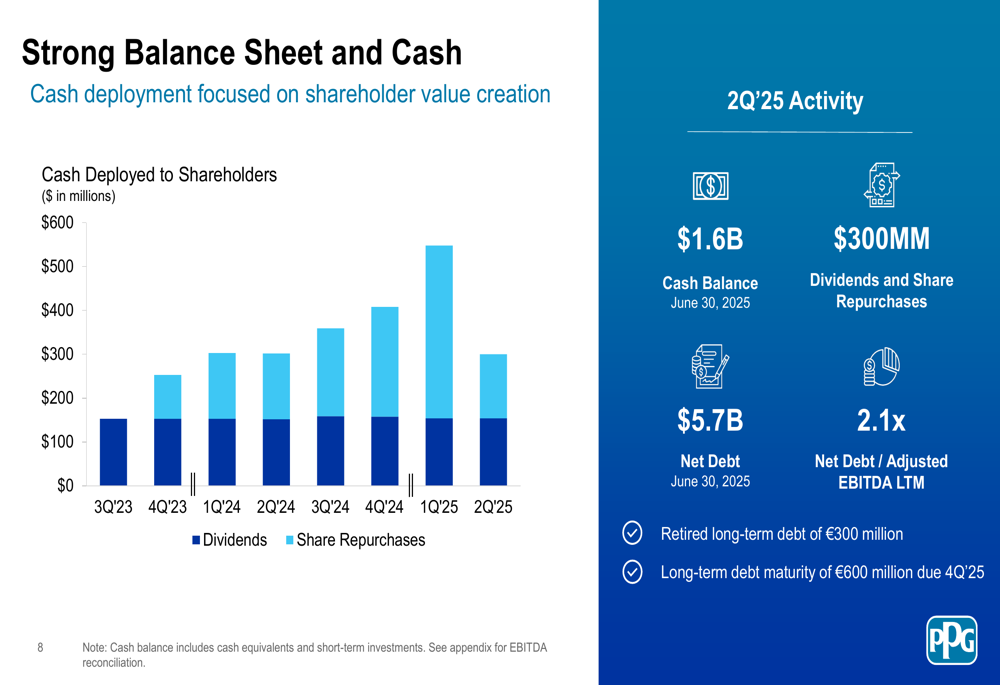

PPG maintained a strong balance sheet with $1.6 billion in cash and cash equivalents as of June 30, 2025. The company’s net debt stood at $5.7 billion, with a net debt to adjusted EBITDA ratio of 2.1x. During the quarter, PPG retired long-term debt of €300 million and noted an upcoming maturity of €600 million due in Q4 2025.

The company continued its focus on shareholder returns, deploying $300 million through dividends and share repurchases in Q2 2025.

As shown in the following chart detailing the company’s cash deployment to shareholders:

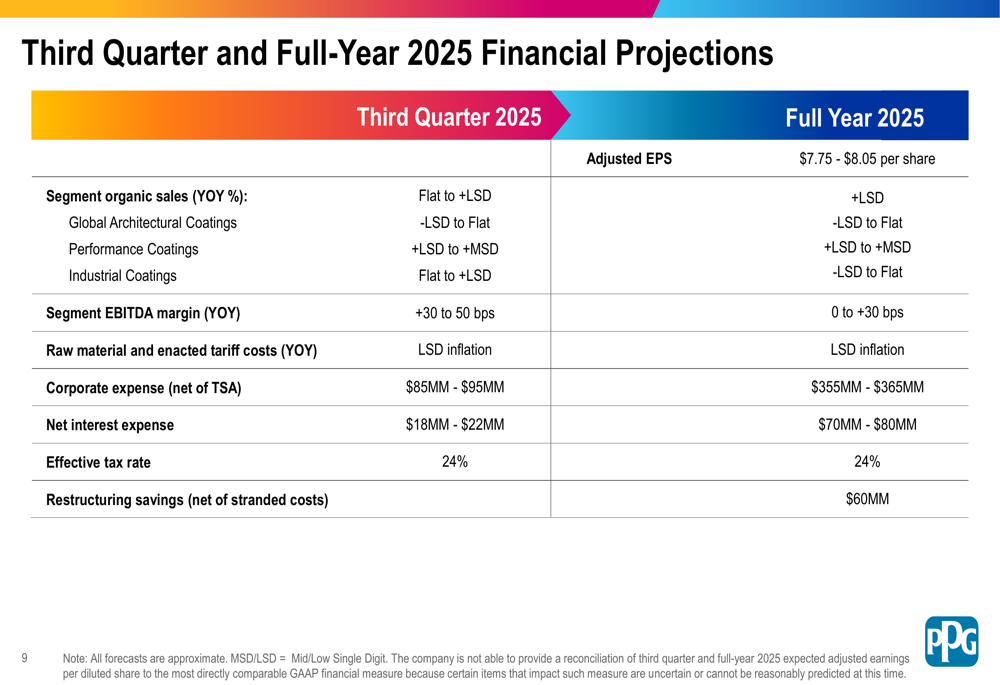

Looking ahead, PPG narrowed its full-year 2025 adjusted EPS guidance to $7.75-$8.05 per share, compared to the previous range of $7.75-$8.50 provided after Q1 results. For the third quarter, the company expects flat to low-single-digit organic sales growth overall, with segment EBITDA margin improvement of 30 to 50 basis points year-over-year.

By segment, PPG projects third-quarter organic sales to range from negative low-single-digit to flat for Global Architectural Coatings, low to mid-single-digit growth for Performance Coatings, and flat to low-single-digit growth for Industrial Coatings.

The company also anticipates low-single-digit raw material and tariff cost inflation, with approximately $60 million in restructuring savings (net of stranded costs) for the full year.

The following table provides a detailed breakdown of PPG’s financial projections:

PPG’s stock closed at $113.97 on July 29, down 1.45% for the day, and edged slightly lower in after-hours trading. The stock has traded in a 52-week range of $90.24 to $137.24, currently positioned in the middle of that range as investors digest the company’s mixed performance across segments and cautious outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.