How are energy investors positioned?

Introduction & Market Context

PrairieSky Royalty Ltd (TSX:PSK) released its Q2 2025 corporate presentation on July 15, 2025, highlighting record royalty oil production despite a significant earnings miss. The company’s stock rose 2.82% to $24.24 following the presentation, showing investor confidence in its long-term strategy despite the EPS shortfall of 57.78% compared to analyst expectations. With an enterprise value of $5.8 billion, PrairieSky continues to position itself as Canada’s largest portfolio of fee simple mineral title with 18.5 million acres of royalty lands.

Quarterly Performance Highlights

PrairieSky reported record royalty oil production of 14,376 barrels per day in Q2 2025, representing an 8% year-over-year increase. The company’s presentation emphasized its strong position in key oil plays, with oil and liquids accounting for 93% of YTD 2025 royalty production revenue. Despite the production growth, PrairieSky posted an EPS of $0.24, well below the expected $0.5684.

The company’s snapshot reveals a financially stable organization with a conservative balance sheet strength of 0.5x D/EBITDA (trailing 12-months) and a sustainable annual dividend of $1.04 per common share paid quarterly.

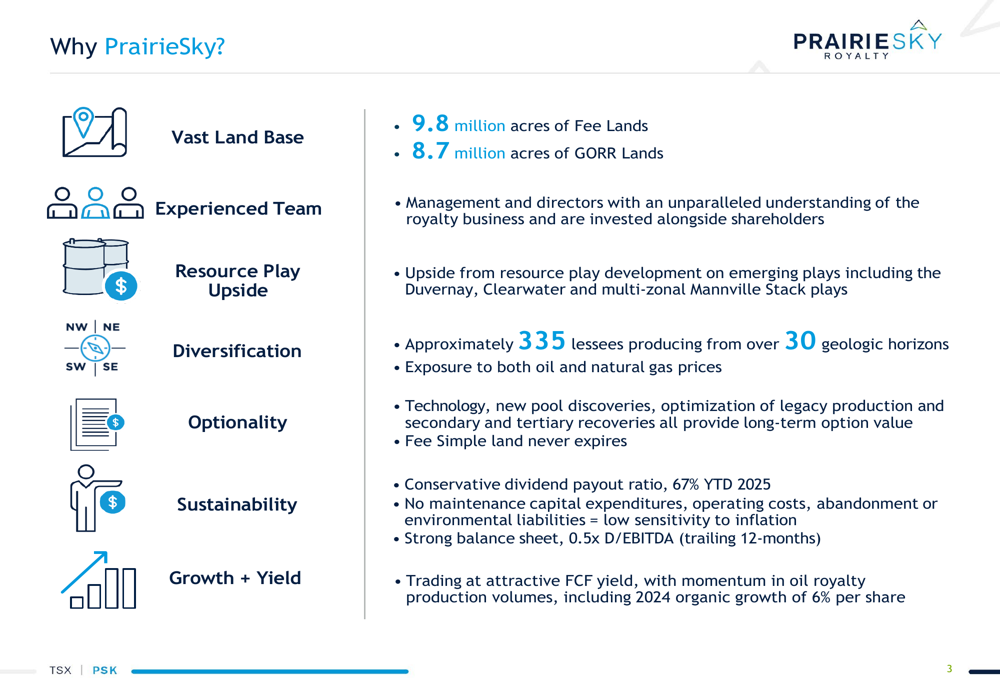

As shown in the following snapshot of key metrics:

PrairieSky’s investment thesis centers on its vast land base, experienced management team, and exposure to multiple resource plays. The company highlights its diversification across 335 lessees producing from over 30 geologic horizons, providing exposure to both oil and natural gas prices.

Strategic Initiatives

PrairieSky’s growth strategy has focused on expanding its land position, which has more than tripled since its IPO in 2014. The company has achieved a 96% increase in royalty lands on a per share basis, including significant acquisitions in Saskatchewan, Clearwater, and Mannville Stack positions.

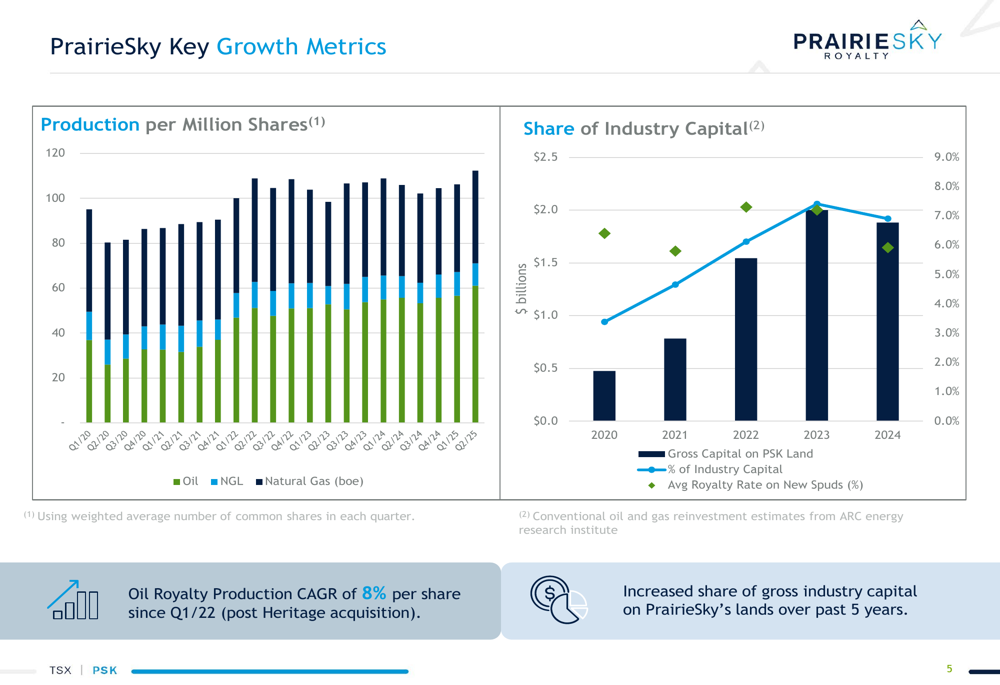

The company’s key growth metrics demonstrate consistent production growth per million shares, with an oil royalty production CAGR of 8% per share since Q1/22 following the Heritage acquisition. This growth has been supported by increased industry capital on PrairieSky lands.

The following chart illustrates these growth trends:

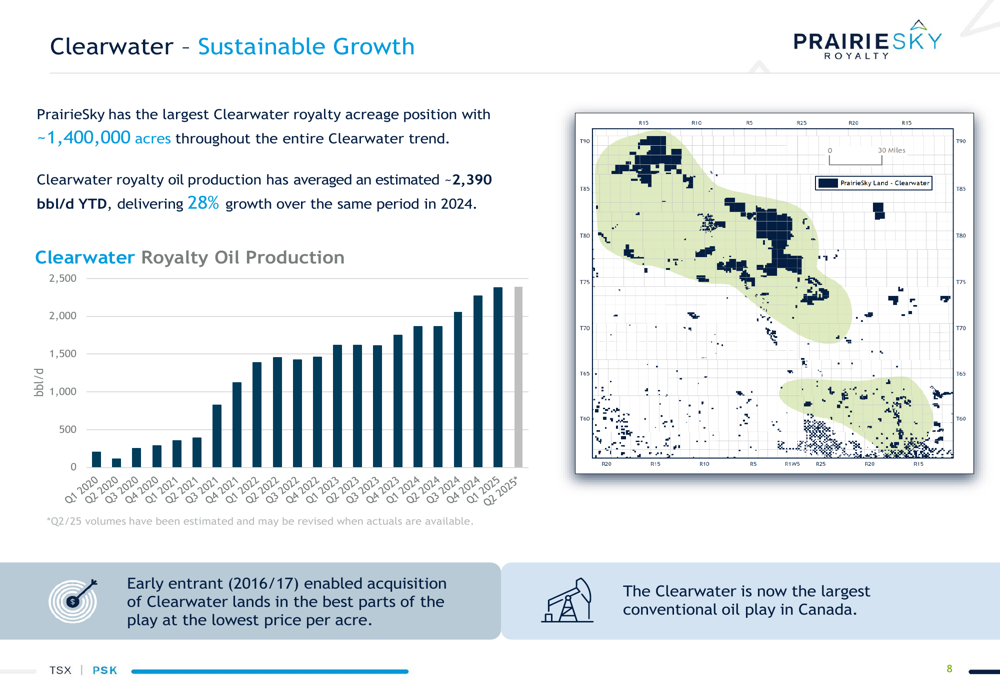

A major driver of PrairieSky’s production growth has been its strategic focus on three key oil plays: Clearwater, Mannville Stack, and Duvernay. The Clearwater play, where PrairieSky holds the largest royalty acreage position with approximately 1.4 million acres, has delivered particularly strong results with royalty oil production averaging an estimated 2,390 bbl/d YTD, representing 28% growth over the same period in 2024.

As shown in the following chart of Clearwater production growth:

Similarly, the company’s expanded position in the Mannville Stack has contributed to production growth of 13% YTD compared to the same period in 2024, while Duvernay royalty volumes have grown by 64% over the same timeframe.

Detailed Financial Analysis

Despite strong production growth, PrairieSky’s Q2 2025 financial results fell short of expectations. The company reported funds from operations of $96.7 million ($0.41 per share) and total royalty production revenue of $111.2 million. The significant EPS miss (-57.78%) contrasts with the positive operational metrics highlighted in the presentation.

PrairieSky maintains a high-margin business model with minimal exposure to inflation, as it has no maintenance capital requirements or operating costs. The company reports a royalty operating margin of 99% and an overall operating margin of 87%, allowing for consistent returns to shareholders.

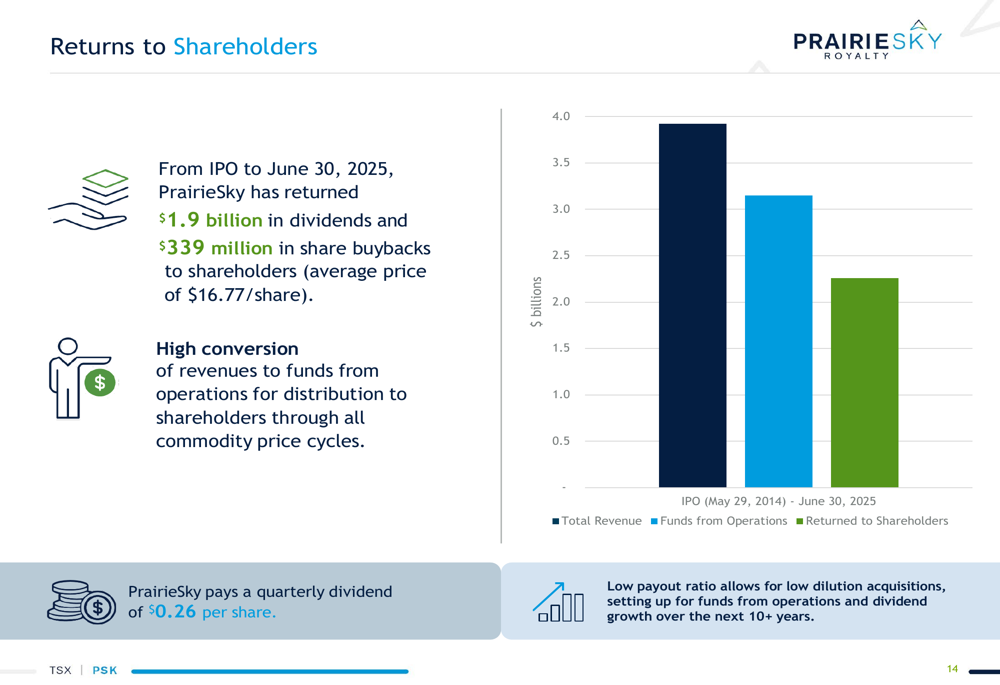

The company has returned $2.3 billion to shareholders since its IPO, including $1.9 billion in dividends and $339 million in share buybacks. For Q2 2025, PrairieSky declared a quarterly dividend of $0.26 per share, maintaining its annual rate of $1.04 per share with a payout ratio of 63%.

As illustrated in the following chart of returns to shareholders:

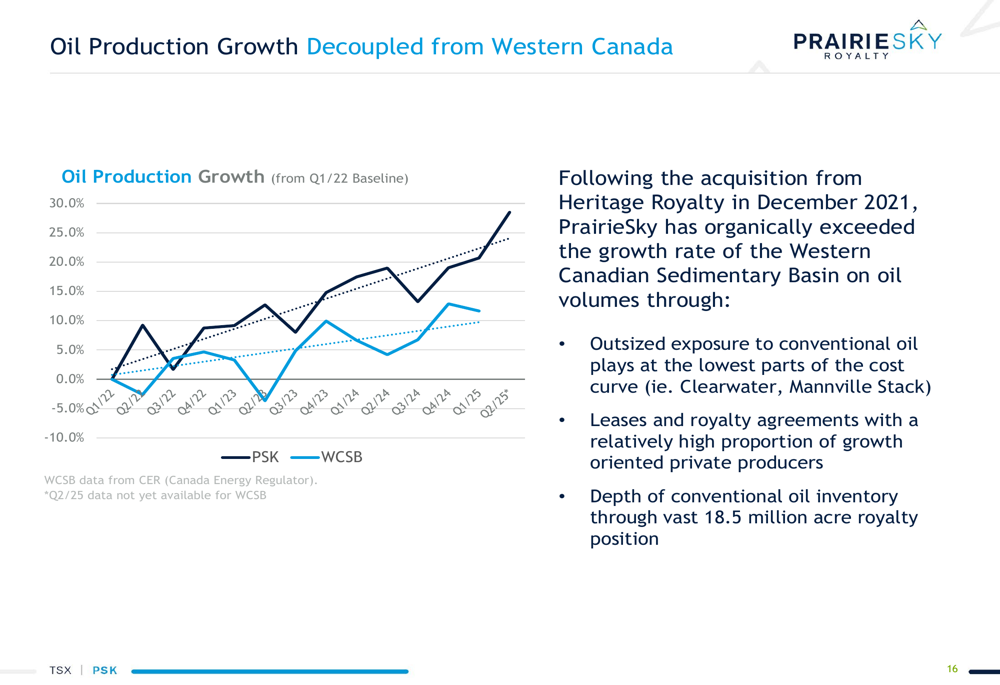

A notable strength of PrairieSky’s business model is its ability to grow oil production at a rate that outpaces the broader Western Canadian Sedimentary Basin. Following the Heritage Royalty acquisition in December 2021, the company has leveraged its outsized exposure to conventional oil plays and relationships with growth-oriented private producers to achieve superior production growth.

The following chart demonstrates this outperformance:

ESG Performance

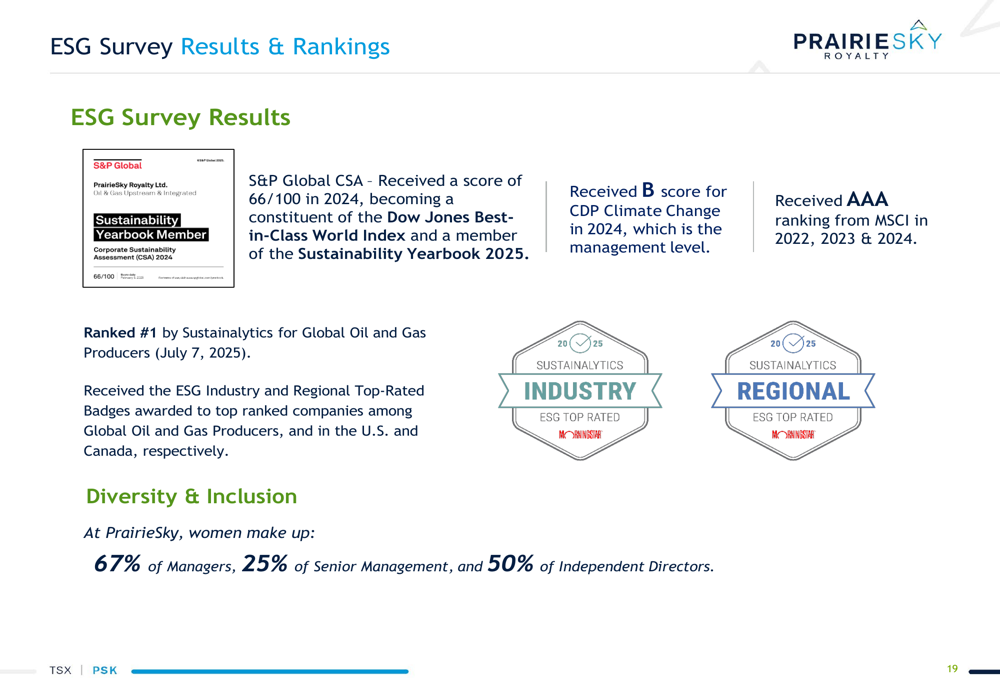

PrairieSky has positioned itself as an ESG leader in the oil and gas sector, receiving top rankings from multiple sustainability rating agencies. The company was ranked #1 by Sustainalytics for Global Oil and Gas Producers as of July 7, 2025, and has maintained an AAA ranking from MSCI for three consecutive years (2022-2024).

The company’s ESG profile benefits from its royalty business model, which involves no oil and gas field operations, facilities, or end-of-life decommissioning liabilities. This structure provides investors with exposure to energy production while minimizing direct environmental impacts.

As shown in the following summary of ESG rankings:

Forward-Looking Statements

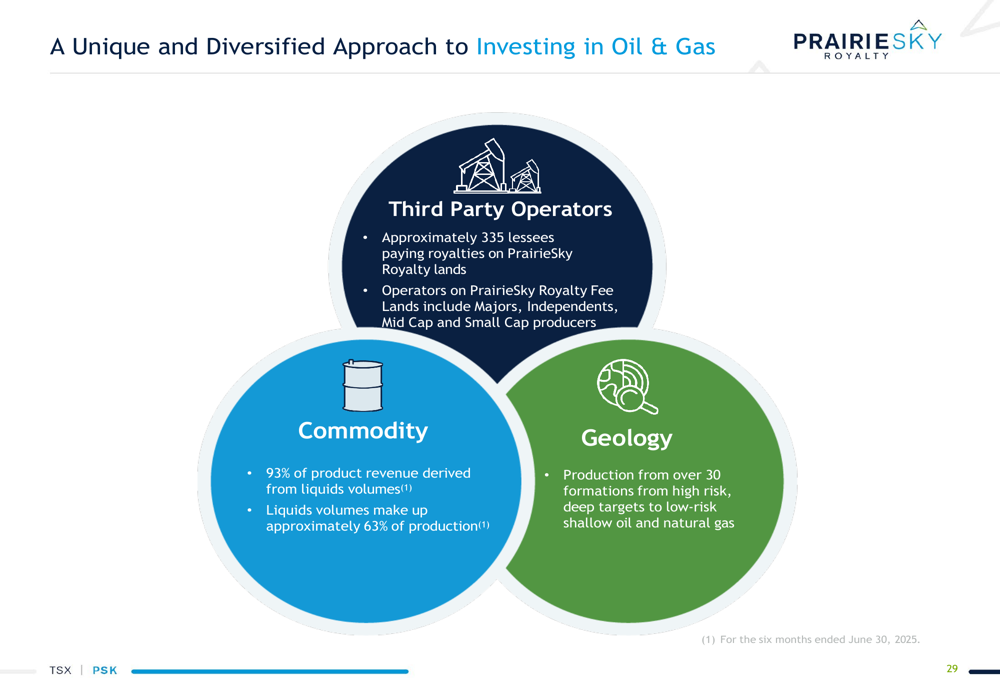

Looking ahead, PrairieSky expects to maintain its growth trajectory through continued development of its key oil plays and potential expansion into new areas. The company’s diversified approach to oil and gas investing provides exposure across operators, commodities, and geological formations.

The company’s unique business model is illustrated in the following diagram:

PrairieSky expects natural gas volume growth in 2026 and plans to leverage its increased credit facility of $600 million for further development. With net debt of $242 million at the end of Q2 2025, the company maintains significant financial flexibility for future acquisitions and shareholder returns.

Management remains focused on high-productivity plays and potential long-duration oil projects, with particular emphasis on the continued development of the Clearwater, Mannville Stack, and Duvernay plays. The company’s low payout ratio (63% in Q2 2025) provides room for dividend growth while maintaining a conservative financial position.

Despite the significant earnings miss in Q2 2025, PrairieSky’s record oil production and strategic positioning in key growth plays suggest the company remains well-positioned to deliver long-term value to shareholders through its unique royalty business model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.