Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Premier, Inc. (NASDAQ:PINC) held its fiscal 2025 third-quarter earnings conference call on May 6, 2025, reporting results that exceeded internal expectations despite revenue challenges. The healthcare improvement company is continuing its strategic restructuring, divesting non-core assets while focusing on strengthening its core supply chain and performance services segments.

Premier’s stock has shown modest movement following the results, with shares trading at $20.51 at previous close and showing a 2.39% increase to $21.00 in premarket trading. The company’s shares have traded between $17.23 and $23.56 over the past 52 weeks.

Quarterly Performance Highlights

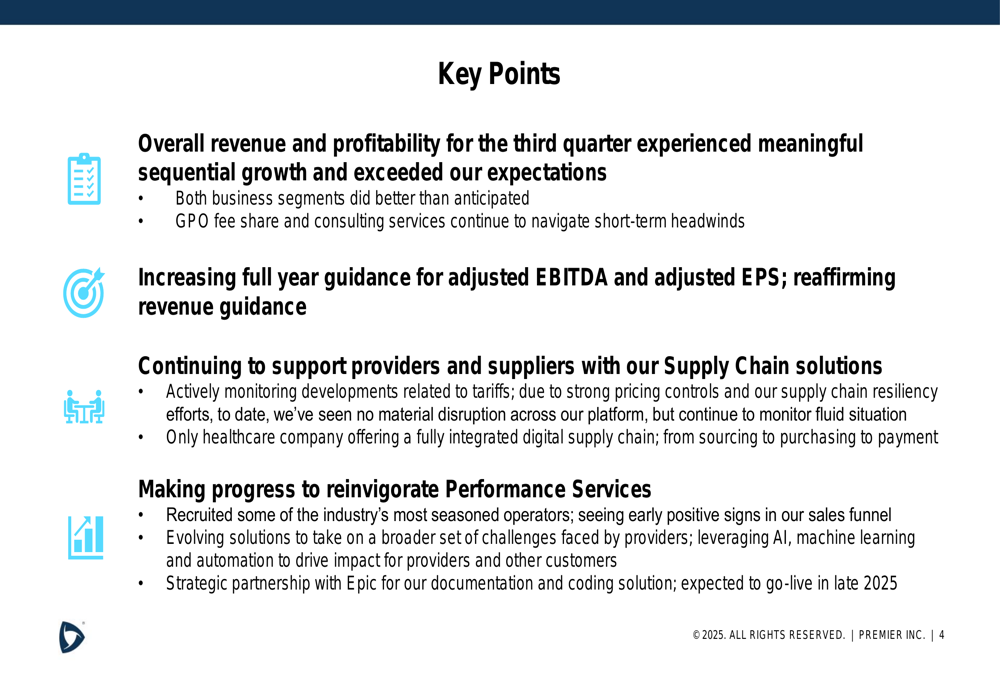

Premier reported declining revenue across both business segments for the third quarter of fiscal 2025, though management emphasized that overall revenue and profitability exceeded their expectations. The company faced headwinds from GPO fee share increases and lower consulting services revenue.

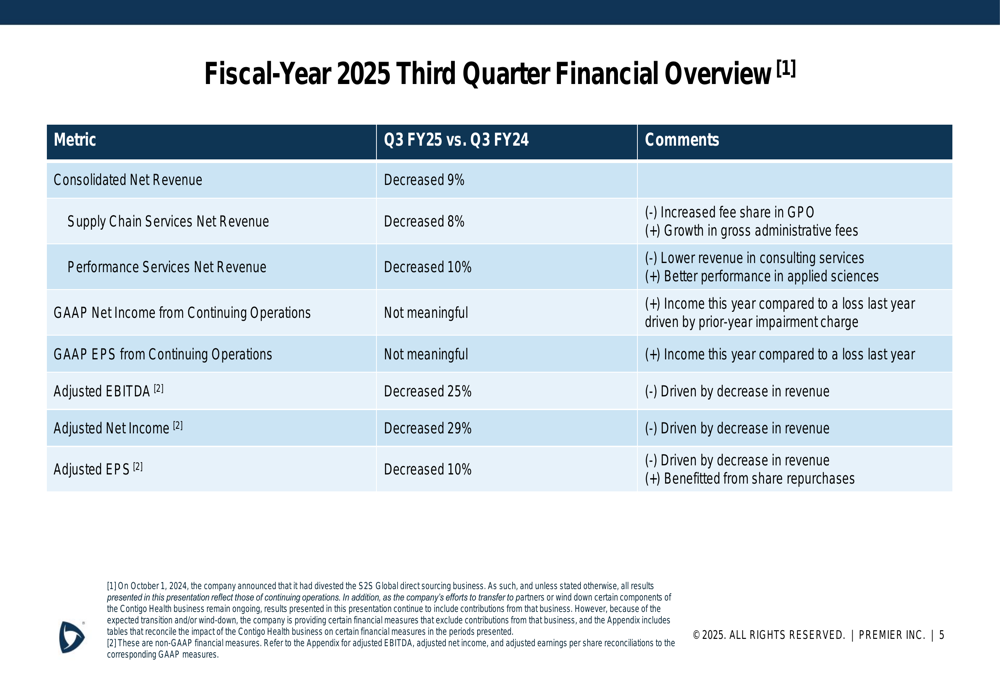

Consolidated net revenue decreased 9% compared to the same period last year, with Supply Chain Services net revenue down 8% and Performance Services net revenue declining 10%. The revenue decreases were primarily attributed to increased fee share in the GPO business and lower consulting services revenue, partially offset by growth in gross administrative fees and better performance in applied sciences.

Despite the revenue declines, Premier reported improved GAAP net income from continuing operations compared to the prior year, which had been impacted by an impairment charge. However, adjusted profitability metrics showed significant year-over-year decreases, with adjusted EBITDA down 25%, adjusted net income down 29%, and adjusted EPS down 10%. The less severe decline in adjusted EPS was attributed to the company’s share repurchase program.

It’s worth noting that the results reflect continuing operations following the divestiture of the S2S Global direct sourcing business, which was completed on October 1, 2024.

Financial Position and Capital Allocation

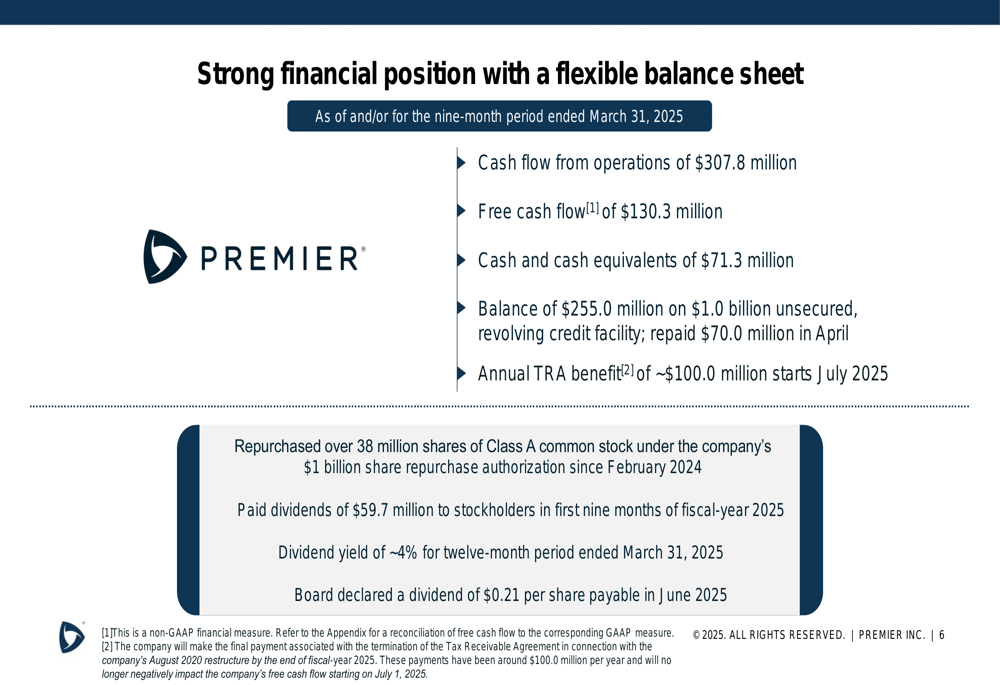

Premier highlighted its strong financial position, emphasizing robust cash flow generation and an active capital return program. For the nine months ended March 31, 2025, the company generated $307.8 million in cash flow from operations and $130.3 million in free cash flow.

The company reported $71.3 million in cash and cash equivalents, with $255 million drawn on its $1 billion unsecured revolving credit facility. Premier noted that it repaid $70 million of this balance in April 2025. Starting in July 2025, the company expects to receive an annual Tax Receivable Agreement (TRA) benefit of approximately $100 million.

Premier has been aggressively returning capital to shareholders, repurchasing over 38 million shares of Class A common stock under its $1 billion share repurchase authorization initiated in February 2024. Additionally, the company paid $59.7 million in dividends during the first nine months of fiscal 2025, maintaining a dividend yield of approximately 4%. The board declared a dividend of $0.21 per share payable in June 2025.

Strategic Initiatives

Premier outlined several strategic initiatives aimed at strengthening its core businesses. For the Supply Chain Services segment, the company is focusing on supporting providers and suppliers with comprehensive supply chain solutions, monitoring tariffs, and offering an integrated digital supply chain.

For the Performance Services segment, Premier is implementing a reinvigoration strategy that includes recruiting seasoned operators, evolving solutions that leverage artificial intelligence, and developing a strategic partnership with Epic, a major healthcare software provider. This partnership is expected to go live in late 2025 and could significantly enhance Premier’s technology offerings.

The company is also continuing its portfolio optimization efforts. Following the divestiture of S2S Global in October 2024, Premier expects to substantially transition or wind down the remaining Contigo Health businesses by December 31, 2025.

Forward-Looking Statements

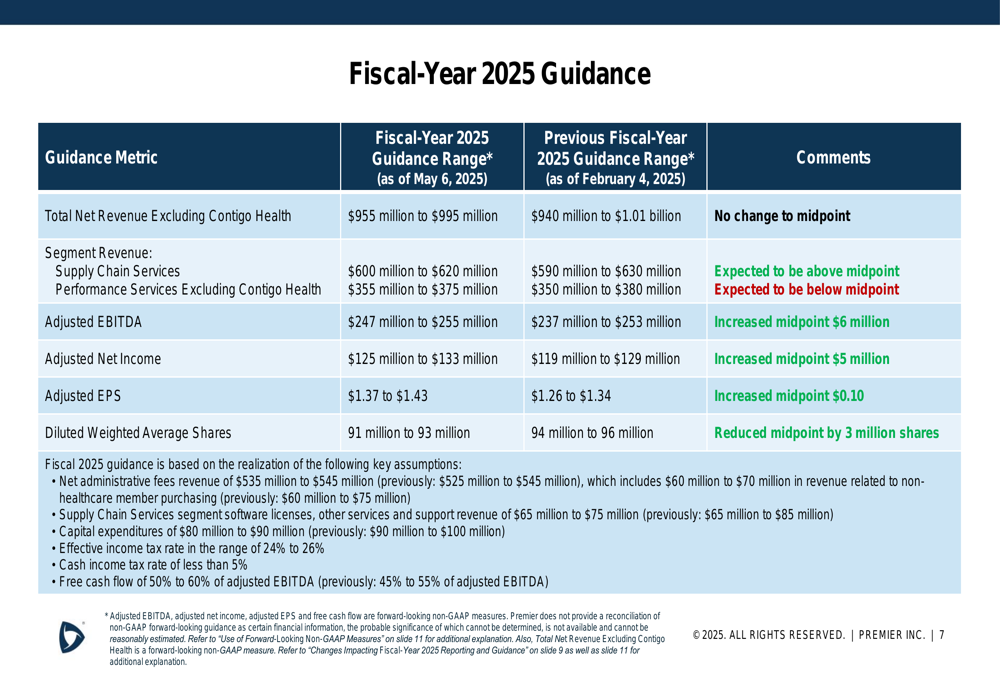

Based on its third-quarter performance, Premier increased its full-year guidance for adjusted EBITDA and adjusted EPS while reaffirming its revenue guidance.

The updated guidance for fiscal year 2025 includes:

- Total (EPA:TTEF) net revenue excluding Contigo Health: $955 million to $995 million (unchanged)

- Supply Chain Services revenue: $600 million to $620 million (expected to be above midpoint)

- Performance Services revenue excluding Contigo Health: $355 million to $375 million (expected to be below midpoint)

- Adjusted EBITDA: $247 million to $255 million (increased midpoint by $6 million)

- Adjusted net income: $125 million to $133 million (increased midpoint by $5 million)

- Adjusted EPS: $1.37 to $1.43 (increased midpoint by $0.10)

The company also reduced its projected diluted weighted average shares to 91-93 million, down by 3 million shares at the midpoint, reflecting the impact of its share repurchase program.

Premier noted several factors impacting its fiscal 2025 reporting and guidance, including the divestiture of S2S Global, the planned transition of Contigo Health businesses, and segment reporting changes. The company also explained that it would exclude the impact of the OMNIA transaction from non-GAAP profitability measures to provide a more comparable basis for analysis.

As Premier continues its strategic transformation, investors will be watching closely to see if the company can successfully reinvigorate its core businesses while maintaining strong cash flow and shareholder returns despite the revenue challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.