Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Prestige Consumer Healthcare Inc (NYSE:PBH) released its first quarter fiscal 2026 results on August 7, 2025, revealing a revenue decline primarily driven by supply chain issues in its Eye Care segment, while maintaining profitability through improved margins. The company’s stock reacted negatively to the results, falling 4.35% in premarket trading to $71.89, moving away from its 52-week high of $90.04.

The healthcare products company, which had been performing well with strong financial health metrics prior to this report, faced unexpected challenges with its Clear Eyes product line that significantly impacted quarterly performance. Despite these headwinds, management announced strategic initiatives to address the supply constraints, including the acquisition of a key supplier.

Quarterly Performance Highlights

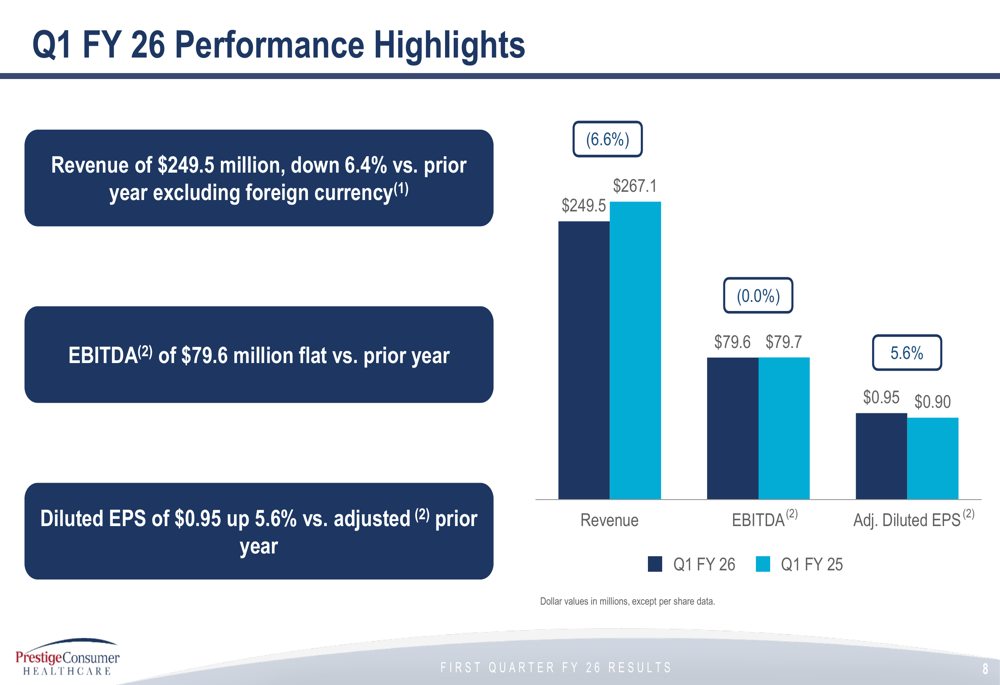

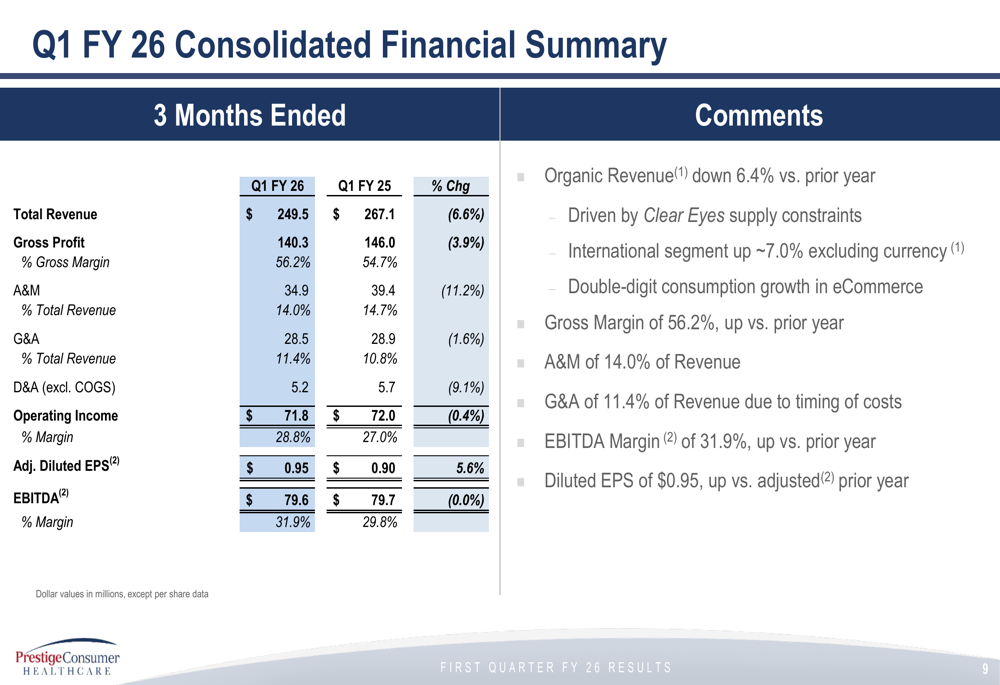

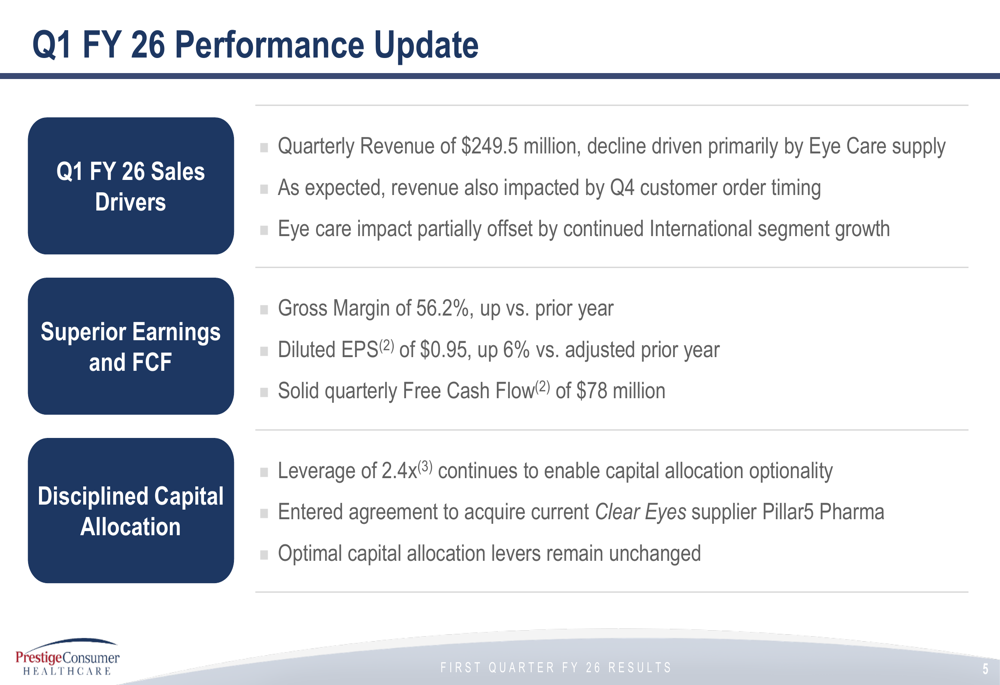

Prestige Consumer Healthcare reported Q1 FY26 revenue of $249.5 million, representing a 6.4% decline compared to the prior year period when excluding foreign currency impacts. Despite this revenue challenge, the company maintained its EBITDA at $79.6 million, flat versus the prior year, while diluted EPS increased by 5.6% to $0.95 compared to adjusted prior year results.

As shown in the following performance highlights chart:

The revenue decline was primarily attributed to Eye Care supply issues, with additional impact from Q4 customer order timing. These negative factors were partially offset by continued growth in the company’s International segment. Despite the revenue challenges, gross margin improved to 56.2% from 54.7% in the prior year period.

Strategic Initiatives

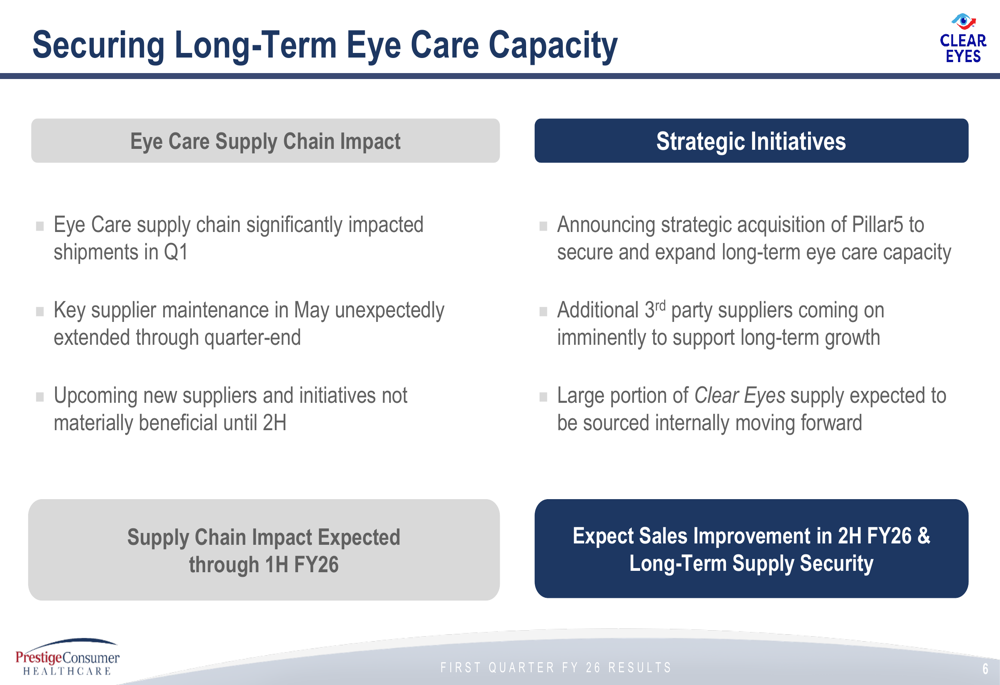

The most significant strategic announcement was Prestige Consumer Healthcare’s agreement to acquire Pillar5 Pharma, a current Clear Eyes supplier, for approximately $100 million. This acquisition is expected to close in the company’s fiscal third quarter and is designed to secure and expand long-term eye care capacity.

The company provided a detailed explanation of both the supply chain challenges and its strategic response:

Management explained that a key supplier’s maintenance in May unexpectedly extended through the end of the quarter, significantly impacting shipments. The company is implementing multiple solutions, including bringing additional third-party suppliers online imminently to support long-term growth. With these initiatives, Prestige expects sales improvement in the second half of fiscal 2026 with long-term supply security.

Detailed Financial Analysis

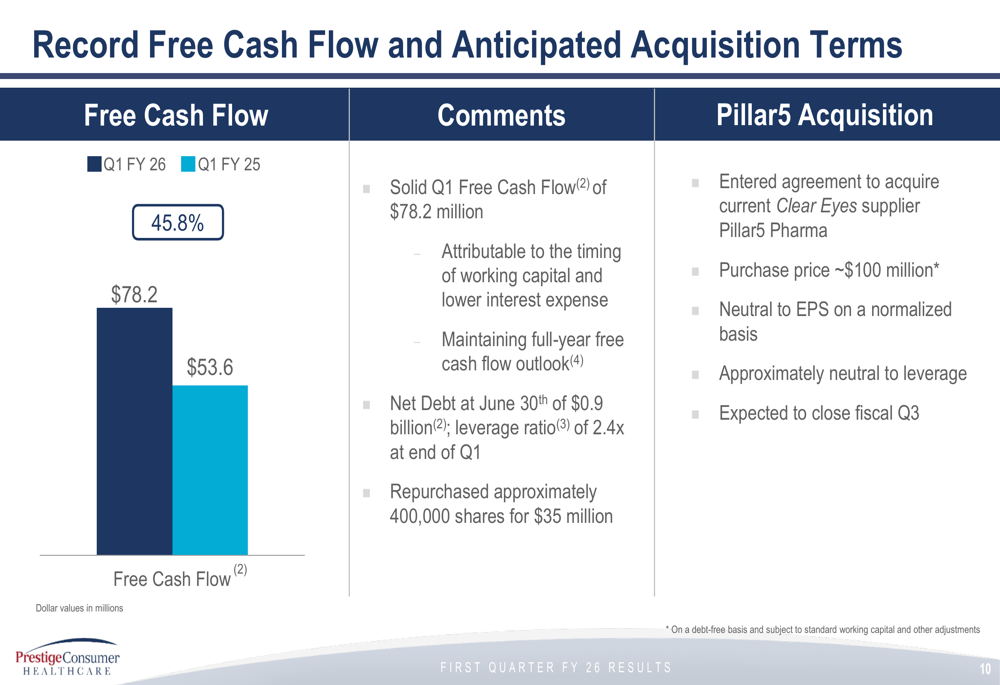

Despite the revenue challenges, Prestige Consumer Healthcare delivered strong cash flow performance in the quarter, generating $78.2 million in free cash flow, a substantial 45.8% increase over the prior year period. This improvement was attributed to favorable timing of working capital and lower interest expense.

The company’s consolidated financial summary reveals the resilience of its business model despite top-line pressure:

Notably, the company maintained disciplined capital allocation during the quarter, with a leverage ratio of 2.4x at the end of Q1. Prestige repurchased approximately 400,000 shares for $35 million, demonstrating confidence in its long-term outlook despite near-term challenges.

The free cash flow performance and acquisition terms were highlighted in the presentation:

Management noted that the Pillar5 acquisition is expected to be neutral to EPS on a normalized basis and approximately neutral to the company’s leverage position.

Forward-Looking Statements

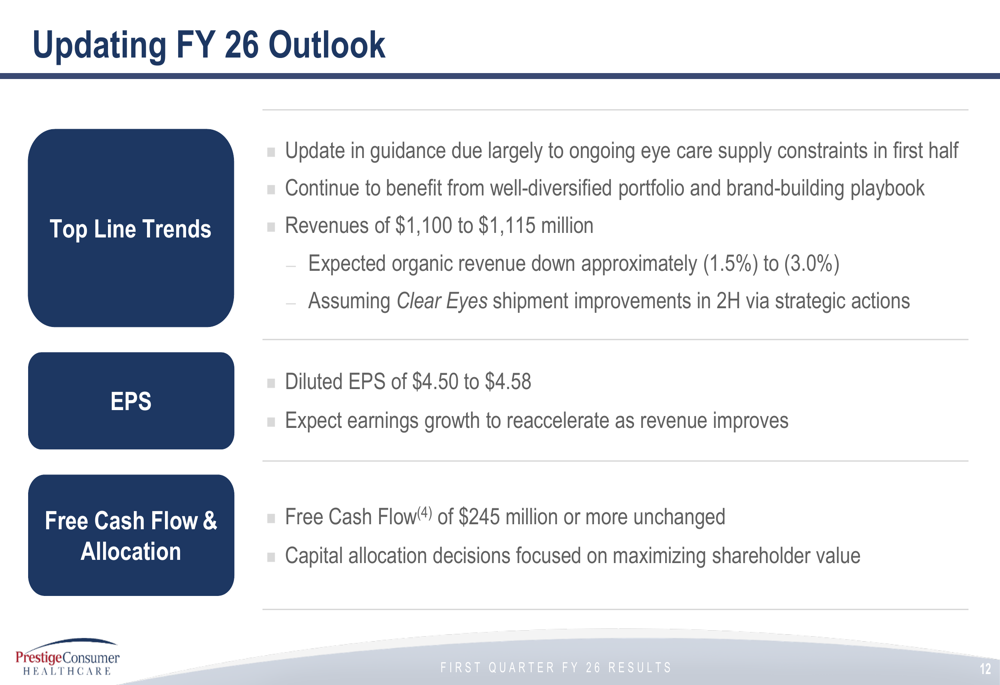

In light of the ongoing eye care supply constraints, Prestige Consumer Healthcare updated its fiscal 2026 outlook. The company now expects revenues of $1,100 to $1,115 million, with organic revenue declining approximately 1.5% to 3.0%. This guidance assumes Clear Eyes shipment improvements in the second half of the fiscal year as the strategic actions take effect.

Despite the revenue adjustment, the company maintained its free cash flow guidance of $245 million or more for the full year, unchanged from previous expectations. Diluted EPS is now projected to be in the range of $4.50 to $4.58, with management expecting earnings growth to reaccelerate as revenue improves in the second half.

The company continues to benefit from its well-diversified portfolio and brand-building strategy, which has helped mitigate the impact of the Clear Eyes supply challenges. Management emphasized that capital allocation decisions remain focused on maximizing shareholder value, with the Pillar5 acquisition representing a strategic investment to secure future growth.

Executive Summary

Prestige Consumer Healthcare’s first quarter results demonstrate the company’s ability to maintain profitability and cash flow generation despite significant supply chain challenges. The 6.4% revenue decline was offset by improved gross margins and disciplined cost management, resulting in a 5.6% increase in adjusted diluted EPS.

The company’s comprehensive performance update summarizes the quarter’s key drivers and strategic initiatives:

The acquisition of Pillar5 Pharma represents a proactive step to address the supply chain vulnerabilities exposed during the quarter. By securing internal manufacturing capacity for a significant portion of its Clear Eyes product line, Prestige is positioning itself for more stable long-term growth while reducing dependency on external suppliers.

While the updated outlook reflects near-term challenges, management’s maintained free cash flow guidance and strategic investments suggest confidence in the company’s ability to navigate the current headwinds and return to growth in the latter half of fiscal 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.