S&P 500 falls on pressure from retail stocks, weak jobless claims

Primis Financial Corp (NASDAQ:FRST) presented its second quarter 2025 results showing improved financial metrics and progress toward its targeted return on assets goal, with specialized lending segments driving growth despite earlier challenges in the year.

Quarterly Performance Highlights

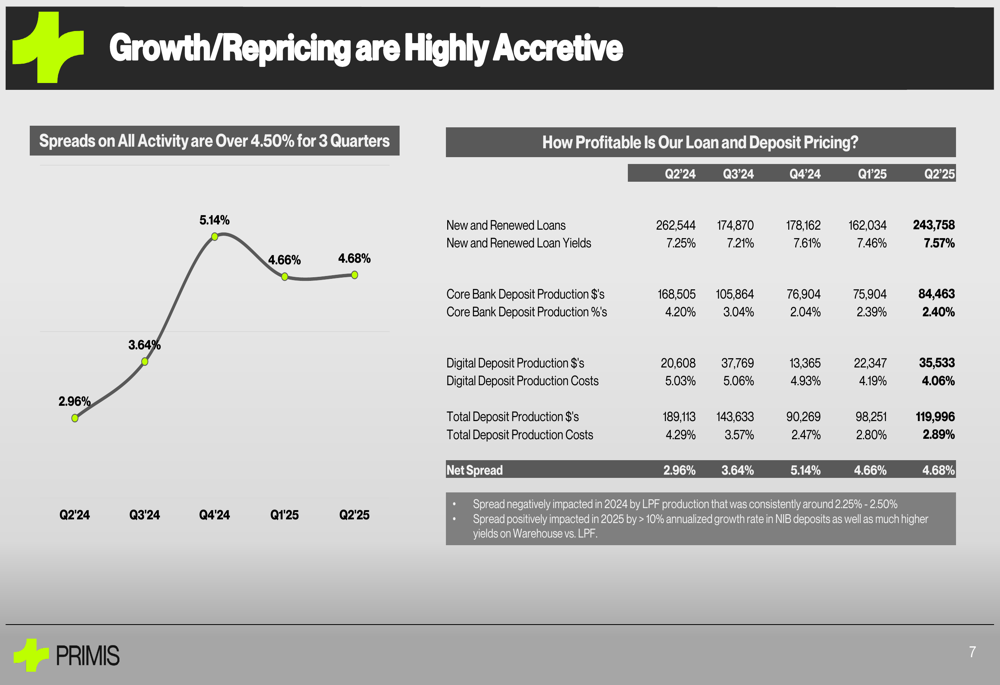

Primis reported a return on assets (ROA) of 0.89% for Q2 2025, moving closer to management’s previously stated 1% target. The company’s core net interest margin improved to 3.15%, up from 2.91% in Q4 2024 and 3.13% in Q1 2025, reflecting the positive impact of higher-yielding new loans and improved deposit strategies.

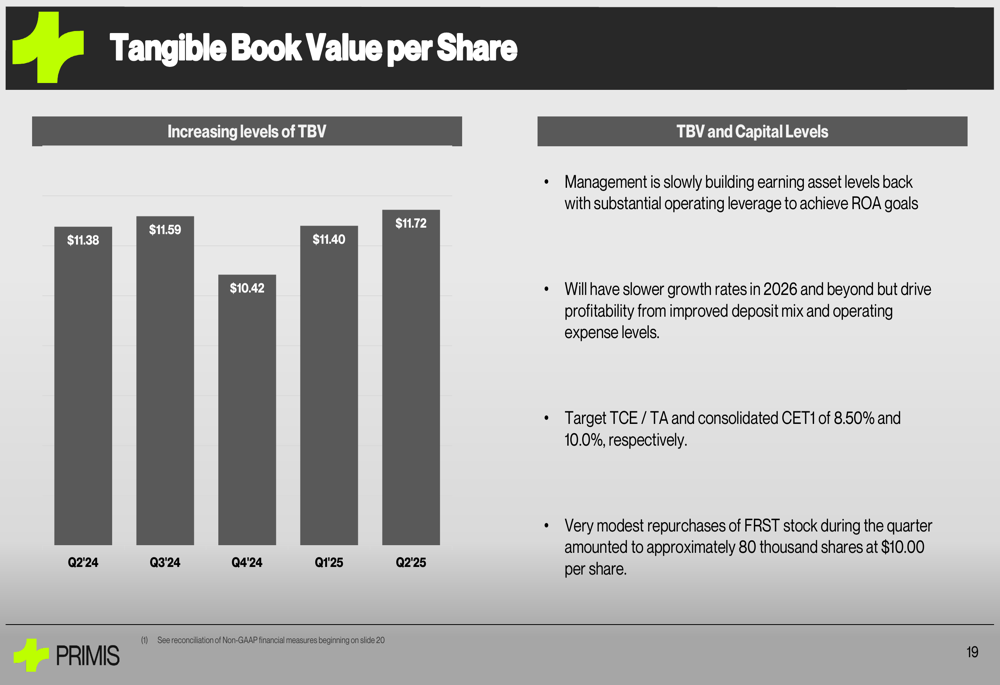

The company’s tangible book value per share reached $11.72 in Q2 2025, continuing its recovery from a dip to $10.42 in Q4 2024 and representing growth from $11.38 in the year-ago quarter.

As shown in the following chart of tangible book value progression:

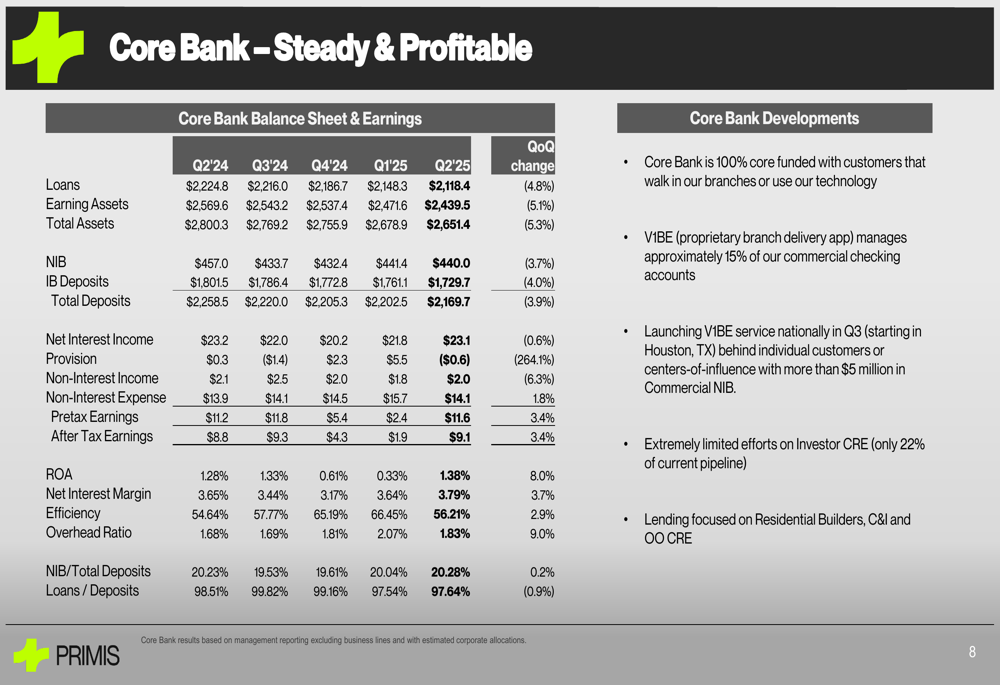

The core bank demonstrated solid performance with after-tax earnings of $9.1 million and an ROA of 1.38% in Q2 2025. The efficiency ratio improved to 56.21%, indicating better operational leverage. These results represent a significant improvement from Q1 2025, when the company reported an EPS of $0.14, missing analyst expectations of $0.26.

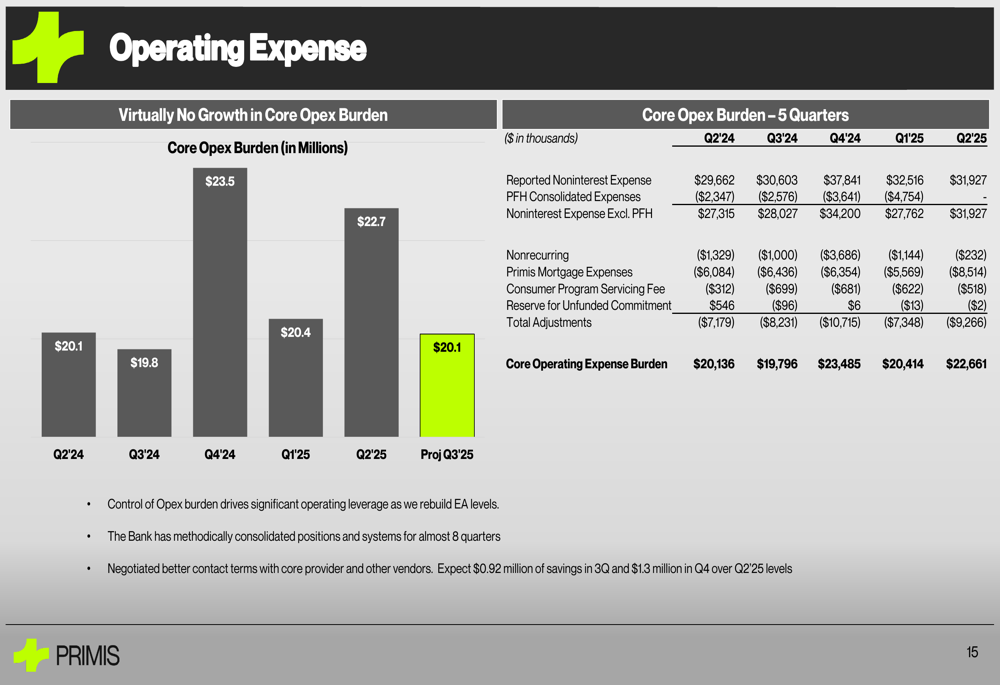

The following table illustrates the core bank’s steady performance:

Growth Drivers and Strategic Initiatives

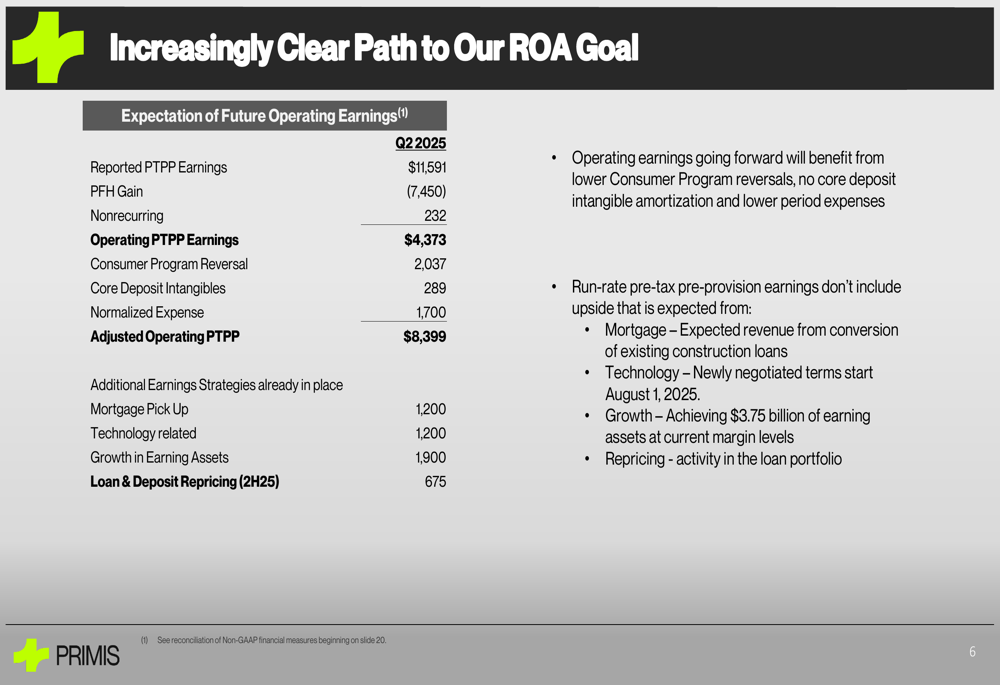

Primis has outlined a clear path to achieving its ROA goals through several strategic initiatives. The company’s presentation detailed specific earnings drivers already in place, including mortgage business improvement ($1.2 million), technology-related savings ($1.2 million), growth in earning assets ($1.9 million), and loan and deposit repricing ($675,000).

The company’s roadmap to improved profitability is illustrated here:

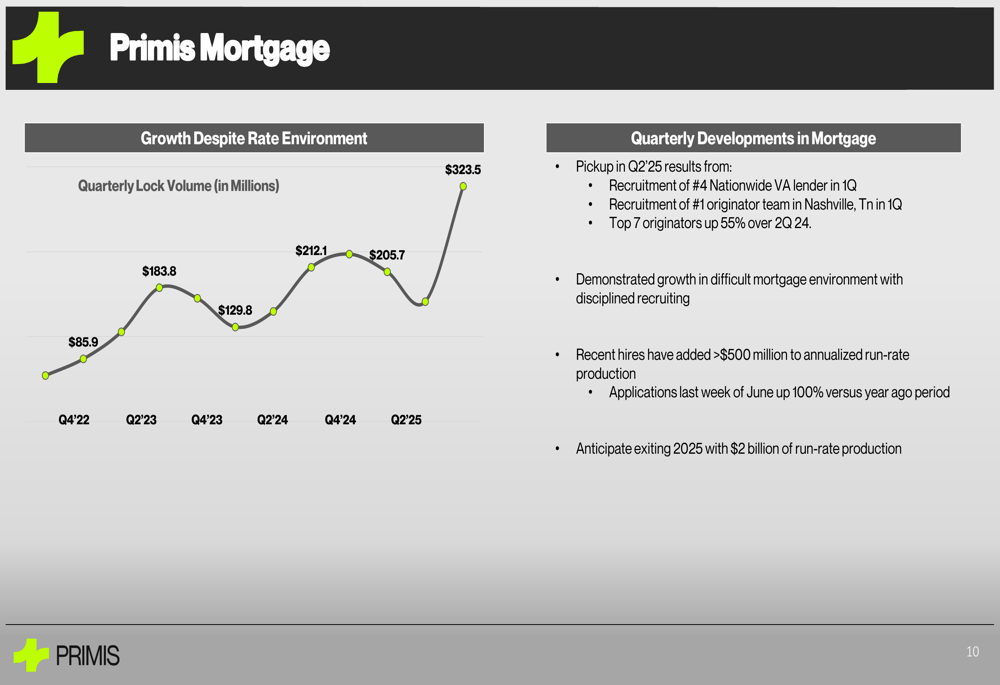

The mortgage business has shown particularly strong growth despite the challenging interest rate environment. Quarterly lock volume reached $323.5 million in Q2 2025, up significantly from $85.9 million in Q4 2022 and $205.7 million in Q4 2024. This growth has been driven by new team recruitment and expanded market presence.

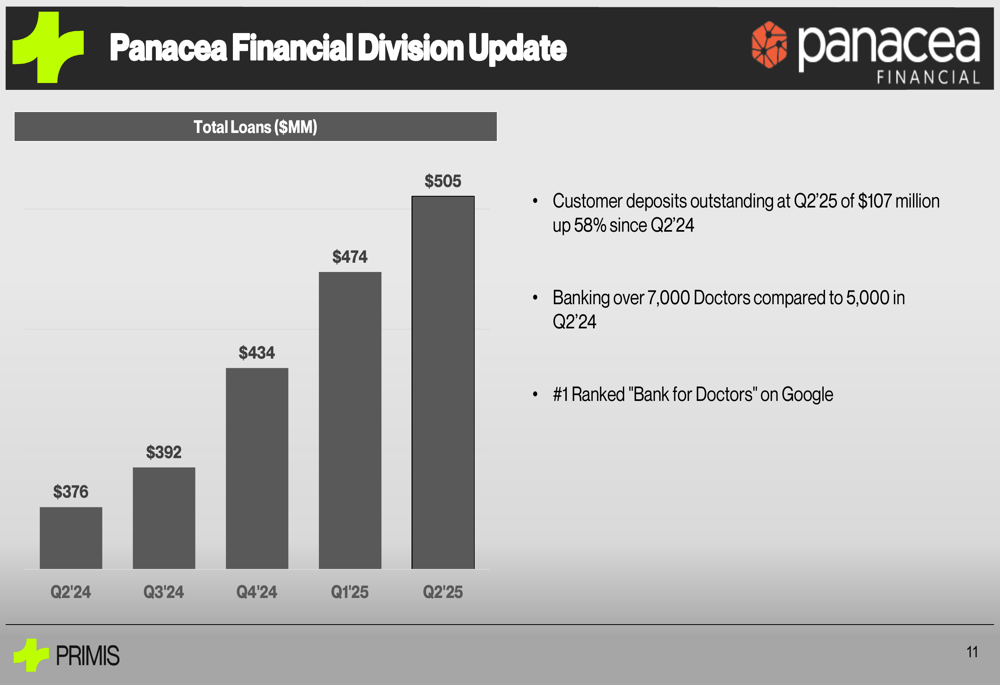

Another key growth driver is the Panacea Financial Division, which focuses on healthcare professionals. Total (EPA:TTEF) loans in this segment have grown consistently from $376 million in Q2 2024 to $505 million in Q2 2025, demonstrating the success of this specialized lending strategy.

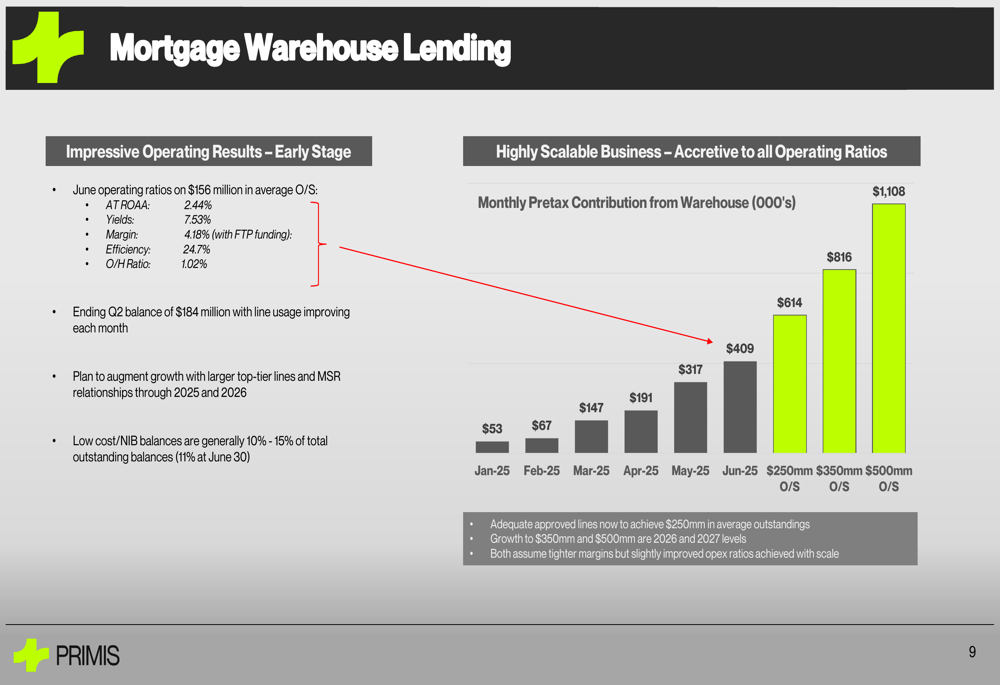

The mortgage warehouse lending business has also emerged as a significant contributor, with June 2025 showing an after-tax ROA of 2.44% and an efficiency ratio of just 24.7%. Monthly pretax contribution from this segment has grown from $53,000 in January 2025 to $409,000 in June 2025.

Asset Quality and Risk Management

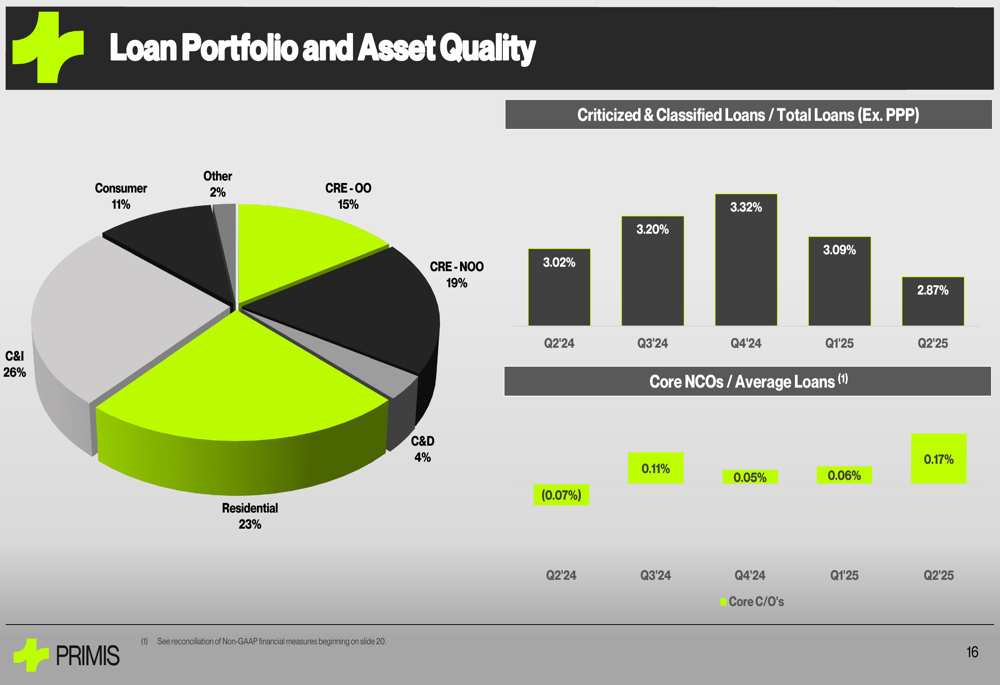

Primis has maintained strong asset quality metrics, with criticized and classified loans decreasing to 2.87% in Q2 2025 from 3.02% a year earlier. Core net charge-offs to average loans remained low at 0.17% for the quarter.

The loan portfolio is well-diversified, with commercial and industrial loans comprising 26%, residential loans 23%, and commercial real estate (owner-occupied and non-owner-occupied) totaling 34%. This diversification helps mitigate concentration risk.

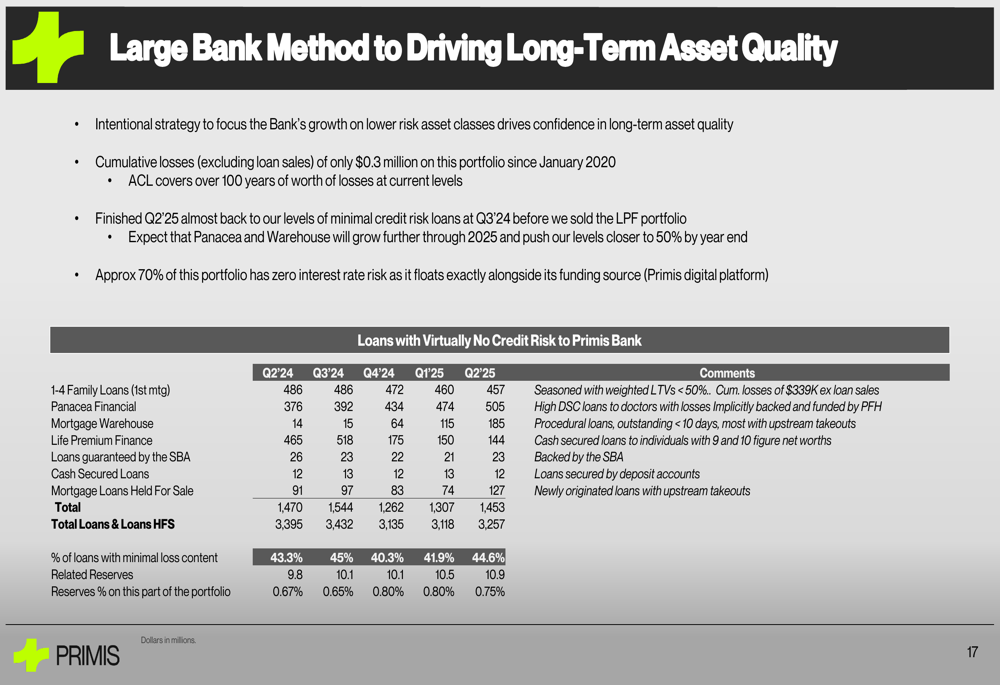

The company employs what it calls a "Large Bank Method" to drive long-term asset quality, focusing on loans with minimal loss content. This approach has resulted in a significant portion of the portfolio having virtually no credit risk to Primis Bank.

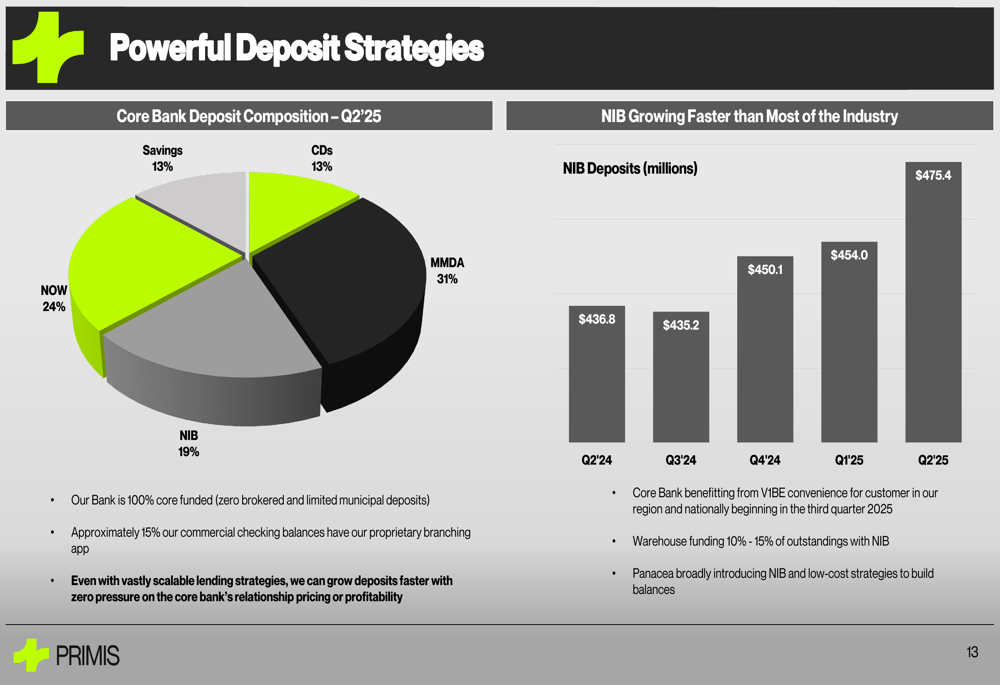

Deposit Strategies and Funding

Primis maintains a 100% core-funded deposit base, with non-interest-bearing (NIB) deposits comprising 19% of total core bank deposits. NIB deposits have shown steady growth, reaching $475.4 million in Q2 2025, up from $436.8 million a year earlier.

The deposit composition and NIB trend are illustrated in the following charts:

The company has achieved attractive spreads on new business, with new and renewed loans in Q2 2025 yielding 7.57% against total deposit production costs of 2.89%, resulting in a net spread of 4.68%.

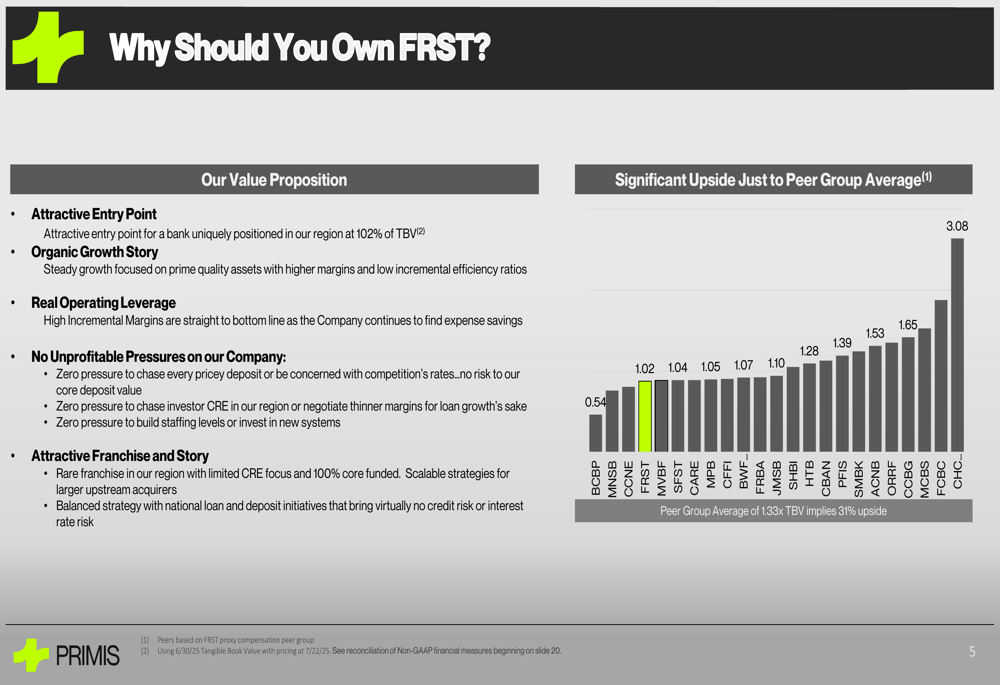

Valuation and Forward Outlook

Primis currently trades at 102% of tangible book value, compared to a peer average of 133%, suggesting a potential 31% upside if the valuation gap closes. Management highlighted this as an attractive entry point for investors, coupled with the company’s organic growth story and operating leverage.

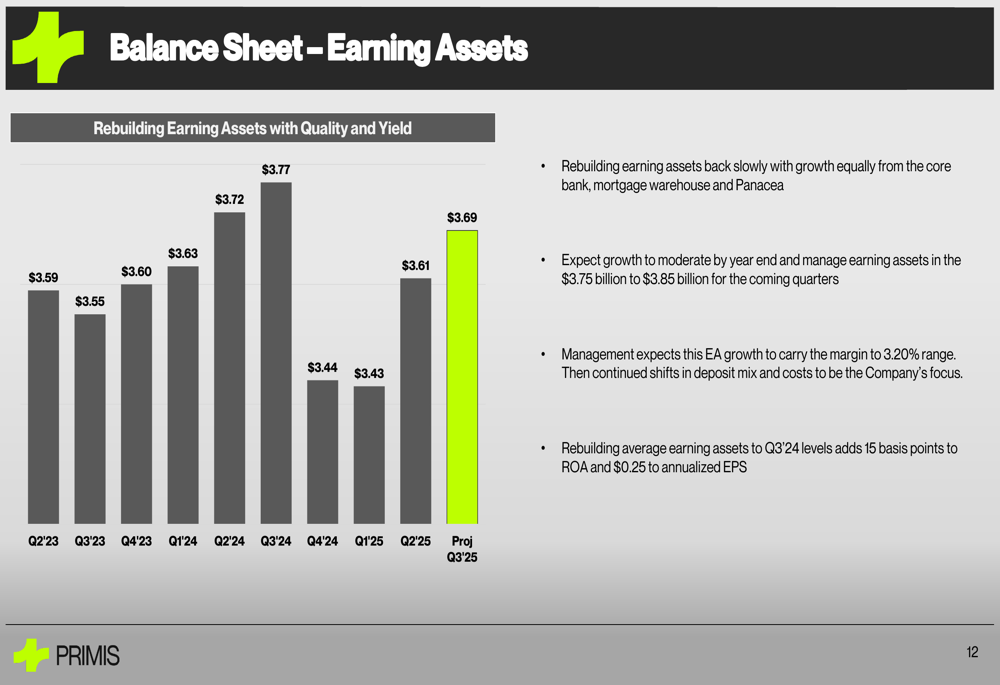

The company is focused on rebuilding earning assets with quality and yield after a dip in Q4 2024 and Q1 2025. Management projects continued growth in earning assets into Q3 2025.

Operating expenses have been well-controlled, with core operating expense expected to normalize at around $20.1 million in Q3 2025 after a temporary increase to $22.7 million in Q2 2025. This discipline in expense management is crucial to achieving the company’s profitability targets.

Primis Financial appears to be on a recovery path after disappointing Q1 2025 results, with improvements in key metrics and specialized lending segments driving growth. The stock has recovered from its post-Q1 decline, trading at $12.10 as of the latest close, up significantly from the $8.34 level seen after the Q1 earnings release. While challenges remain, the company’s strategic initiatives and improving financial metrics suggest progress toward its stated goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.