Fubotv earnings beat by $0.10, revenue topped estimates

Primo Water Corp (NYSE:PRMB) shares plunged over 11% in premarket trading Thursday after the company’s Q2 2025 earnings presentation revealed mixed results, with comparable sales declining despite margin improvements. The bottled water giant faced significant operational challenges, including tornado damage to a key facility, while its premium brands continued to deliver strong growth.

Quarterly Performance Highlights

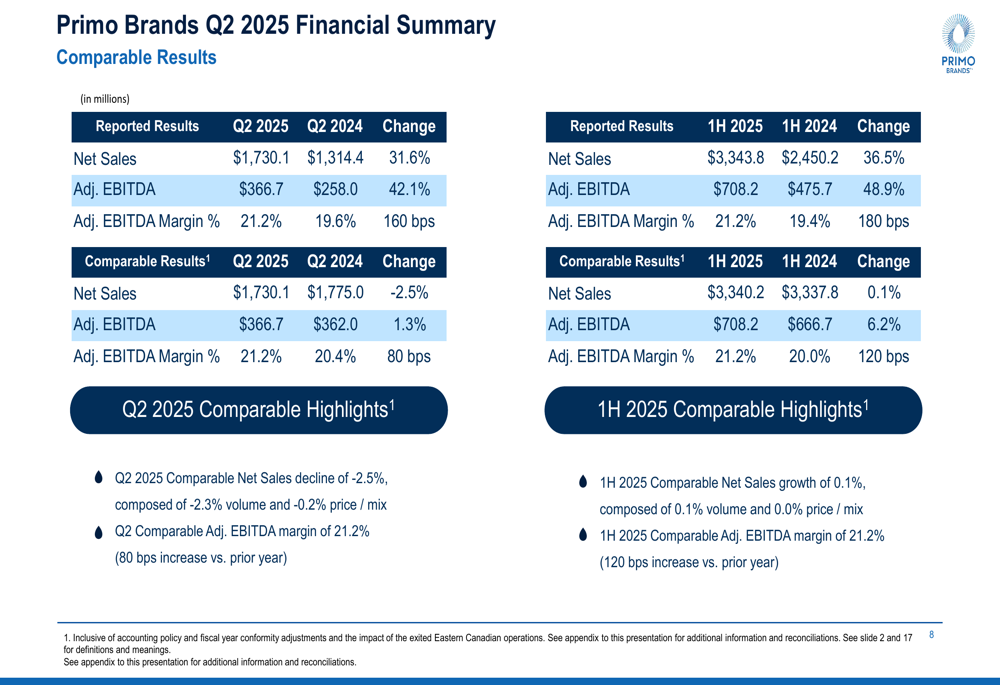

Primo Water reported Q2 2025 net sales of $1,730.1 million, representing a 31.6% increase on a reported basis. However, on a comparable basis, net sales declined by 2.5%. Adjusted EBITDA reached $366.7 million, up 42.1% from the prior year, with adjusted EBITDA margin expanding to 21.2%, a 160 basis point improvement.

For the first half of 2025, reported net sales totaled $3,343.8 million, up 36.5%, while comparable net sales showed minimal growth of 0.1%. First-half adjusted EBITDA increased 48.9% to $708.2 million, with margins improving 180 basis points to 21.2%.

As shown in the following financial summary:

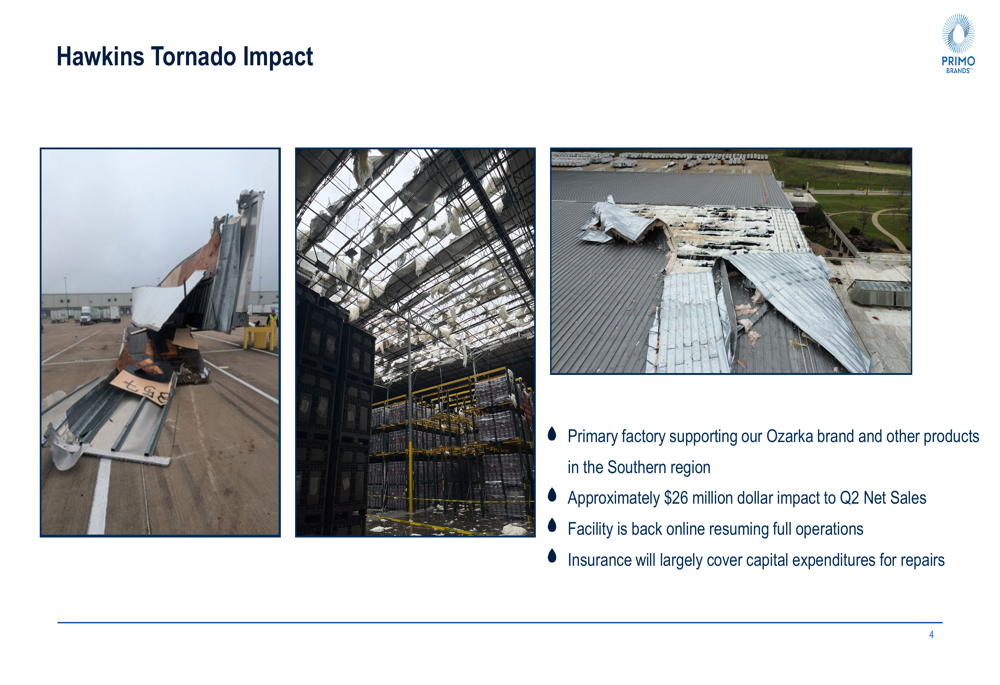

The company’s results were significantly impacted by a tornado that struck its Hawkins (NASDAQ:HWKN) facility, a primary source for the Ozarka brand and other products in the Southern region. The natural disaster caused approximately $26 million in lost Q2 net sales, though the company noted the facility is now back online with full operations resuming. Insurance is expected to cover most capital expenditures for repairs.

The tornado damage to the manufacturing facility is depicted here:

Premium Segment Success

The premium water channel emerged as a bright spot in Primo’s portfolio, with Mountain Valley and Saratoga brands delivering 44.2% year-over-year net sales growth in Q2. The company attributed this success to expanded PET (polyethylene terephthalate) offerings, which fueled growth in total points of distribution.

To address supply constraints and support continued growth in this segment, Primo broke ground on a new Mountain Valley facility in Hot Springs, Arkansas during Q2 2025, with completion anticipated by the first half of 2026.

The premium brands and new facility construction are shown here:

Operational Challenges and Recovery Plans

Beyond the tornado impact, Primo Water faces challenges in its direct delivery segment, which serves homes and offices. The company outlined a comprehensive recovery plan focusing on five key areas: product supply, logistics planning, route optimization, recovery actions, and operations updates.

"We’re implementing weekend and holiday route delivery, bottle recovery initiatives, and customer service promotions to improve our direct delivery performance," said Robbert Rietbroek, Chief Executive Officer, during the presentation.

Additionally, the company’s water dispenser business, representing approximately 1% of total net sales, faces uncertainty due to tariff implications. Management noted they are working with suppliers on promotional spending to mitigate these impacts, while emphasizing that 98% of company-wide net sales are U.S.-based, limiting overall tariff exposure.

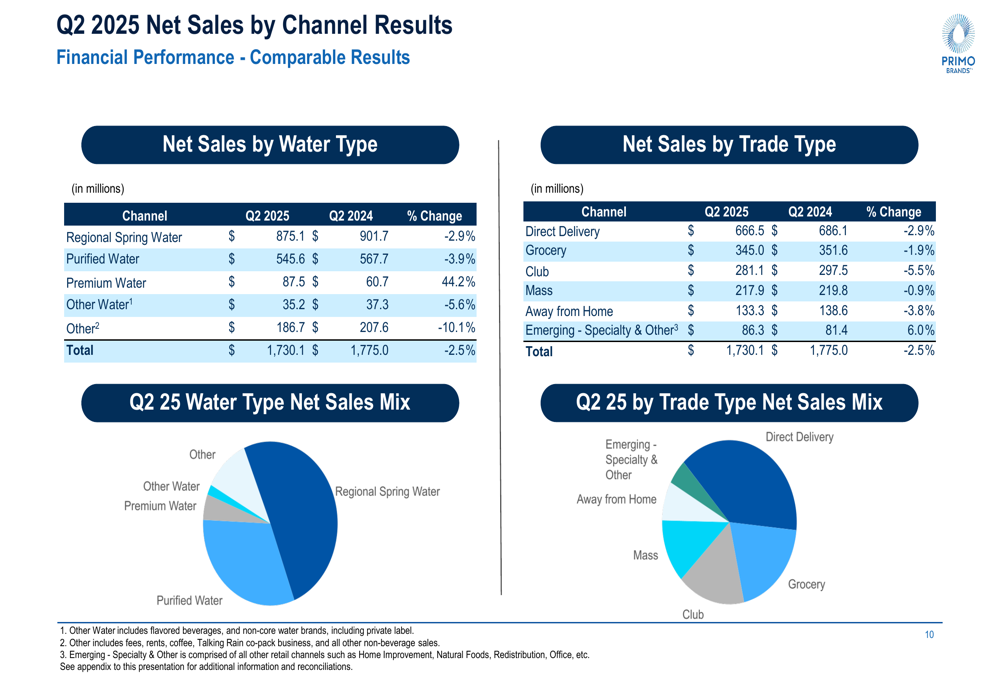

The sales mix by water type and trade channel for Q2 2025 is illustrated in these charts:

Financial Position and Outlook

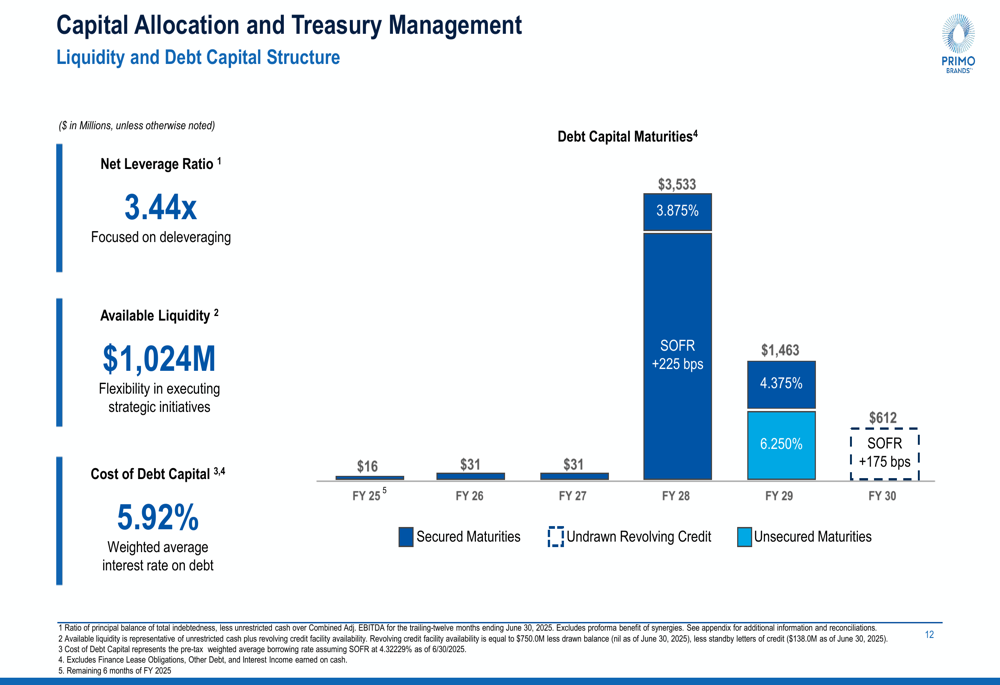

Primo Water reported a net leverage ratio of 3.44x, with management emphasizing a focus on deleveraging. The company maintains strong liquidity of $1,024 million, providing flexibility for strategic initiatives, with a current cost of debt capital at 5.92%.

The company’s debt maturity profile shows minimal near-term obligations, with only $16 million maturing in FY25 and $31 million in both FY26 and FY27. The majority of debt matures in FY28 ($3,533 million) and FY29 ($1,463 million).

The debt maturity schedule is shown here:

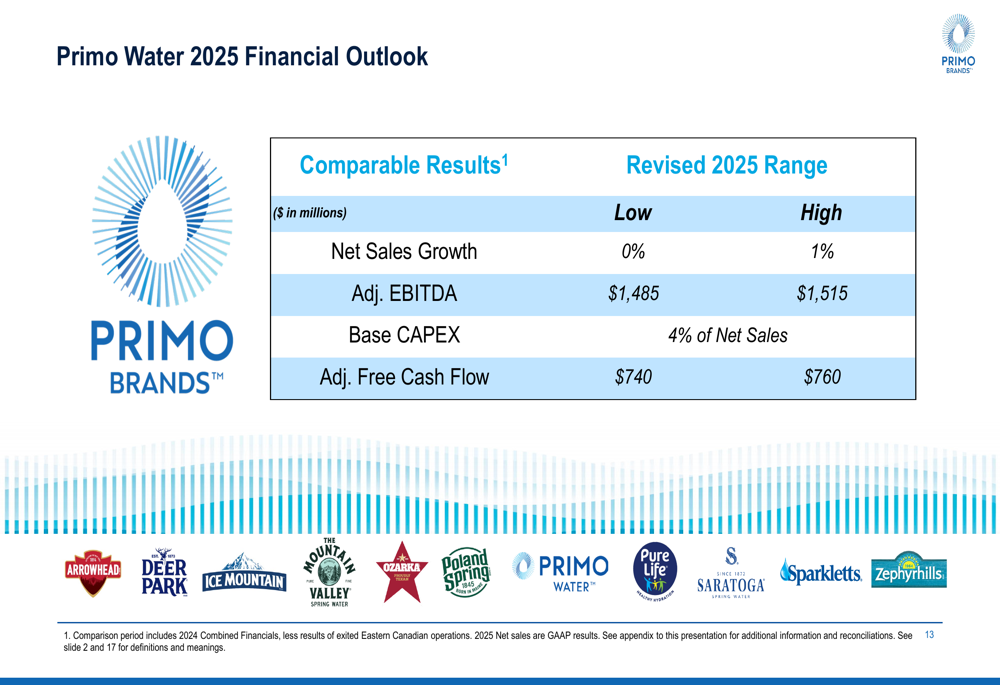

Looking ahead, Primo Water provided its 2025 financial outlook, projecting modest net sales growth of 0-1%, adjusted EBITDA of $1,485-$1,515 million, capital expenditures at 4% of net sales, and adjusted free cash flow of $740-$760 million.

The company’s full-year guidance is detailed here:

Synergy Opportunities

Following its merger with BlueTriton, Primo Water identified significant cost synergy opportunities across multiple functional areas. These include optimizing manufacturing locations, routes, branches, and inventory management; improving procurement efficiencies; leveraging BlueTriton’s newly implemented ERP system; aligning call center operations; and streamlining systems and processes across key functional areas.

The stock’s sharp premarket decline suggests investors may be concerned about the sales decline and modest growth outlook, despite margin improvements and premium segment success. This reaction contrasts with the company’s strong performance in 2024, when it delivered 5.4% net sales growth and a 19.5% increase in adjusted EBITDA.

As Primo Water navigates operational challenges while pursuing synergy opportunities, investors will be watching closely to see if management can deliver on its recovery plans and financial targets for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.