JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Principal Financial Group (NYSE:NASDAQ:PFG) reported solid first-quarter 2025 results on April 24, delivering 10% earnings per share growth and returning $370 million to shareholders through dividends and share repurchases.

Quarterly Performance Highlights

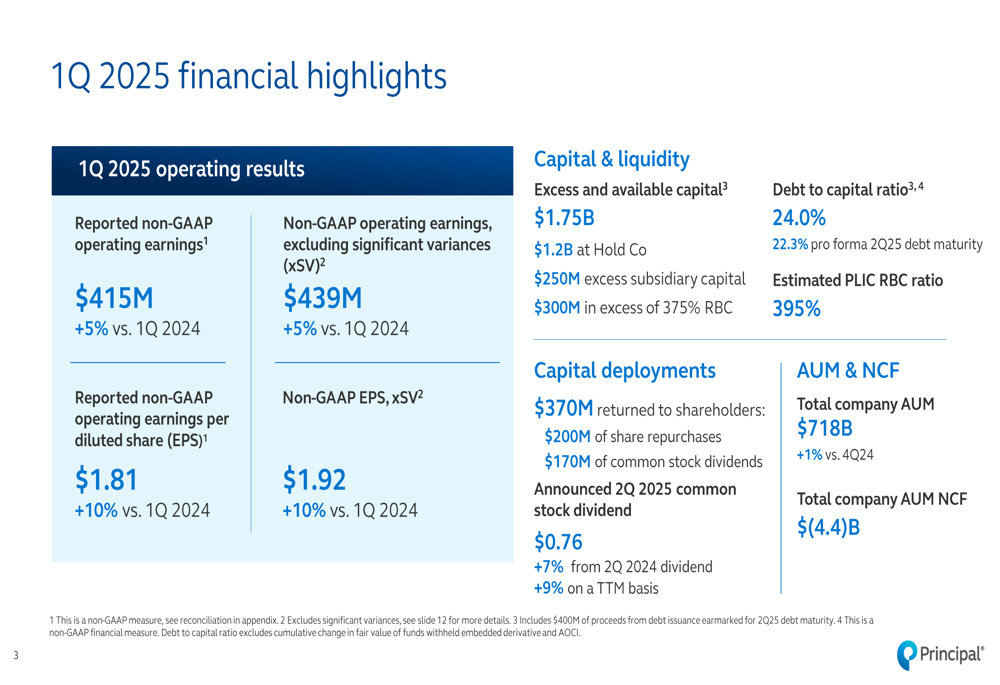

Principal reported non-GAAP operating earnings of $415 million for the first quarter, up 5% compared to the same period in 2024. Non-GAAP operating earnings per diluted share increased 10% to $1.81, while adjusted EPS excluding significant variances reached $1.92, also up 10% year-over-year.

The company’s return on equity stood at 14.0%, within its long-term target range of 14-16%, while trailing twelve-month free cash flow reached 84% of net income, at the high end of the 75-85% target range.

As shown in the following financial highlights slide, Principal maintained a strong capital position with $1.75 billion in excess and available capital, including $1.2 billion at the holding company level:

Total (EPA:TTEF) assets under management (AUM) reached $718 billion, a 1% increase from the fourth quarter of 2024. However, the company experienced negative net cash flow of $(4.4) billion, primarily driven by $(3.0) billion of low-fee institutional outflows in the asset management business.

Segment Performance Analysis

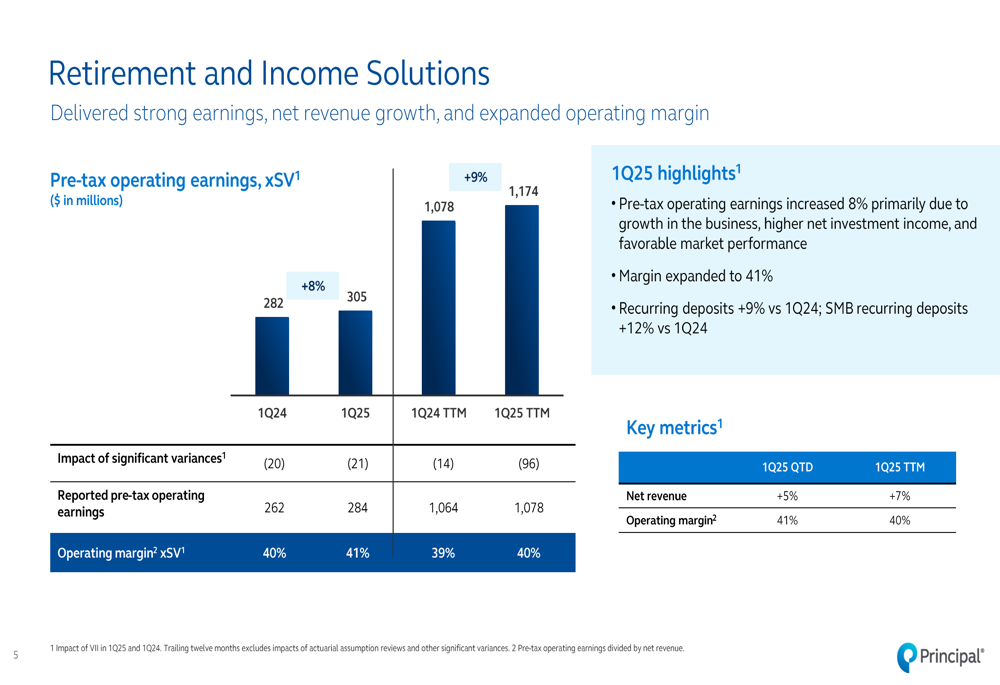

Principal’s Retirement and Income Solutions segment delivered strong results, with pre-tax operating earnings increasing 8% year-over-year to $305 million. The segment’s margin expanded to 41%, driven by business growth, higher net investment income, and favorable market performance. Recurring deposits grew 9% compared to Q1 2024, with small and medium-sized business (SMB) recurring deposits up 12%.

The following slide illustrates the segment’s consistent earnings growth trajectory:

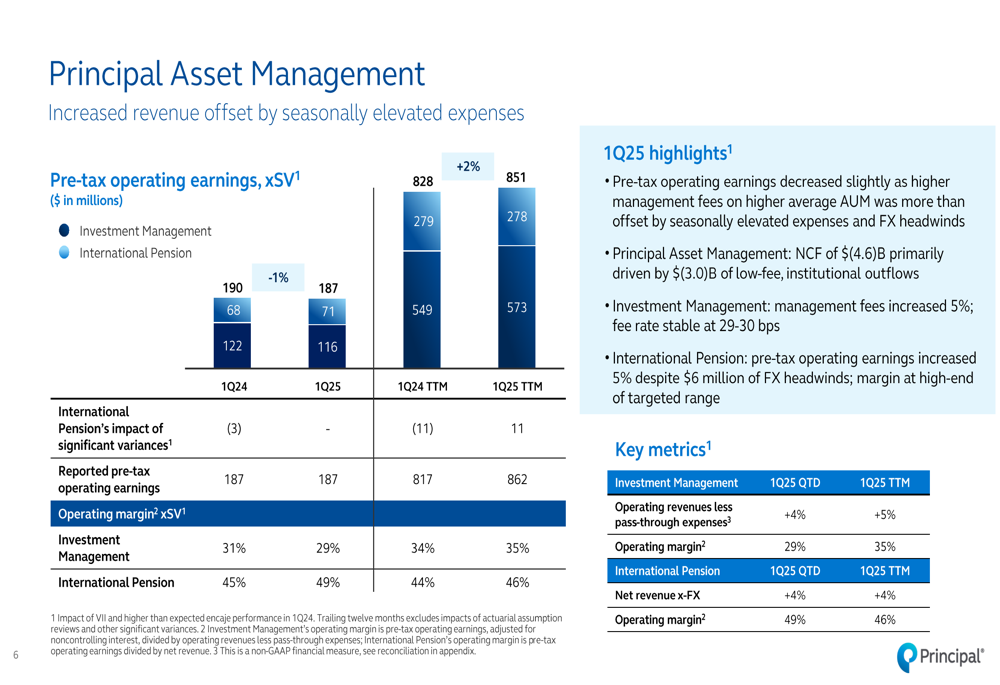

Principal Asset Management saw mixed results as higher management fees on increased AUM were offset by seasonally elevated expenses and foreign exchange headwinds. Investment Management’s management fees increased 5% with a stable fee rate of 29-30 basis points. The International Pension business increased pre-tax operating earnings by 5% despite $6 million in FX headwinds, maintaining margins at the high end of the targeted range.

The company’s asset management performance is detailed in this slide:

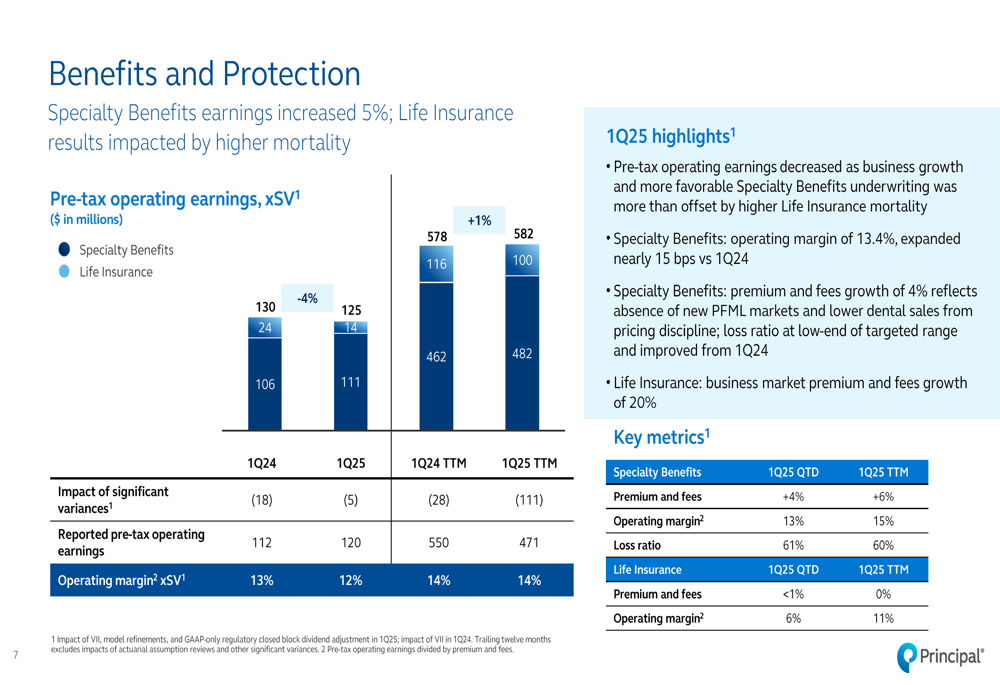

In the Benefits and Protection segment, Specialty Benefits earnings increased 5% with an operating margin of 13.4%, expanding nearly 15 basis points compared to Q1 2024. The loss ratio improved 40 basis points from the prior year, reaching the low end of the targeted range due to more favorable underwriting experience in group disability and group life.

Life Insurance (NSE:LIFI) results were impacted by higher mortality, though the business market saw premium and fee growth of 20% year-over-year.

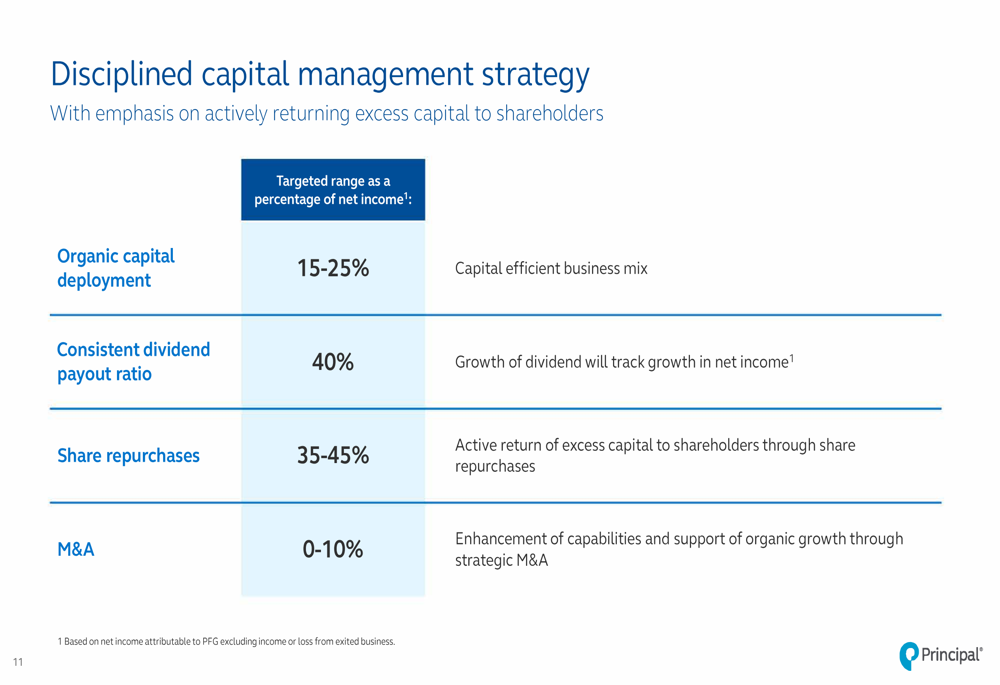

Capital Management & Shareholder Returns

Principal maintained its disciplined approach to capital management, returning $370 million to shareholders during the quarter through $200 million in share repurchases and $170 million in common stock dividends.

The company announced a Q2 2025 common stock dividend of $0.76 per share, representing a 7% increase from the Q2 2024 dividend and a 9% increase on a trailing twelve-month basis.

Principal’s capital deployment strategy continues to balance organic growth, dividends, share repurchases, and strategic acquisitions:

The company’s debt-to-capital ratio stood at 22.3% (pro forma for Q2 2025 debt maturity), while the estimated RBC ratio for Principal Life Insurance Company was 395%, well above regulatory requirements.

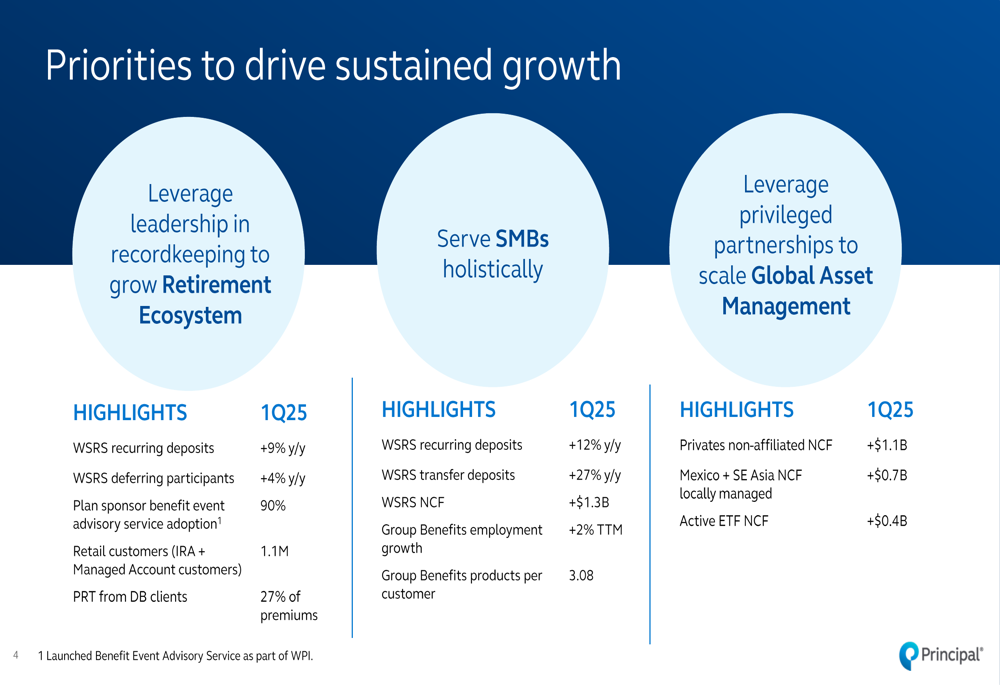

Strategic Initiatives & Growth Priorities

Principal outlined three key priorities to drive sustained growth: leveraging its leadership in recordkeeping to grow the retirement ecosystem, serving small and medium-sized businesses holistically, and scaling global asset management through privileged partnerships.

The company highlighted several achievements in these areas, including 9% year-over-year growth in workplace savings and retirement solutions recurring deposits, 4% growth in deferring participants, and 90% adoption of plan sponsor benefit event advisory services.

The following slide details these strategic priorities:

In asset management, Principal reported $1.1 billion in non-affiliated net cash flow for private real estate, $0.7 billion in locally managed strategies in Mexico and Southeast Asia, and $0.4 billion in active ETF net cash flow.

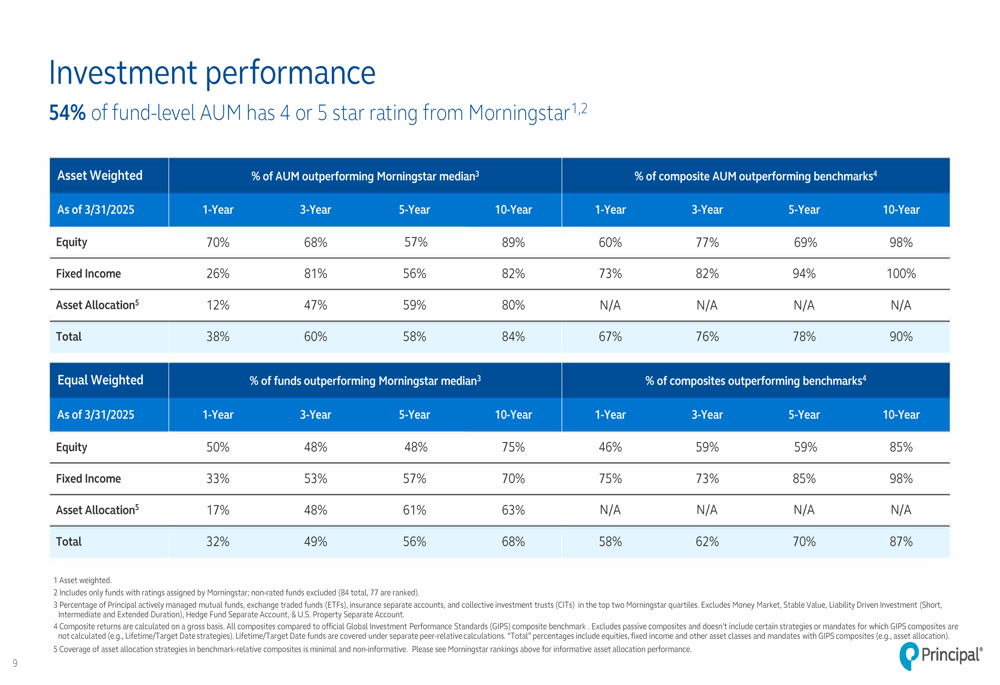

Investment performance remained strong, with 54% of fund-level AUM receiving 4 or 5-star ratings from Morningstar. Over the long term, 84% of asset-weighted AUM outperformed the Morningstar median over 10 years.

Forward Outlook

Principal Financial Group appears well-positioned to continue meeting its long-term financial targets, with EPS growth tracking at the 9-12% target range and ROE within the 14-16% target. The company’s focus on capital-efficient businesses, consistent dividend growth, and strategic share repurchases supports its disciplined capital management approach.

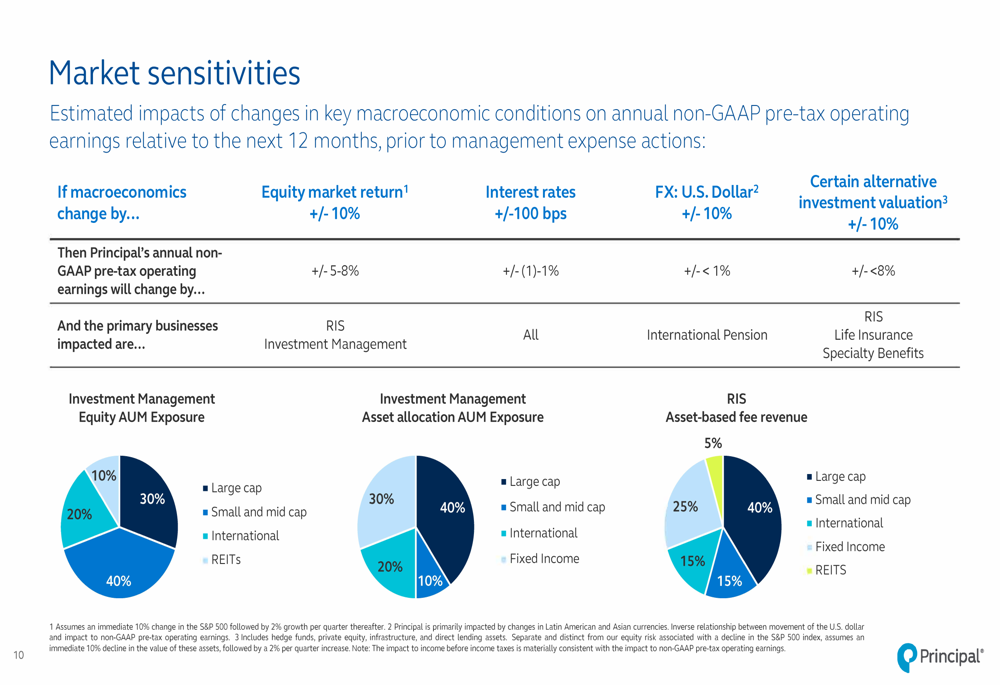

The company’s market sensitivities indicate that a 10% change in equity markets would impact annual pre-tax operating earnings by 5-8%, primarily affecting the Retirement and Income Solutions and Investment Management segments:

Principal’s Q1 2025 results demonstrate the company’s ability to deliver consistent earnings growth while navigating market challenges. With a strong capital position, expanding margins in key businesses, and strategic focus on high-growth areas, Principal continues to execute on its long-term strategy of delivering value to shareholders while growing its core businesses.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.