TSX up after index logs fresh record high close

Introduction & Market Context

Principal Financial Group (NYSE:NASDAQ:PFG) presented its second quarter 2025 earnings results on July 28, 2025, revealing strong performance across most business segments. The company’s shares closed at $81.05, down 0.8% on the day, but the robust quarterly results represent a significant improvement from the first quarter’s performance when the company missed analyst expectations.

The Q2 results demonstrate a substantial recovery from Q1 2025, when Principal reported an EPS of $1.81 that fell short of the forecasted $1.89. This quarter’s strong performance comes amid continued market volatility, with the company effectively leveraging its diversified business model to exceed its long-term guidance targets.

Quarterly Performance Highlights

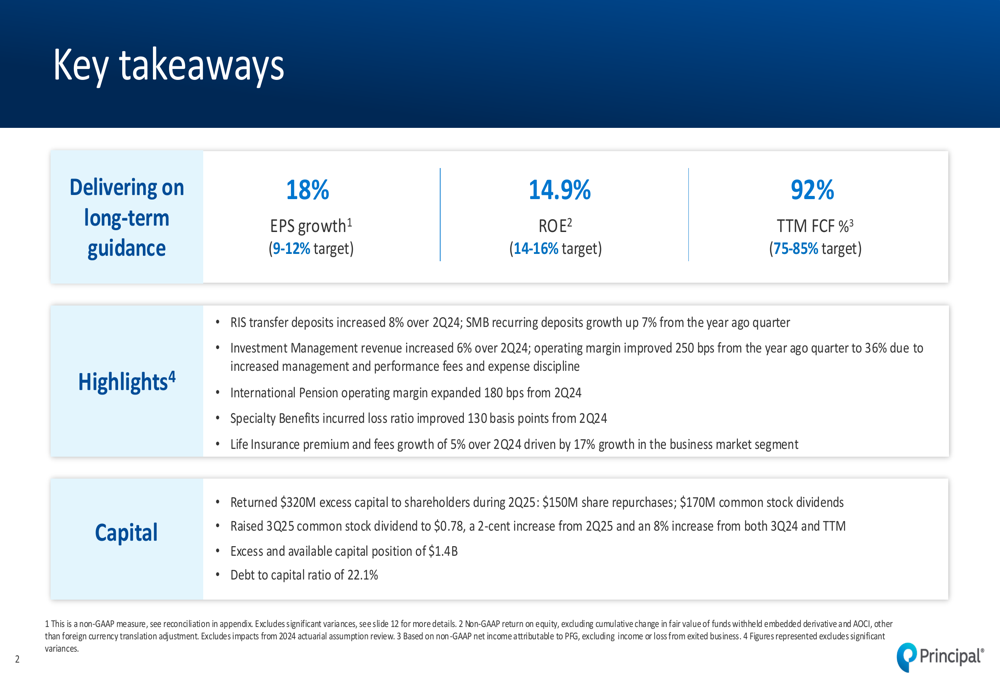

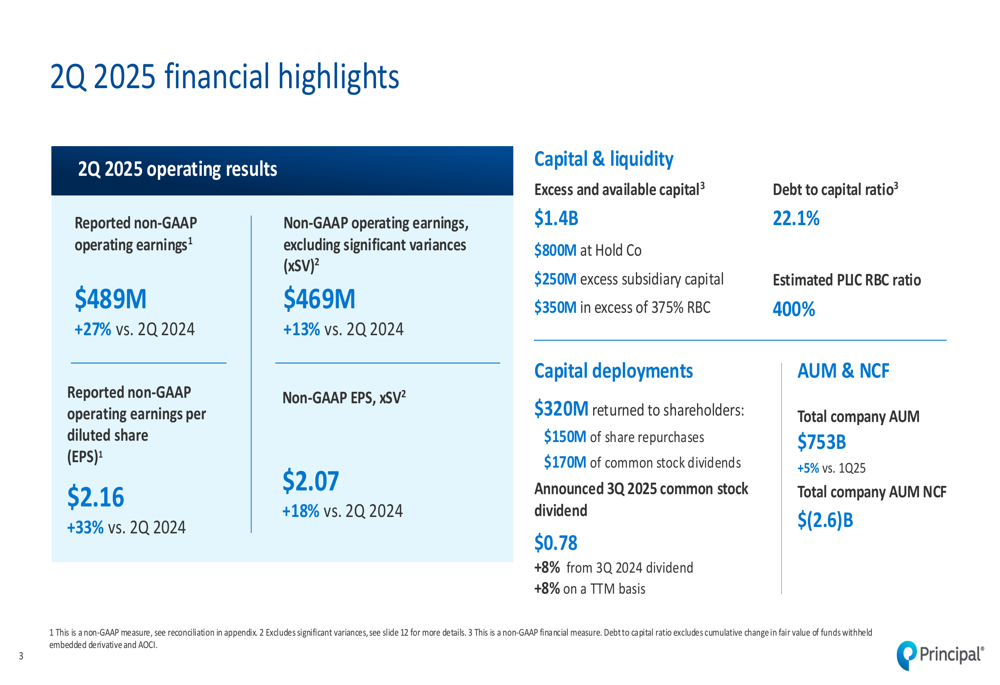

Principal reported non-GAAP operating earnings of $489 million for Q2 2025, representing a 27% increase compared to the same period in 2024. Excluding significant variances, operating earnings were $469 million, up 13% year-over-year. The company’s non-GAAP operating earnings per diluted share reached $2.16, a 33% increase from Q2 2024, while EPS excluding significant variances was $2.07, up 18%.

As shown in the following key takeaways slide, Principal is exceeding its long-term guidance across several metrics:

The company’s return on equity stood at 14.9%, within the target range of 14-16%, while trailing twelve-month free cash flow reached 92%, significantly above the 75-85% target range. These results highlight Principal’s ability to generate strong returns while maintaining financial flexibility.

Total (EPA:TTEF) assets under management (AUM) reached $753 billion, a 5% increase from the first quarter of 2025, though net cash flow was negative at $(2.6) billion. The company’s detailed financial results are presented in the following slide:

Segment Analysis

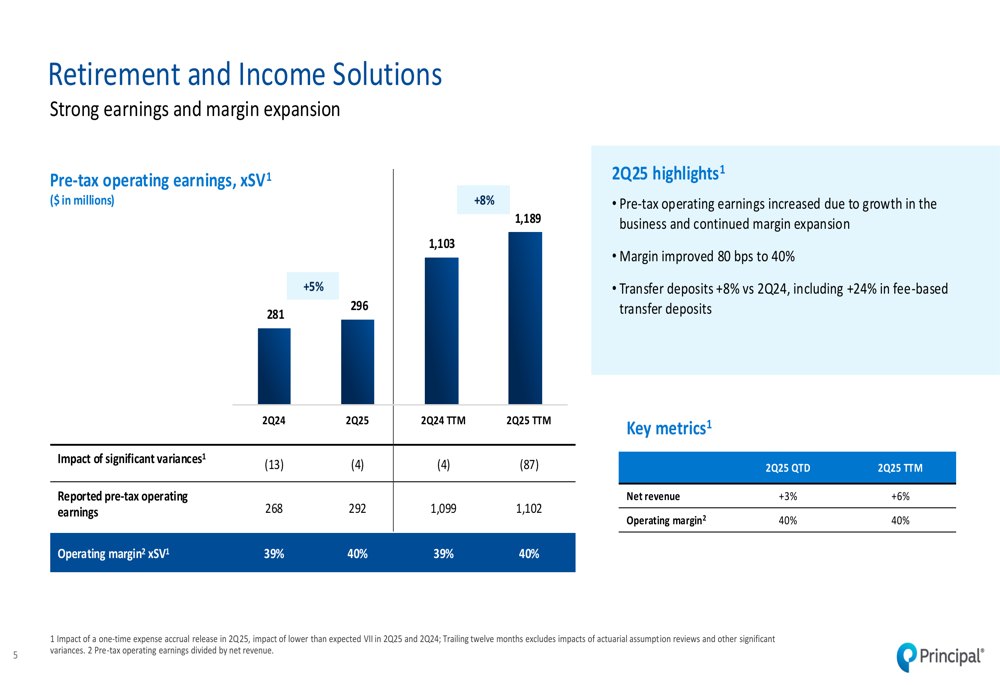

Principal’s Retirement and Income Solutions (RIS) segment showed solid growth, with pre-tax operating earnings of $296 million in Q2 2025, up from $281 million in Q2 2024. The segment’s operating margin improved by 80 basis points to 40%, driven by business growth and continued margin expansion. Transfer deposits increased 8% compared to Q2 2024, with fee-based transfer deposits up 24%.

The following slide details the RIS segment’s performance:

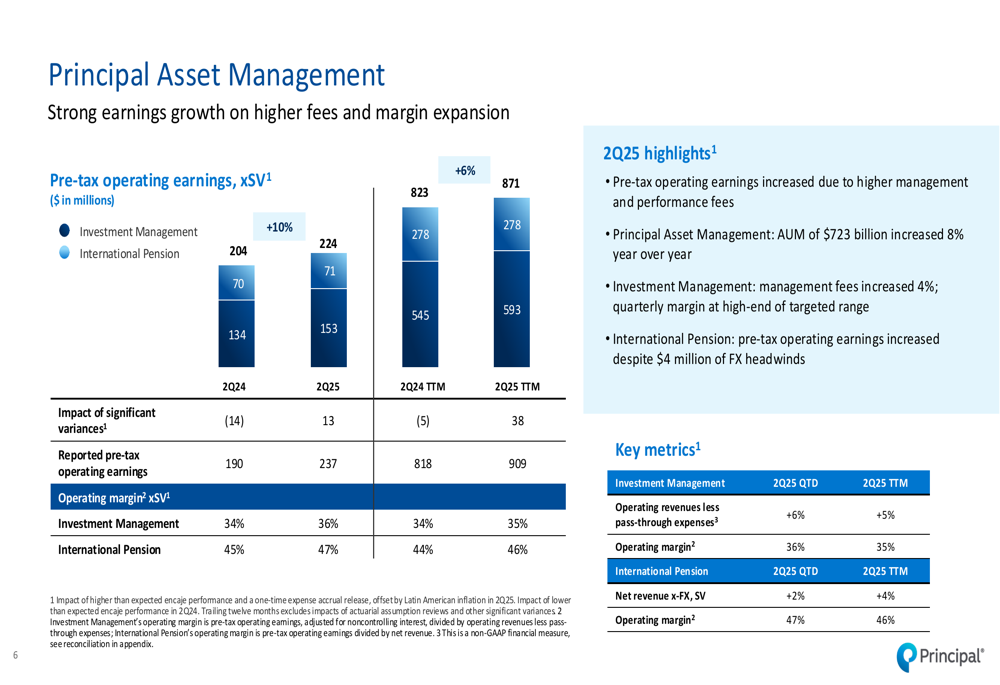

Principal Asset Management delivered strong results across both Investment Management and International Pension business lines. Investment Management pre-tax operating earnings reached $153 million, up from $134 million in Q2 2024, while International Pension contributed $71 million, slightly up from $70 million in the prior year. Investment Management’s operating margin improved significantly, expanding 250 basis points from the year-ago quarter to 36%.

The Asset Management segment’s performance is illustrated in this slide:

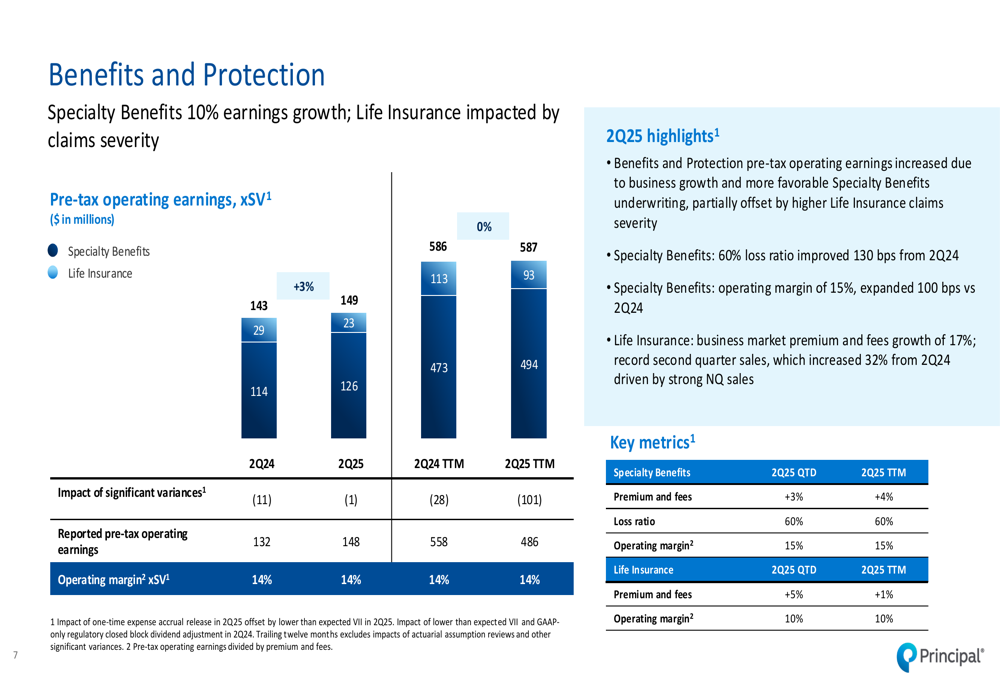

In the Benefits and Protection segment, Specialty Benefits showed particularly strong results with pre-tax operating earnings of $126 million, up from $114 million in Q2 2024. The loss ratio improved 130 basis points to 60%, and operating margin expanded 100 basis points to 15%. Life Insurance (NSE:LIFI) reported pre-tax operating earnings of $23 million, down from $29 million in Q2 2024, primarily due to higher claims severity, though business market premium and fees grew by 17%.

The following slide provides details on the Benefits and Protection segment:

Strategic Initiatives

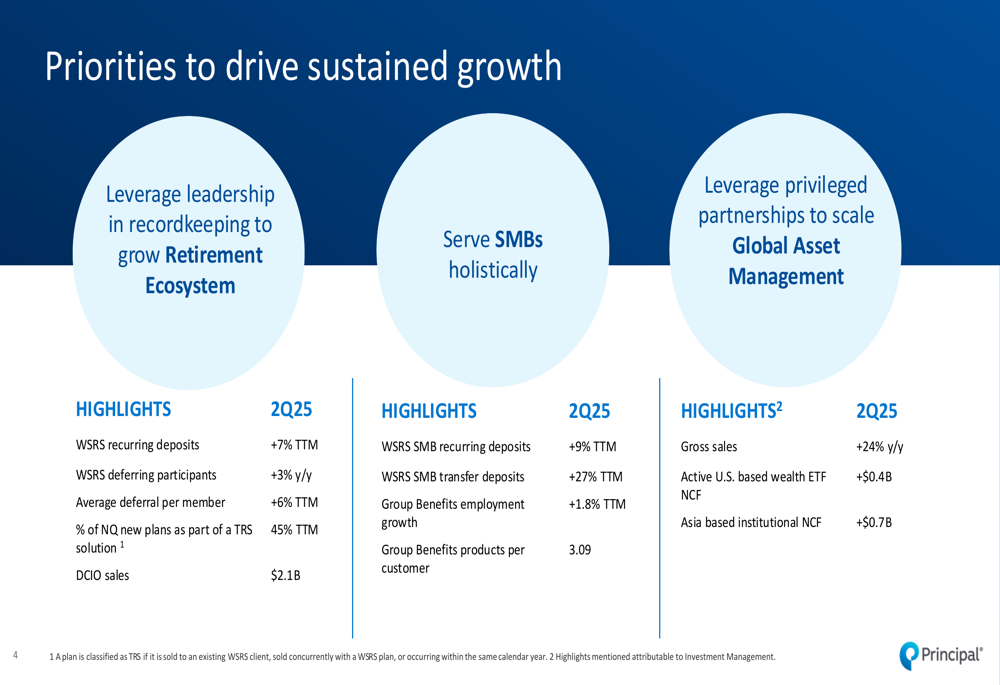

Principal outlined three key strategic priorities to drive sustained growth. The company is focusing on leveraging its leadership in recordkeeping to grow its Retirement Ecosystem, serving small and medium-sized businesses holistically, and scaling its Global Asset Management business through privileged partnerships.

The strategy is yielding results, with workplace savings and retirement solutions (WSRS) recurring deposits up 7% on a trailing twelve-month basis, and WSRS deferring participants increasing 3% year-over-year. In the SMB market, recurring deposits grew 9% and transfer deposits surged 27% on a trailing twelve-month basis.

The company’s strategic priorities and associated metrics are presented in this slide:

Capital Management

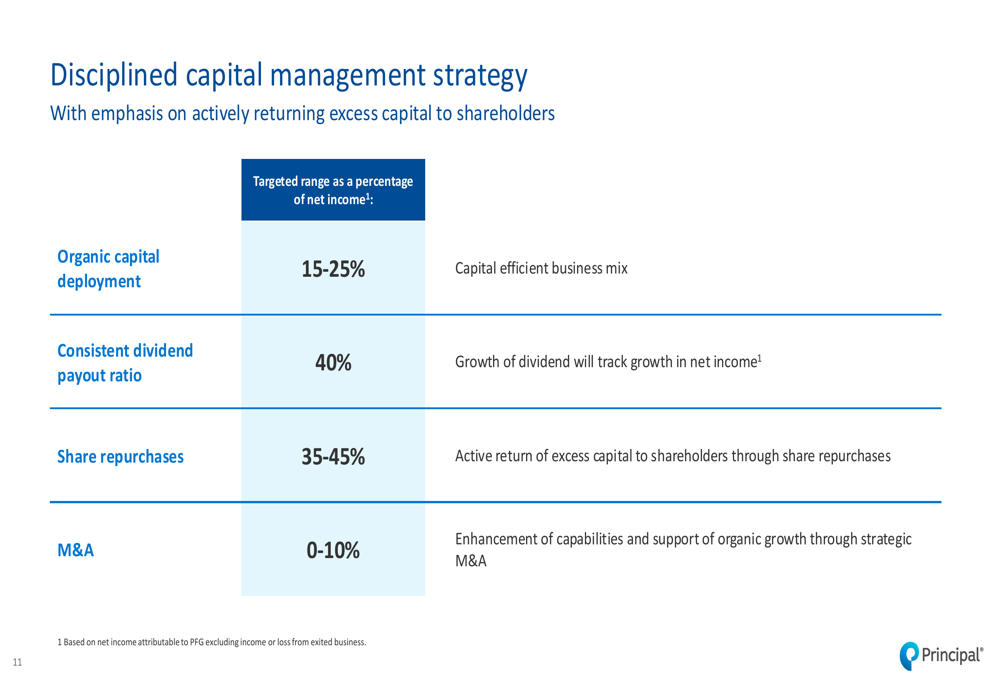

Principal maintained a strong capital position in Q2 2025, with $1.4 billion in excess and available capital. The company returned $320 million to shareholders during the quarter, consisting of $150 million in share repurchases and $170 million in common stock dividends. Additionally, Principal raised its Q3 2025 common stock dividend to $0.78 per share, an 8% increase from both Q3 2024 and the trailing twelve months.

The company’s disciplined capital management strategy focuses on actively returning excess capital to shareholders, with target ranges for various capital deployment activities as shown in the following slide:

Principal’s debt-to-capital ratio stood at 22.1%, and the estimated RBC ratio for Principal Life Insurance Company was 400%, both indicating a strong financial foundation.

Forward-Looking Statements

Principal provided insights into market sensitivities that could impact future earnings. The company disclosed estimated impacts of changes in equity markets, interest rates, foreign exchange rates, and alternative investment valuations on its annual non-GAAP pre-tax operating earnings.

While not providing specific guidance for Q3 or full-year 2025, the strong Q2 results suggest Principal is well-positioned to continue exceeding its long-term targets for EPS growth (9-12%), ROE (14-16%), and free cash flow (75-85% of net income).

This performance represents a significant improvement from Q1 2025, when the company missed analyst expectations. The robust Q2 results demonstrate Principal’s ability to navigate market volatility while delivering strong financial performance across most business segments.

As the company continues to execute on its strategic priorities and maintain disciplined capital management, investors will be watching to see if this momentum can be sustained through the second half of 2025, particularly given the ongoing market volatility and economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.