AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Priority Technology Holdings Inc (NASDAQ:PRTH) released its second quarter 2025 earnings presentation on August 7, showing continued momentum across its business segments. The payment technology provider reported 9% revenue growth and 13% adjusted gross profit growth, with particularly strong performance in its higher-margin B2B and Enterprise segments.

The company’s stock, which had fallen 12.42% following its Q1 2025 earnings despite beating EPS estimates, showed signs of recovery with premarket trading indicating a 6.62% increase to $7.25 following the Q2 results.

Quarterly Performance Highlights

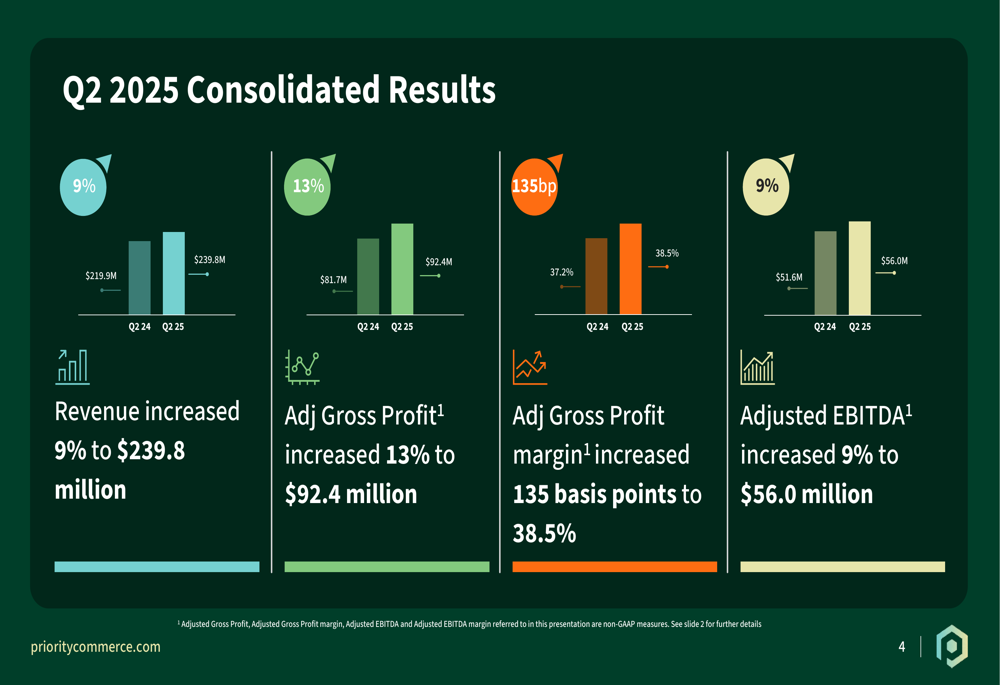

Priority Technology reported solid financial results for Q2 2025, with revenue increasing 9% year-over-year to $239.8 million compared to $219.9 million in Q2 2024. Adjusted gross profit grew at an even faster rate of 13% to reach $92.4 million, while adjusted EBITDA increased 9% to $56.0 million.

The company’s adjusted gross profit margin expanded by 135 basis points to 38.5%, up from 37.2% in the same period last year, reflecting a continued shift toward higher-margin business segments.

As shown in the following consolidated results chart:

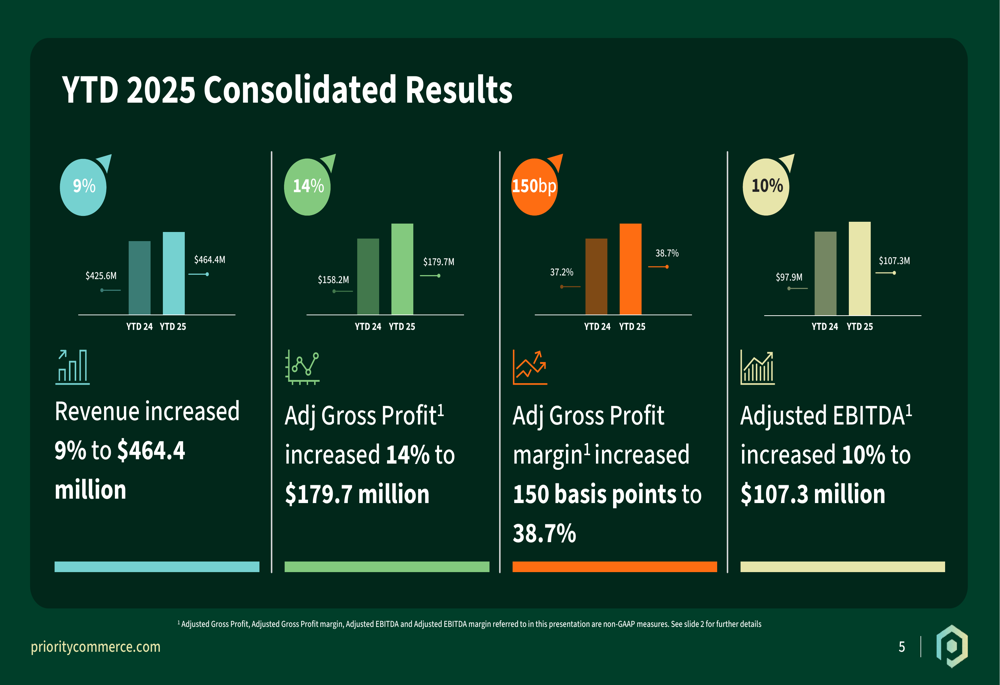

For the first half of 2025, Priority’s year-to-date performance maintained similar growth trajectories, with revenue up 9% to $464.4 million and adjusted gross profit increasing 14% to $179.7 million. The year-to-date adjusted gross profit margin expanded by 150 basis points to 38.7%.

Segment Analysis

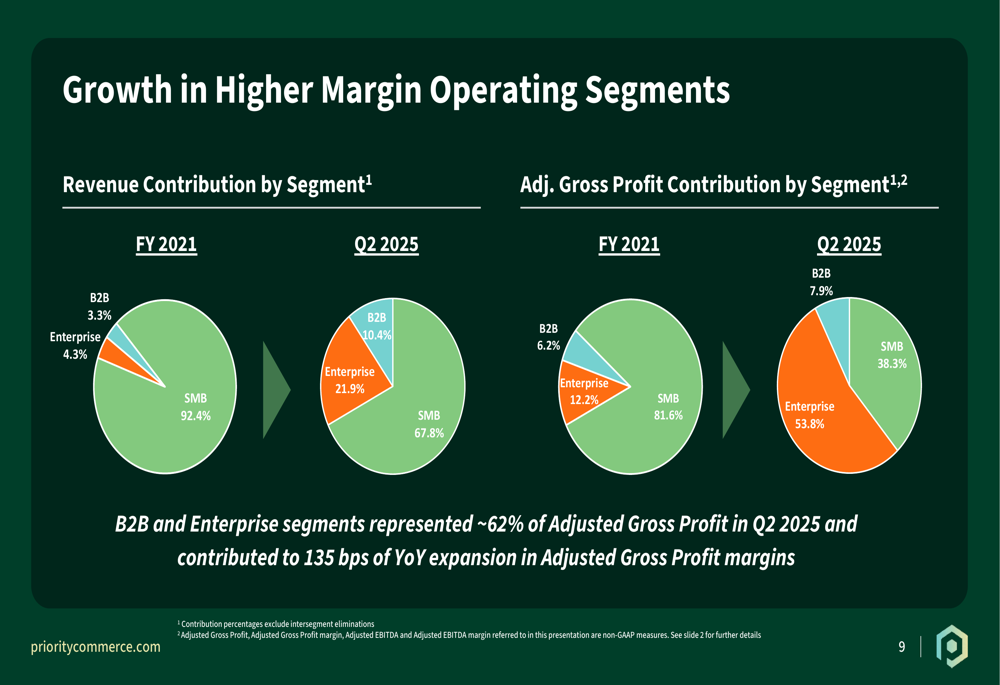

Priority’s business mix continues to evolve toward higher-margin segments. The company’s presentation highlighted that B2B and Enterprise segments now represent approximately 62% of adjusted gross profit, contributing to the overall margin expansion.

The following chart illustrates this shift in revenue and profit contribution by segment:

Breaking down performance by segment:

The SMB (Small and Medium Business) segment showed moderate revenue growth of 5% year-over-year to $163.2 million, though adjusted gross profit declined slightly by 1% to $35.4 million. The company noted that core SMB growth was stronger at 9.5%, with total card volumes increasing 2% to $18.7 billion.

The B2B segment delivered 14% revenue growth to $25.0 million, with a substantial 31% increase in adjusted gross profit to $7.3 million. This segment’s adjusted EBITDA grew by an impressive 146% year-over-year, demonstrating strong operating leverage. The growth was driven by a 22% increase in supplier-funded revenues and a 13% increase in buyer-funded revenues.

The Enterprise segment showed the strongest performance with 21% revenue growth to $52.7 million and a 23% increase in adjusted gross profit to $49.7 million. This segment maintains exceptionally high margins, with a 94.4% adjusted gross profit margin and 86.5% adjusted EBITDA margin. Key drivers included a 4% increase in CFTPay average monthly new enrollments to 58,000 and a 30% increase in average billed clients to 992,000.

Capital Structure Improvements

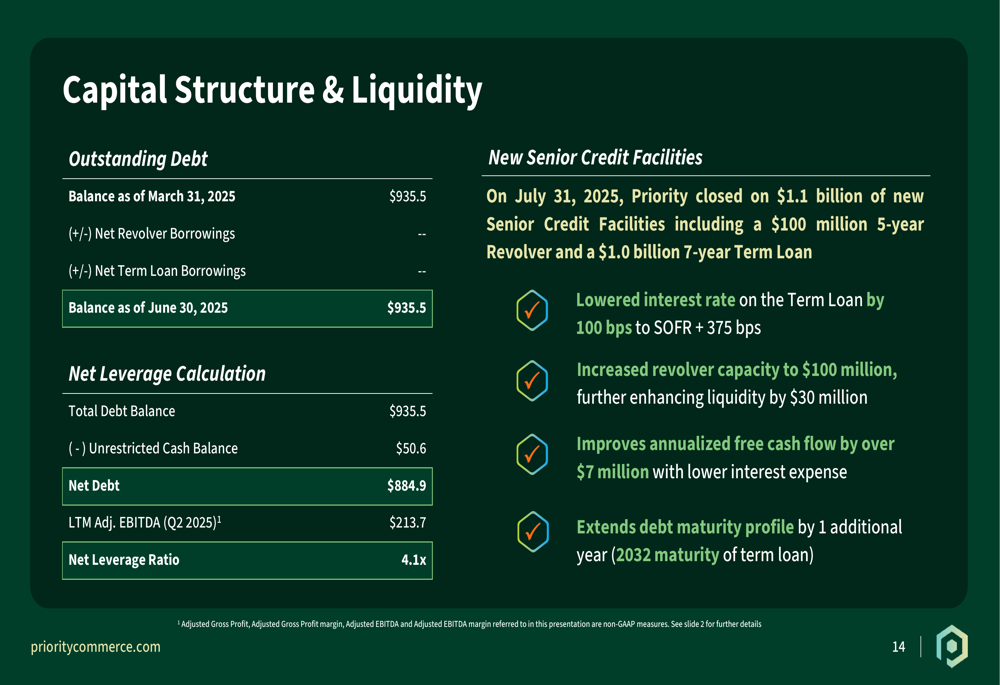

A significant development in the quarter was Priority’s refinancing of its debt. On July 31, 2025, the company closed on $1.1 billion of new senior credit facilities, including a $100 million five-year revolver and a $1.0 billion seven-year term loan.

The refinancing provides several benefits, as illustrated in the following capital structure overview:

The new credit facilities lowered the interest rate on the term loan by 100 basis points to SOFR + 375 bps, increased revolver capacity by $30 million, improved annualized free cash flow by over $7 million through lower interest expenses, and extended the debt maturity profile by an additional year to 2032.

As of June 30, 2025, Priority reported a net leverage ratio of 4.1x, based on total debt of $935.5 million, unrestricted cash of $50.6 million, and last twelve months adjusted EBITDA of $213.7 million.

Forward-Looking Statements

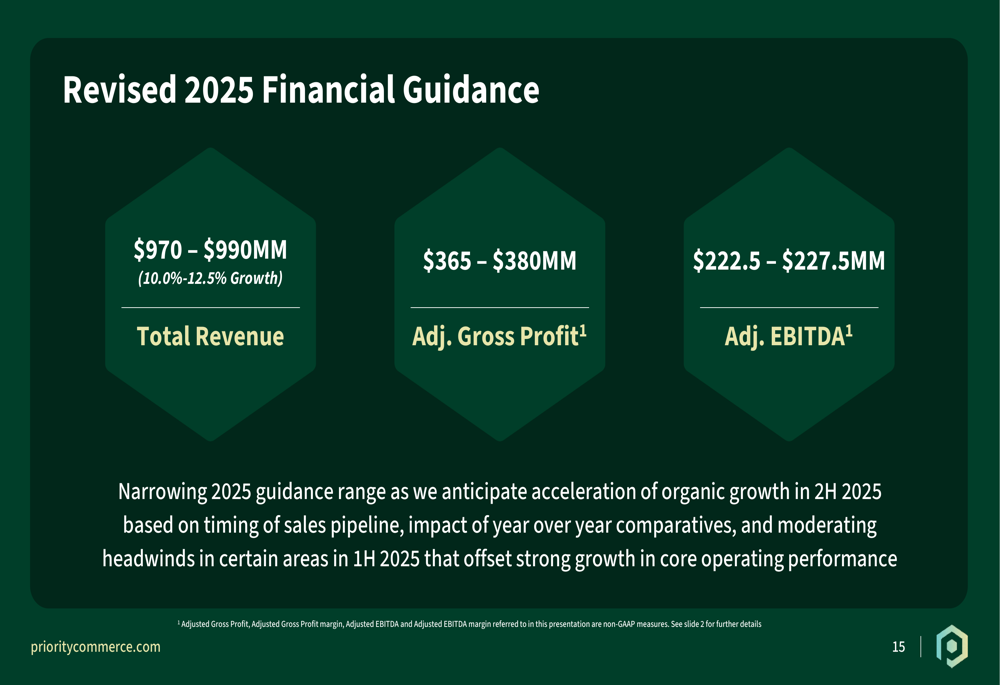

Priority Technology revised its full-year 2025 guidance, narrowing the ranges as it anticipates accelerated growth in the second half of the year:

The updated guidance projects total revenue of $970-$990 million, representing 10.0%-12.5% growth, with adjusted gross profit of $365-$380 million and adjusted EBITDA of $222.5-$227.5 million.

This guidance aligns with the company’s year-to-date performance, with $464 million in revenue and $107 million in adjusted EBITDA already achieved in the first half of 2025.

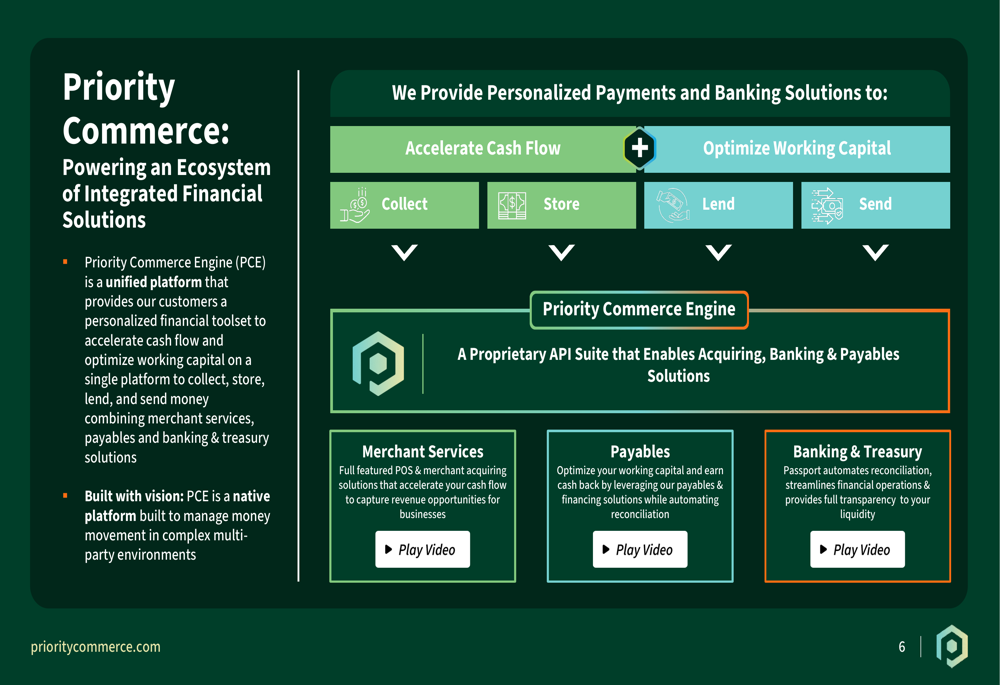

Priority’s commerce ecosystem continues to expand across multiple industry sectors, including consumer finance, sports and entertainment, payroll and benefits, property tech, and construction. The company’s integrated platform provides solutions for collecting, storing, lending, and sending money, with revenue streams including interchange on card volume, monthly platform SaaS fees, payment processing fees, and float income on account balances.

With 1.6 million customer accounts, $1.4 billion in account balances, and $140 billion in total payments volume, Priority Technology appears well-positioned to continue its growth trajectory through the remainder of 2025, particularly if the anticipated acceleration in the second half materializes as projected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.