Asahi shares mark weekly slide after cyberattack halts production

Progress Software Corporation (NASDAQ:PRGS) reported strong third-quarter results that exceeded guidance across key metrics, according to the company’s Q3 2025 financial presentation released on September 29, 2025. The enterprise software provider posted significant revenue growth and raised its full-year outlook, driving its stock price up 1.67% in regular trading and an additional 2.31% in after-market activity.

Quarterly Performance Highlights

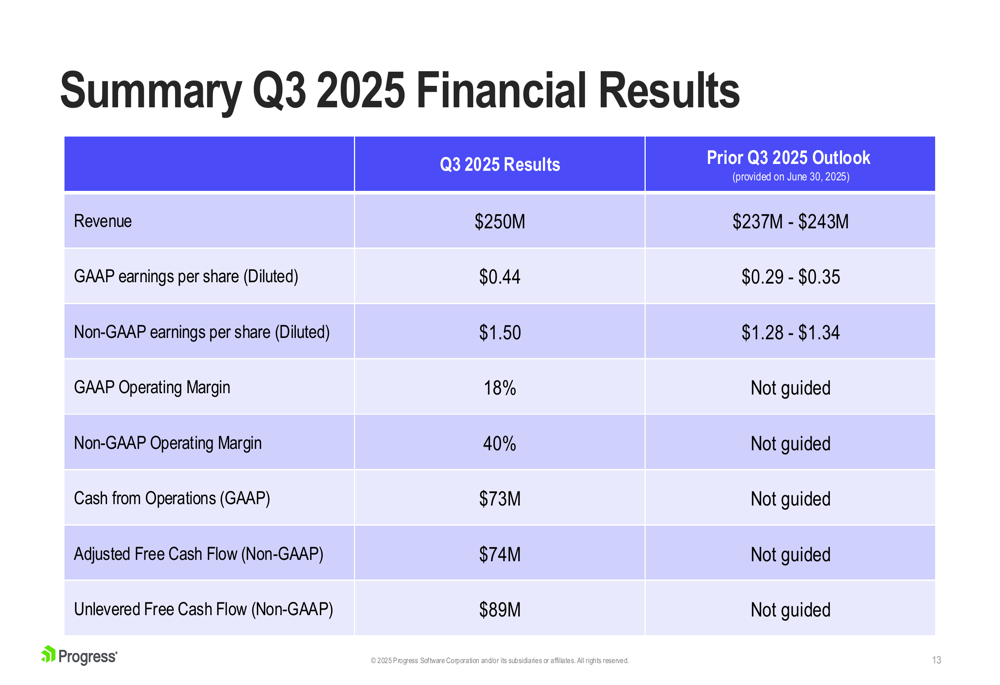

Progress delivered revenue of $250 million in Q3 2025, surpassing its prior guidance range of $237-$243 million and representing a 38% year-over-year increase in constant currency. Non-GAAP earnings per share reached $1.50, significantly exceeding the high end of the company’s previous guidance of $1.28-$1.34.

The company maintained its strong profitability profile with a non-GAAP operating margin of 40%, while generating $73 million in cash from operations, $74 million in adjusted free cash flow, and $89 million in unlevered free cash flow during the quarter.

As shown in the following summary of Q3 2025 financial results compared to prior guidance:

Revenue and ARR Growth Analysis

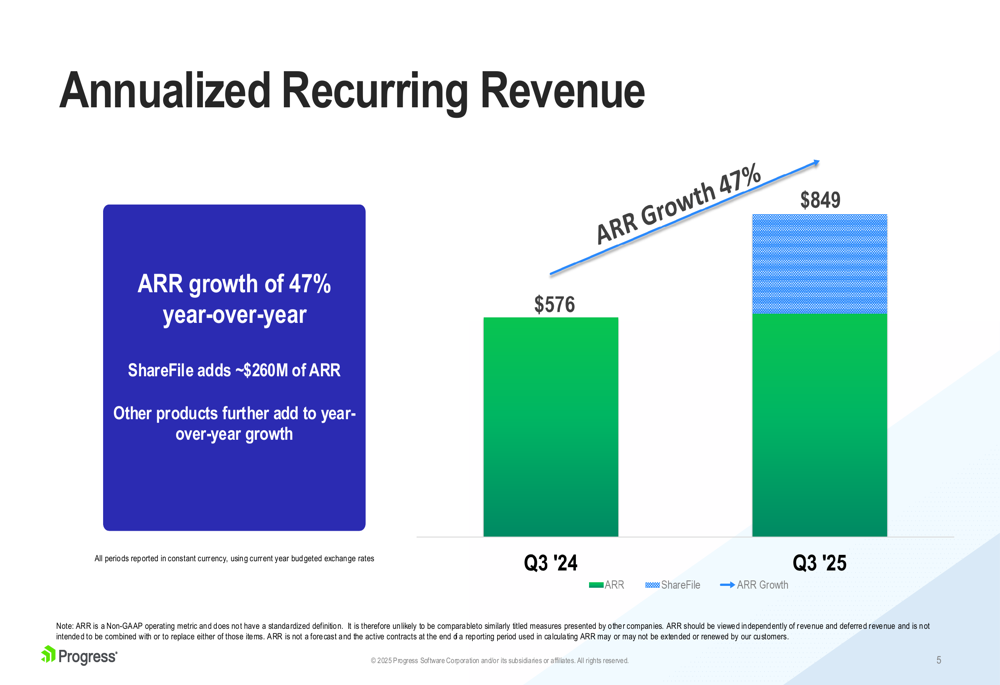

Annualized recurring revenue (ARR) grew to $849 million, up 47% year-over-year in constant currency. This substantial increase was largely driven by the ShareFile acquisition, which added approximately $260 million to ARR. On a pro-forma basis, including ShareFile in all periods, ARR grew 3% year-over-year.

The following chart illustrates the significant ARR growth from Q3 2024 to Q3 2025:

Progress has maintained a consistent Net Retention Rate (NRR) of 100%, indicating stable customer relationships. The company’s ARR has shown steady growth over several quarters, as demonstrated in this trend chart:

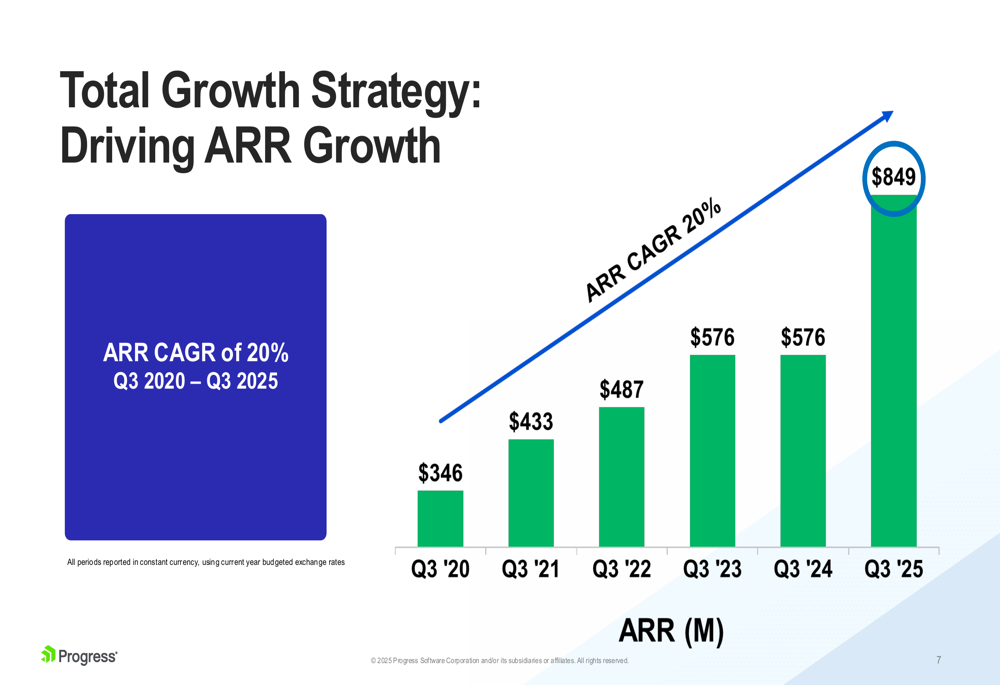

The company’s long-term growth trajectory remains impressive, with an ARR CAGR of 20% from Q3 2020 to Q3 2025:

Similarly, revenue has grown at a 15% CAGR from fiscal year 2021 to the midpoint of 2025 guidance:

Updated Guidance and Outlook

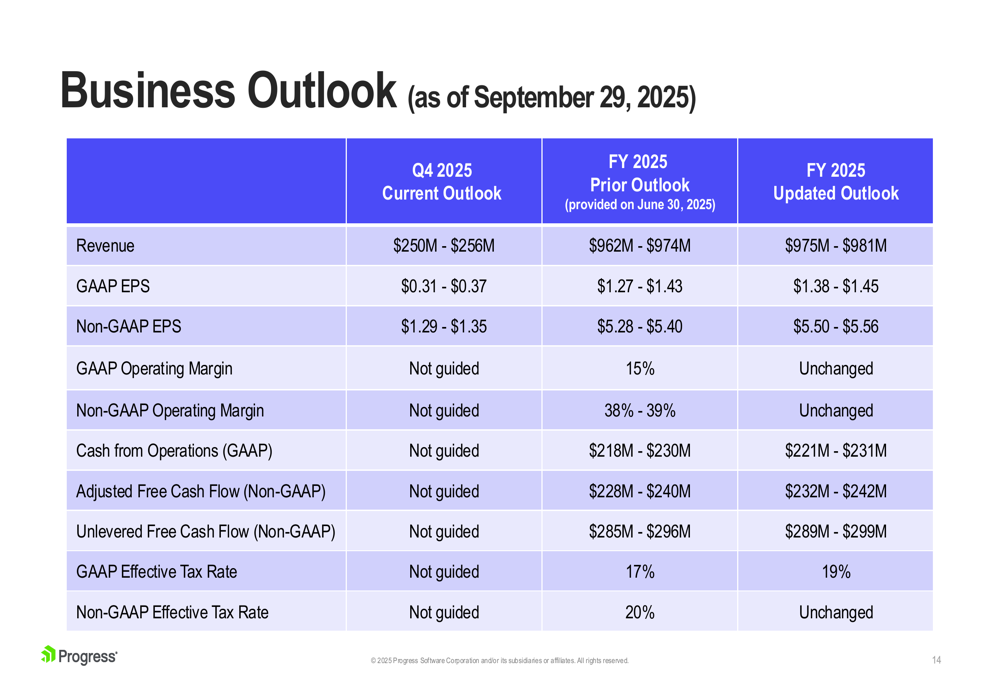

Based on its strong Q3 performance, Progress raised its full-year 2025 guidance. The company now expects:

- Revenue of $975-$981 million, up from previous guidance of $962-$974 million

- Non-GAAP EPS of $5.50-$5.56, increased from $5.28-$5.40

- Cash from operations of $221-$231 million, up from $218-$230 million

- Adjusted free cash flow of $232-$242 million, improved from $228-$240 million

For Q4 2025, Progress projects revenue of $250-$256 million and non-GAAP EPS of $1.29-$1.35.

The detailed business outlook is presented in the following table:

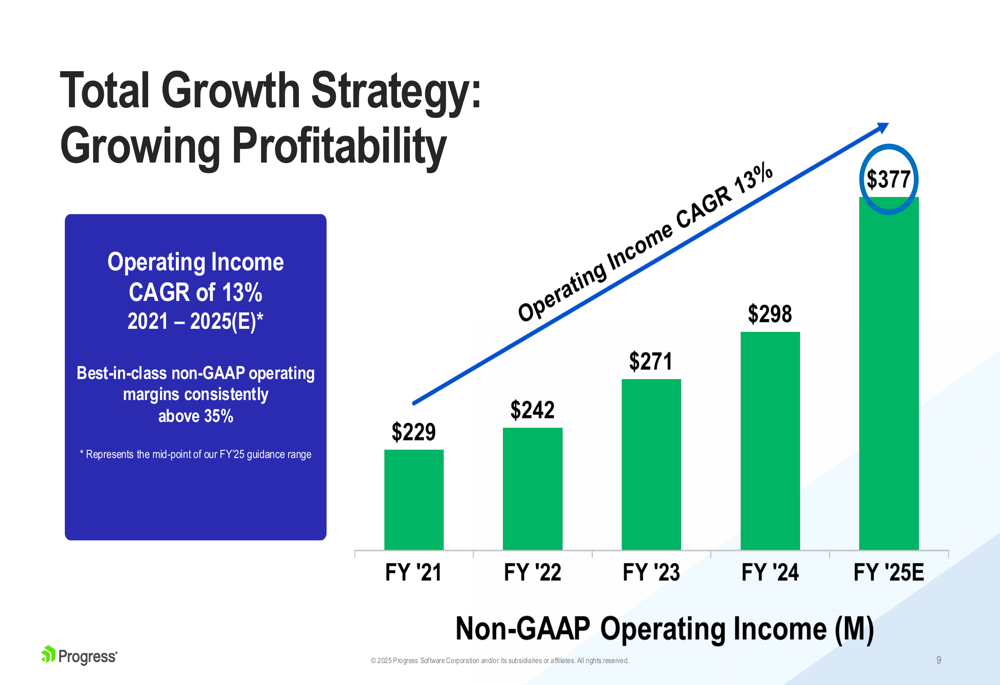

Profitability and Cash Flow Performance

Progress continues to demonstrate strong profitability metrics, with best-in-class non-GAAP operating margins consistently above 35%. The company’s operating income has grown at a 13% CAGR from 2021 to the midpoint of 2025 guidance:

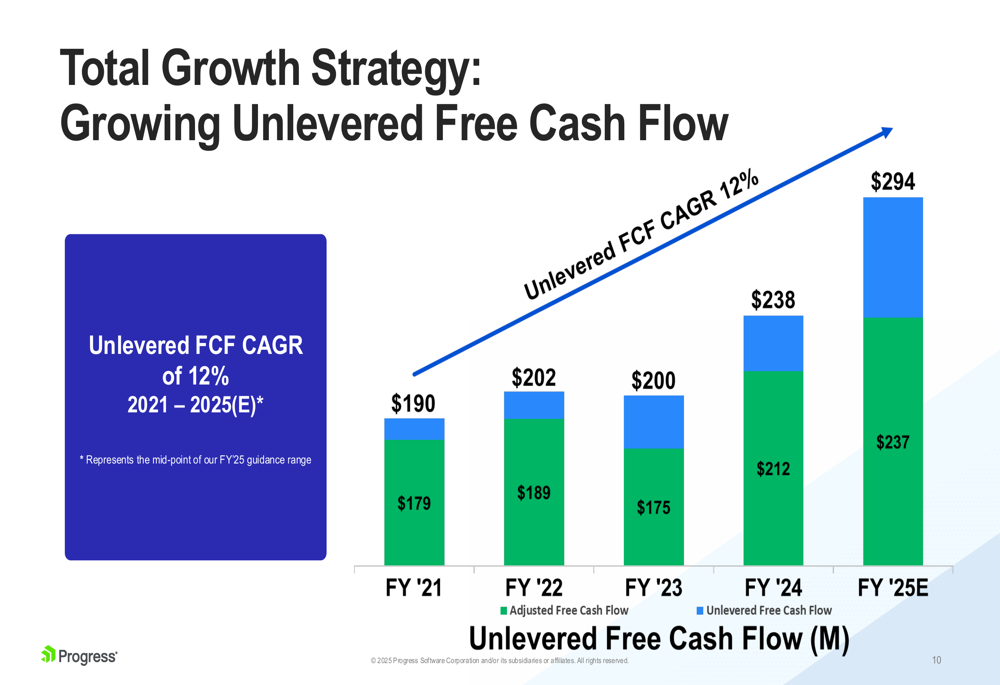

This profitability translates into robust cash generation, with unlevered free cash flow growing at a 12% CAGR from 2021 to 2025(E):

Capital Allocation and M&A Strategy

Progress outlined its capital allocation strategy, which prioritizes accretive M&A opportunities while using its significant free cash flow to reduce debt and prepare for future acquisitions. The company repaid $40 million in debt during Q3 2025 and $110 million year-to-date, with plans to repay approximately $160 million in total for fiscal year 2025.

Additionally, Progress repurchased $15 million of shares in Q3 2025 and $65 million year-to-date to offset dilution from equity programs.

The company’s M&A framework focuses on opportunities in infrastructure software and all aspects of the development lifecycle, targeting companies with revenues representing 10-25% of Progress’s current revenues, high recurring revenue, strong customer retention, and returns on invested capital exceeding weighted average cost of capital.

Forward-Looking Statements

Progress Software’s Q3 2025 results demonstrate the company’s ability to execute on its growth strategy through both organic initiatives and strategic acquisitions. The integration of ShareFile has significantly boosted ARR, while consistent customer retention rates provide a stable foundation for future growth.

With raised guidance for the full year and strong cash generation supporting its capital allocation strategy, Progress appears well-positioned to continue its growth trajectory. The company’s focus on maintaining high operating margins while pursuing strategic acquisitions suggests a balanced approach to delivering shareholder value through both profitability and expansion.

Investors will likely be watching how effectively Progress can maintain its growth momentum while integrating acquisitions and navigating the competitive landscape in enterprise software.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.