Bitcoin price today: tumbles below $90k as Fed cut doubts spark risk-off mood

Introduction & Market Context

Protector Forsikring ASA (OB:PROT) presented its Q1 2025 interim results on April 24, 2025, revealing strong performance across key metrics despite ongoing financial market turbulence. The Norwegian insurer, which positions itself as "The Challenger" in the industry, reported significant premium growth and improved underwriting results while maintaining a robust capital position.

The company’s stock closed at 336.5 NOK on April 23, 2025, representing a 2.67% increase on the day before the presentation, suggesting positive market sentiment ahead of the results announcement.

Quarterly Performance Highlights

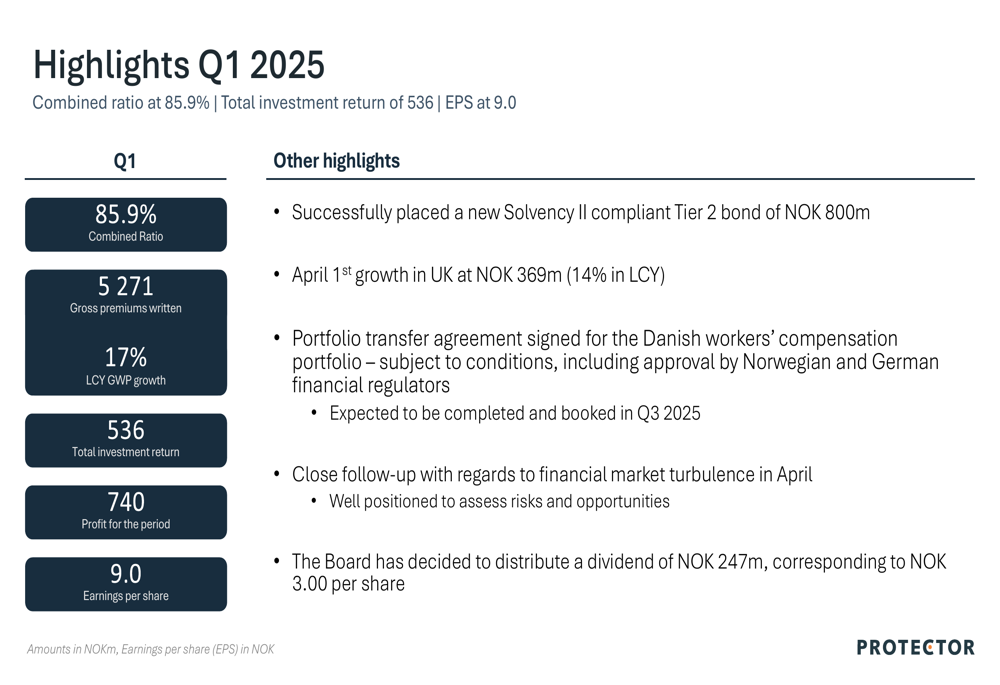

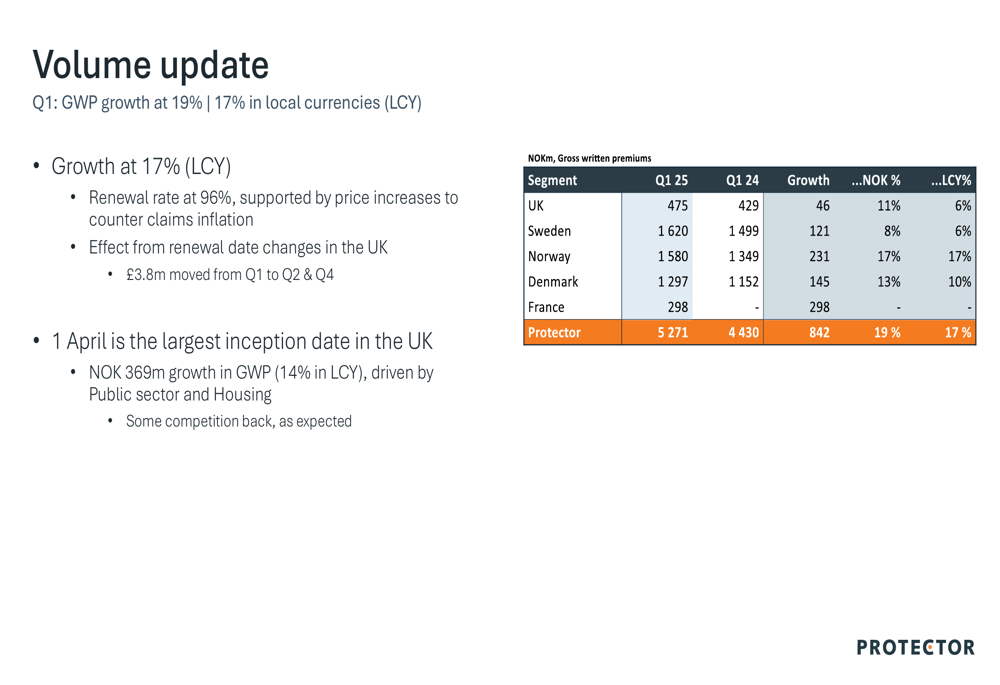

Protector Forsikring delivered impressive financial results for Q1 2025, with a combined ratio of 85.9%, total investment return of 536 million NOK, and earnings per share (EPS) of 9.0 NOK. The company achieved 19% growth in gross written premiums (GWP), or 17% in local currencies, supported by a strong renewal rate of 96%.

As shown in the following chart of quarterly highlights:

The company’s growth strategy continues to yield results across all markets, with Norway showing the strongest performance at 17% growth in local currency. Notably, Protector has successfully expanded into France, which contributed 298 million NOK to the group’s premium volume in Q1.

The following table illustrates the premium growth across all markets:

Detailed Financial Analysis

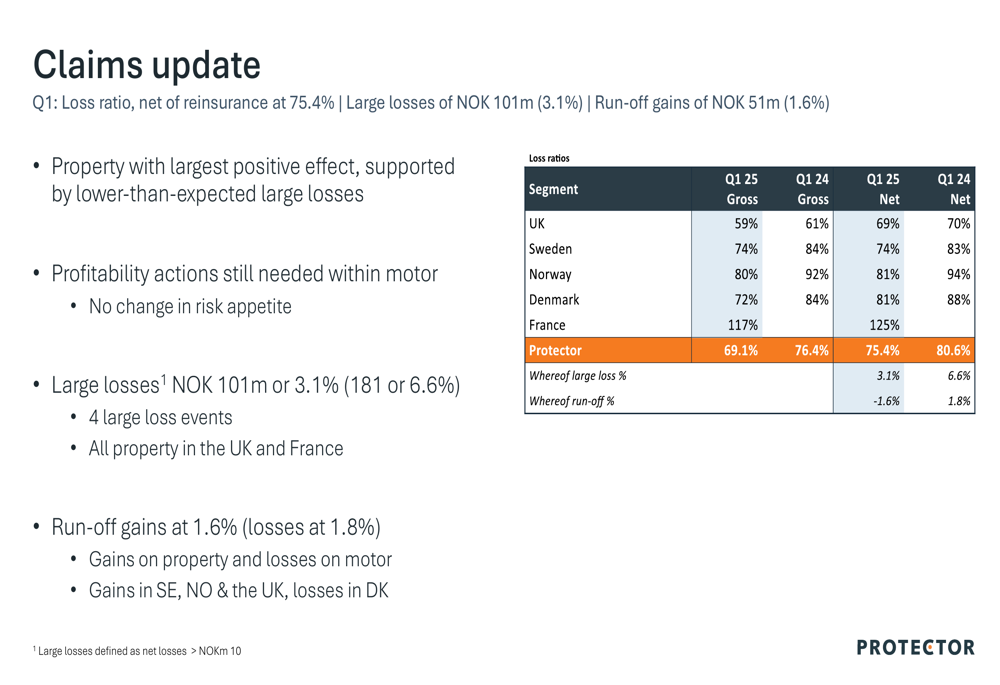

Protector’s underwriting performance improved significantly compared to the same period last year, with the loss ratio, net of reinsurance, decreasing to 75.4% from 80.6% in Q1 2024. Large losses amounted to 101 million NOK (3.1% of premiums), down from 181 million NOK (6.6%) in the previous year. The company also reported run-off gains of 51 million NOK (1.6%), compared to losses of 1.8% in Q1 2024.

The property segment was the main contributor to the positive performance, benefiting from lower-than-expected large losses. However, the company acknowledged that further profitability actions are needed within the motor segment.

The following table provides a detailed breakdown of loss ratios by country:

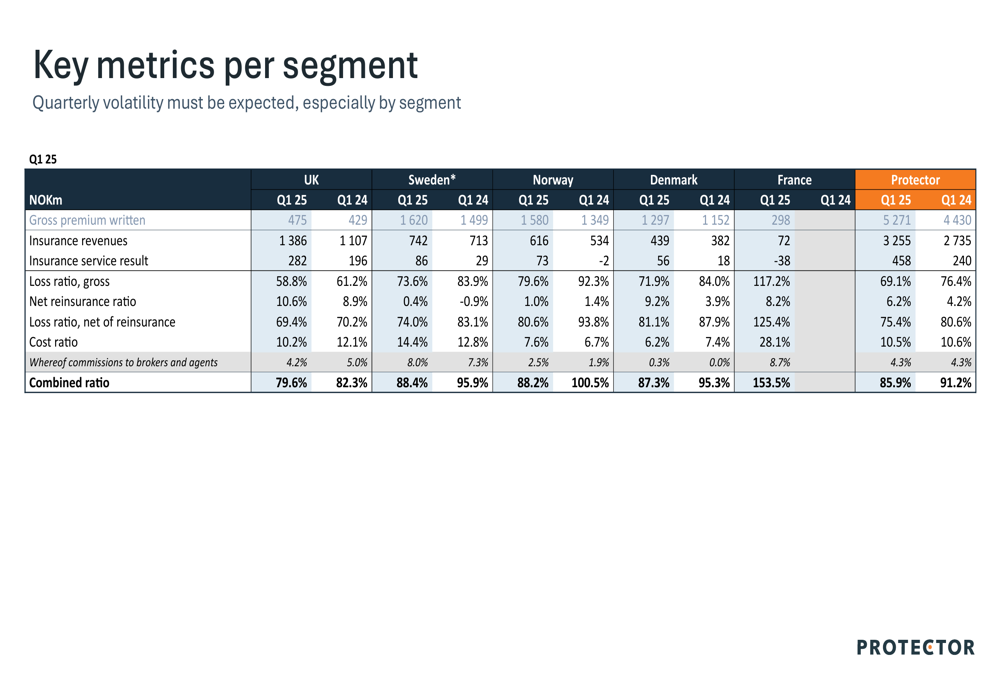

Looking at key metrics across segments, the UK and Sweden delivered the strongest performance with combined ratios of 82.9% and 83.3% respectively. France, as a new market entry, showed a higher combined ratio of 130.1%, reflecting the initial challenges of market penetration.

The comprehensive segment performance is detailed in this table:

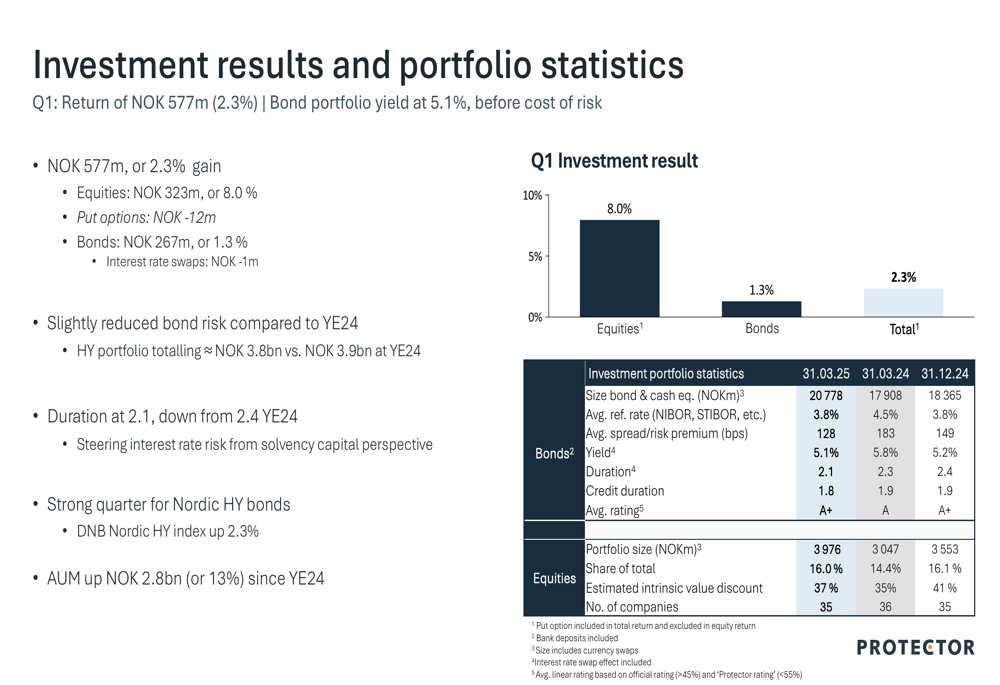

On the investment side, Protector reported a return of 577 million NOK (2.3%) for Q1 2025, with the bond portfolio yielding 5.1% before cost of risk. The investment portfolio statistics reveal a well-diversified approach with careful management of duration and credit exposure.

The following chart details the investment results and portfolio statistics:

Strategic Initiatives

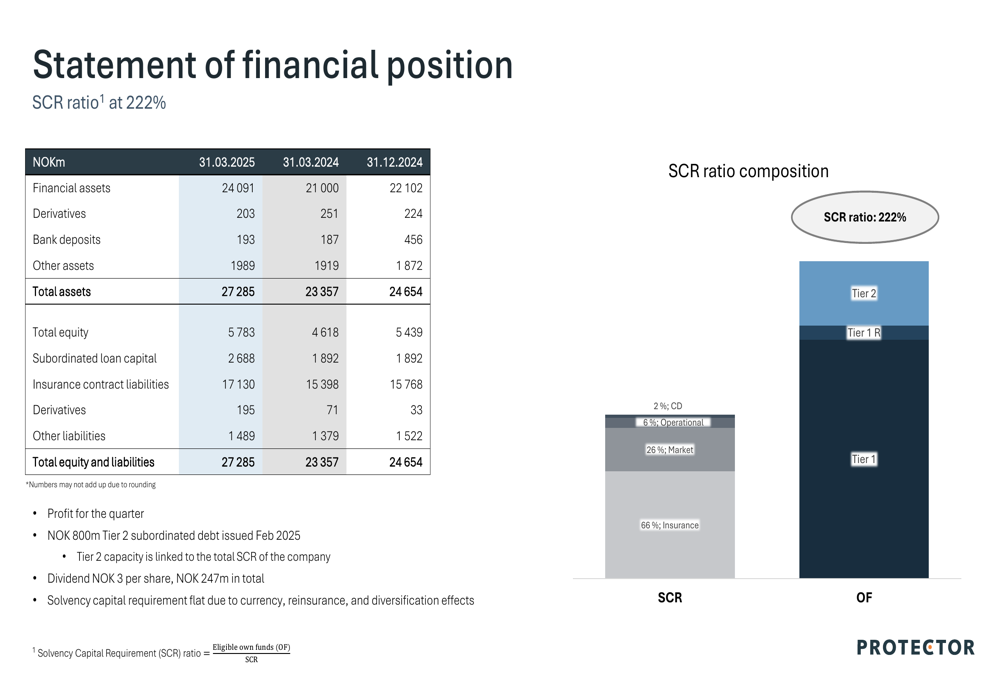

Protector’s financial strength is evidenced by its solid capital position, with a Solvency Capital Requirement (SCR) ratio of 222%. This strong position has enabled the board to declare a dividend of 247 million NOK, equivalent to 3.00 NOK per share, to be paid on May 9, 2025.

The company’s balance sheet and SCR ratio composition are illustrated here:

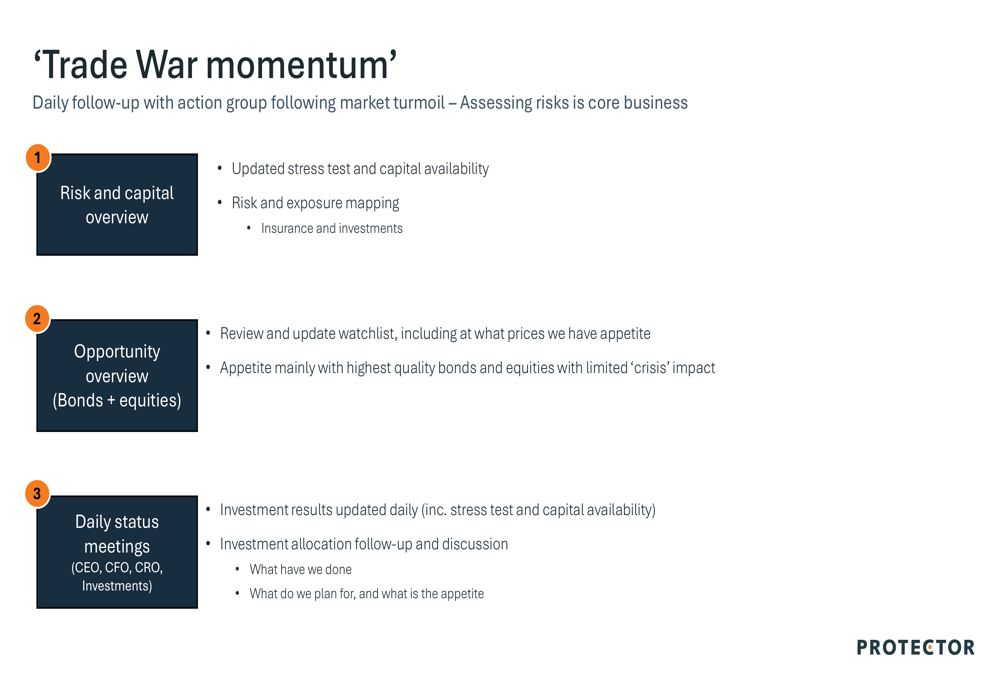

In response to financial market turbulence in April, Protector has implemented a structured approach focused on daily risk assessment and capital management. This includes updated stress testing, risk mapping, and daily status meetings involving key executives.

The company’s action plan for navigating market volatility is outlined below:

Protector also successfully placed a new Solvency II compliant Tier 2 bond of 800 million NOK during the quarter, further strengthening its capital structure. Additionally, the company signed a portfolio transfer agreement for the Danish workers’ compensation portfolio, which is expected to be completed and booked in Q3 2025.

Forward-Looking Statements

Protector maintains its strategic focus as "The Challenger" in the insurance market, emphasizing unique relationships, best-in-class decision-making, and cost-effective solutions. The company’s main targets include cost and quality leadership, profitable growth, and becoming a top 3 player in its chosen markets.

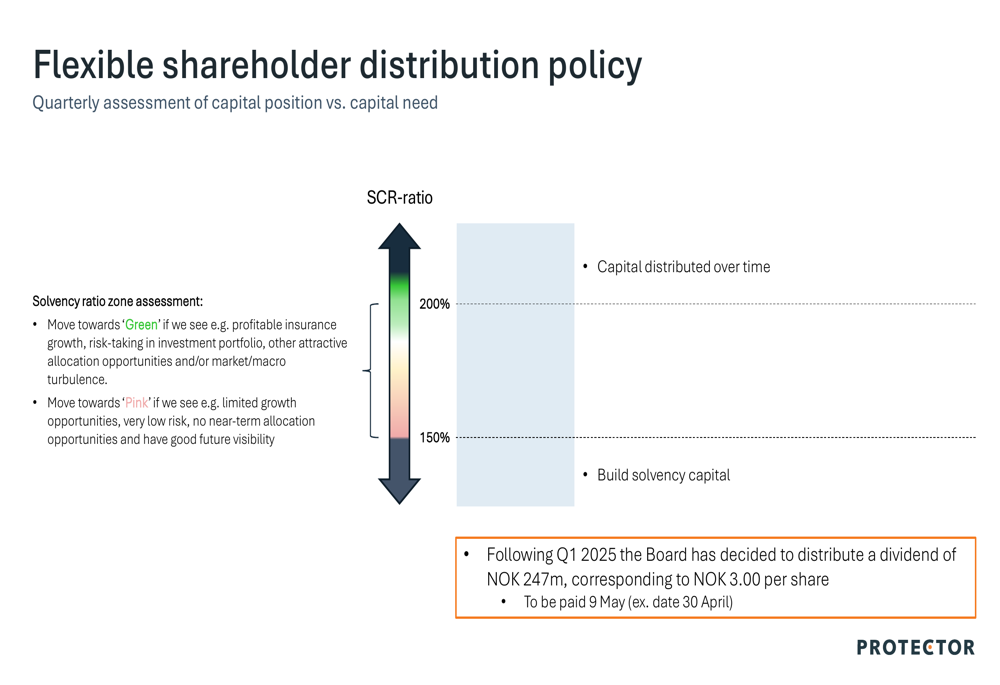

The company has implemented a flexible shareholder distribution policy based on its solvency position, with different approaches for "Green" zones (supporting profitable insurance growth and investment risk-taking) and "Pink" zones (limited growth opportunities and very low risk).

This distribution policy is illustrated in the following slide:

With the April 1st renewal date being the largest inception date in the UK, Protector reported additional growth of 369 million NOK (14% in local currency) in this market. This suggests continued momentum into Q2 2025, although the company remains vigilant regarding financial market turbulence.

The Q1 2025 results demonstrate Protector’s ability to execute its growth strategy while maintaining underwriting discipline and effective capital management, positioning the company well for the remainder of 2025 despite potential market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.