Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Protector Forsikring ASA (OB:PROT) presented its Q2 2025 interim results on July 11, 2025, revealing substantial improvements across key performance metrics. The Norwegian insurer, which positions itself as "The Challenger" in the market, reported a significant profit increase and continued premium growth across its European operations.

The company’s stock has shown strong momentum in recent months, rising from 357.5 after Q1 results to the current 462, representing a 29% increase. This performance reflects investor confidence in Protector’s strategic direction and financial strength.

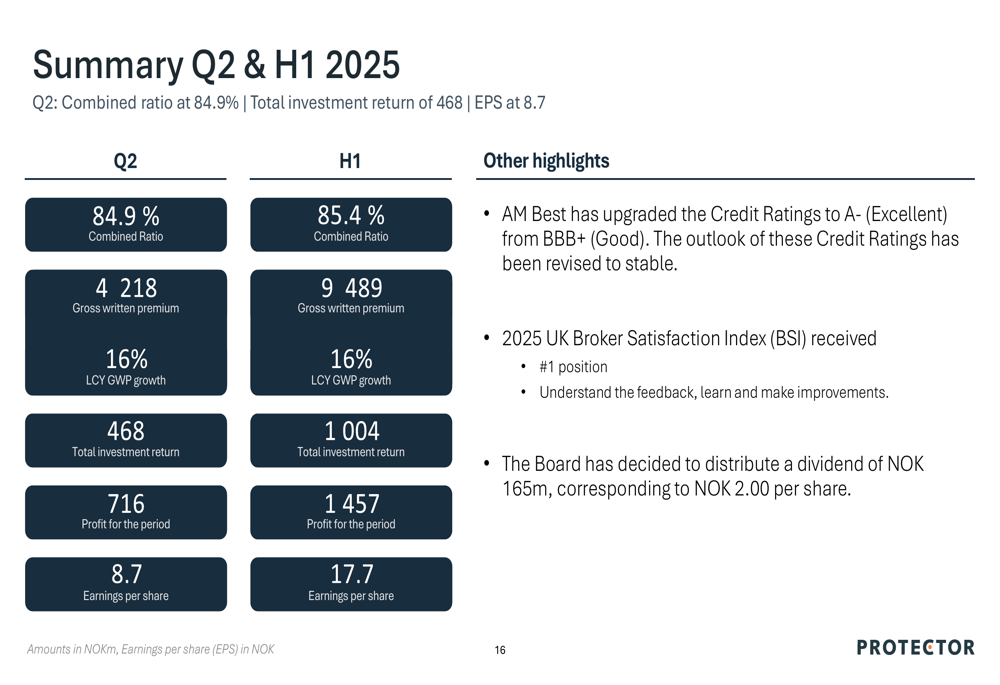

Quarterly Performance Highlights

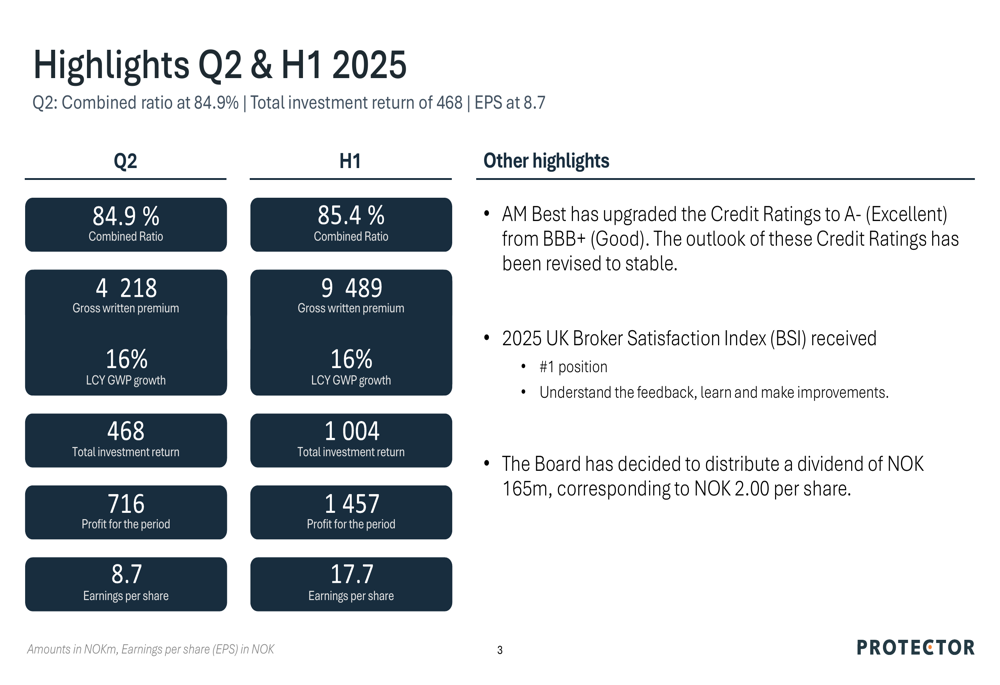

Protector reported a Q2 2025 profit of NOK 716 million, nearly tripling from NOK 254 million in the same period last year. Earnings per share reached NOK 8.7, compared to NOK 3.1 in Q2 2024, while the combined ratio improved to 84.9% from higher levels in previous quarters.

As shown in the following comprehensive overview of the company’s Q2 and H1 2025 performance:

For the first half of 2025, Protector achieved a profit of NOK 1,457 million with earnings per share of NOK 17.7. The company’s board approved a dividend distribution of NOK 165 million, corresponding to NOK 2.00 per share.

Other notable achievements include AM Best upgrading Protector’s credit rating to A- (Excellent) and the company securing the #1 position in the 2025 UK Broker Satisfaction Index with a score of 84, up from 80 in 2024.

Premium Growth and Market Expansion

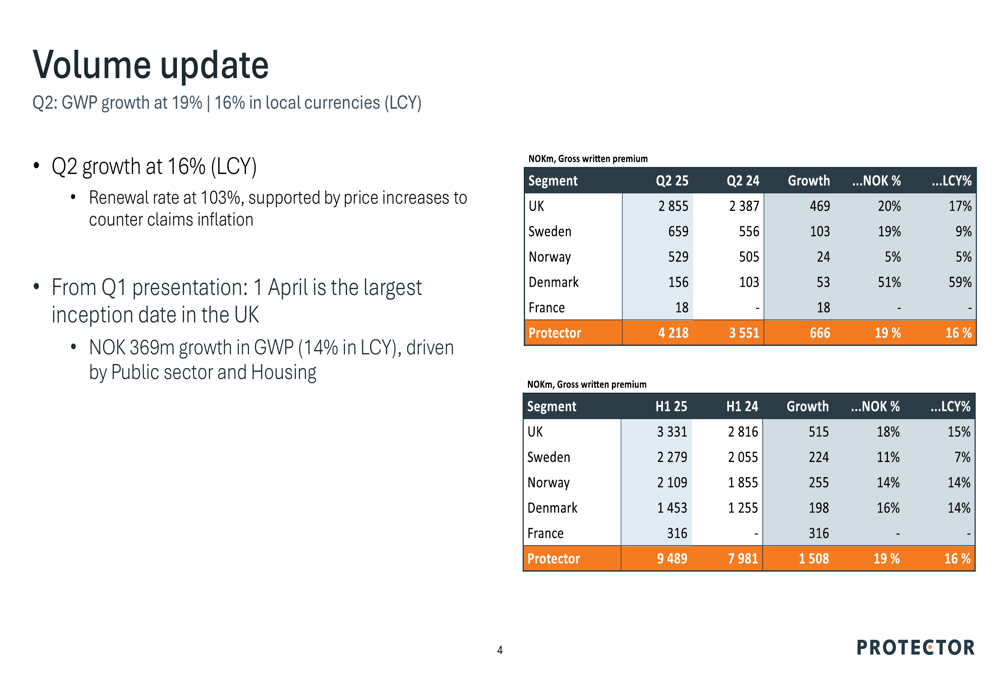

Protector continued its strong growth trajectory with gross written premiums (GWP) increasing by 19% (16% in local currencies) to NOK 4,218 million in Q2 2025. This growth was supported by a renewal rate of 103%, reflecting the company’s ability to implement price increases to counter claims inflation.

The detailed breakdown of premium growth across markets demonstrates consistent performance:

The UK market, where April 1st represents the largest inception date according to the company, showed particularly strong results. Growth in GWP of NOK 369 million (14% in local currency) was primarily driven by the Public sector and Housing segments.

For the first half of 2025, total GWP reached NOK 9,489 million, representing a 19% increase (16% in local currencies) compared to H1 2024.

Claims Performance and Profitability

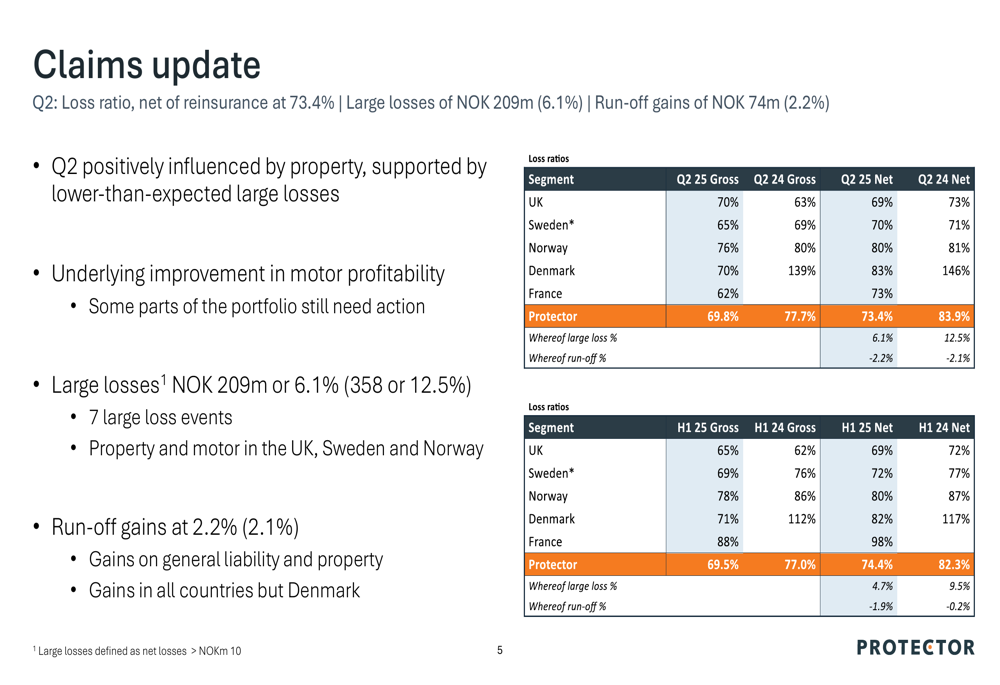

Protector’s improved profitability was largely driven by better claims performance. The Q2 2025 loss ratio, net of reinsurance, improved to 73.4% from 83.9% in Q2 2024. This improvement was positively influenced by property insurance results, supported by lower-than-expected large losses.

The following breakdown shows the claims performance across different markets:

Large losses in Q2 2025 amounted to NOK 209 million (6.1% of premiums), while run-off gains contributed NOK 74 million (2.2%). The company’s segment-by-segment performance reveals improvements across most markets:

The combined ratio of 84.9% for Q2 2025 represents a significant improvement from previous periods and demonstrates Protector’s effective underwriting and pricing strategies.

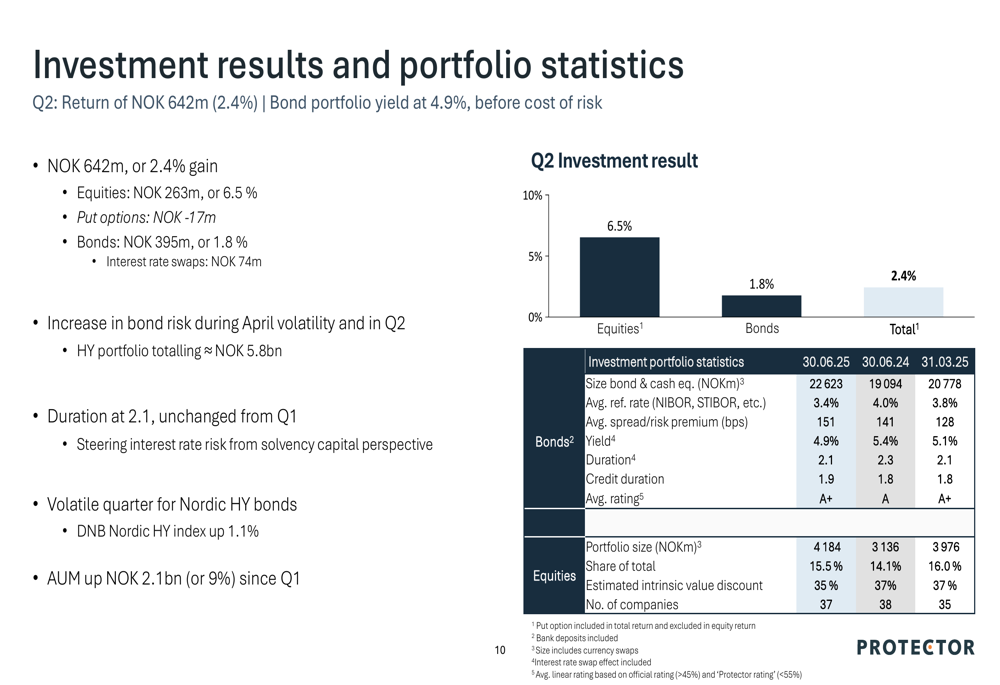

Investment Results and Capital Position

Protector reported strong investment returns for Q2 2025, with a total return of NOK 642 million (2.4%). The company’s investment portfolio is primarily allocated between bonds (with a yield of 4.9% before cost of risk) and equities.

The investment portfolio statistics reveal a balanced approach to risk and return:

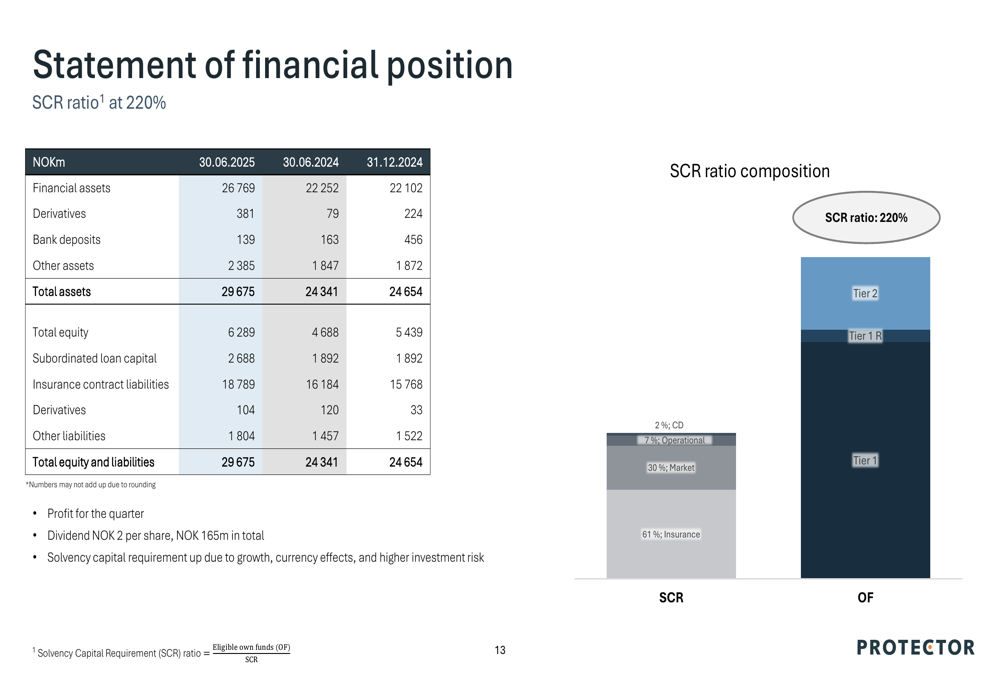

From a capital perspective, Protector maintains a strong position with a Solvency Capital Requirement (SCR) ratio of 220%. The company’s total equity stands at NOK 6,289 million, with total assets of NOK 29,675 million.

The SCR composition shows that insurance risk accounts for 61% of the total, followed by market risk at 30%, operational risk at 7%, and counterparty default risk at 2%.

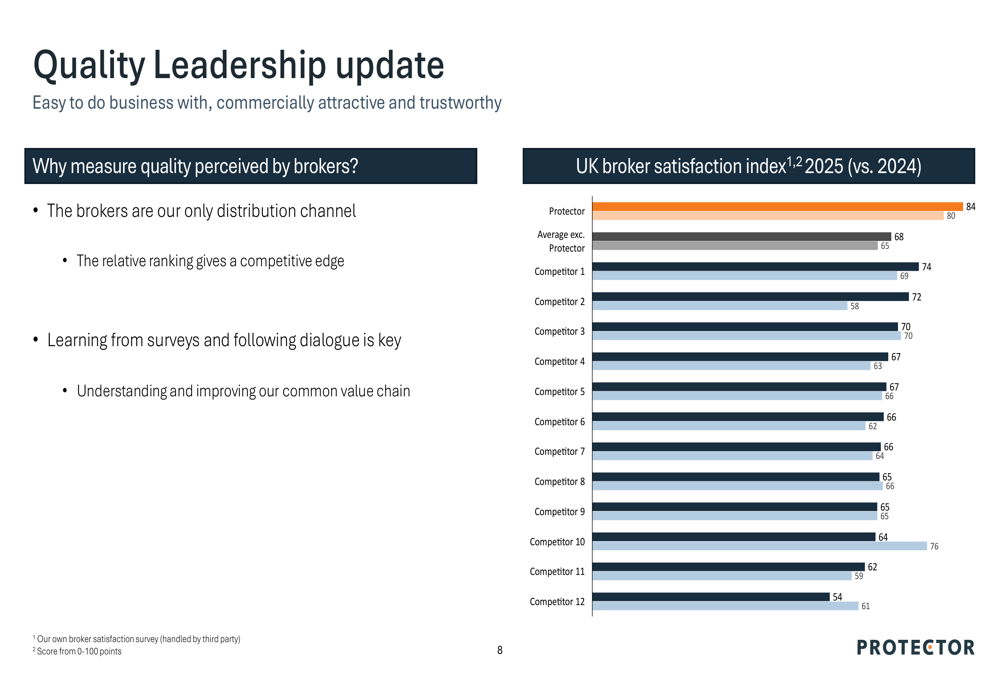

Strategic Positioning and Outlook

Protector continues to position itself as "The Challenger" in the insurance market, focusing on unique relationships, best-in-class decision-making, and cost-effective solutions. The company’s main strategic targets include cost and quality leadership, profitable growth, and achieving a top 3 position in its markets.

The company’s quality leadership is evidenced by its top position in the UK Broker Satisfaction Index:

This achievement underscores Protector’s commitment to building strong broker relationships, which is crucial for its business model. The improvement from a score of 80 in 2024 to 84 in 2025 demonstrates the company’s focus on service quality and broker satisfaction.

Looking ahead, Protector appears well-positioned to maintain its growth momentum, supported by its strong capital position, improved operational efficiency, and strategic focus on key markets. The company’s ability to implement price increases while maintaining high renewal rates suggests continued resilience in a competitive market environment.

The summary of Q2 and H1 2025 results highlights the key achievements and sets a positive tone for the remainder of the year:

With its strong financial performance, improved credit rating, and leading position in broker satisfaction, Protector Forsikring continues to demonstrate its ability to execute its strategic vision as a challenger in the European insurance market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.