Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Executive Summary

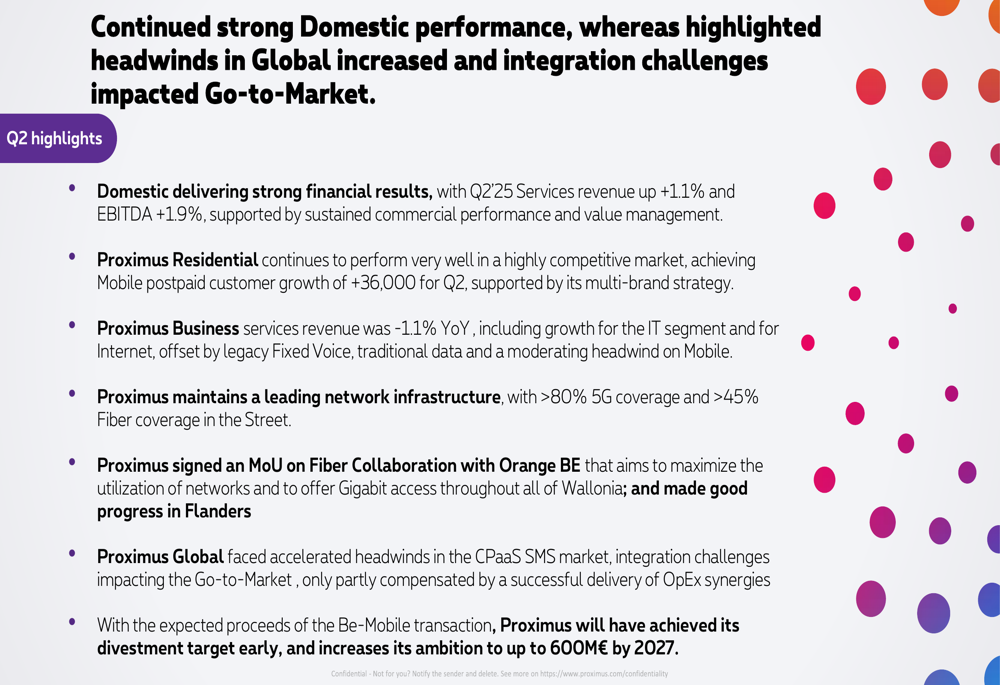

Proximus (EBR:PROX) reported mixed Q2 2025 results on July 25, showing domestic strength but facing challenges in its global operations. The Belgian telecom operator delivered domestic EBITDA growth of 1.9% year-over-year while revising its full-year guidance to reflect these contrasting performances across segments.

The company’s Q2 presentation highlighted solid performance in its residential business, continued fiber network expansion, and strategic partnerships to accelerate infrastructure deployment. However, headwinds in the CPaaS SMS market significantly impacted the global segment, leading to a downward revision of the global EBITDA outlook.

As shown in the following comprehensive overview of key results:

Quarterly Performance Highlights

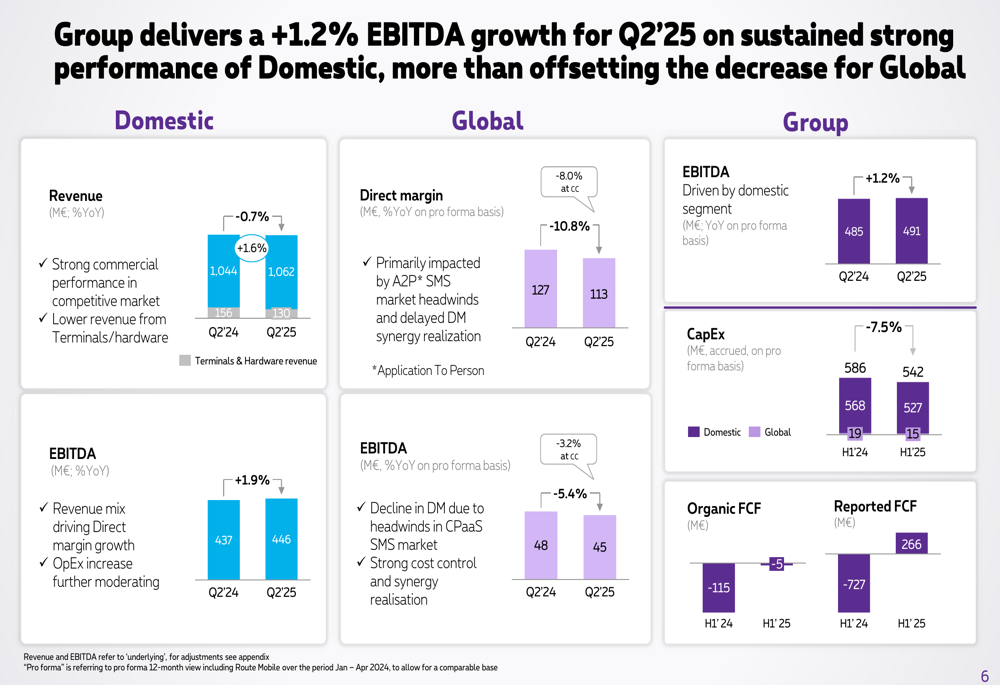

Proximus reported Group EBITDA of €491 million in Q2 2025, representing a 1.2% increase year-over-year. This growth was driven by domestic operations, which saw EBITDA rise by 1.9% to €446 million, while global operations experienced a 5.4% decline to €45 million.

Domestic services revenue grew by 1.1%, supported by strong residential performance, while business services revenue declined by 1.1% year-over-year. The company’s mobile postpaid customer base expanded by 36,000 in Q2, contributing to overall operational growth.

The following slide illustrates the Q2 2025 financial performance across domestic, global, and group segments:

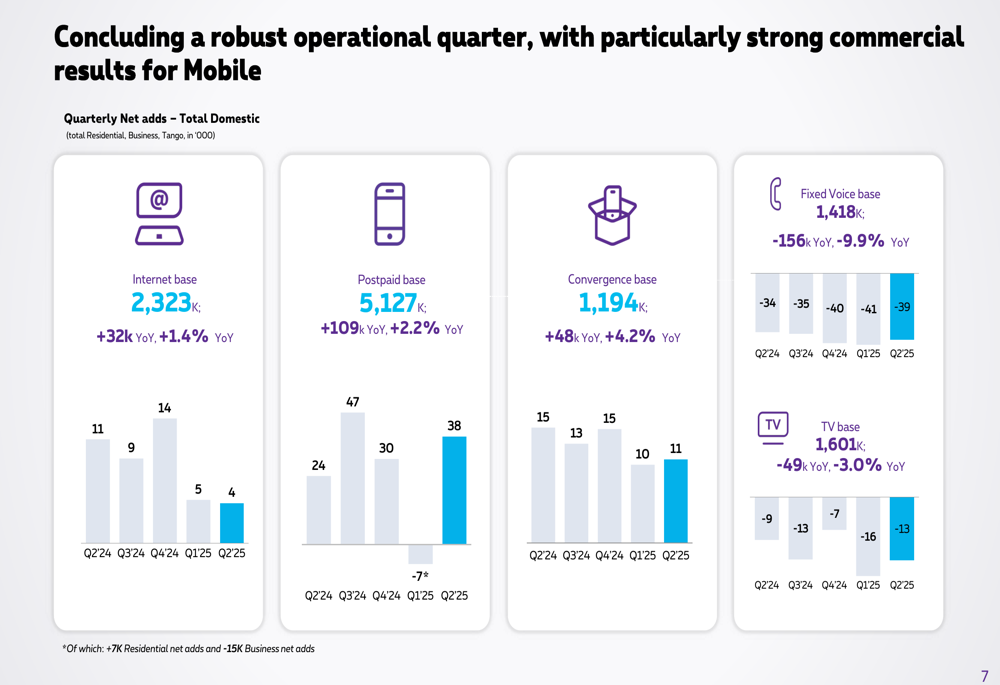

On the operational front, Proximus continued to grow its internet and mobile customer base, with the postpaid base reaching 5,127,000 subscribers, up 2.2% year-over-year. The convergence base grew by 4.2% to 1,194,000, though fixed voice and TV bases declined by 9.9% and 3.0% respectively.

The operational metrics demonstrate continued growth in mobile and internet services:

Revised Financial Guidance

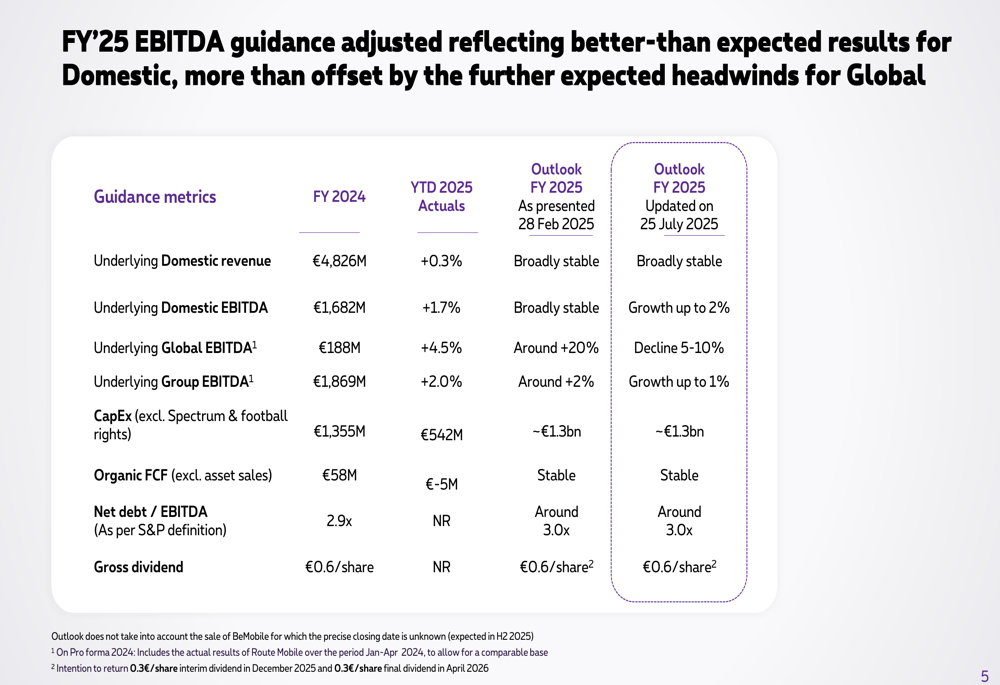

Based on Q2 results, Proximus has adjusted its full-year 2025 outlook, reflecting stronger domestic performance but weaker global results. The company now expects domestic EBITDA to grow up to 2% (improved from "broadly stable"), while global EBITDA is projected to decline by 5-10% (previously expected to grow around 20%).

As a result, group EBITDA is now expected to grow up to 1%, down from the previous guidance of around 2%. Other financial targets remain unchanged, including capital expenditure of approximately €1.3 billion, stable organic free cash flow, and a dividend of €0.6 per share.

The revised guidance is detailed in the following comparison table:

Strategic Network Expansion

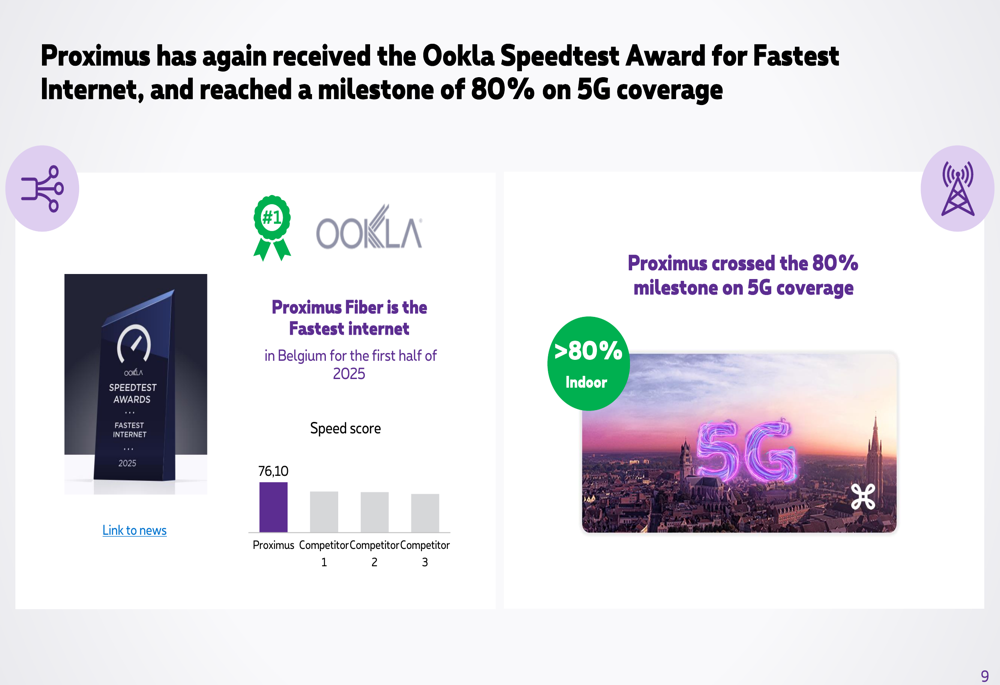

Proximus continues to strengthen its network leadership position, having achieved over 80% 5G coverage and receiving the Ookla Speedtest Award for Fastest Internet in Belgium for the first half of 2025.

The company’s network achievements are highlighted in this slide:

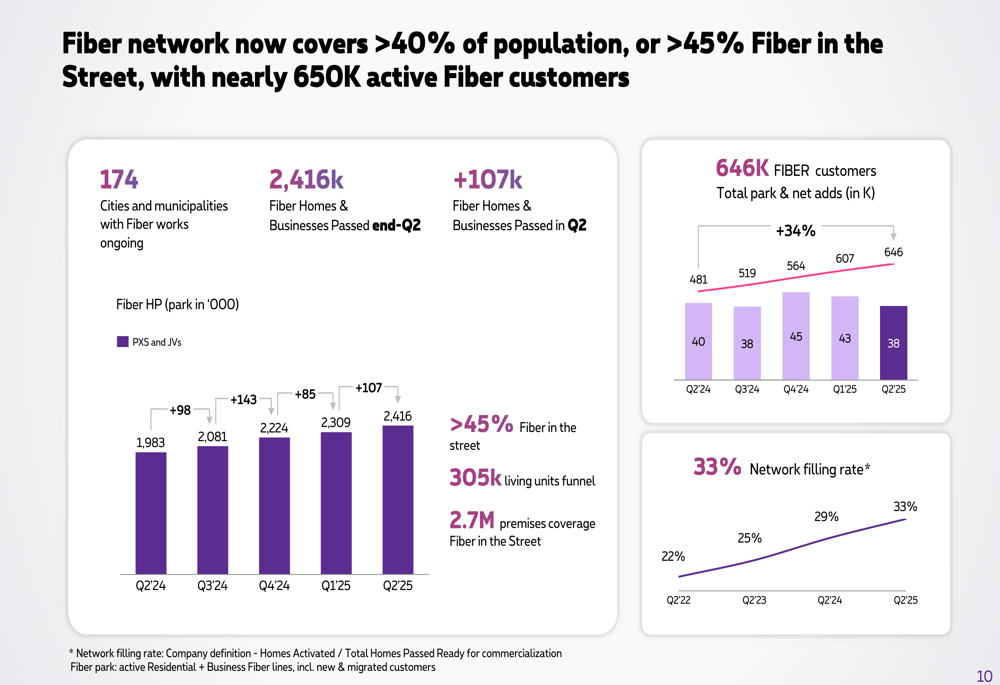

Fiber deployment remains a strategic priority, with 2,416,000 homes and businesses passed by the end of Q2 2025, representing over 45% fiber coverage in the street. The company added 107,000 new premises in Q2 alone and now serves 646,000 fiber customers, achieving a 33% network filling rate.

The fiber expansion metrics are detailed in the following slide:

Strategic Partnerships

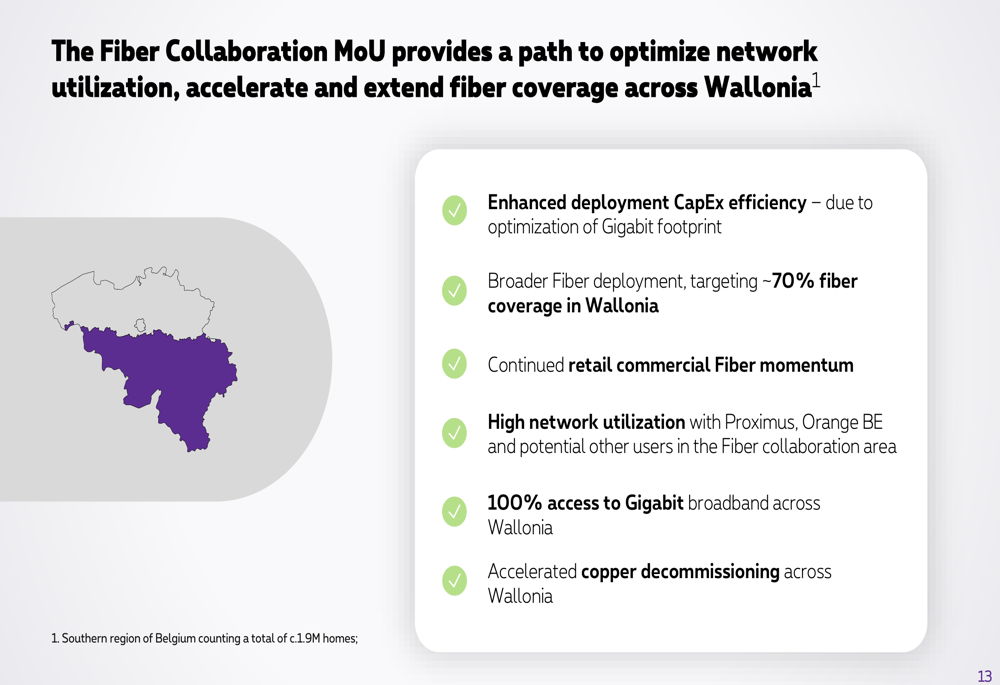

A significant development in Q2 was the signing of a Memorandum of Understanding (MoU) with Orange Belgium for fiber collaboration in Wallonia. This partnership aims to enhance deployment efficiency and expand fiber coverage to approximately 70% in the region.

The collaboration will cover medium-dense (50%) and rural (20%) areas, while dense areas (30%) where fiber is already mostly deployed remain outside the scope. This strategic partnership is expected to accelerate fiber deployment, improve network utilization, and enable faster copper decommissioning.

The following slide outlines the benefits of this fiber collaboration:

In addition to the Orange Belgium partnership, Proximus announced an agreement in principle with Wyre, Telenet, and Fiberklaar to accelerate fiber deployment across Flanders, further strengthening its nationwide fiber strategy.

Segment Analysis

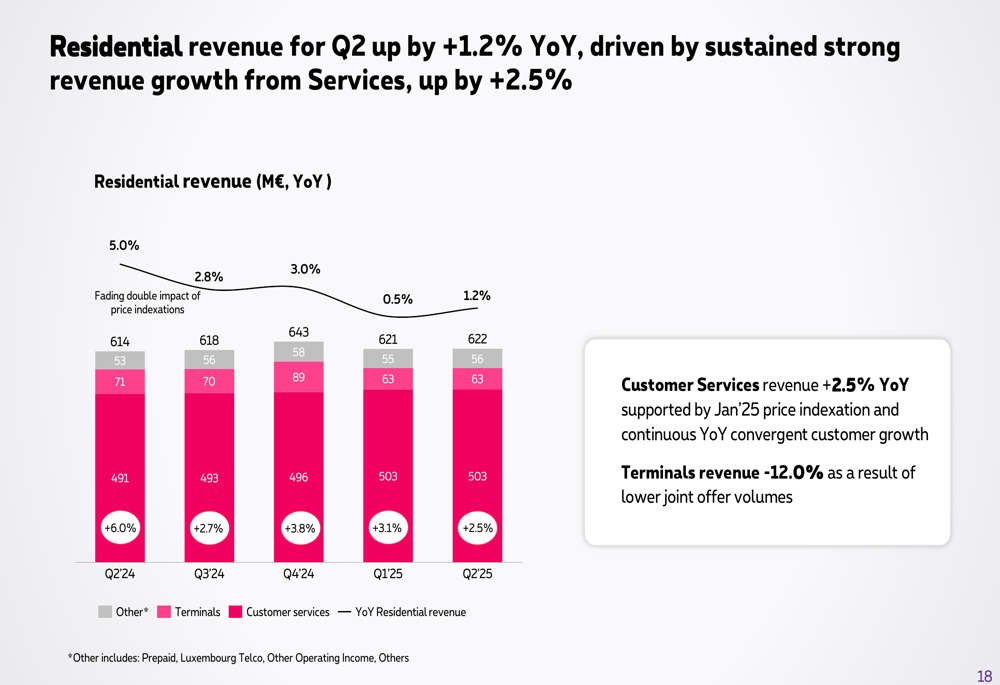

The residential segment showed strong performance, with revenue increasing by 1.2% year-over-year to €622 million. This growth was primarily driven by a 2.5% increase in customer services revenue, supported by the January 2025 price indexation and continuous growth in convergent customers. However, terminals revenue declined by 12.0% due to lower joint offer volumes.

The residential revenue performance is illustrated in this slide:

Convergent revenue grew by 5.4%, with 65% of services revenue now generated by convergent customers. This reflects Proximus’ successful multi-brand strategy, which positions the Proximus brand as premium, Mobile Vikings for cord-cutters, and Scarlet as a defense against low-cost competitors.

In contrast, the business segment faced challenges, with overall revenue declining by 4.4% year-over-year. Services revenue decreased by 1.1%, while products revenue fell sharply by 19.7%. Within B2B services, IT services grew by 1.7% and fixed data by 0.1%, but these gains were offset by declines in mobile (-1.9%) and fixed voice (-6.9%).

Global Segment Challenges

Proximus Global, which includes international operations like Route Mobile, faced significant headwinds in the CPaaS SMS market. The segment’s direct margin declined by 8.0% year-over-year to €113 million, while EBITDA fell by 5.4% to €45 million.

To address these challenges, Proximus outlined a course of action for the second half of 2025, including accelerating growth product initiatives, increasing reach in the omnichannel segment, refocusing on growing markets and more profitable customers, and leveraging global partnerships. The company also announced that Rajdip would be reappointed as CEO for Route Mobile, with a new Global CEO to be appointed shortly.

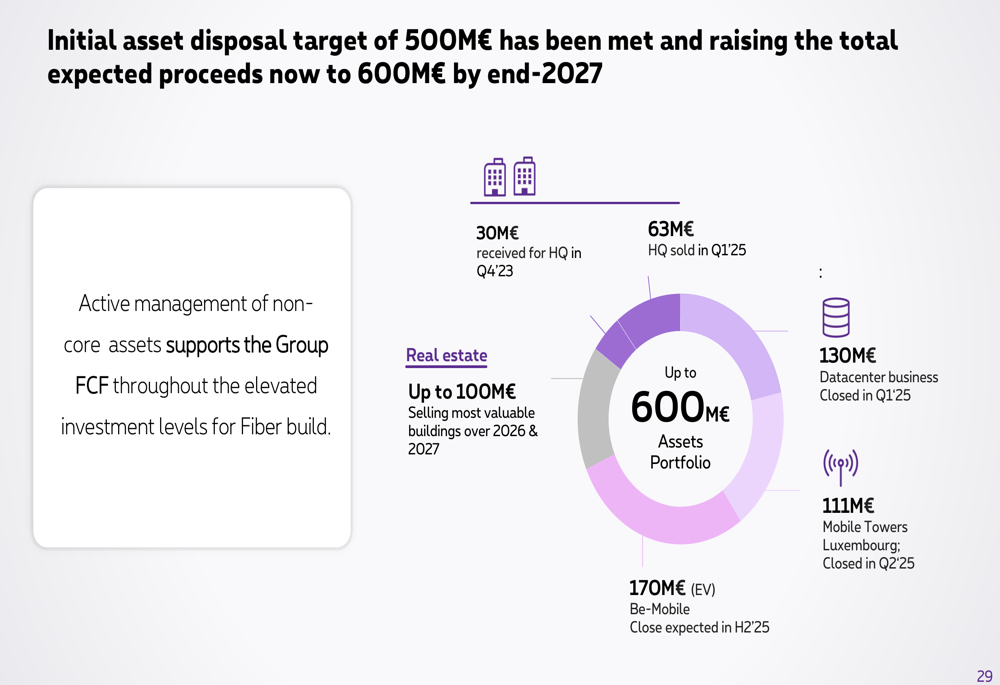

Asset Disposal Program

Proximus has successfully achieved its initial asset disposal target of €500 million and has increased its ambition to up to €600 million by 2027. The company has made significant progress in divesting non-core assets, which will help strengthen its financial position.

The progress of the asset disposal program is detailed in this slide:

Forward Outlook

Despite the challenges in the global segment, Proximus remains confident in its domestic business, which continues to deliver solid results. The company’s strategic focus on network leadership, fiber expansion, and multi-brand approach positions it well in the competitive Belgian telecom market.

The revised guidance reflects a realistic assessment of the contrasting performances across segments, with domestic operations expected to outperform initial expectations while global operations face significant headwinds. The strategic partnerships for fiber deployment are expected to enhance long-term value creation by improving deployment efficiency and accelerating network coverage.

As Proximus navigates through 2025, executing its global segment turnaround strategy and maintaining domestic momentum will be crucial for achieving its financial and operational goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.