Gold prices hover near record peaks as Fed rate cut bets mount

Introduction & Market Context

PYC Therapeutics Ltd (ASX:PYC) hosted its Q3 2025 investor webinar on August 1, 2025, highlighting progress across its RNA therapeutics pipeline targeting genetic diseases with significant unmet needs. The company’s stock closed at $1.24 on July 31, down 2.75% ahead of the presentation, and has faced significant pressure over the past year with a total return of -68.08% according to recent earnings data.

Despite these financial headwinds, PYC emphasized its scientific progress and upcoming clinical milestones, positioning itself as a specialized player in the RNA therapeutics sector with a focus on diseases where current treatment options are limited or nonexistent.

Pipeline Overview

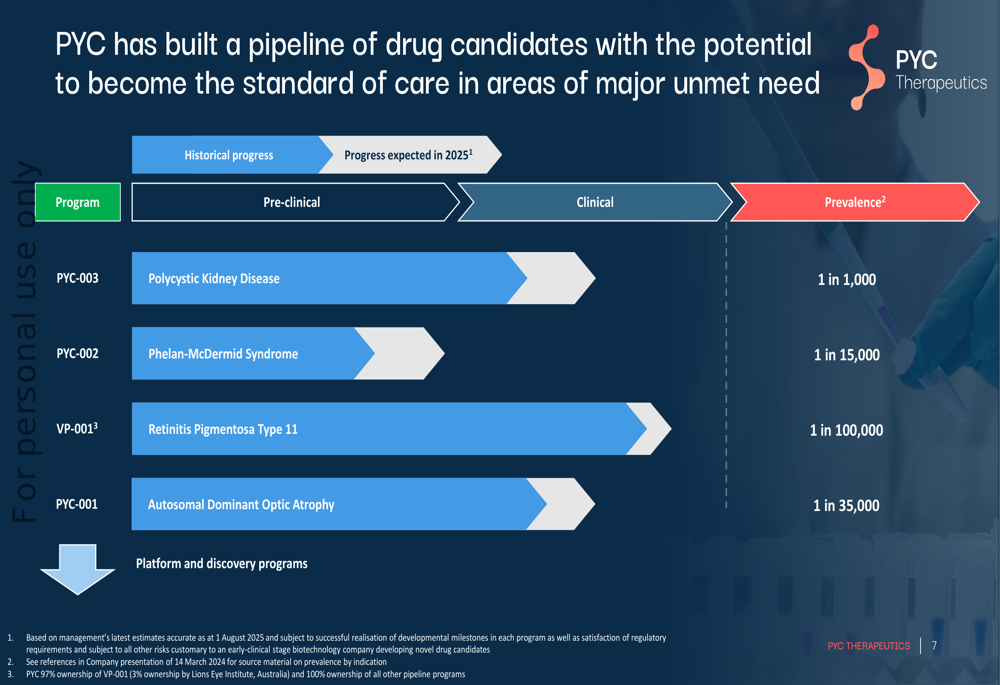

PYC Therapeutics has built a pipeline of drug candidates addressing rare genetic diseases, with three assets now in clinical stages. The company’s strategy centers on using RNA therapeutics to increase gene expression in haploinsufficient diseases where delivery challenges have been overcome.

As shown in the following pipeline overview:

The company’s lead programs include treatments for Polycystic Kidney Disease (prevalence 1 in 1,000), Phelan-McDermid Syndrome (1 in 15,000), Retinitis Pigmentosa Type 11 (1 in 100,000), and Autosomal Dominant Optic Atrophy (1 in 35,000). PYC claims its candidates have a five times higher probability of success than industry averages, targeting diseases with potential markets between $1-10 billion annually.

This pipeline advancement comes as the company faces financial challenges, with recent earnings reports showing negative EBITDA of $0.84M in the last twelve months, though maintaining strong liquidity with a current ratio of 4.77.

Polycystic Kidney Disease Program Deep Dive

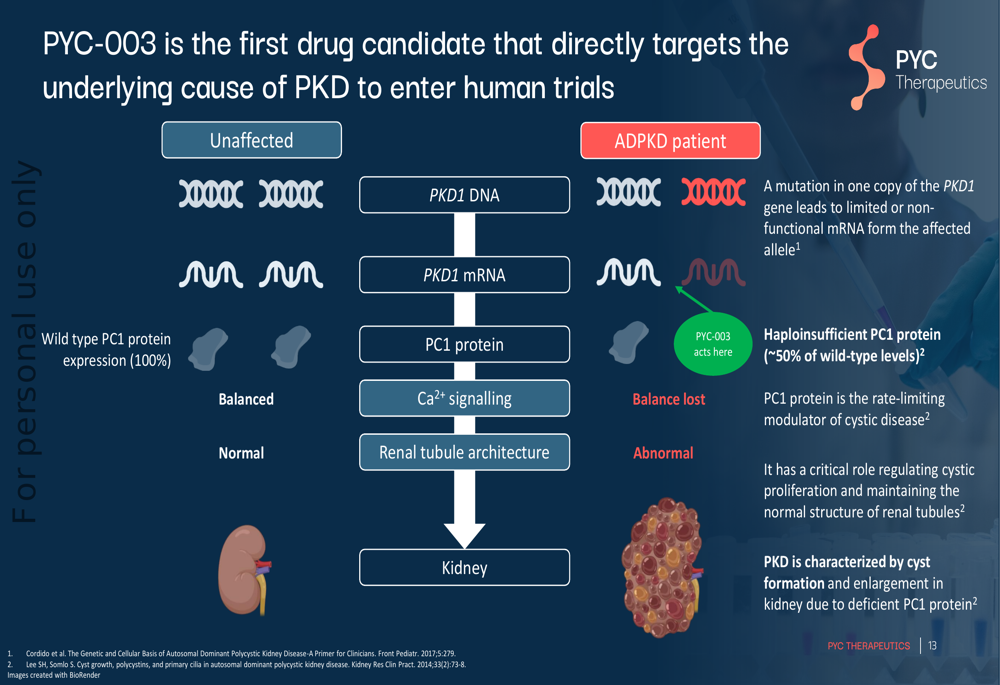

PYC’s PKD program (PYC-003) targets a disease affecting approximately 1 in 1,000 people, with a total addressable market exceeding $15 billion annually. The company noted that current treatment options are limited, with Tolvaptan used by only 7% of the addressable patient population.

The mechanism of action for PYC-003 addresses the root cause of PKD as illustrated below:

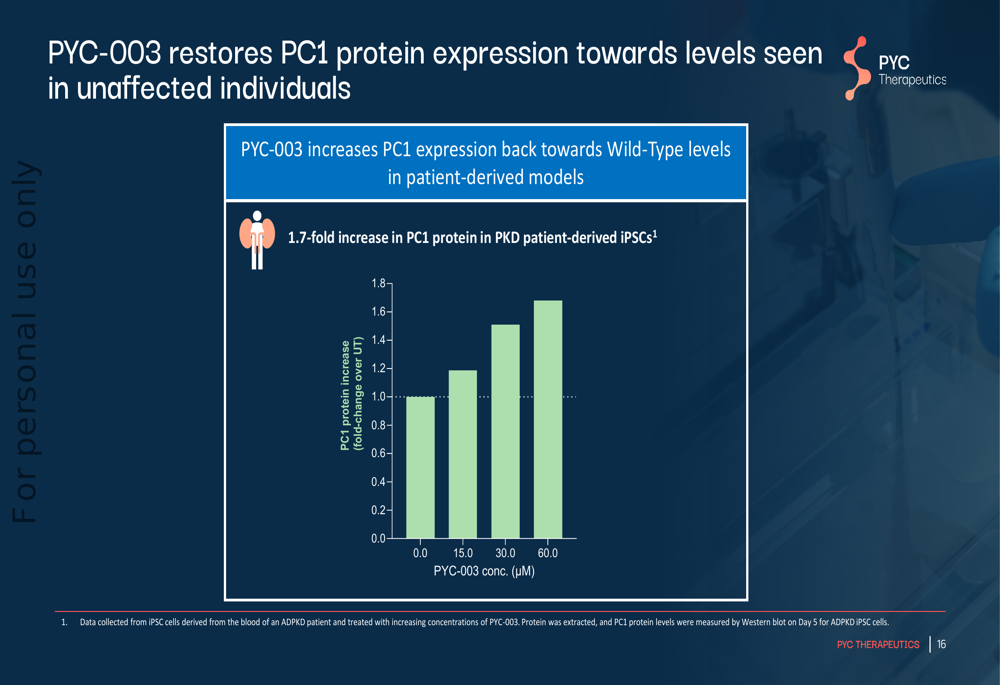

The drug aims to increase levels of functional PC1 protein, which is deficient in PKD patients due to mutations in the PKD1 gene. Pre-clinical data presented shows that PYC-003 increases PC1 protein expression by 1.7-fold in patient-derived models:

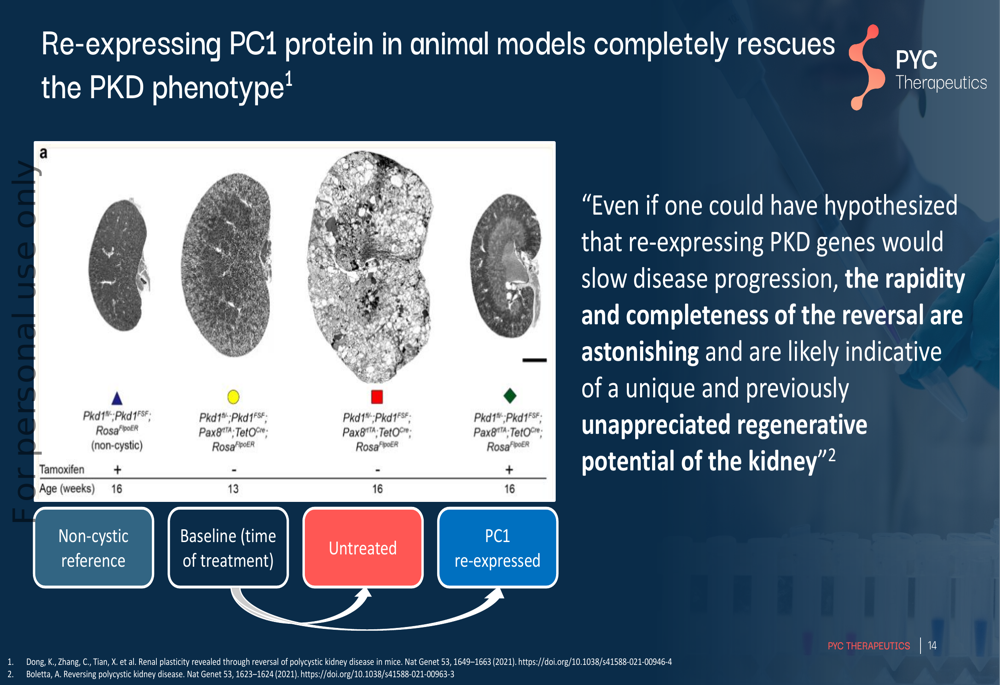

Perhaps most compelling were the animal model results showing potential disease reversal, not just halting progression:

The presentation quoted research stating: "Even if one could have hypothesized that re-expressing PKD genes would slow disease progression, the rapidity and completeness of the reversal are astonishing and are likely indicative of a unique and previously unappreciated regenerative potential of the kidney."

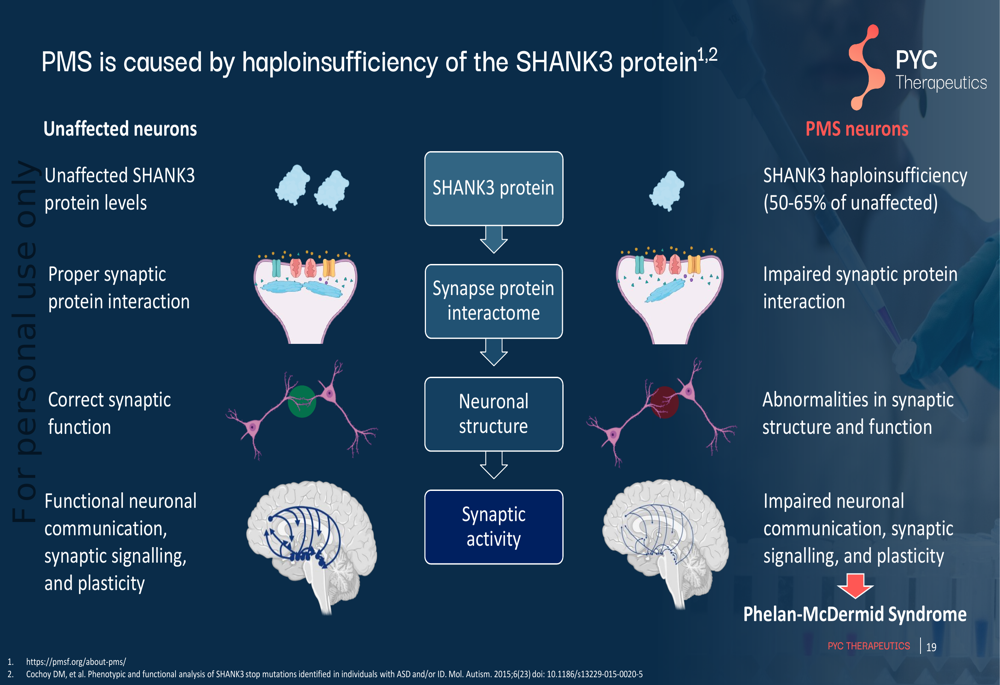

Phelan-McDermid Syndrome Program Highlights

PYC’s second clinical focus is Phelan-McDermid Syndrome (PMS), a rare genetic disorder caused by haploinsufficiency of the SHANK3 protein. The company’s PYC-002 candidate aims to address the underlying neuronal communication deficits, as illustrated in this comparison:

The presentation highlighted potential reversibility of PMS symptoms based on animal models, noting that "genetic restoration of Shank3 in rodents has been shown to reverse core deficits even in adult animals."

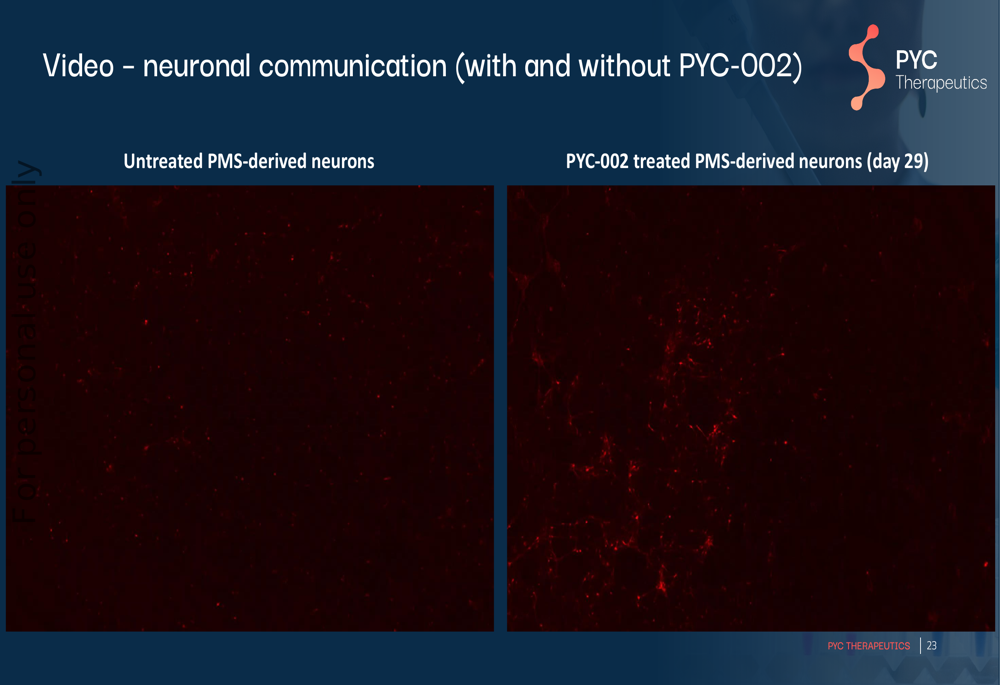

Pre-clinical results showed improved neuronal communication in PYC-002 treated PMS-derived neurons compared to untreated cells:

This data supports the company’s disease-modifying approach, though clinical validation in humans remains pending with pre-clinical data expected in Q3 2025.

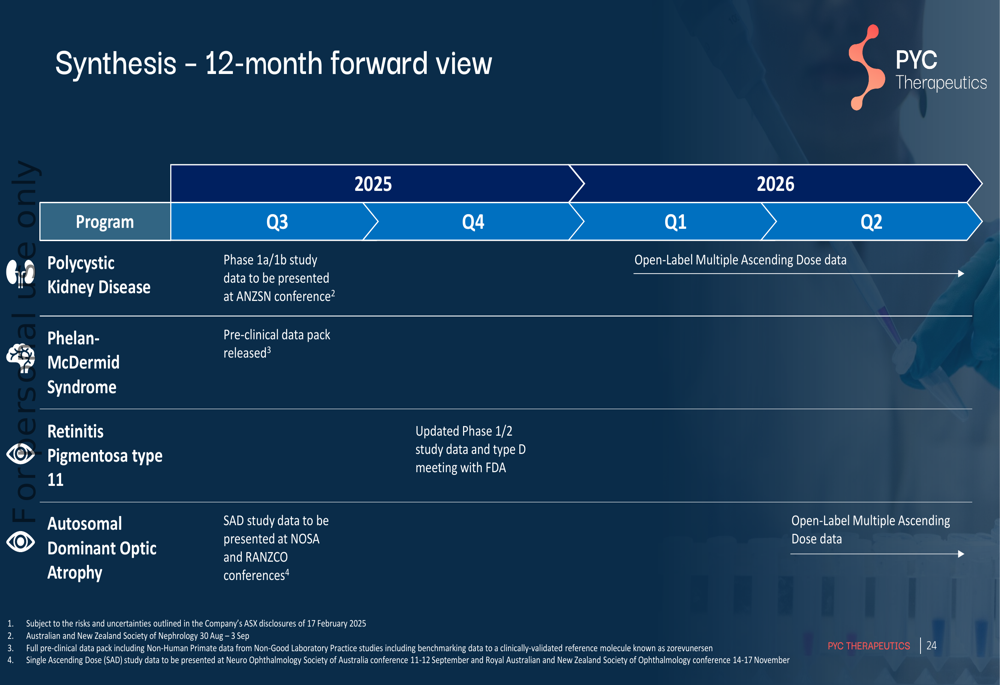

Upcoming Milestones and Catalysts

PYC outlined several near-term catalysts across its pipeline, with multiple data readouts expected over the next 12 months:

Key upcoming milestones include:

- Polycystic Kidney Disease: Phase 1a/1b study data at the ANZSN conference in Q3 2025

- Phelan-McDermid Syndrome: Pre-clinical data pack release in Q3 2025

- Retinitis Pigmentosa type 11: Updated Phase 1/2 study data and FDA meeting in Q4 2025

- Autosomal Dominant Optic Atrophy: SAD study data at conferences in Q3 2025

These data readouts represent potential inflection points for the company as it seeks to demonstrate clinical proof-of-concept for its technology platform.

Financial Position and Challenges

While PYC’s presentation focused primarily on scientific progress and upcoming milestones, it’s worth noting the company’s financial challenges as reflected in recent earnings reports. The company maintains a "weak" financial health score according to analyst assessments, with expectations of continued net income decline this year.

Management has indicated they are exploring non-dilutive funding options through potential out-licensing deals, which could help address capital needs for advancing their pipeline. The estimated cost for just the RP11 registrational study is projected at approximately $60 million, highlighting the significant funding requirements ahead.

The disconnect between scientific progress and stock performance (currently trading near $1.24, down from a 52-week high of $2.089) suggests investors remain cautious about the company’s path to commercialization despite the promising pre-clinical and early clinical data presented across multiple programs.

As PYC moves toward multiple clinical readouts in the coming quarters, these results will be critical in determining whether the company can translate its scientific approach into commercial success and reverse the negative stock performance trend of the past year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.