Michigan survey ahead; Applied Digital surges; gold dips - what’s moving markets

Introduction & Market Context

QCR Holdings Inc (NASDAQ:QCRH) recently presented its Q2 2025 investor slides, showcasing the Midwest-based bank holding company’s continued growth trajectory and differentiated business model. Established in 1993, the company has grown to $9.2 billion in total assets with 36 locations across three states, supported by over 1,000 team members. Following its Q2 earnings release where it beat EPS expectations but missed revenue forecasts, QCRH shares have stabilized around $76.11, well above its 52-week low of $60.83 but below its high of $96.08.

The bank’s presentation emphasizes its relationship-driven approach and track record of profitable growth, with a vision focused on "exceptional people providing extraordinary performance." This strategy appears to be working, as the company reported an adjusted net income of $29 million in Q2 2025, translating to an EPS of $1.73 that surpassed the forecasted $1.59 by 8.81%.

Business Model & Market Position

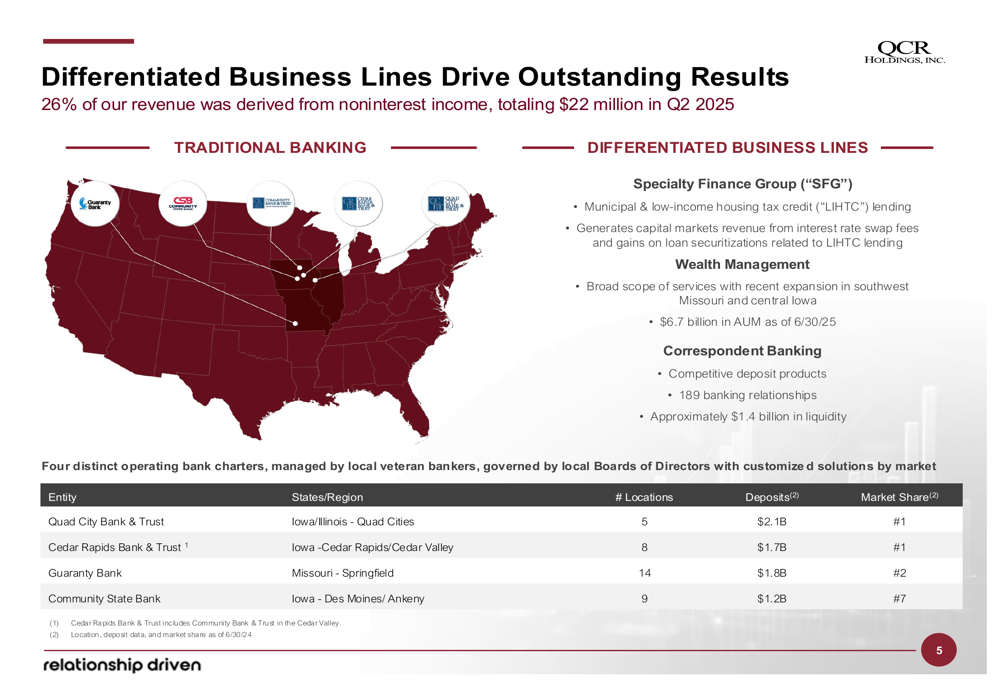

QCR Holdings operates through four distinct bank charters, each managed by local veteran bankers with significant autonomy. This structure has helped the company achieve leading market positions in key regions, including the #1 market share in both the Quad Cities (Iowa/Illinois) and Cedar Rapids (Iowa), and the #2 position in Springfield, Missouri.

As shown in the following chart of the company’s differentiated business lines:

The company’s business model extends beyond traditional banking to include specialty finance, wealth management, and correspondent banking services. This diversification strategy has allowed QCR to generate 26% of its revenue from non-interest income, totaling $22 million in Q2 2025. This significantly outpaces peer banks, which typically derive around 20% of revenue from non-interest sources.

Financial Performance

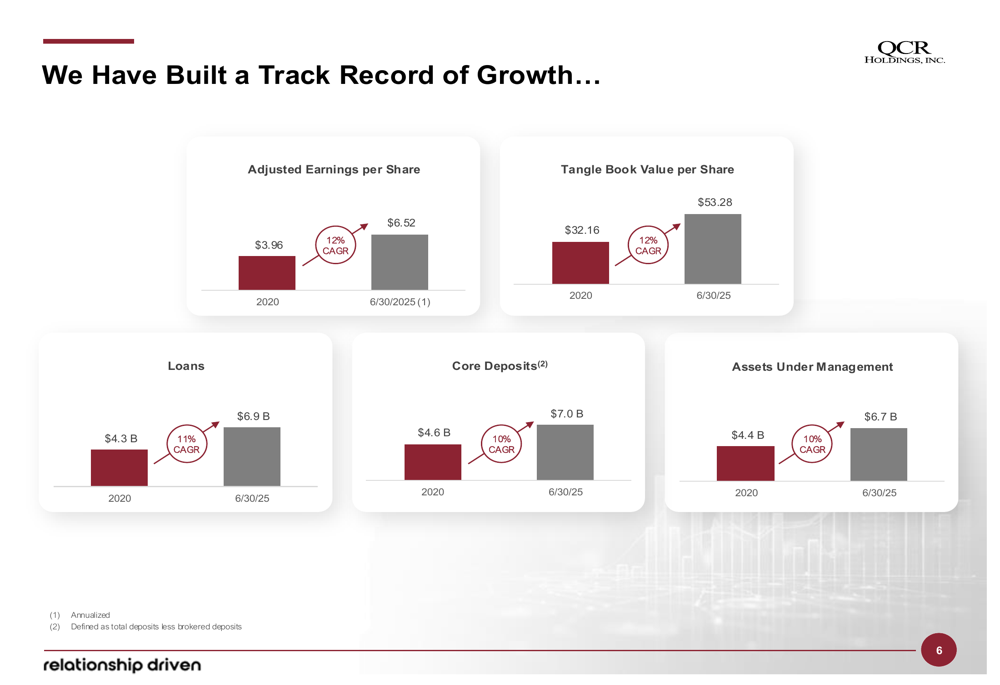

QCR Holdings has demonstrated consistent growth across all key financial metrics over the past several years. The company’s adjusted earnings per share grew at a 12% CAGR from $3.96 in 2020 to $6.52 as of June 30, 2025, while tangible book value per share increased at the same rate from $32.16 to $53.28 during this period.

The following chart illustrates this impressive growth trajectory across multiple metrics:

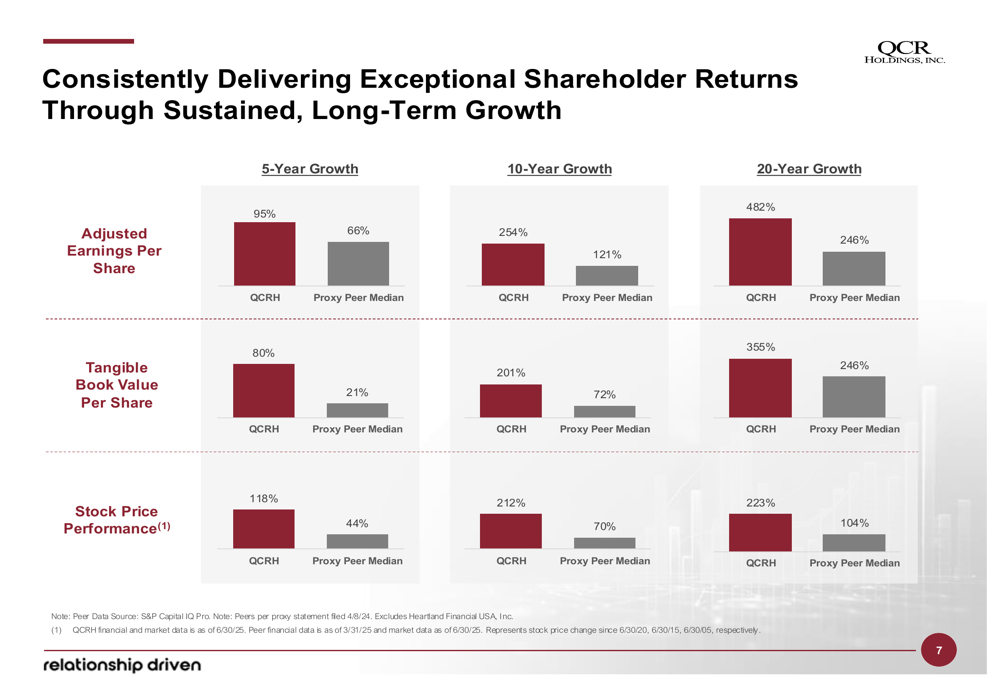

When compared to its proxy peer group, QCR Holdings has delivered exceptional shareholder returns. Over the past five years, the company’s adjusted EPS grew by 95% versus 66% for peers, while tangible book value per share increased by 80% compared to just 21% for peers. This superior performance has translated into stock price appreciation of 118% over five years, substantially outperforming the peer median of 44%.

The company’s strong performance is further illustrated in this comparative chart:

Revenue Diversification

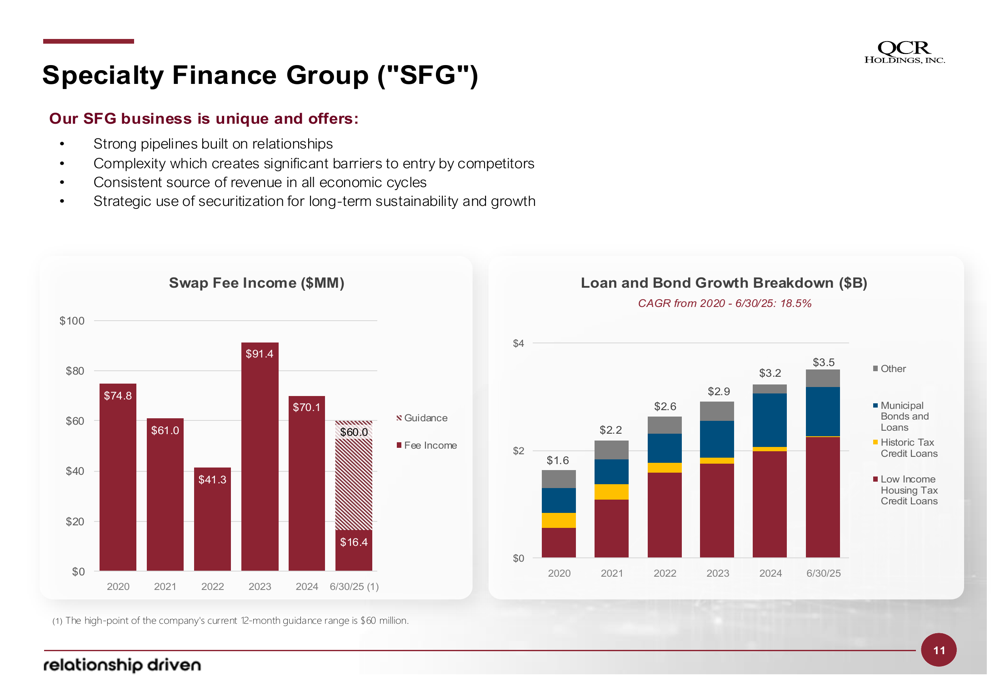

A key differentiator for QCR Holdings is its Specialty Finance Group (SFG), which focuses on municipal and low-income housing tax credit (LIHTC) lending. This business segment has been a consistent source of revenue across economic cycles, with swap fee income growing from $41.3 million in 2020 to $91.4 million in 2024.

The following chart demonstrates the growth and contribution of the Specialty Finance Group:

The company has successfully leveraged securitization to sustain growth in its LIHTC portfolio, closing four securitizations that sold nearly $650 million of LIHTC loans via Freddie Mac Programs. These transactions strengthened capital, improved net interest margin, and increased liquidity, while generating a $1 million net gain in 2024.

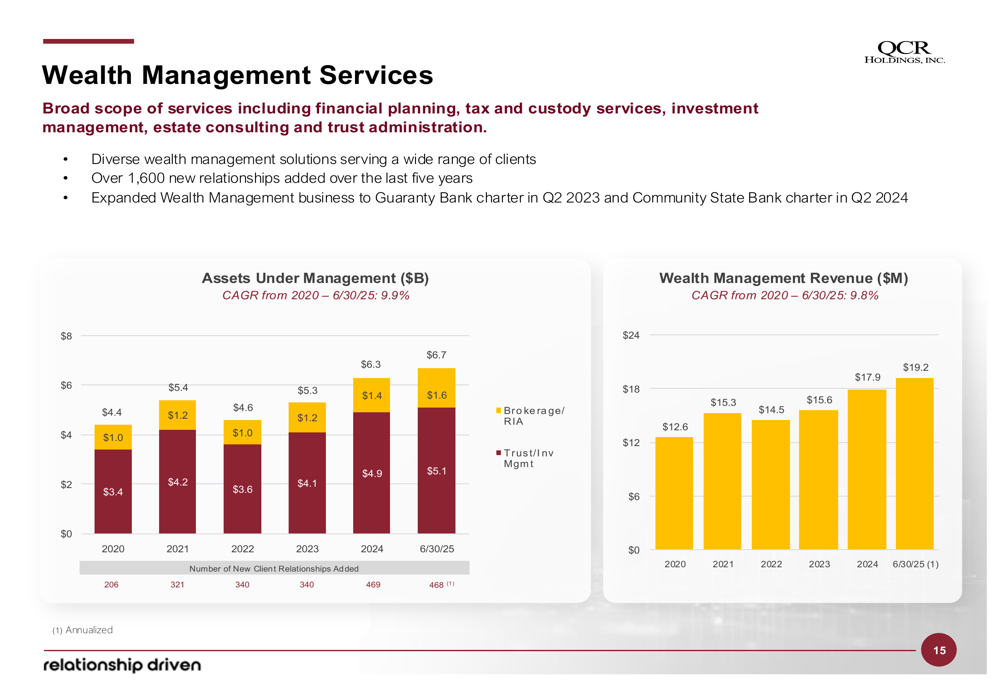

Wealth management represents another significant non-interest income stream for QCR Holdings. With $6.7 billion in assets under management as of June 30, 2025, this business has grown at a CAGR of 9.9% since 2020. The company has expanded its wealth management services to its Guaranty Bank charter in Q2 2023 and Community State Bank charter in Q2 2024, adding over 1,600 new relationships over the past five years.

Credit Quality & Risk Management

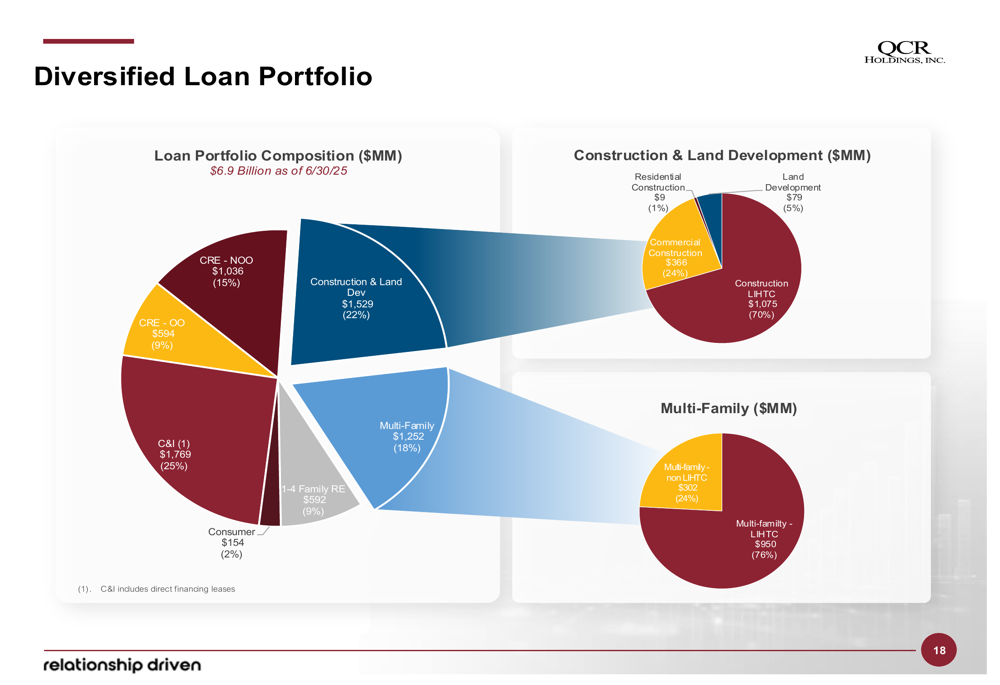

QCR Holdings maintains a diversified loan portfolio with a focus on commercial lending, which represents 92% of the total loan book. The portfolio is well-balanced across various sectors, with construction and land development accounting for 22%, multi-family properties 18%, commercial real estate (non-owner occupied) 15%, and commercial and industrial loans 25%.

The following chart provides a detailed breakdown of the loan portfolio composition:

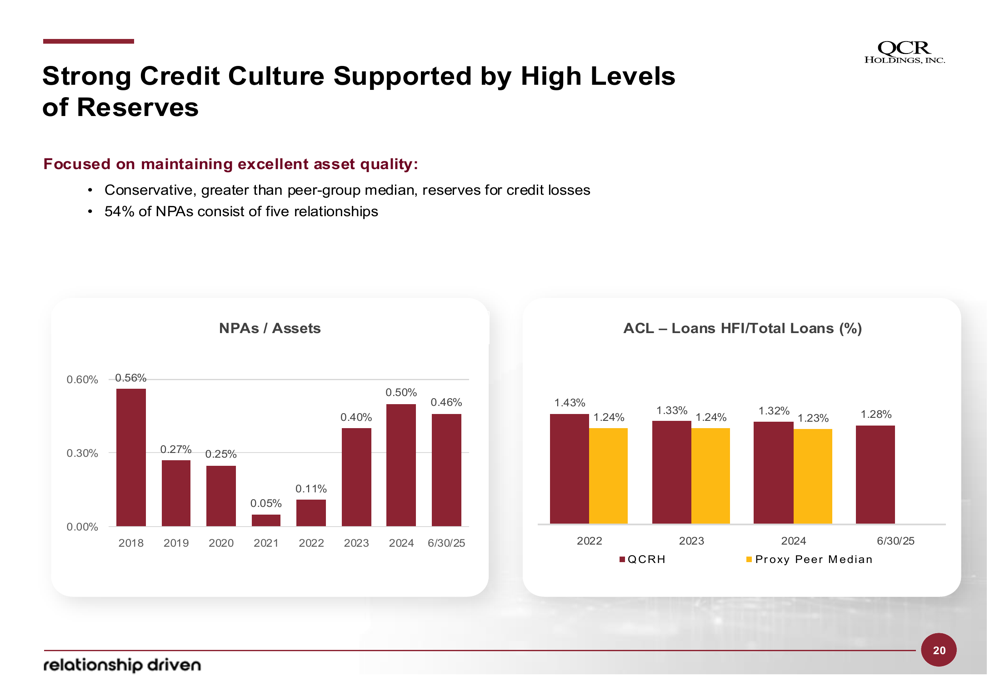

Despite having 58% of total loans in commercial real estate, the company has maintained strong credit quality. CRE-Office exposure is limited to just 3% of total loans, and over 99% of all CRE loans are performing. This conservative approach to lending is reflected in the company’s non-performing assets ratio and allowance for credit losses, which exceeds peer-group median levels.

Outlook & Guidance

Looking ahead, QCR Holdings projects gross loan growth of 8-10% in the second half of 2025, aligning with the 8% annualized loan growth reported in Q2 (excluding equipment finance runoff). The company anticipates capital markets revenue of $50-60 million over the next four quarters, with Q3 expected to contribute $13-16 million.

The bank is well-positioned in the current interest rate environment, having become liability sensitive due to shifts in its core deposit portfolio. Management expects to benefit from recent and future interest rate cuts, while also capitalizing on continued loan repricing under a potentially steepening yield curve.

During the recent earnings call, CEO Todd Gipple emphasized the company’s strategic focus, stating, "We are focused on building something here that is materially different and significantly better than others." He also highlighted the LIHTC program’s role in providing affordable housing, underscoring the company’s commitment to leveraging its unique capabilities for sustained growth.

Investment Thesis

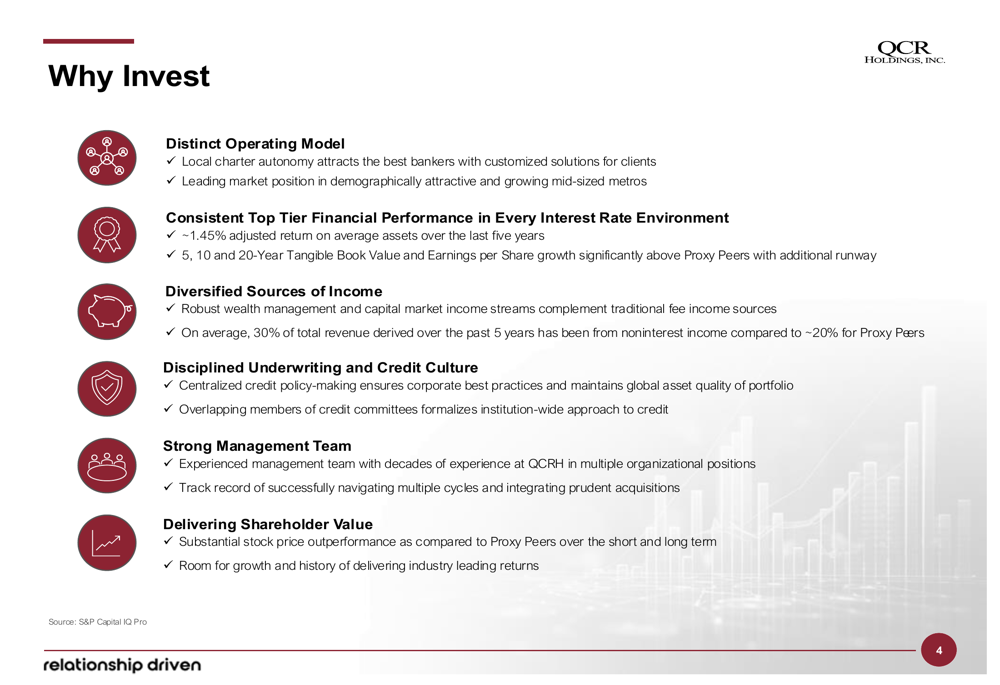

QCR Holdings presents a compelling investment case based on its differentiated operating model, consistent top-tier financial performance, and diversified income streams. The company has demonstrated superior tangible book value and earnings per share growth compared to peers, supported by disciplined underwriting and a strong management team.

The following slide summarizes the key investment highlights:

With the lowest dividend payout ratio in its peer group, the company retains significant capital for both organic growth and potential acquisitions. This approach, combined with strong earnings and strategic securitizations, has enabled QCR Holdings to expand its capital base organically while delivering substantial shareholder value.

While the company faces challenges including revenue shortfalls and potential regulatory hurdles as it approaches the $10 billion asset threshold, its differentiated business model and strong market positions provide a solid foundation for continued growth and outperformance relative to peers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.