Fiserv earnings missed by $0.61, revenue fell short of estimates

Introduction & Market Context

Qoria Ltd (ASX:QOR) presented its Q1 2026 activity report on October 21, 2025, highlighting record cash receipts and strong growth across its business segments. The company, which positions itself as a global leader in online safety and student wellbeing, reported significant improvements in key financial metrics, leading to an upgrade in its revenue guidance for the fiscal year.

The stock responded positively to the presentation, rising 2.34% to $0.855 per share, continuing its strong performance trajectory. Qoria’s share price has seen substantial growth over the past year, trading near its 52-week high of $0.94, compared to a low of $0.31.

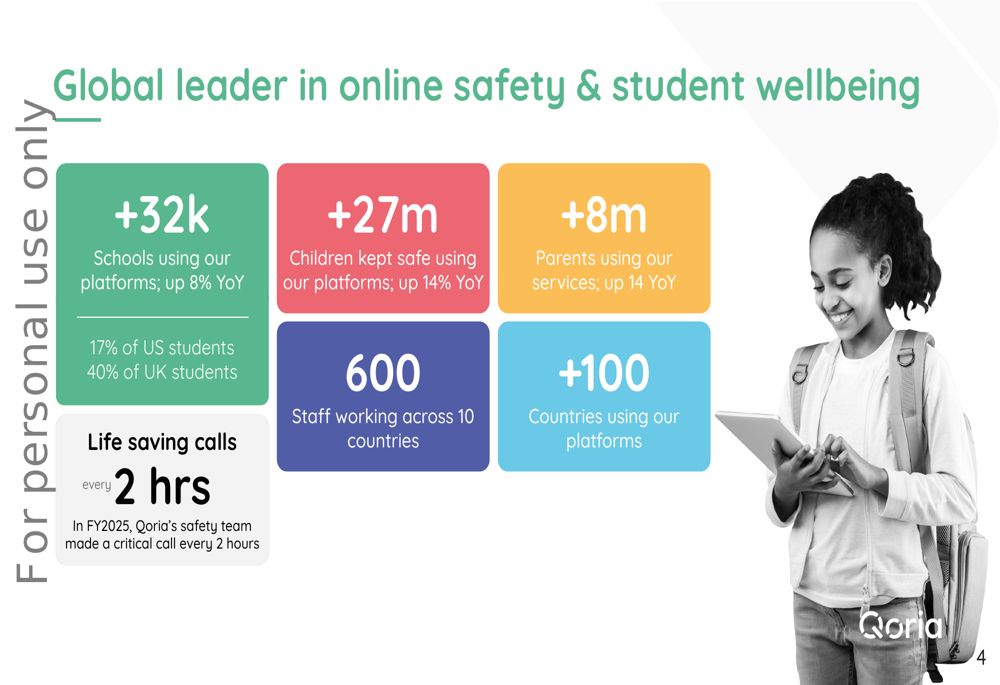

As shown in the following slide highlighting Qoria’s global market position:

Quarterly Performance Highlights

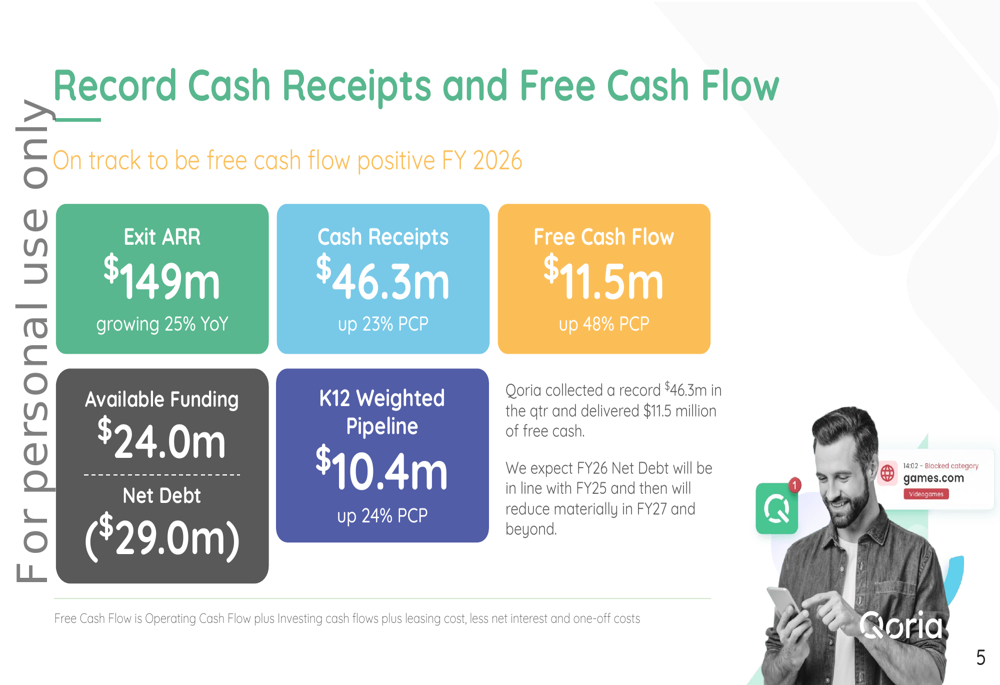

Qoria reported record cash receipts of $46.3 million for Q1 2026, representing a 23% year-over-year increase. Free cash flow surged to $11.5 million, up 48% compared to the same period last year. The company’s Annual Recurring Revenue (ARR) reached $149 million, growing 25% year-over-year.

These strong results have prompted management to upgrade its FY 2026 revenue guidance from +$140 million to +$145 million. The company is targeting 20% growth and a 20% EBITDA margin, while maintaining positive free cash flow for the year.

The following slide illustrates Qoria’s record cash receipts and free cash flow performance:

Managing Director Tim Levy expressed satisfaction with the results, noting that strong growth across segments and collections/free cash flow exceeded guidance, enabling the company to upgrade its revenue outlook for the fiscal year.

Segment Analysis

Qoria demonstrated growth across all its key market segments. The US K12 business generated US$41.5 million in Last Twelve Months (LTM) revenue, growing 28%. The UK K12 segment reached £23.5 million LTM with 6% growth, while ANZ K12 delivered AUD$7 million LTM, growing 24%.

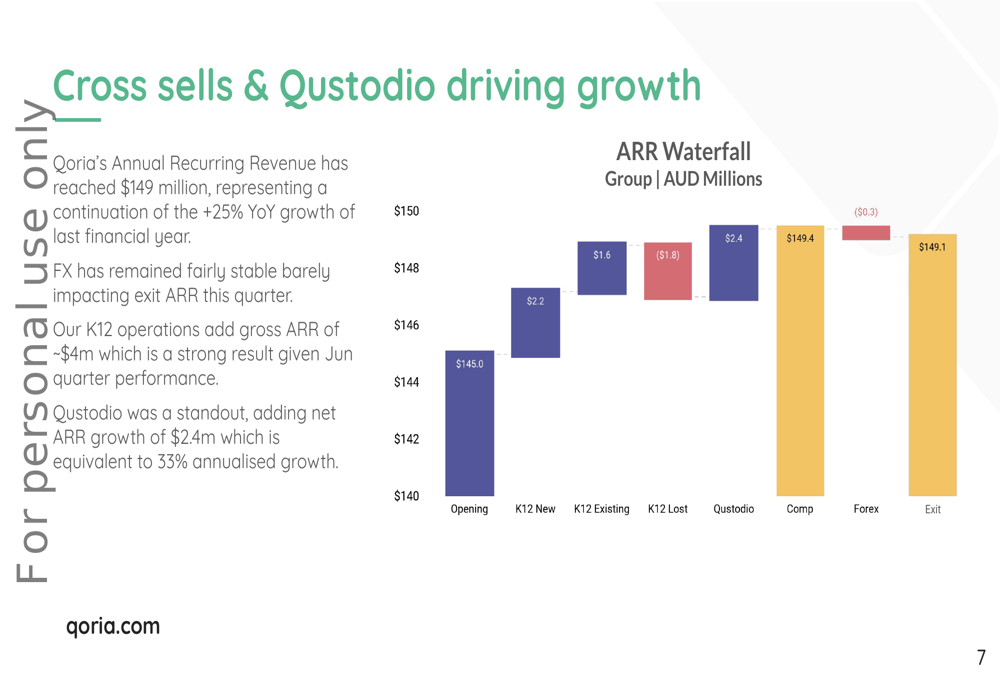

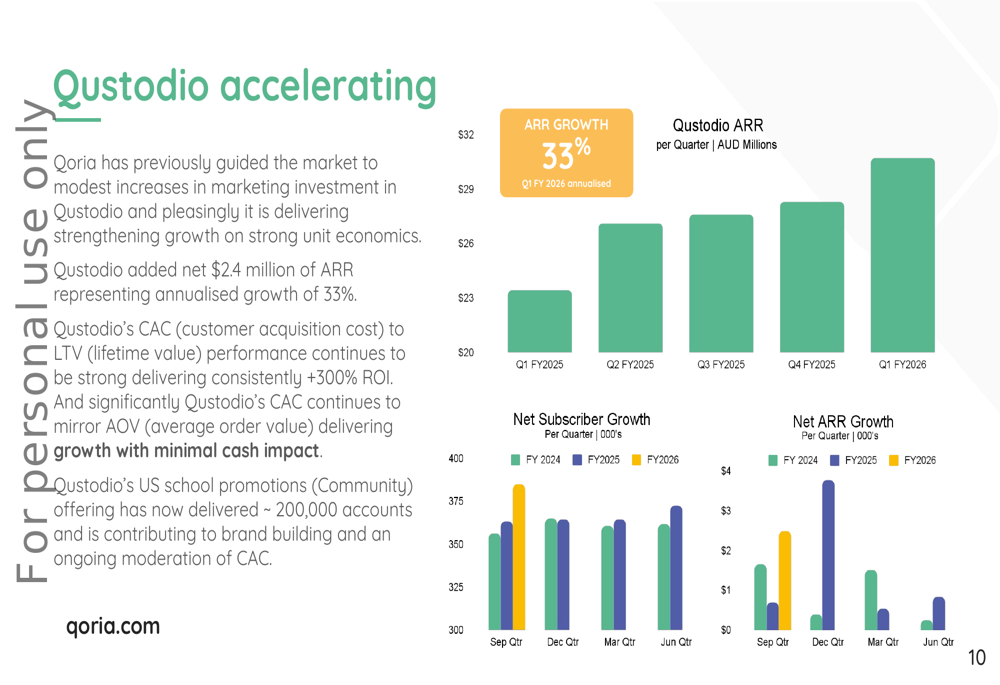

Notably, Qustodio, the company’s consumer-focused product, was a standout performer with US$20 million LTM revenue (26% growth). During Q1, Qustodio added net ARR of $2.4 million, representing an annualized growth rate of 33%.

The following waterfall chart breaks down the components of Qoria’s ARR growth:

The company’s cross-selling and upselling strategy is delivering results, contributing 43% of new ARR in the K12 segment. Qoria was also awarded ’Education partner of 2025’ by new channel partner CDW, potentially opening new growth avenues.

As shown in the following slide detailing Qustodio’s accelerating performance:

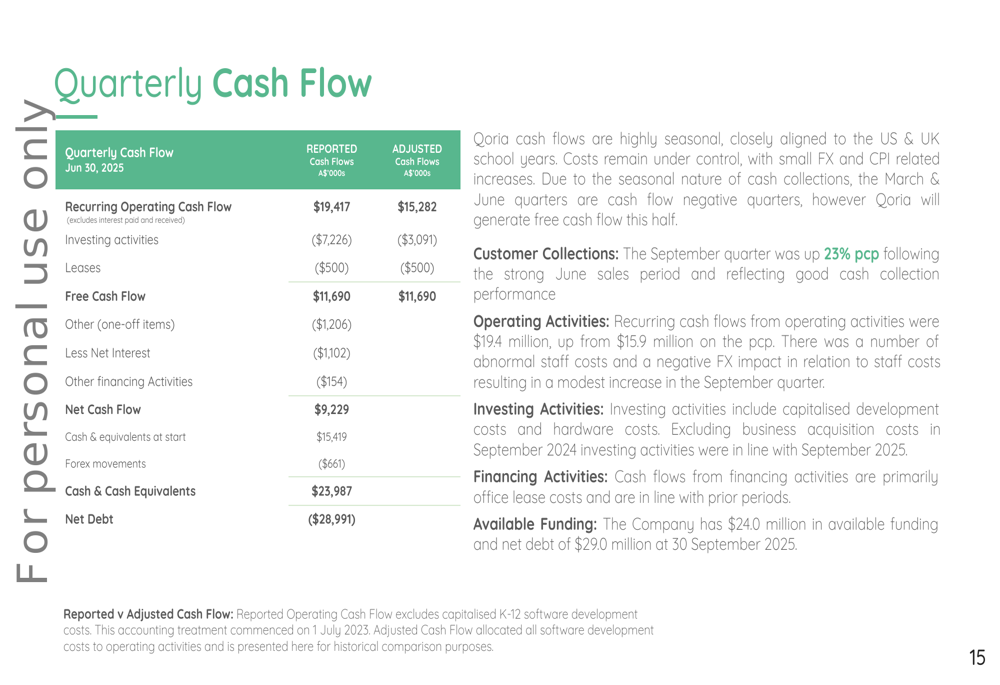

Financial Position and Cash Flow

Qoria’s cash flow demonstrated strong seasonality aligned with the US and UK school years, with 60-65% of K12 invoicing collected between July and October. The company expects receipts in H1 FY 2026 to be 20% higher than the previous corresponding period.

The company maintained a solid financial position with available funding of $24.0 million and net debt of $29.0 million. Management expects FY26 net debt to remain in line with FY25 levels, with material reductions anticipated in FY27.

The following slide details Qoria’s quarterly cash flow performance:

Operating leverage continues to improve, with fixed costs falling relative to ARR. The company is EBITDA positive and guiding to 20% EBITDA margins this financial year.

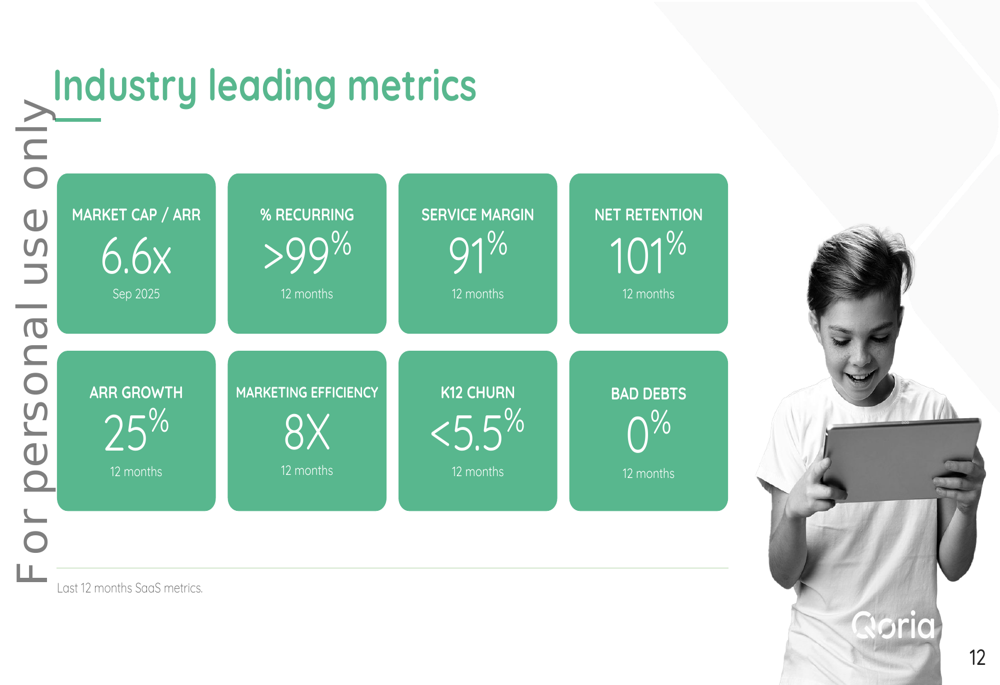

Industry Position and Key Metrics

Qoria continues to strengthen its position in the online safety and student wellbeing sector. The company now protects over 27 million children (up 14% YoY) across more than 32,000 schools (up 8% YoY) in over 100 countries. Additionally, more than 8 million parents are using Qoria’s services, representing a 14% year-over-year increase.

The company highlighted several industry-leading metrics, including a market cap to ARR ratio of 6.6x, recurring revenue exceeding 99%, service margin of 91%, and net retention of 101%. K12 churn remains below 5.5%, while bad debts stand at 0%.

The following slide presents Qoria’s key performance metrics:

Forward-Looking Statements

Looking ahead, Qoria expects a strong calendar year close, despite December typically being a seasonally quiet quarter for its K12 business units. The company reported a K12 weighted pipeline of $10.4 million, up 24% from the previous corresponding period.

For FY 2026, Qoria has reiterated its guidance for positive free cash flow and is now targeting revenue of over $145 million, representing growth of more than 20% year-over-year. The company aims to achieve an EBITDA margin of at least 20%.

Management noted that FY26 net debt is expected to remain in line with FY25 levels, with material reductions anticipated in FY27. The company also highlighted its exposure to currency fluctuations, noting that it is a net beneficiary of a weakening Australian dollar against the US dollar and British pound.

As the digital safety landscape continues to evolve, Qoria appears well-positioned to capitalize on growing demand for online safety solutions in both educational and consumer markets, supported by its strong financial performance and expanding global footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.