Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

Quadient SA (EPA:QDT) released its first-half 2025 results on September 24, showing a 3% organic revenue decline to €517 million while maintaining stable profitability. The company’s shares closed at €15.98 on the presentation day, down 0.25% and well below their 52-week high of €20.15, reflecting ongoing investor concerns about the transition from traditional mail solutions to digital services and parcel lockers.

The results presentation highlighted Quadient’s continued strategic shift toward recurring revenue streams, which now account for 74% of total revenue, providing stability amid challenges in the mail hardware business. This follows a similar pattern observed in Q1 2025, when the company reported a 1.1% revenue decline but maintained its full-year guidance.

Executive Summary

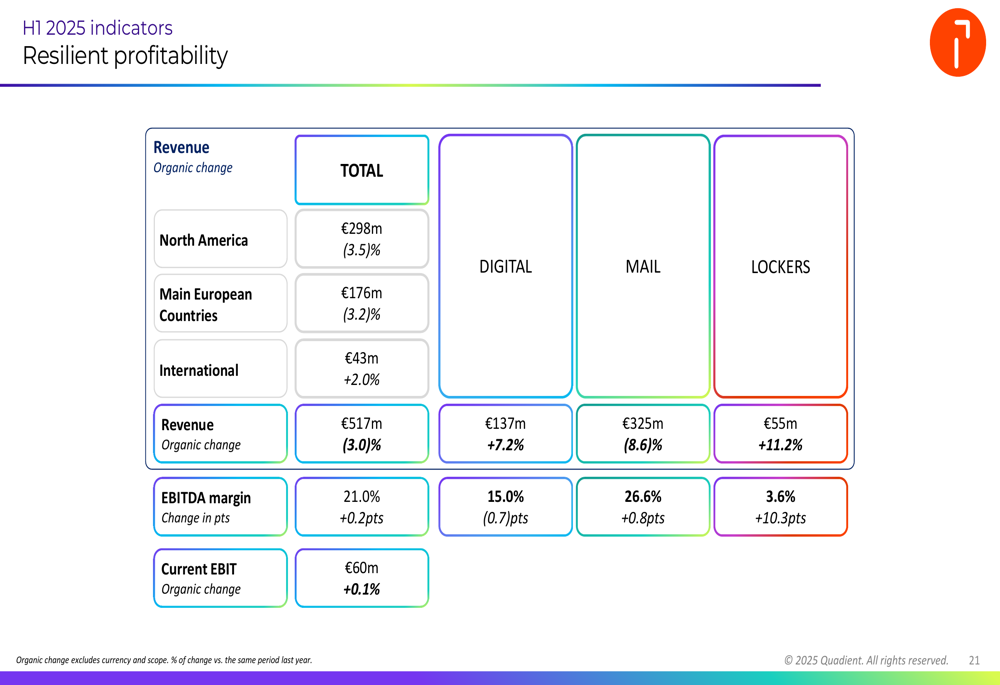

Quadient reported H1 2025 revenue of €517 million, representing a 3% organic decline from the €534 million recorded in H1 2024. Despite this topline pressure, the company delivered a stable current EBIT of €60 million, demonstrating resilience in its profitability metrics.

The performance was characterized by diverging trends across business segments: strong momentum in Digital with double-digit growth in subscription-related revenue, 30% reported growth in Lockers (including the Package Concierge acquisition), and weakness in Mail hardware sales due to a temporary low point in the US renewal cycle.

As shown in the following breakdown of H1 2025 key financial indicators by segment:

Income before tax improved to €37 million from €24 million in H1 2024, though net income decreased to €21 million from €26 million in the prior year period. The company’s EBITDA margin remained resilient at 21.0%, a slight improvement of 0.2 percentage points year-over-year.

Detailed Financial Analysis

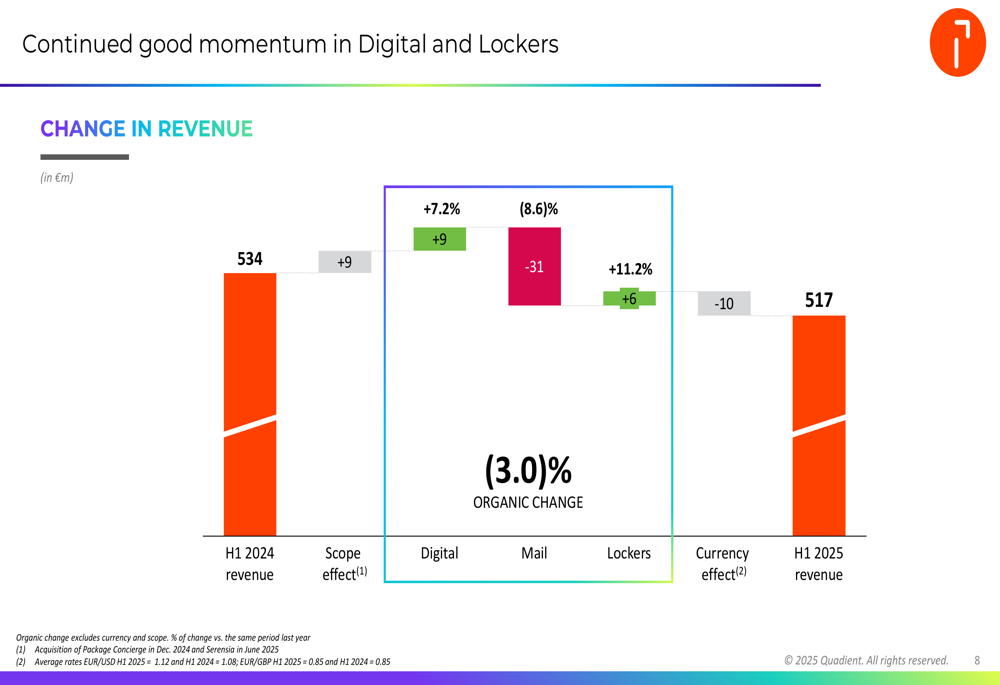

Quadient’s revenue decline was primarily driven by an 8.6% organic decrease in the Mail segment, partially offset by 7.2% organic growth in Digital and 11.2% organic growth in Lockers. The following waterfall chart illustrates these changes:

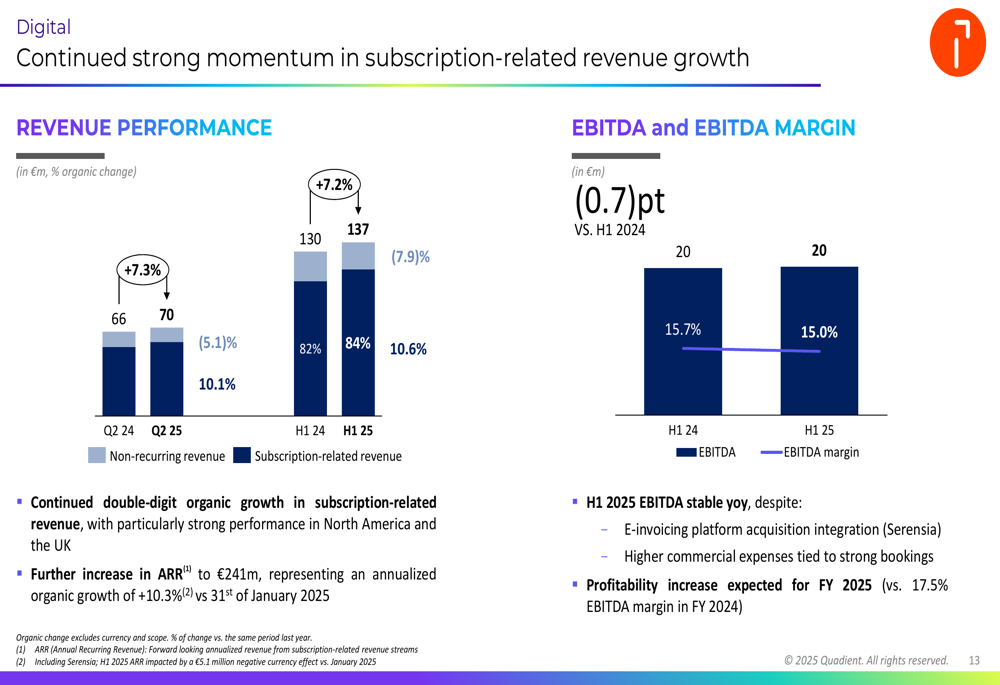

The Digital segment generated €137 million in revenue, with continued double-digit organic growth in subscription-related revenue. Annual Recurring Revenue (ARR) increased to €241 million. Despite integration costs for Serensia and higher commercial expenses, the segment maintained a stable EBITDA compared to the previous year, with profitability increases expected for the full year 2025.

The Digital segment’s performance is illustrated in the following chart:

The Mail segment, while declining as expected, maintained strong profitability with an EBITDA margin of 26.6%, up 0.8 percentage points despite the revenue decline. Hardware sales fell 17.5%, primarily due to lower product placements in the US. The company confirmed its 2030 expectations for this segment, projecting a continued decline in transaction mail volume (approximately -7% CAGR) and addressed mail market segment value (approximately -5% CAGR), with Quadient Mail revenue expected to reach around €600 million by 2030.

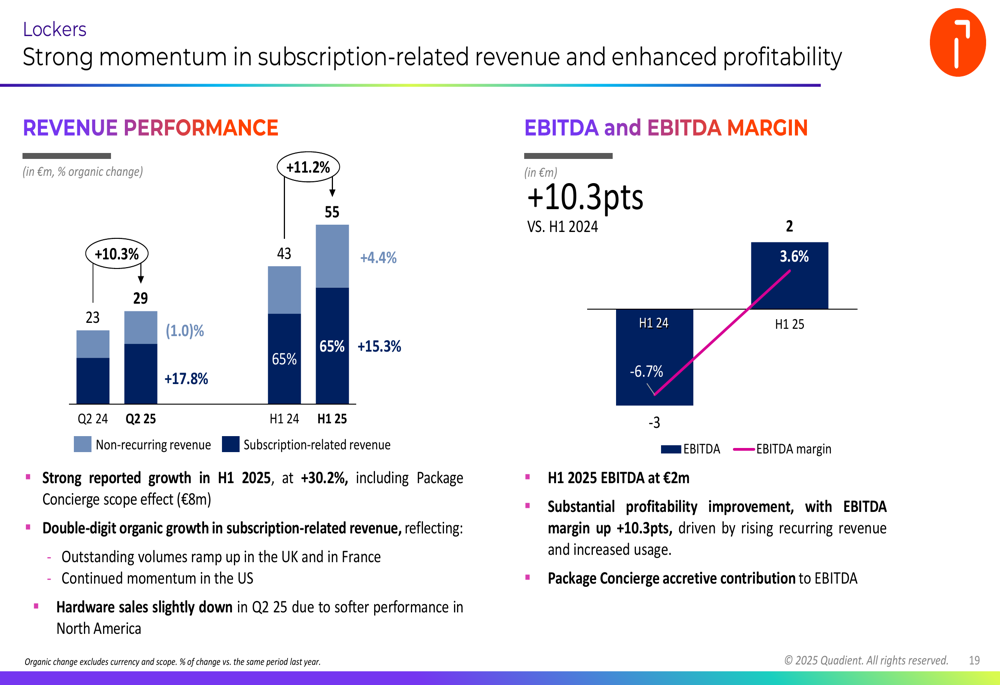

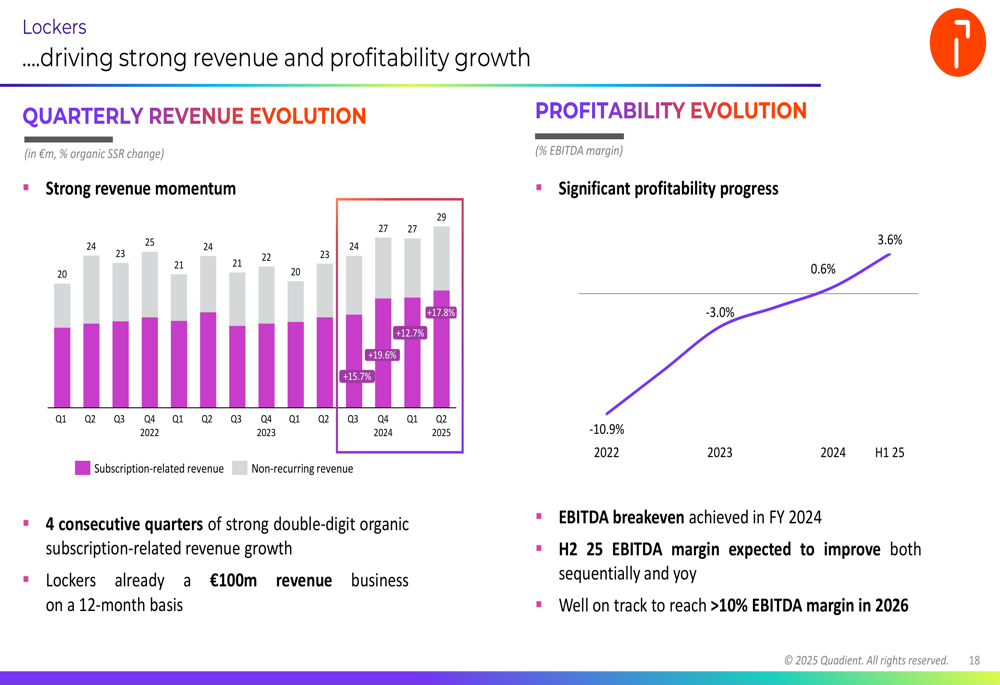

The Lockers segment showed the most dramatic improvement, with revenue increasing to €55 million and EBITDA reaching €2 million. The segment’s EBITDA margin improved by 10.3 percentage points, driven by rising recurring revenue and increased usage. The following chart demonstrates this strong performance:

Strategic Initiatives

Quadient’s Digital business continues to gain market recognition, with the company highlighted as a "Most Valuable Pioneer" in AI Maturity Matrix for CCM by QKS and maintaining leadership positions across multiple analyst reports. The Digital segment added 1,100 new customers in H1 2025, with strong cross-selling from Mail customers up by more than 30%.

A key strategic development was the successful testing of Quadient’s e-invoicing module with French tax authorities, with the platform already guaranteed to manage over 200 million invoices annually by 2026.

The Lockers business has seen accelerating momentum, particularly in the UK through alliances with Shell Service Stations and partnerships with The Range. The company added 1,100 lockers globally in H1 2025, bringing the total installed base to approximately 26,600 units. The European installed base has tripled over the past 18 months, with outstanding volume increases in both pick-up and drop-off services.

The following chart illustrates the rapid growth trajectory of the Lockers segment:

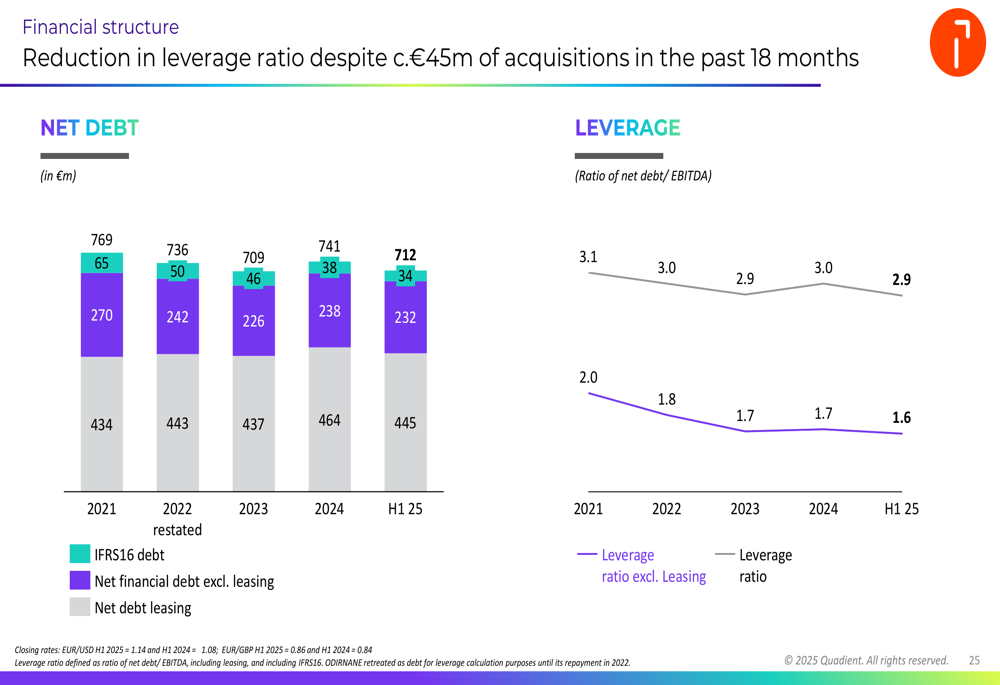

From a financial structure perspective, Quadient has continued to strengthen its balance sheet, with net debt decreasing to €712 million from a high of €769 million in 2021. The leverage ratio improved to 2.9x from 3.1x over the same period, as shown in this chart:

Forward-Looking Statements

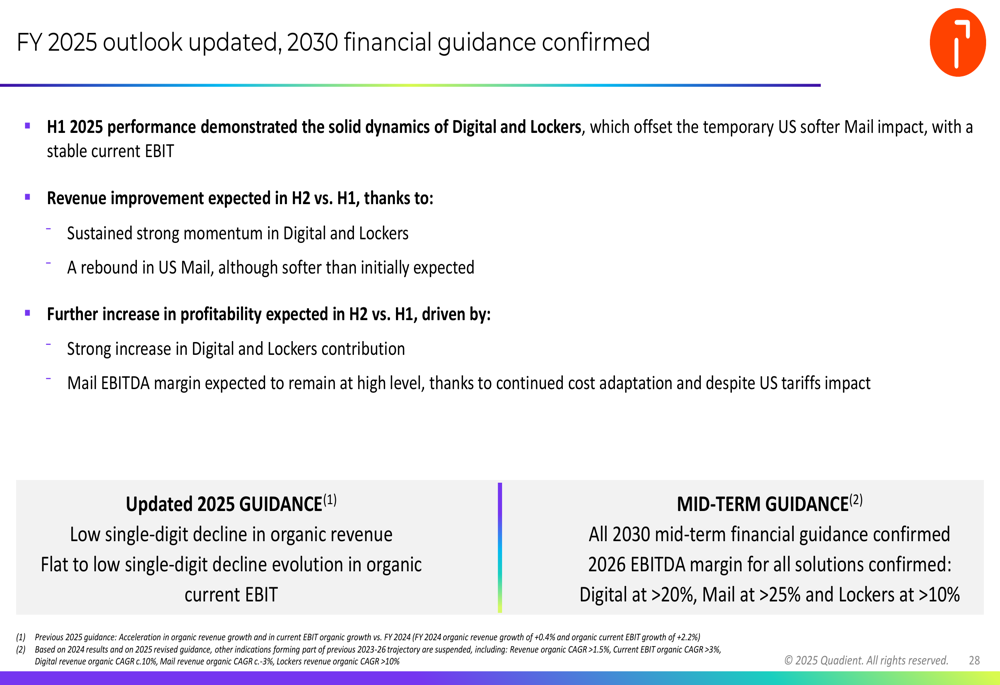

Based on its H1 2025 performance, Quadient has updated its guidance for the full year 2025, now expecting a low single-digit decline in organic revenue (previously expected to be flat to low single-digit growth) and a flat to low single-digit decline in organic current EBIT. The company anticipates revenue improvement in H2 compared to H1, with further increases in profitability.

Looking further ahead, Quadient confirmed its 2030 financial guidance, maintaining confidence in its long-term strategic direction despite near-term challenges. The company expects continued strong performance from its Digital and Lockers segments to increasingly offset the planned decline in its Mail business.

As illustrated in the outlook slide:

CEO Geoffrey Godet expressed confidence in the company’s trajectory, noting that H1 2025 performance demonstrated the solid dynamics of Digital and Lockers segments. The company expects a recovery in mail equipment renewals and continued momentum in its growth segments during the second half of the year.

While facing headwinds in the North American market and a challenging renewal cycle in mail equipment, Quadient’s strategic shift toward recurring revenue streams and growth in Digital and Lockers segments positions the company to navigate the current environment while building toward its 2030 vision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.