Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Quanterix Corporation (NASDAQ:QTRX) released its second quarter 2025 earnings presentation on August 7, revealing a significant revenue decline while emphasizing its strategic transformation and path to positive cash flow. The company’s stock closed at $5.51, down 1.78% on the day, reflecting continued investor concerns about its financial performance.

The biomarker detection company reported a 29% year-over-year revenue decline amid constrained biopharma budgets and ongoing integration of its recent Akoya acquisition. This follows a challenging first quarter where revenue fell 5% year-over-year, indicating an accelerating downward trend in the company’s top line.

Quarterly Performance Highlights

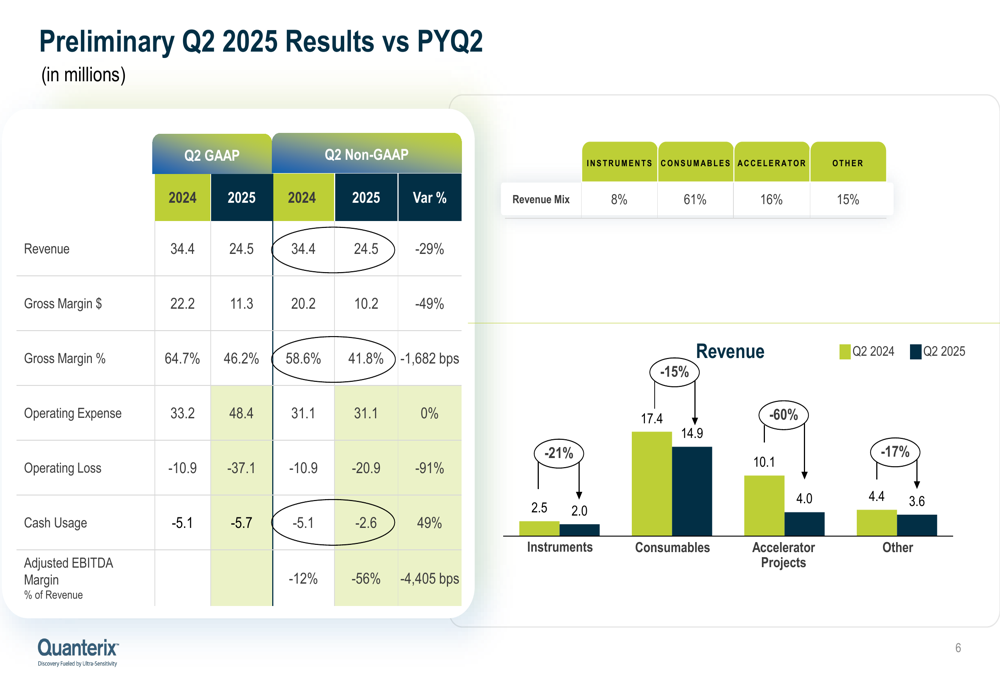

Quanterix reported Q2 2025 revenue of $24.5 million, a substantial 29% decrease from $34.4 million in the same period last year. This also represents a concerning 19% sequential decline from the $30.3 million reported in Q1 2025.

The company’s gross margin deteriorated significantly, falling to 46.2% from 64.7% in Q2 2024. On a non-GAAP basis, gross margin declined to 41.8% from 58.6% year-over-year. Operating loss widened to $37.1 million from $10.9 million in the prior year, while adjusted EBITDA margin plummeted to -56% from -12%.

As shown in the following financial results chart:

The revenue mix shows consumables continuing to dominate at 61% of total revenue, followed by accelerator services at 16%, other revenue at 15%, and instruments at just 8%. The company highlighted its "$100M high-margin consumables business" as showing resiliency despite end-market pressures.

Strategic Initiatives

Quanterix completed what it describes as a "transformative" acquisition of Akoya, positioning the company to offer protein biomarker measurements across both tissue and blood samples. Management emphasized that strategic investments in new assays, the Simoa One platform, and Alzheimer’s diagnostics are designed to drive long-term growth despite current financial challenges.

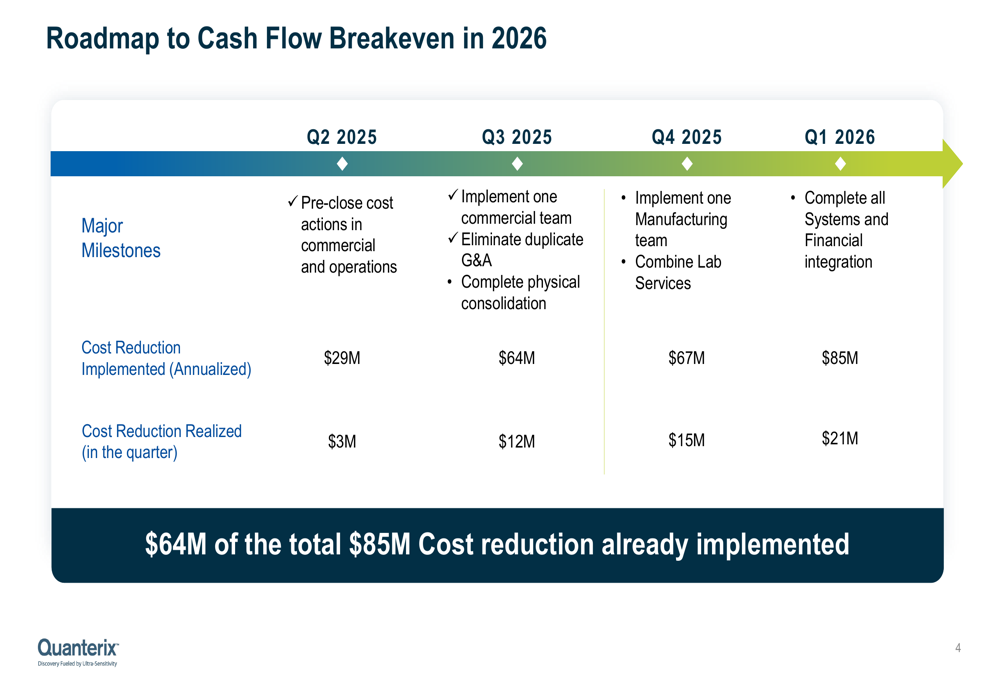

The company outlined an aggressive cost reduction plan targeting $85 million in synergies and expense reductions, with 75% of these cuts already implemented. This roadmap to cash flow breakeven in 2026 includes specific milestones across quarters:

The cost reduction plan shows an implementation schedule with $29 million implemented by Q2 2025, increasing to $64 million by Q3, $67 million by Q4, and the full $85 million by Q1 2026. This translates to quarterly cost savings of $3 million in Q2 2025, growing to $21 million by Q1 2026.

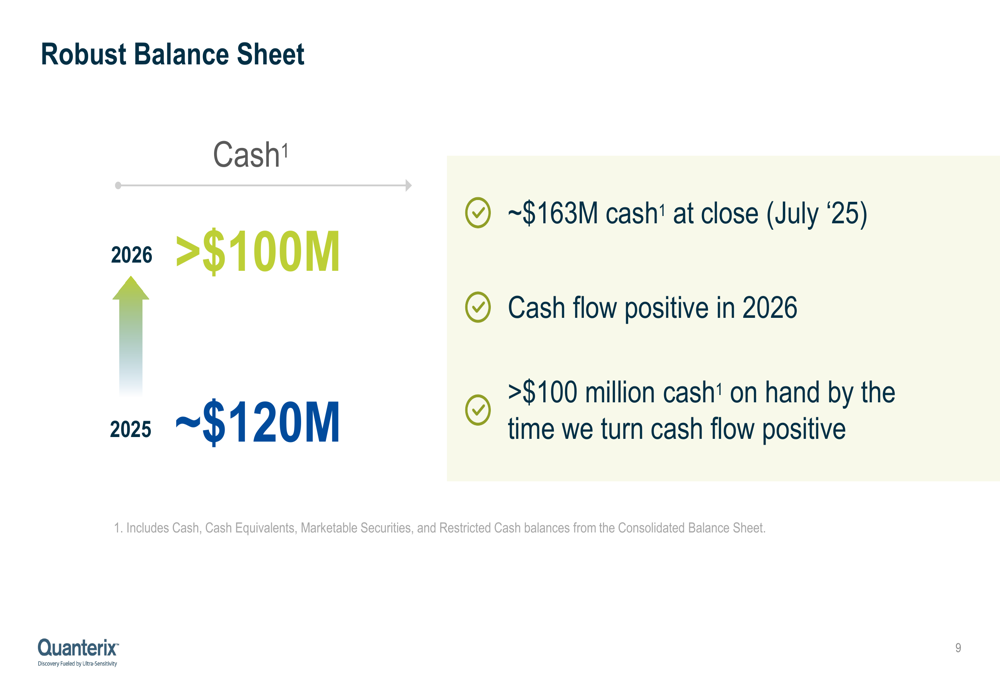

Despite current financial challenges, Quanterix maintains a strong balance sheet with approximately $163 million in cash as of July 2025, and expects to maintain over $100 million when it reaches cash flow positivity in 2026:

Alzheimer’s Testing Platform

A key growth driver for Quanterix is its Alzheimer’s disease testing infrastructure. The company’s LucentAD multi-marker test, which measures p-Tau217, Aβ42, Αβ40, NfL, and GFAP biomarkers, boasts 90% sensitivity, specificity, and accuracy with a low intermediate zone of approximately 11%.

The company is pursuing FDA approval with a single-site IVD submission anticipated by the end of 2025. On the reimbursement front, Quanterix has secured a PLA Code approval and expects Medicare pricing of approximately $897 per test in 2025.

The following slide illustrates the company’s progress in building its Alzheimer’s testing infrastructure:

Quanterix has expanded its lab-enabled partnerships, adding more than 20 partners to date, including 3 new ones in Q2 2025. The company has also secured regulatory approvals in international markets, including China NMPA approval for its pTau-217 Assay Kit on the HD-X platform and South Korea MFDS approval for HD-X.

Scientific Validation and Technology Adoption

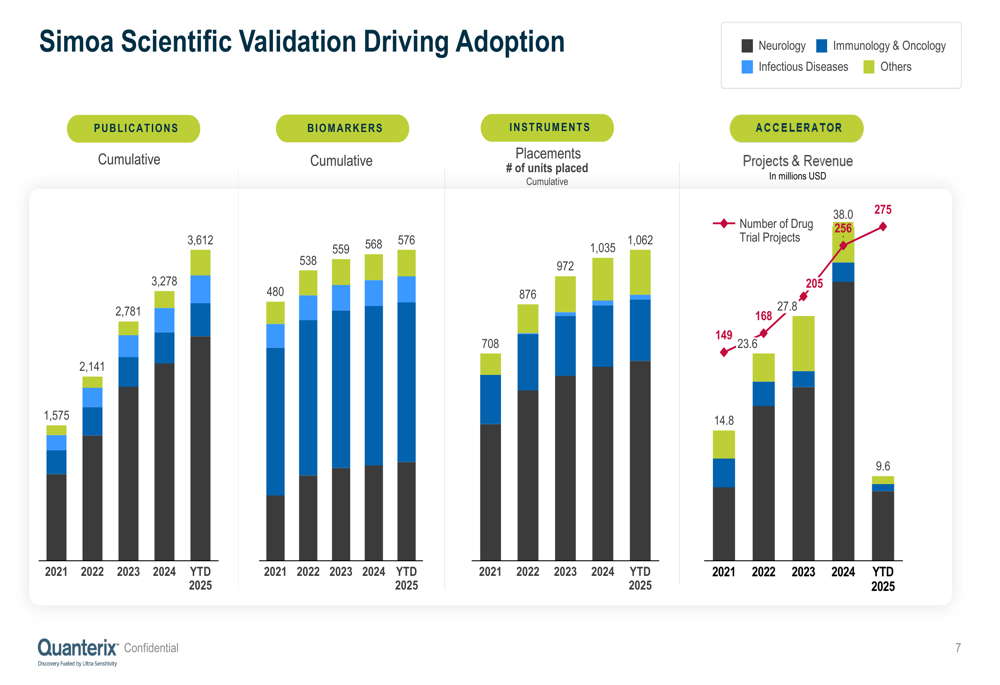

Despite financial headwinds, Quanterix continues to see growth in scientific validation metrics. The company’s Simoa technology has been featured in an increasing number of scientific publications, growing from 1,575 in 2021 to 3,612 year-to-date in 2025. Similarly, instrument placements have increased from 708 in 2021 to 1,062 currently.

The following chart illustrates these adoption trends:

While the number of accelerator projects has grown from 149 in 2021 to 275 year-to-date in 2025, revenue from this segment has declined, reflecting the company’s observation that constrained biopharma budgets are leading to smaller project sizes.

Forward-Looking Statements

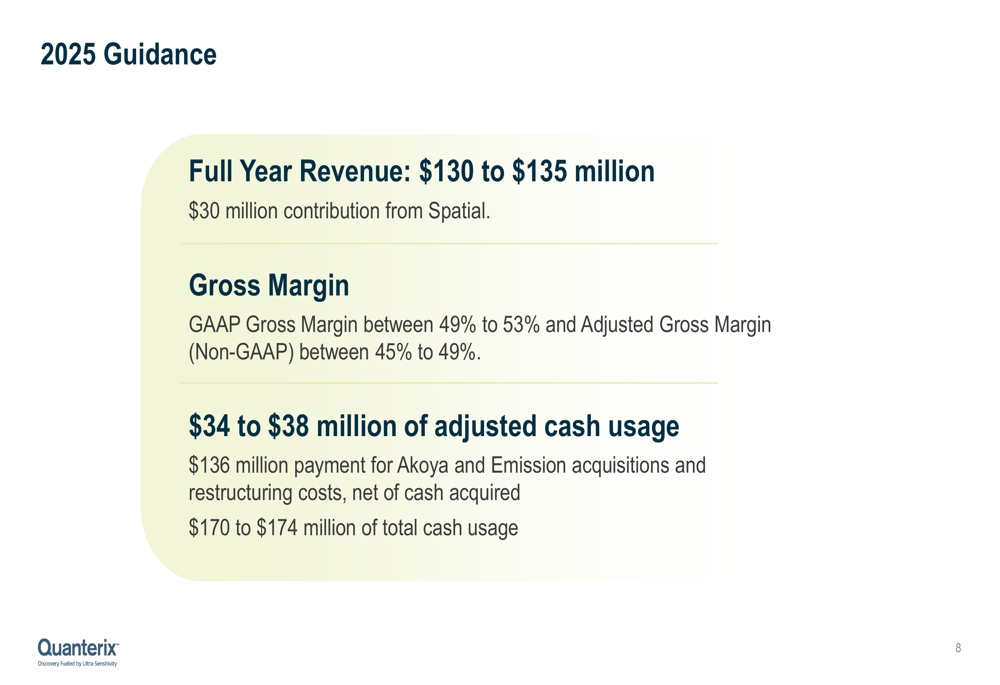

Quanterix provided full-year 2025 revenue guidance of $130 to $135 million, including a $30 million contribution from its Spatial business. This represents an increase from the $120-130 million guidance provided in Q1 2025, likely reflecting the inclusion of Akoya’s revenue contribution.

The company expects GAAP gross margin between 49% to 53% and adjusted gross margin between 45% to 49% for the full year. Cash usage is projected at $34 to $38 million on an adjusted basis, including the $136 million payment for Akoya and Emission acquisitions and restructuring costs, net of cash acquired.

Quanterix reaffirmed its target of achieving positive cash flow in 2026, with expectations of maintaining a cash balance exceeding $100 million by that time. This timeline aligns with the company’s cost reduction roadmap, which shows full implementation of $85 million in cost savings by Q1 2026.

Conclusion

Quanterix’s Q2 2025 results reveal a company in transition, facing significant revenue and margin pressures while simultaneously implementing strategic changes designed to position it for future growth. The 29% revenue decline and deteriorating margins highlight the challenges ahead, but management’s focus on cost reduction, the Akoya integration, and the promising Alzheimer’s testing market provide potential paths to recovery.

Investors will likely remain cautious given the accelerating revenue decline from Q1 to Q2 and the extended timeline to cash flow positivity. However, the company’s strong cash position, aggressive cost-cutting measures, and focus on high-value markets like Alzheimer’s diagnostics could provide the foundation for a turnaround if execution meets expectations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.