Bubble Wrap maker Sealed Air surges on report of buyout talks

Quest Diagnostics Incorporated (NYSE:DGX) delivered strong second-quarter results, reporting accelerating revenue growth and raising its full-year guidance, according to the company’s Q2 2025 presentation released on July 22.

The diagnostic testing leader reported total revenue of $2.76 billion, representing a 15.2% increase compared to the same period in 2024. Shares responded positively in premarket trading, rising 3.33% to $172.

Quarterly Performance Highlights

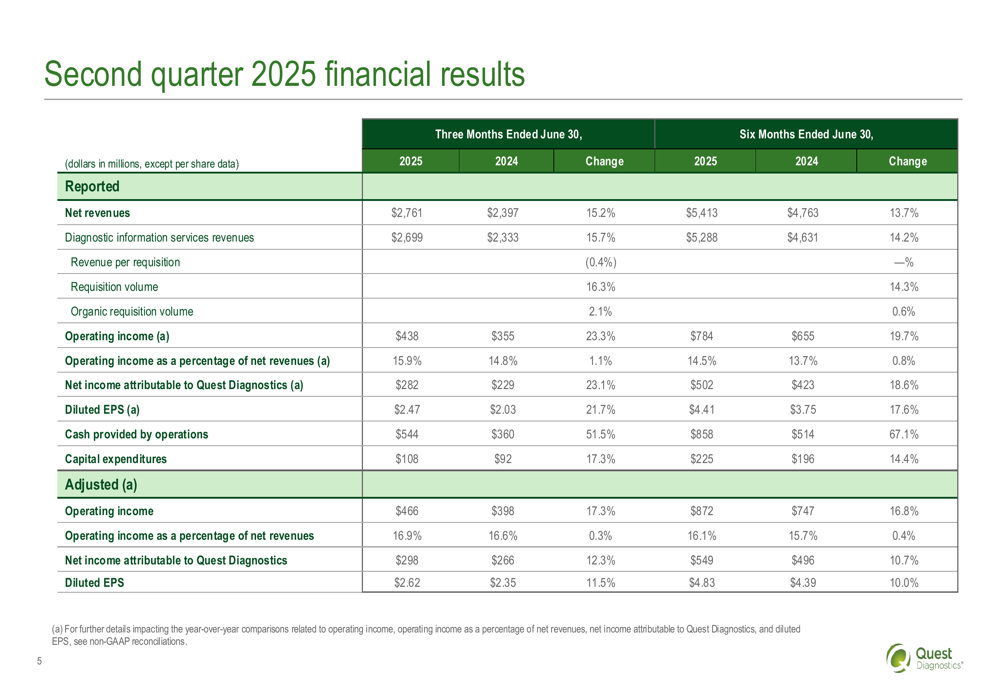

Quest reported adjusted diluted earnings per share of $2.62, up 11.5% from $2.35 in the prior-year period. Reported diluted EPS reached $2.47, marking a 21.7% increase. The company’s adjusted operating income margin stood at 16.9% of revenue.

"We had a strong second quarter, with revenues growing 15.2%, including 5.2% organic revenue growth, and adjusted EPS growth of 11.5%," said Jim Davis, Chairman, CEO, and President of Quest Diagnostics. "Our performance was driven by innovative clinical solutions, enterprise accounts, acquisitions, and automation and digital technologies."

The company highlighted several growth drivers, including its brain health offerings with the AD-Detect blood test for Alzheimer’s disease, promotional hormone testing, and digital health initiatives. Quest also noted it fulfilled its millionth customer order on questhealth.com during the quarter.

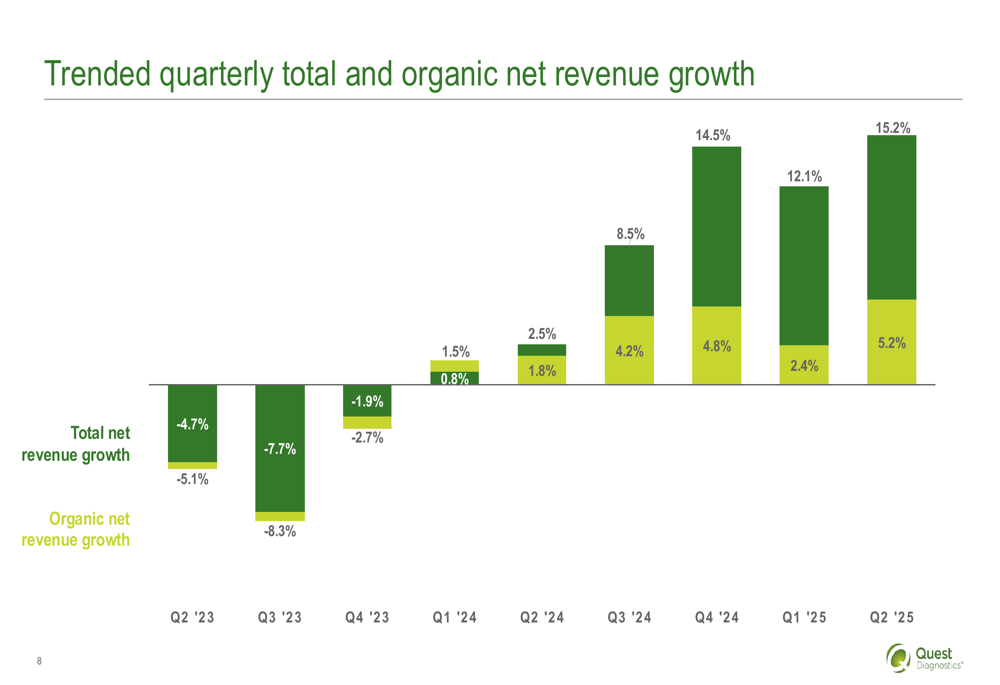

As shown in the following chart of quarterly revenue growth trends:

The second quarter’s 15.2% total revenue growth continues an upward trajectory that began in late 2023. More importantly, organic revenue growth accelerated to 5.2% in Q2 2025, up significantly from 2.4% in Q1 2025, suggesting strengthening underlying business momentum.

Detailed Financial Analysis

Quest’s Diagnostic Information Services (NASDAQ:III) revenues increased 15.7% to $2.70 billion in Q2 2025. Cash provided by operations surged 51.5% to $544 million, while capital expenditures increased 17.3% to $108 million.

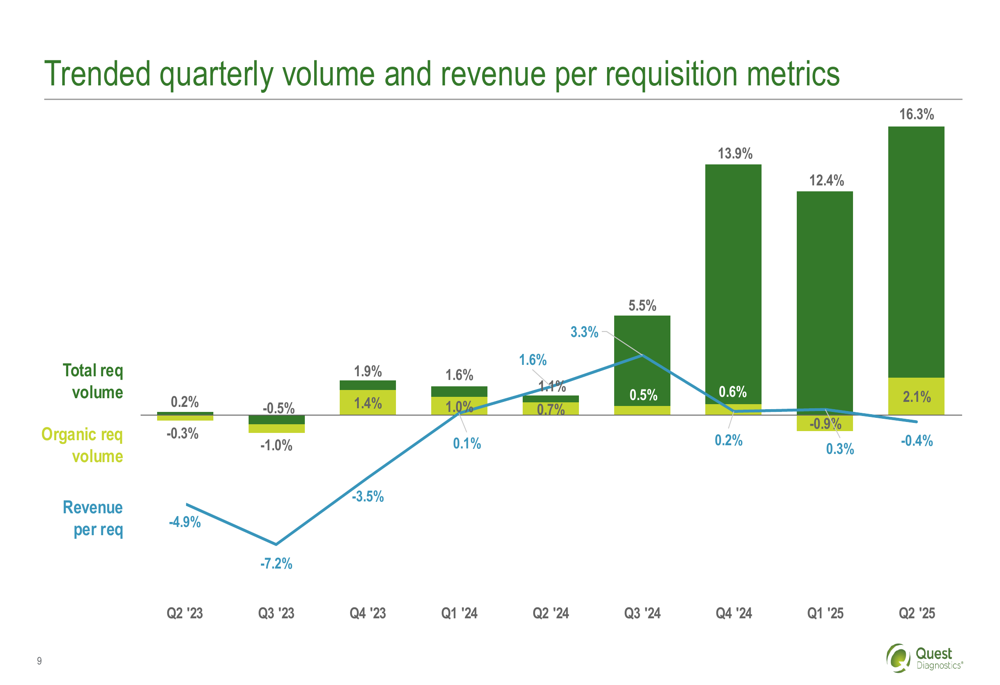

The company’s volume metrics showed strong growth, with total requisition volume up 16.3% and organic requisition volume increasing 2.1% year-over-year, as illustrated in this chart:

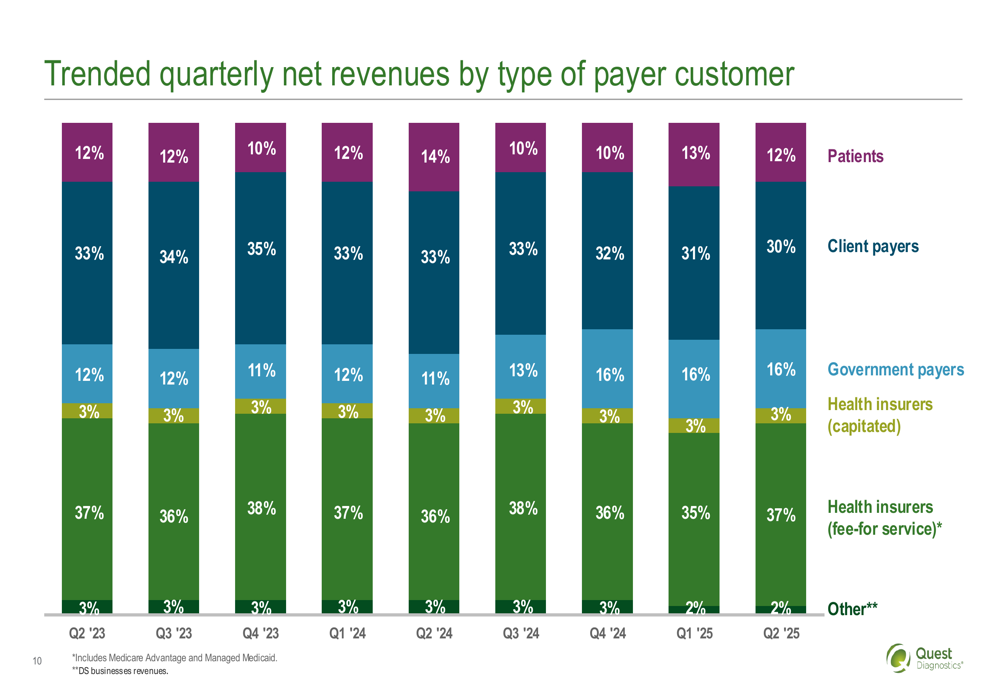

Revenue per requisition declined slightly by 0.4% in Q2, but this was more than offset by the strong volume growth. The company’s payer mix remained relatively stable, with fee-for-service health insurers accounting for 37% of revenues, followed by client payers at 30% and government payers at 16%.

The following breakdown shows Quest’s revenue distribution by payer type:

Quest’s financial results table provides a comprehensive view of the quarter’s performance:

Strategic Initiatives

Quest continues to execute on its strategic priorities, with acquisitions playing a significant role in the company’s growth. While organic growth accounted for 5.2% of the 15.2% total revenue increase, the remaining 10% came primarily from acquisitions.

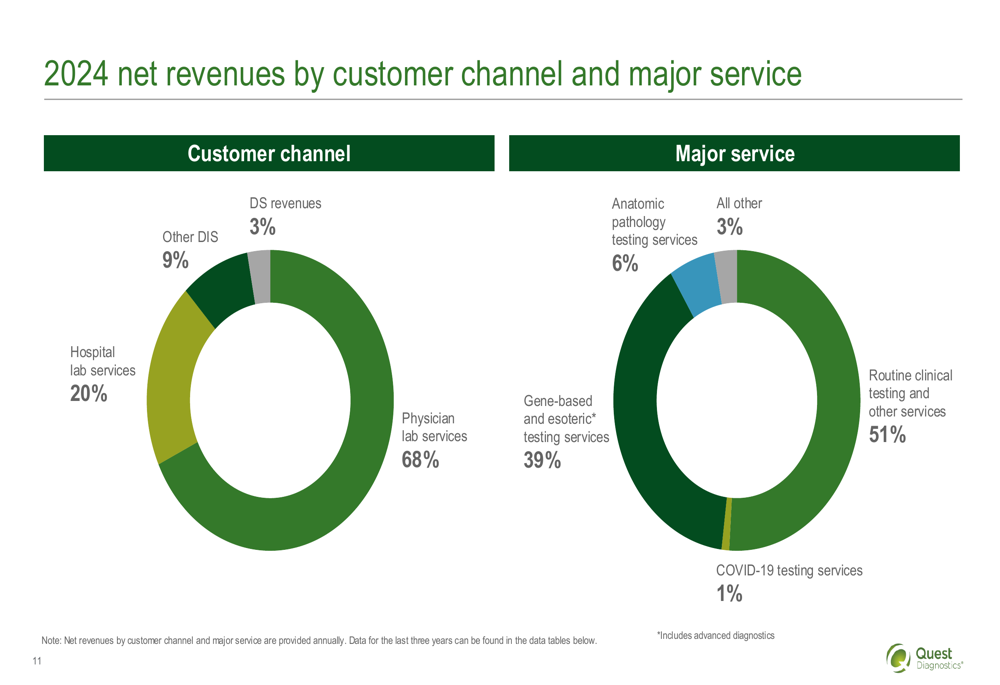

The company’s service mix reflects its focus on higher-value testing, with gene-based and esoteric testing services representing 39% of 2024 revenues, as shown in this breakdown:

Quest is also investing in Project Nova, which was mentioned in the underlying assumptions for full-year guidance. While specific details weren’t provided, this appears to be a strategic initiative that the company expects to support future growth.

Forward-Looking Statements

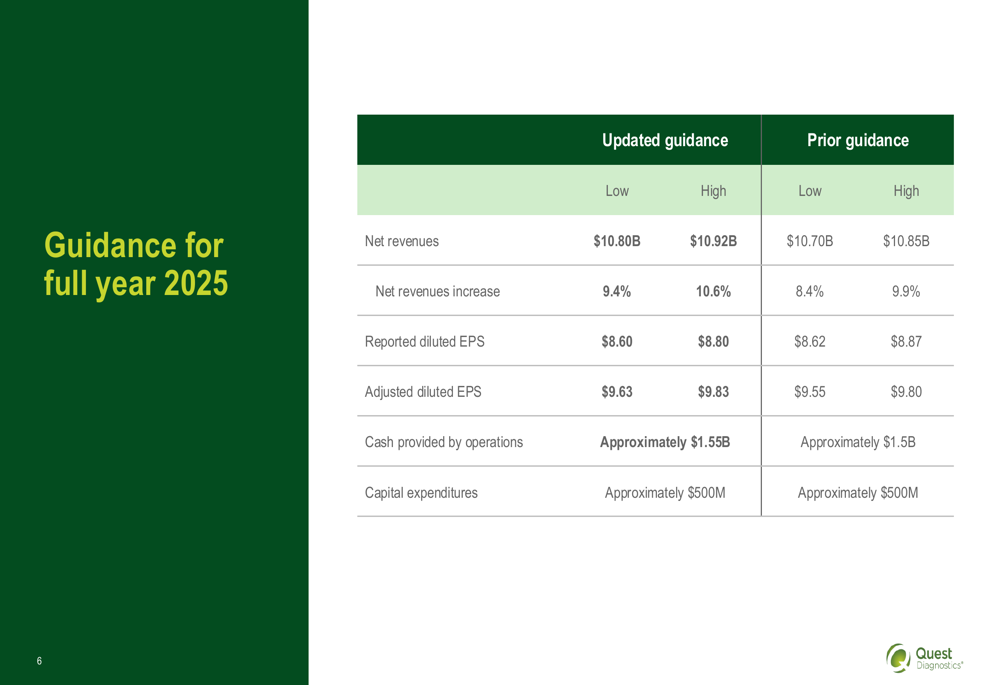

Based on its strong first-half performance, Quest raised its full-year 2025 guidance:

The updated revenue guidance of $10.80-$10.92 billion represents year-over-year growth of 9.4%-10.6%, up from the previous range of $10.70-$10.85 billion. Adjusted diluted EPS guidance was also raised to $9.63-$9.83, compared to prior guidance of $9.55-$9.80.

The company’s underlying assumptions for full-year 2025 guidance include:

- Approximately 3.5-4% organic revenue growth (up from 3% in previous guidance)

- Operating margin expansion versus the prior year

- Continued investments in Project Nova

- Ability (OTC:ABILF) to absorb the impact of tariffs

This outlook builds on the momentum seen in Q1 2025, when the company reported 12.1% revenue growth and exceeded analyst expectations with adjusted EPS of $2.21.

Quest’s consistent revenue growth trajectory and improving organic growth rate suggest the company’s strategic initiatives are gaining traction. With its strong market position serving 50% of US hospitals and physicians, Quest appears well-positioned to continue delivering on its financial targets for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.