106%+ returns, 97% win rate: A fresh list of AI-picked stock is out NOW

Introduction & Market Context

QuidelOrtho (NASDAQ:QDEL) presented its first quarter 2025 financial results on May 7, 2025, showcasing significant earnings growth despite revenue challenges. The diagnostic healthcare company’s stock jumped 7.5% in aftermarket trading, reaching $27.79 following the announcement, as investors responded positively to the substantial margin improvements and cost-cutting initiatives.

The company has faced headwinds in 2025, with its stock down 42% year-to-date prior to this earnings release. However, the Q1 results suggest QuidelOrtho’s operational efficiency strategies are beginning to yield tangible results, potentially marking a turning point for the company.

Quarterly Performance Highlights

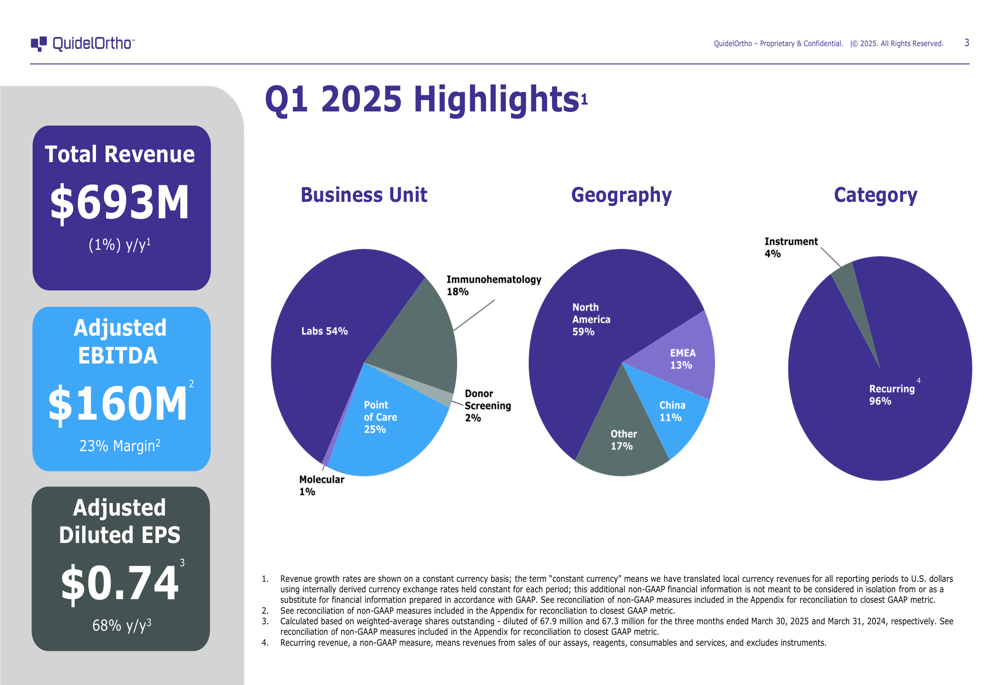

QuidelOrtho reported total revenue of $693 million for Q1 2025, representing a 1% year-over-year growth on a constant currency basis. While revenue remained relatively flat, the company delivered impressive bottom-line growth with adjusted diluted EPS of $0.74, a substantial 68% increase compared to Q1 2024.

As shown in the following quarterly highlights breakdown:

The company’s business remains diversified across multiple segments, with Labs comprising 54% of revenue, Point of Care at 25%, and Immunohematology at 18%. Geographically, North America continues to be the dominant market at 59% of revenue, followed by EMEA (13%), China (11%), and other regions (17%).

A key strength in QuidelOrtho’s business model is its recurring revenue stream, which accounts for 96% of total revenue, providing stability and predictability to the company’s financial performance.

Detailed Financial Analysis

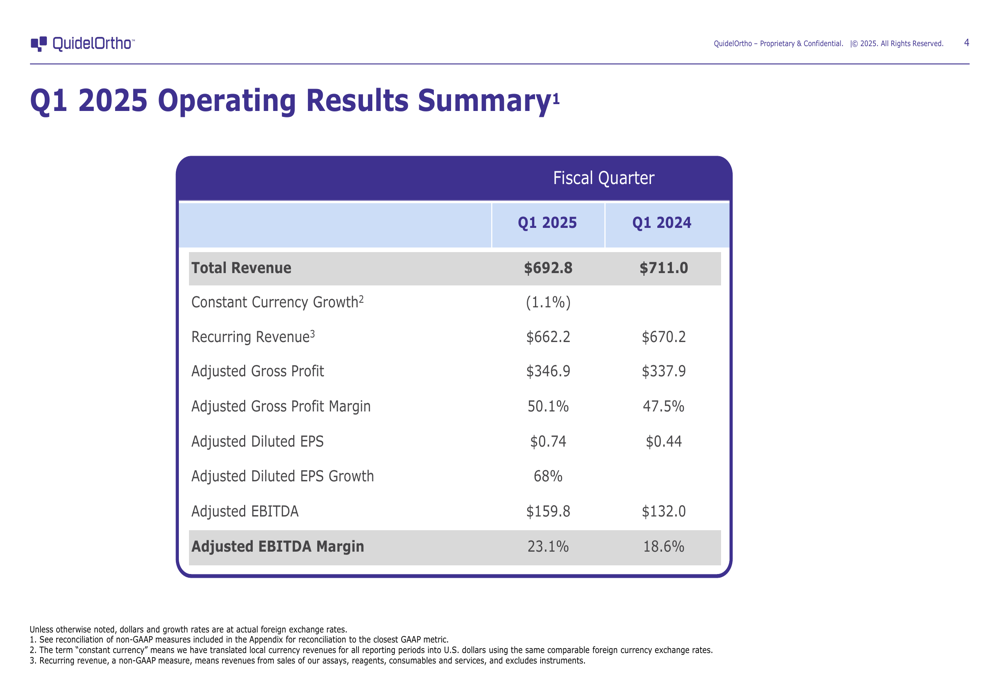

The company’s operating results show significant improvement in profitability metrics despite modest top-line performance. The detailed comparison between Q1 2025 and Q1 2024 reveals the extent of these improvements:

QuidelOrtho’s adjusted gross profit margin expanded from 47.5% to 50.1%, while adjusted EBITDA margin increased dramatically from 18.6% to 23.1%. This margin expansion drove adjusted EBITDA to $159.8 million, up from $132.0 million in the prior year period.

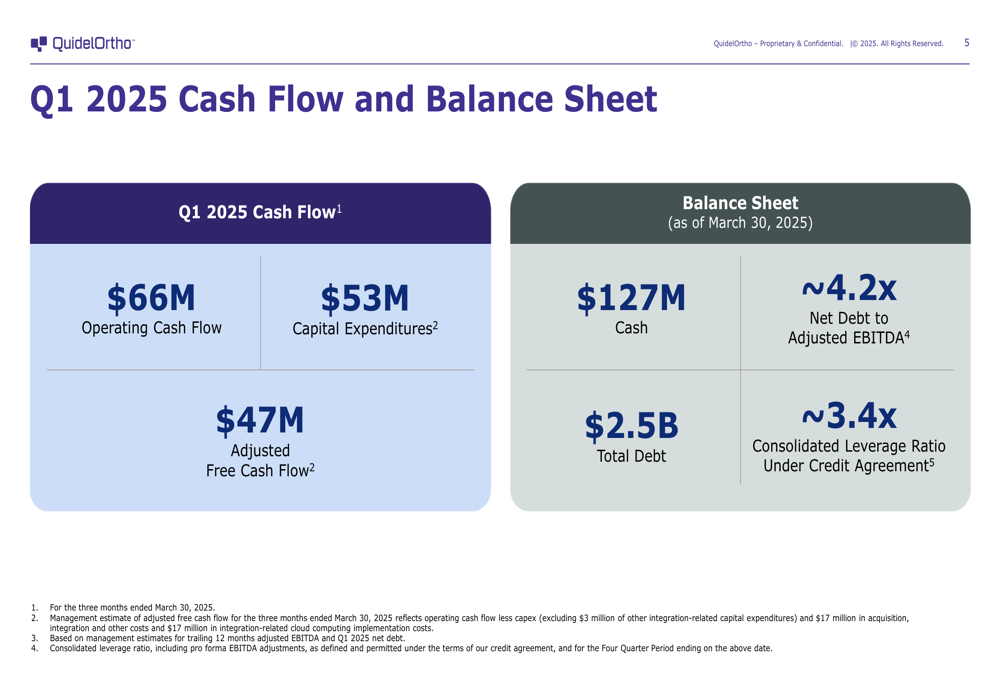

The company’s cash position and balance sheet metrics as of March 30, 2025, show:

With $127 million in cash and $2.5 billion in total debt, QuidelOrtho’s net debt to adjusted EBITDA ratio stands at approximately 4.2x. The company generated $66 million in operating cash flow during the quarter, with capital expenditures of $53 million, resulting in adjusted free cash flow of $47 million.

A closer examination of the revenue breakdown reveals mixed performance across business segments:

"Labs revenue increased from $356.9 million in Q1 2024 to $373.1 million in Q1 2025, while Donor Screening revenue declined significantly from $33.3 million to $12.8 million. Point of Care revenue also decreased from $186.6 million to $170.8 million, reflecting ongoing normalization of respiratory testing demand post-pandemic."

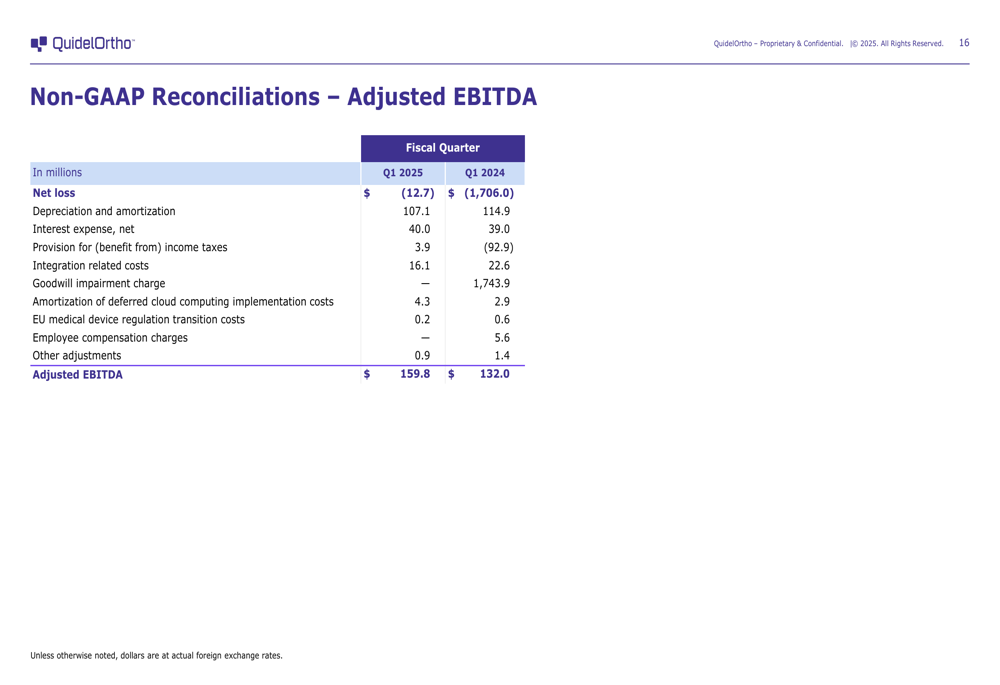

The reconciliation from net loss to adjusted EBITDA provides insight into the company’s profitability drivers:

Despite reporting a net loss of $12.7 million for Q1 2025 (compared to a substantial $1,706.0 million loss in Q1 2024 that included a goodwill impairment charge), QuidelOrtho achieved adjusted EBITDA of $159.8 million after accounting for depreciation, amortization, interest expenses, and integration-related costs.

Strategic Initiatives & Cost Savings

QuidelOrtho’s impressive margin expansion can be attributed to its aggressive cost-saving initiatives. The company reported achieving $50 million in cost savings during the first half of 2025, with an additional $30-$50 million expected throughout the remainder of the year.

These efficiency measures include operational streamlining, supply chain optimization, and integration synergies following the merger of Quidel Corporation and Ortho Clinical Diagnostics. The company has also successfully mitigated potential gross tariff impacts through strategic pricing and supply chain adjustments.

CEO Brian Blazer expressed satisfaction with the quarterly results, stating, "We are pleased with the strength of our first-quarter results," while CFO Joe Buske emphasized the company’s "focus on execution, commercial excellence, and cost savings initiatives."

Forward-Looking Statements

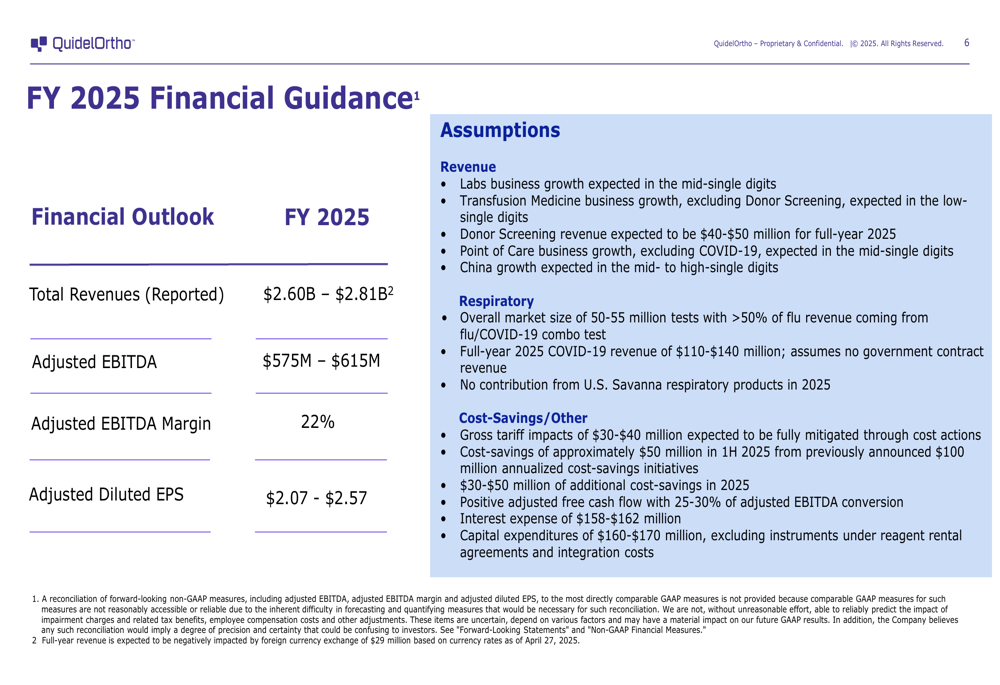

Looking ahead, QuidelOrtho provided the following financial guidance for fiscal year 2025:

The company expects total revenues between $2.60 billion and $2.81 billion, with adjusted EBITDA of $575-$615 million (approximately 22% margin) and adjusted diluted EPS of $2.07-$2.57.

Growth is anticipated across multiple business segments, with Labs and Point of Care (excluding COVID-19) projected to grow at mid-single-digit rates. China remains a key growth market, with expectations of mid- to high-single-digit expansion.

For its respiratory business, QuidelOrtho forecasts an overall market size of 50-55 million tests, with more than 50% of flu revenue coming from flu/COVID-19 combo tests. Full-year 2025 COVID-19 revenue is projected at $110-$140 million.

The company’s guidance aligns with analyst expectations, as InvestingPro forecasts EPS of $2.37 for FY2025, falling within QuidelOrtho’s projected range. Despite recent challenges, the strong Q1 performance and focused cost-saving initiatives suggest the company is well-positioned to meet its financial targets for the year, potentially reversing the negative stock performance trend seen in early 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.