Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Rackspace Technology (NASDAQ:RXT) presented its first quarter 2025 financial results on May 8, showing continued revenue challenges despite some year-over-year operational improvements. The multicloud technology solutions provider, which has been working on an operational turnaround, reported declining revenue in both its Private Cloud and Public Cloud segments compared to the previous year.

The company’s stock, which closed at $1.43 on the day of the announcement (up 0.7%), saw a 4.17% increase in after-hours trading to $1.50, suggesting investors found some positive elements in the mixed results. This reaction comes against the backdrop of significant stock momentum over the past year, with previous reports indicating a 120% return over the twelve months prior to Q3 2024.

Quarterly Performance Highlights

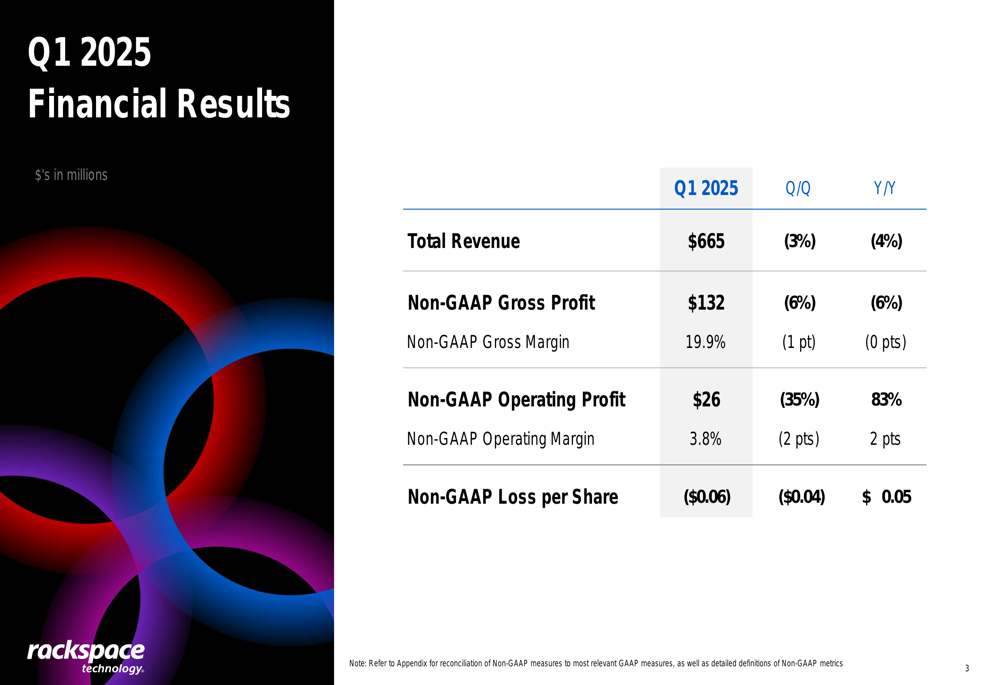

Rackspace reported total revenue of $665 million for Q1 2025, representing a 3% decrease quarter-over-quarter and a 4% decline year-over-year. The company’s Non-GAAP gross profit reached $132 million, down 6% both sequentially and compared to the same period last year, while maintaining a gross margin of 19.9%.

As shown in the following financial results summary:

Despite the revenue challenges, Rackspace’s Non-GAAP operating profit showed mixed results at $26 million – a significant 35% decline from the previous quarter but an impressive 83% improvement year-over-year. This suggests the company’s operational efficiency initiatives may be yielding results on an annual basis, even as quarterly performance fluctuates. The Non-GAAP operating margin stood at 3.8%, down 2 percentage points quarter-over-quarter but up 2 percentage points year-over-year.

The company reported a Non-GAAP loss per share of ($0.06), which represents a deterioration from both the previous quarter’s ($0.04) and the year-ago quarter’s positive $0.05 per share.

Segment Analysis

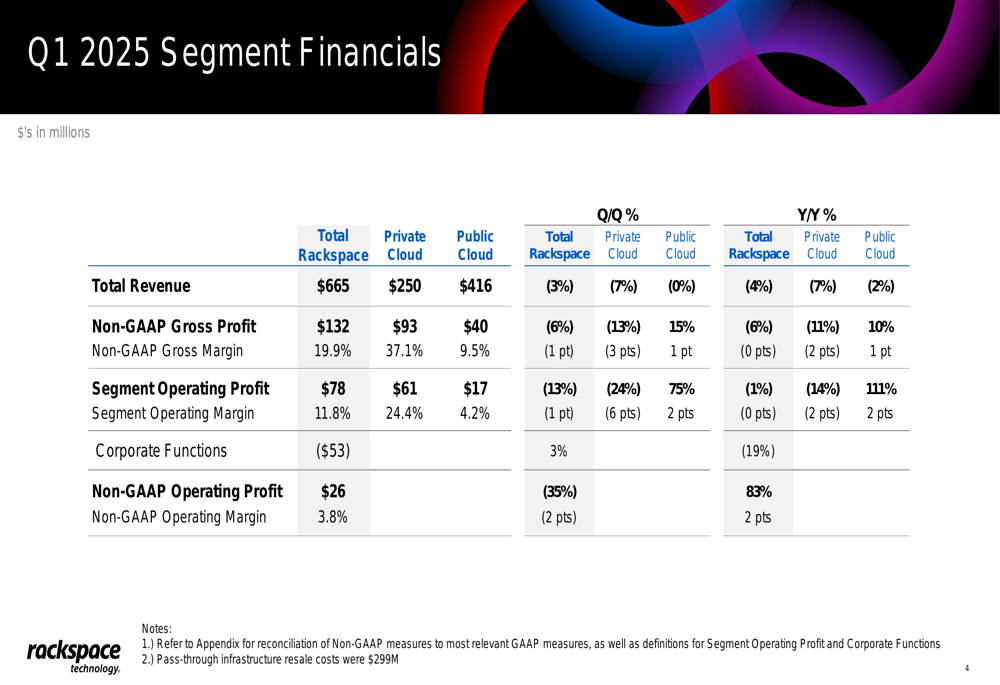

Rackspace’s business performance varied significantly between its two main segments. The company’s detailed segment breakdown reveals the specific challenges and bright spots:

The Private Cloud segment, which accounted for approximately 38% of total revenue, generated $250 million in Q1 2025, declining 7% both quarter-over-quarter and year-over-year. This segment maintained a relatively high Non-GAAP gross margin of 37.1%, though this represented a decline from previous periods. The segment operating profit for Private Cloud was $61 million, translating to a 24.4% operating margin.

In contrast, the Public Cloud segment showed more stability in revenue at $416 million, flat quarter-over-quarter but down 2% year-over-year. Notably, this segment demonstrated improvement in profitability, with Non-GAAP gross profit increasing 15% quarter-over-quarter and 10% year-over-year, reaching $40 million with a 9.5% gross margin. The segment operating profit for Public Cloud was $17 million, resulting in a 4.2% operating margin.

These results appear somewhat at odds with previous communications, which had highlighted record bookings in Public Cloud and anticipated growth in the healthcare Private Cloud business. The presentation noted that pass-through infrastructure resale costs were $299 million, which represents a significant portion of the company’s revenue.

Cash Flow and Debt Position

Rackspace reported modest but positive cash flow metrics for the quarter, as illustrated in the following summary:

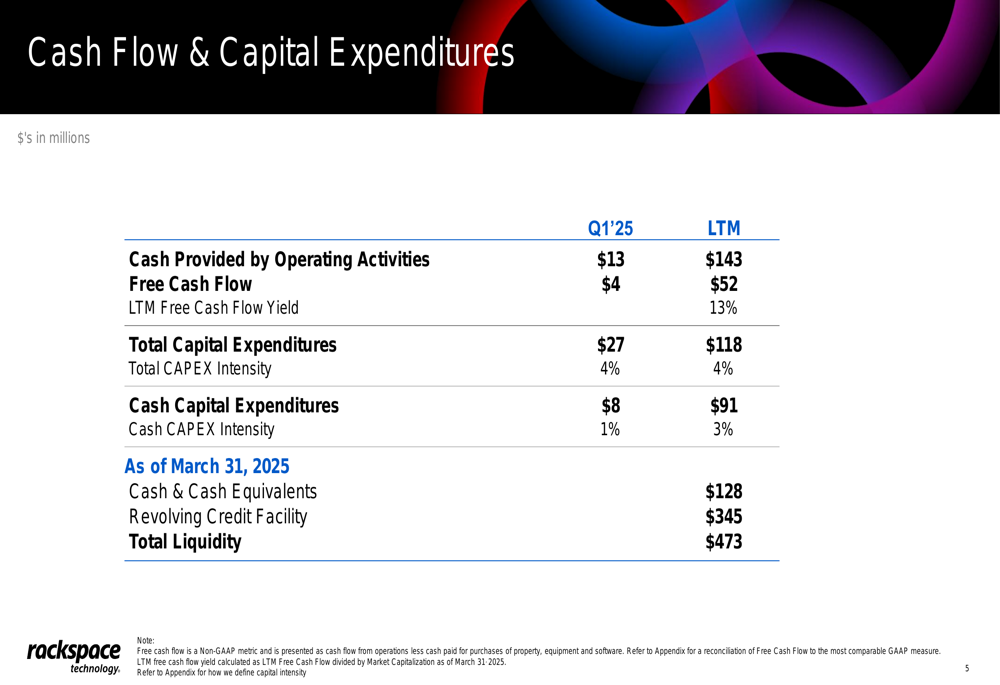

The company generated $13 million in cash from operating activities during Q1 2025 and $4 million in free cash flow. On a last-twelve-months basis, Rackspace produced $143 million from operations and $52 million in free cash flow, representing a 13% free cash flow yield. Total (EPA:TTEF) capital expenditures for the quarter were $27 million, with cash capital expenditures of $8 million.

As of March 31, 2025, Rackspace maintained $128 million in cash and cash equivalents, with $345 million available through its revolving credit facility, bringing total liquidity to $473 million.

The company’s debt structure, while substantial, appears manageable in the near term:

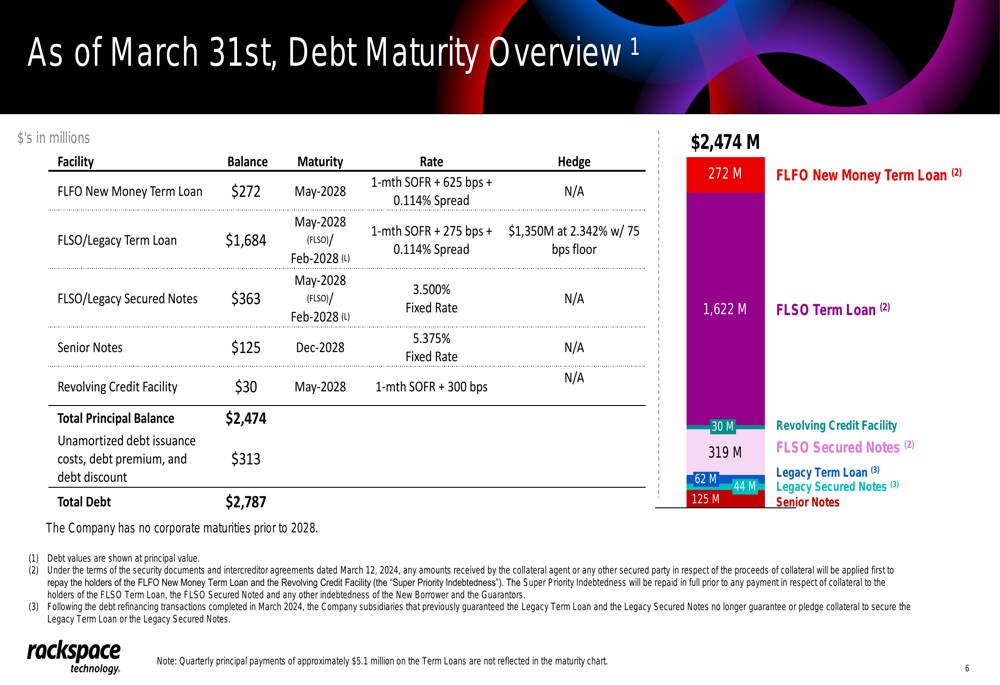

Rackspace’s total debt stood at $2.787 billion as of March 31, 2025. Importantly, the company has no corporate debt maturities prior to 2028, providing a runway of several years to improve operational performance before facing significant refinancing requirements. The debt consists primarily of term loans and secured notes, with the largest component being a $1.684 billion FLSO/Legacy Term Loan maturing in 2028.

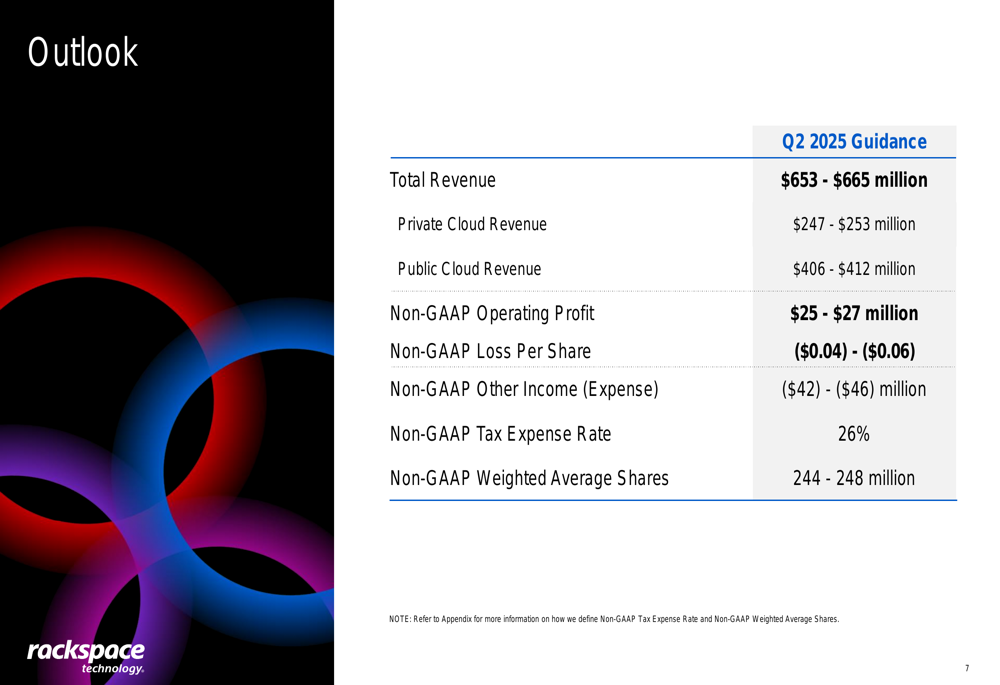

Forward Guidance and Outlook

Looking ahead to the second quarter of 2025, Rackspace provided the following guidance:

The company expects Q2 2025 total revenue between $653 million and $665 million, suggesting a potential further sequential decline from Q1 levels. This includes Private Cloud revenue of $247-253 million and Public Cloud revenue of $406-412 million.

Rackspace anticipates Non-GAAP operating profit of $25-27 million for Q2, roughly in line with Q1 results, and projects a Non-GAAP loss per share between ($0.04) and ($0.06). These projections indicate that while the company doesn’t expect immediate improvement in top-line performance, it aims to maintain its current level of operational profitability.

Based on previous communications, Rackspace has been focusing on high-growth verticals, particularly healthcare and banking/financial services, which were expected to account for approximately one-third of total revenue by the end of fiscal 2024. The company has also been developing AI initiatives, with nearly 50 customers reportedly engaged in AI projects as of late 2024.

While the Q1 2025 results present ongoing challenges, particularly in revenue growth, Rackspace’s year-over-year improvement in operating profit and positive free cash flow provide some foundation for the company’s continued transformation efforts. Investors will likely be watching closely to see if the company can stabilize revenue while continuing to enhance operational efficiency in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.