5 big analyst AI moves: Nvidia, AMD upgraded; ASML seen on €1,000 path

Introduction & Market Context

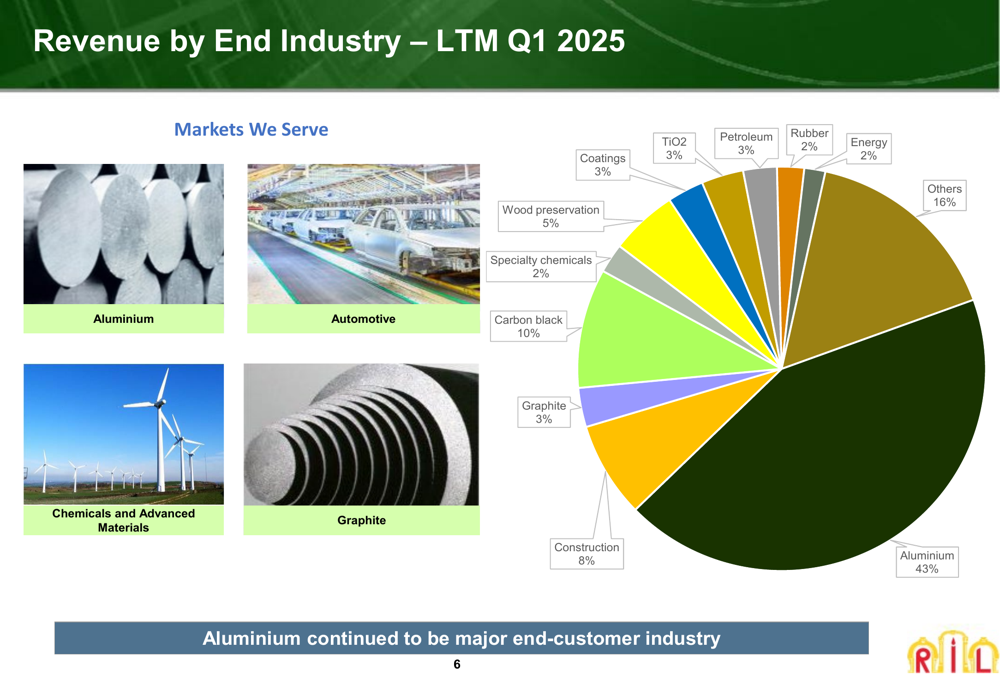

RAIN Industries Limited presented its Q1 2025 earnings results on May 8, 2025, highlighting mixed performance across its three business segments: Carbon, Advanced Materials, and Cement. The global producer of essential raw materials operates in a market environment where aluminum production continues to expand worldwide, with aluminum remaining the company’s primary end-customer industry at 43% of total revenue.

The company’s presentation noted that the aluminum 3-month LME price was trading around US$2,400 per tonne at the end of April 2025, providing a stable backdrop for its Carbon segment, which supplies critical materials to aluminum producers.

As shown in the following chart, aluminum production is growing globally, with both China and the rest of the world showing steady increases:

Quarterly Performance Highlights

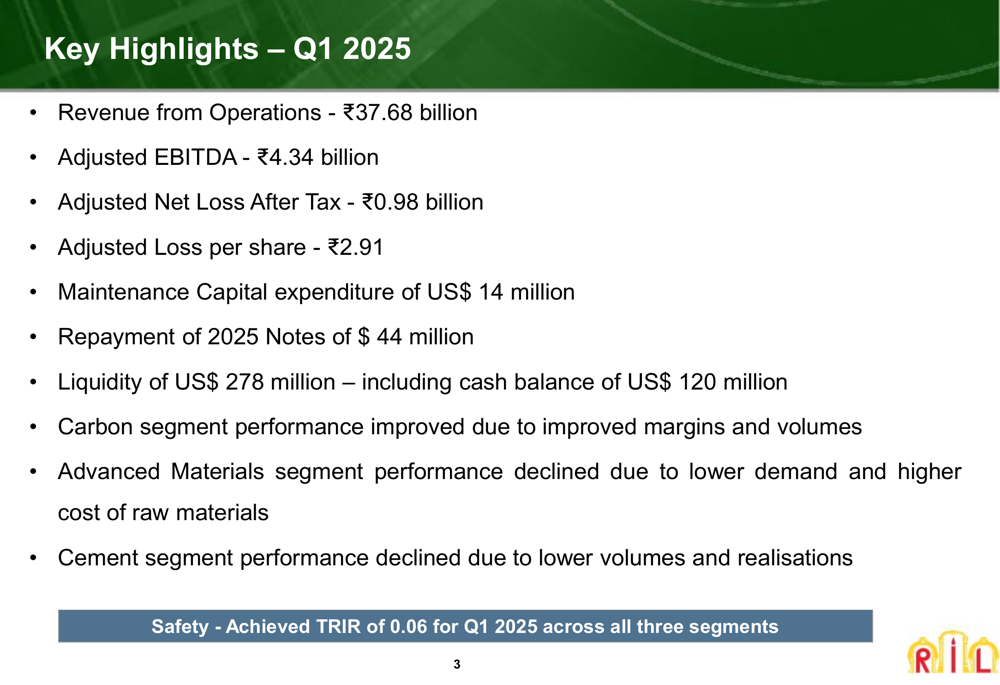

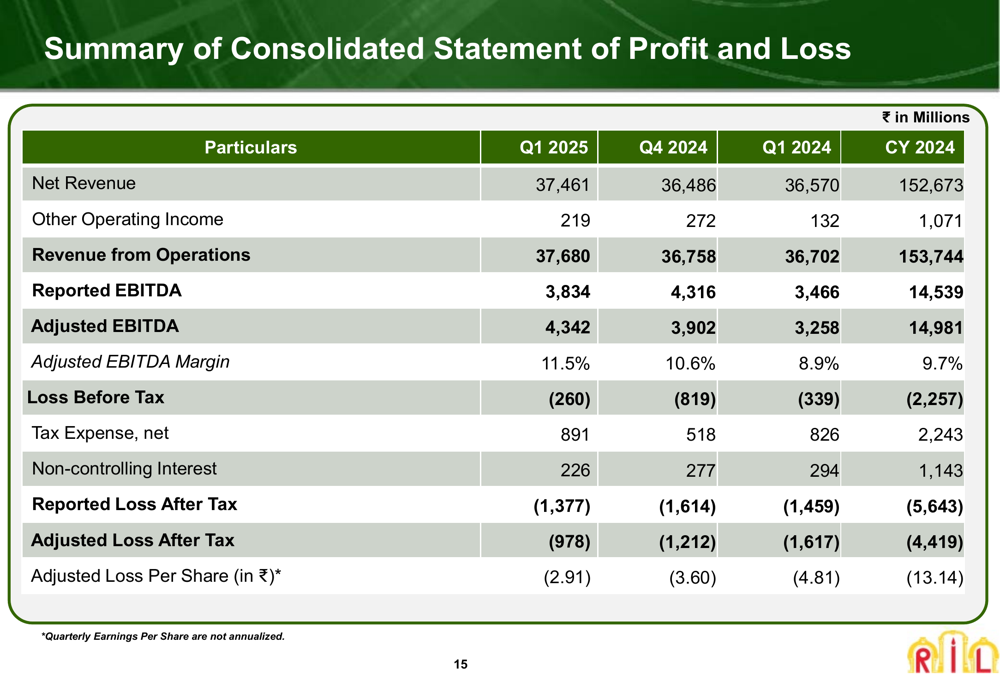

RAIN Industries reported revenue from operations of ₹37.68 billion for Q1 2025, with an adjusted EBITDA of ₹4.34 billion. Despite the improved EBITDA performance, the company still recorded an adjusted net loss after tax of ₹0.98 billion, translating to an adjusted loss per share of ₹2.91.

The company’s key financial metrics for the quarter show some improvement in operational performance despite continuing to operate at a loss:

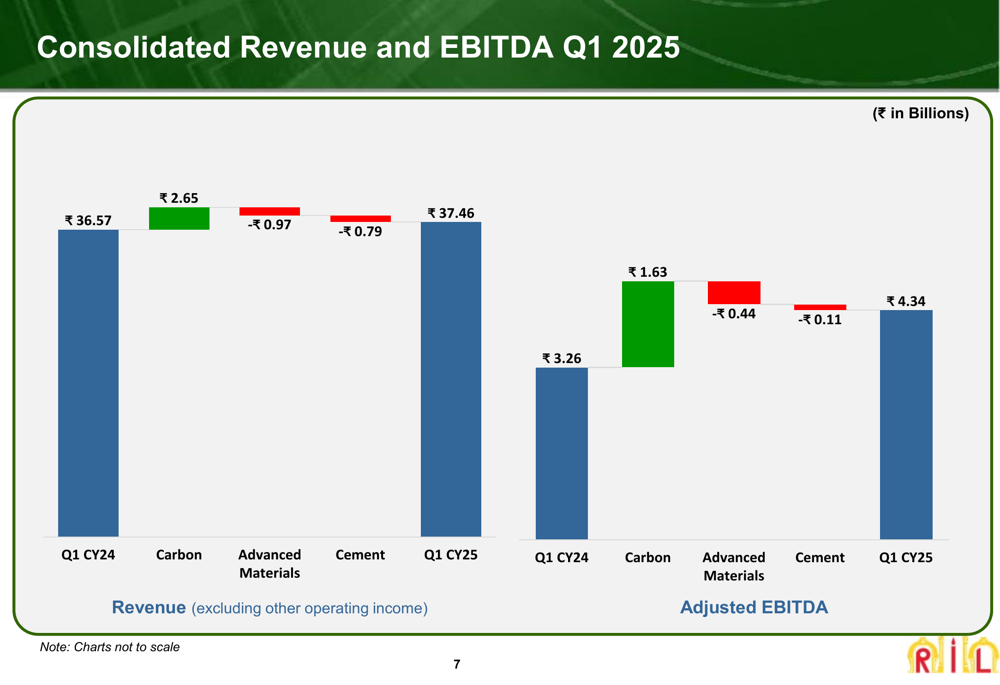

The consolidated financial results demonstrate year-over-year improvement in adjusted EBITDA, which increased from ₹3.26 billion in Q1 2024 to ₹4.34 billion in Q1 2025. This improvement was primarily driven by the strong performance of the Carbon segment:

Segment Analysis

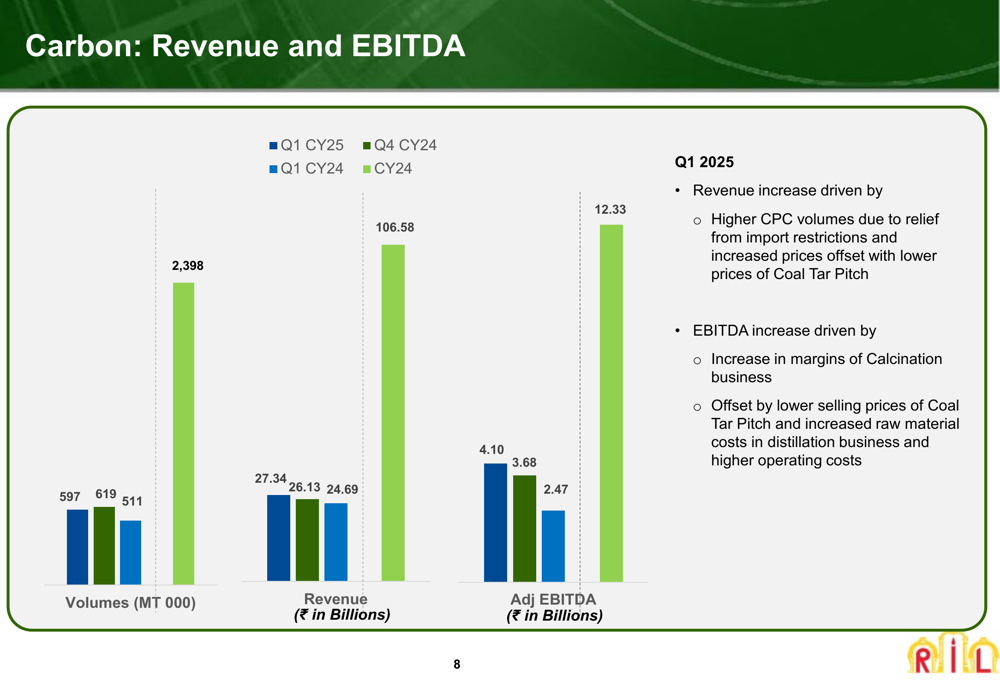

RAIN’s Carbon segment, which contributes the largest portion of revenue, showed significant improvement in Q1 2025. Revenue increased to ₹27.34 billion from ₹24.69 billion in Q1 2024, while adjusted EBITDA rose to ₹4.10 billion from ₹2.47 billion in the same period last year. This improvement was driven by higher CPC (Calcined Petroleum Coke) volumes and increased margins in the Calcination business.

The following chart illustrates the Carbon segment’s performance:

In contrast, the Advanced Materials segment experienced a decline in performance. Revenue decreased to ₹7.24 billion in Q1 2025 from ₹8.21 billion in Q1 2024, while adjusted EBITDA fell to ₹0.18 billion from ₹0.62 billion. This decline was attributed to decreased volumes from chemical intermediates and resins sub-segments due to lower demand, coupled with higher operational costs.

Similarly, the Cement segment also faced challenges, with revenue decreasing to ₹2.88 billion from ₹3.67 billion in Q1 2024. Adjusted EBITDA declined to ₹0.06 billion from ₹0.08 billion, primarily due to lower selling prices and reduced volumes.

The company’s revenue remains diversified across multiple end industries, though aluminum continues to be the dominant sector:

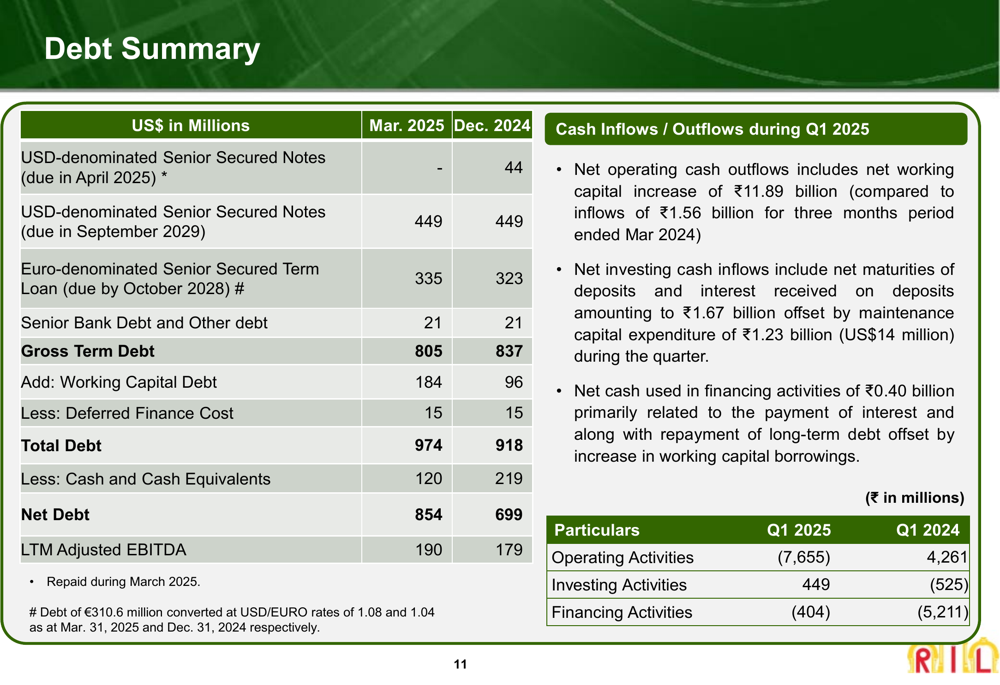

Debt Position and Liquidity

RAIN Industries’ debt position showed some changes during Q1 2025. The company repaid $44 million of its USD-denominated Senior Secured Notes due in April 2025. However, total debt increased to $974 million as of March 2025, up from $918 million in December 2024, primarily due to an increase in working capital debt.

Cash and cash equivalents decreased significantly to $120 million from $219 million at the end of 2024, resulting in net debt of $854 million, up from $699 million. The company maintained liquidity of US$278 million, including its cash balance.

The detailed debt summary provides insight into the company’s financial obligations:

The increase in net debt coupled with the reduction in cash reserves suggests potential liquidity challenges if the company cannot improve its cash flow generation. The presentation noted negative cash flow from operating activities of ₹7,655 million during Q1 2025, compared to a positive ₹4,261 million in the previous quarter.

Forward-Looking Statements

Looking ahead, RAIN Industries expects its Carbon segment to continue improving with increased capacity utilization and the re-introduction of Indian blending operations. However, the company also anticipates raw material constraints due to changing market dynamics.

Future strategies include enhancing research facilities in Canada and improving production facilities in Germany. The company has already proceeded with the repayment of its 2025 Senior Secured Notes, demonstrating a commitment to managing its debt obligations.

For the Cement segment, RAIN expects government investments to drive cement demand, potentially improving the segment’s performance in future quarters.

The company’s consolidated profit and loss statement provides a comprehensive view of its financial performance:

While RAIN Industries has shown improvement in its EBITDA performance, particularly in its Carbon segment, the company continues to face challenges in achieving profitability. The ongoing losses, increased debt levels, and negative operating cash flow in Q1 2025 highlight the difficulties ahead, even as the company implements strategic initiatives to improve its operational performance across all segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.