Gold prices edge higher on raised Fed rate cut hopes

Introduction & Market Context

Ralliant Corp (NYSE:RAL) presented its second quarter 2025 results on August 11, showcasing a company navigating challenging market conditions following its recent spin-off. The newly public entity, which operates as a diversified technology company, reported results that highlighted both segment-specific challenges and areas of resilience.

The company’s shares moved up 1.56% in after-hours trading to $45.70, despite reporting year-over-year declines in revenue and profitability, suggesting investors may have already priced in the challenges or were encouraged by sequential improvements and forward guidance.

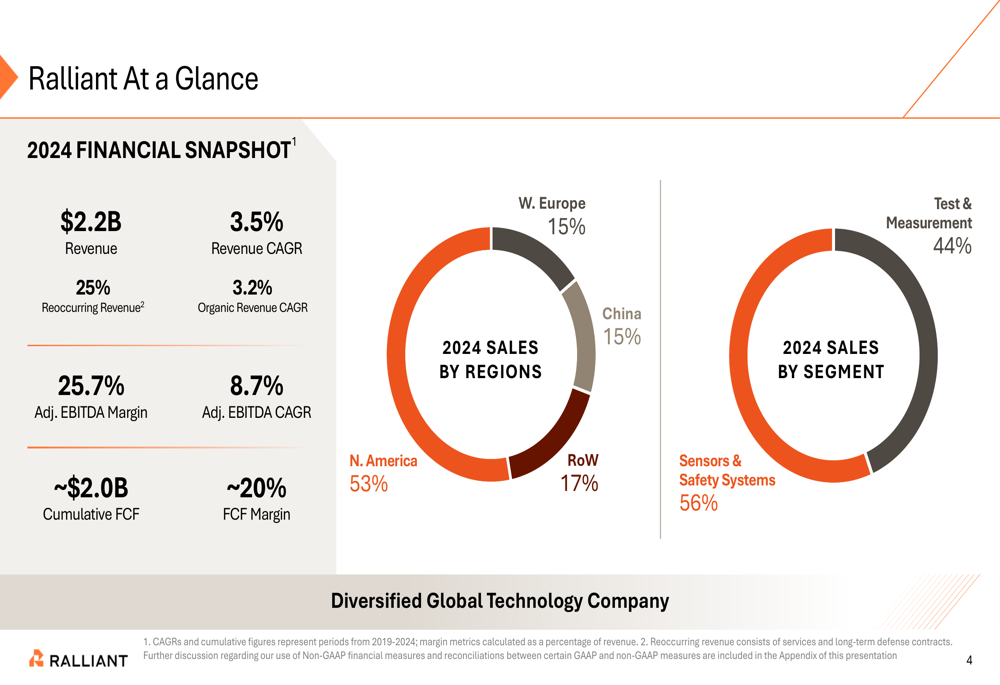

As shown in the following snapshot of Ralliant’s business composition:

Quarterly Performance Highlights

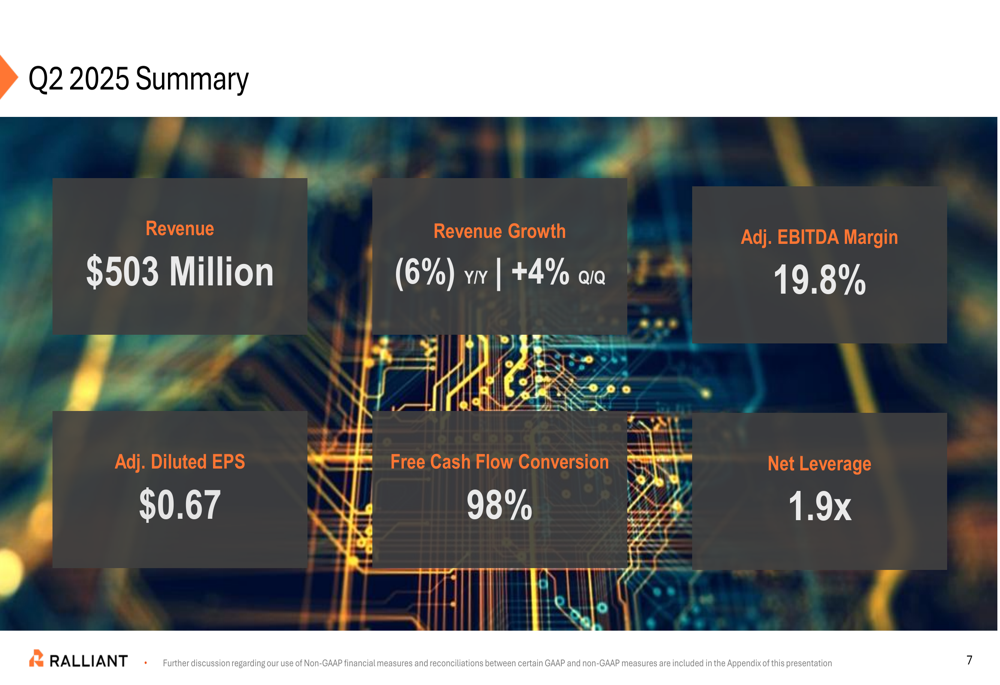

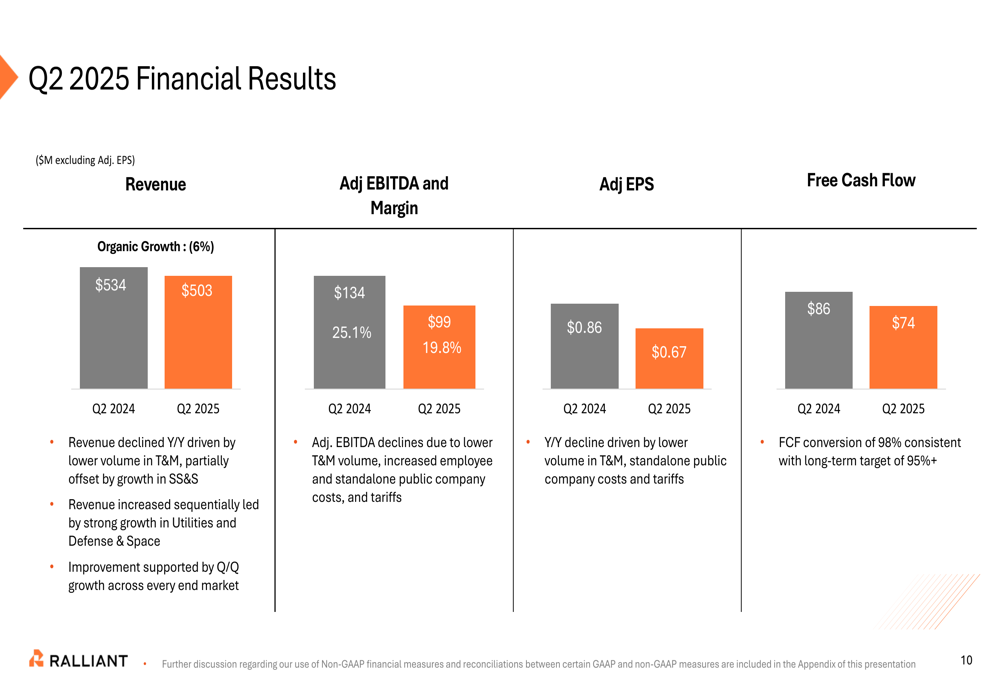

Ralliant reported Q2 2025 revenue of $503 million, representing a 6% year-over-year decline but a 4% sequential improvement from Q1. Adjusted EBITDA margin contracted to 19.8% from 25.1% in the prior-year period, while adjusted diluted EPS fell to $0.67 from $0.86 a year earlier.

Despite these challenges, the company maintained strong free cash flow conversion at 98%, consistent with its long-term target of 95%+, and reported a net leverage ratio of 1.9x.

The following summary highlights Ralliant’s key Q2 2025 metrics:

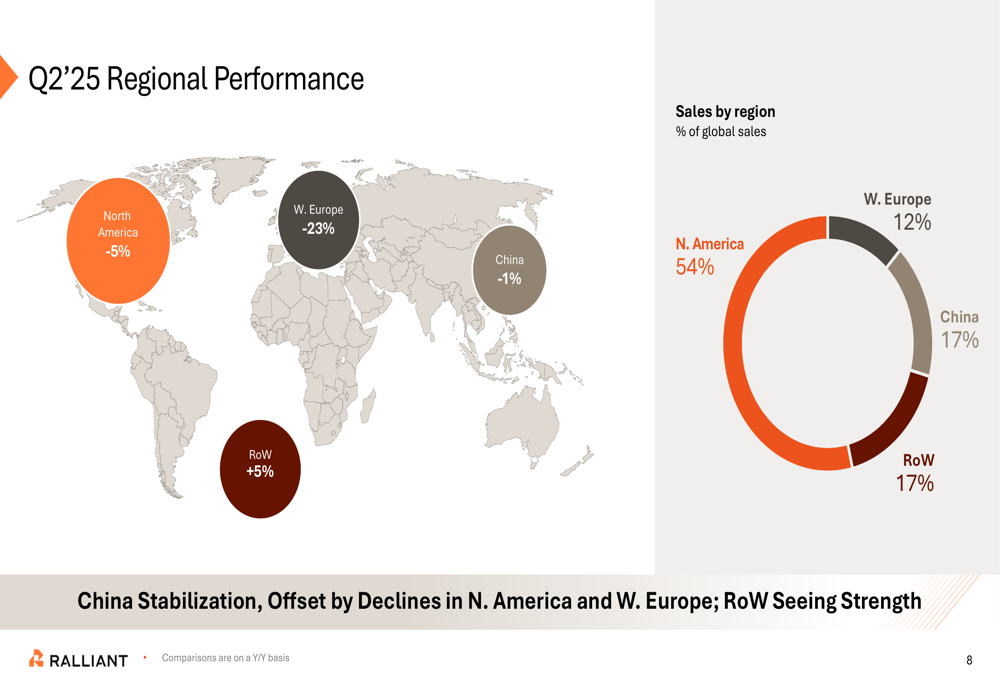

Regional performance varied significantly, with Western Europe showing the steepest decline at -23% year-over-year, while Rest of World markets grew 5%. North America, which represents 54% of sales, declined 5%, while China showed signs of stabilization with just a 1% decline.

This regional breakdown illustrates the geographic disparities in Ralliant’s performance:

Segment Analysis

Ralliant’s performance diverged significantly between its two main segments. The Sensors & Safety Systems segment, which accounts for 56% of 2024 revenue, demonstrated resilience with 1% total revenue growth and a 28.4% adjusted EBITDA margin, up from 27.5% in Q2 2024. This segment benefited from strong demand in utilities and defense & space markets.

In contrast, the Test & Measurement segment experienced substantial challenges, with revenue declining 15% year-over-year and adjusted EBITDA margin collapsing to 9.1% from 22.0% in the prior-year period. Management attributed this weakness to declining demand in automotive and EV batteries in Western Europe and mainland China, though noted sequential improvement in communications, diversified electronics, and semiconductor markets.

The following detailed financial results illustrate this segment divergence:

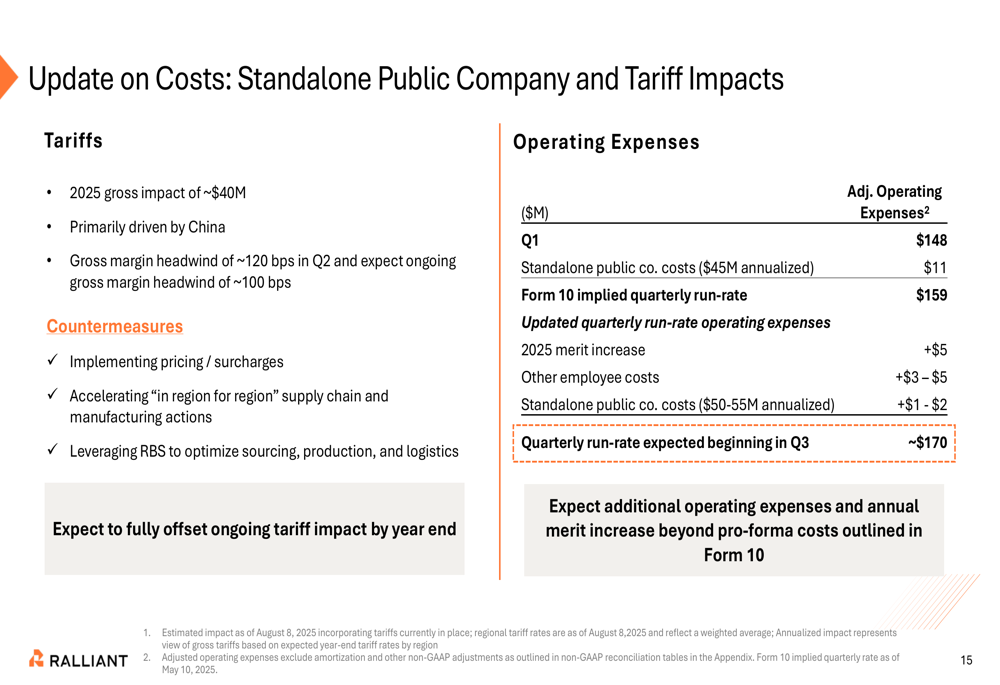

Cost Challenges and Countermeasures

Ralliant identified two significant cost pressures affecting its business: standalone public company costs and tariff impacts. The company expects tariffs to have a 2025 gross impact of approximately $40 million, creating a gross margin headwind of about 120 basis points in Q2.

To address these challenges, management announced a Cost Savings Program targeting $9-11 million in annualized savings, focused primarily on addressing spin-related dis-synergies in the Test & Measurement segment. The company expects to implement countermeasures including pricing adjustments, supply chain optimization, and accelerating "in region for region" sourcing to fully offset ongoing tariff impacts by year-end.

The following slide details these cost challenges and planned countermeasures:

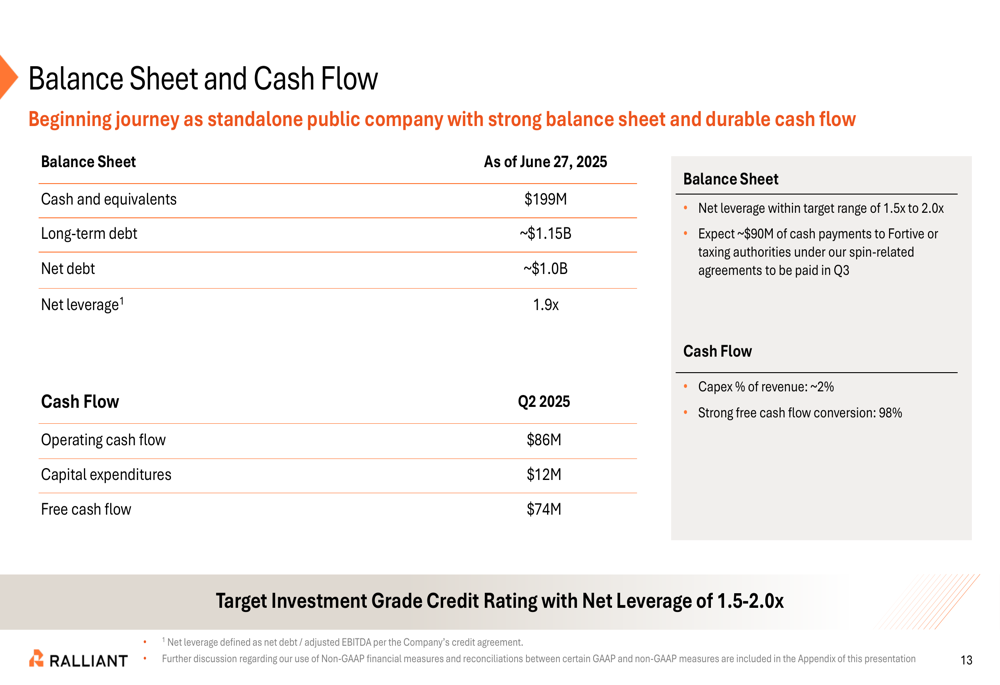

Ralliant’s balance sheet remains relatively strong, with $199 million in cash and equivalents, long-term debt of approximately $1.15 billion, and net leverage of 1.9x as of June 27, 2025. The company generated $86 million in operating cash flow and $74 million in free cash flow during Q2.

The following overview illustrates Ralliant’s financial position:

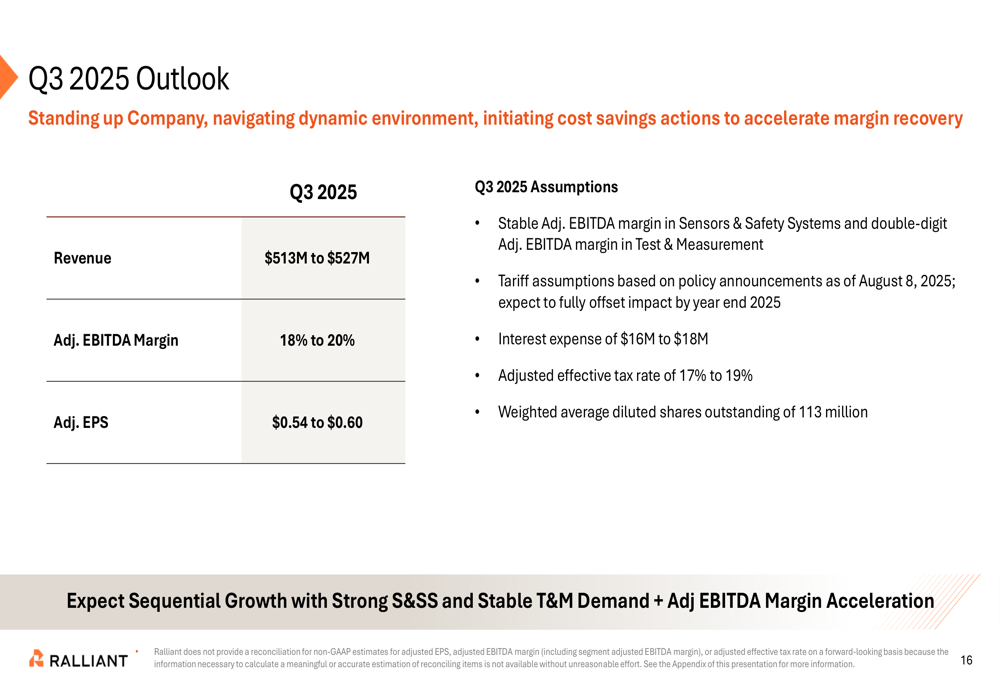

Forward Guidance and Strategic Initiatives

For Q3 2025, Ralliant provided guidance of $513-527 million in revenue, adjusted EBITDA margin of 18-20%, and adjusted EPS of $0.54-0.60. This outlook assumes sequential growth with continued strength in Sensors & Safety Systems and stabilization in Test & Measurement.

The company’s Q3 outlook and key assumptions are detailed here:

Ralliant’s capital allocation strategy focuses on three areas: organic reinvestment in high-growth markets, returning capital to shareholders, and pursuing strategic tuck-in acquisitions. The company recently announced a share repurchase authorization of up to $200 million and declared a quarterly dividend of $0.05 per share.

Management emphasized its focus on executing a profitable growth strategy through the Ralliant Business System (RBS (LON:NWG)), leveraging stronghold positions in key markets, and pursuing growth vectors in grid modernization, defense technologies, and power electronics. For the Test & Measurement segment specifically, the company outlined a recovery plan that includes new product introductions and targeted cost savings.

"We are executing our strategy focused on stronghold positions and high-growth vectors for enduring customer value," said Tami Newcombe, President and CEO of Ralliant, highlighting the company’s focus on innovation despite current market challenges.

While Ralliant faces significant headwinds, particularly in its Test & Measurement segment, management expressed confidence in gradual sequential improvement through the second half of 2025, supported by its cost-saving initiatives and strategic focus on higher-growth markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.