Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

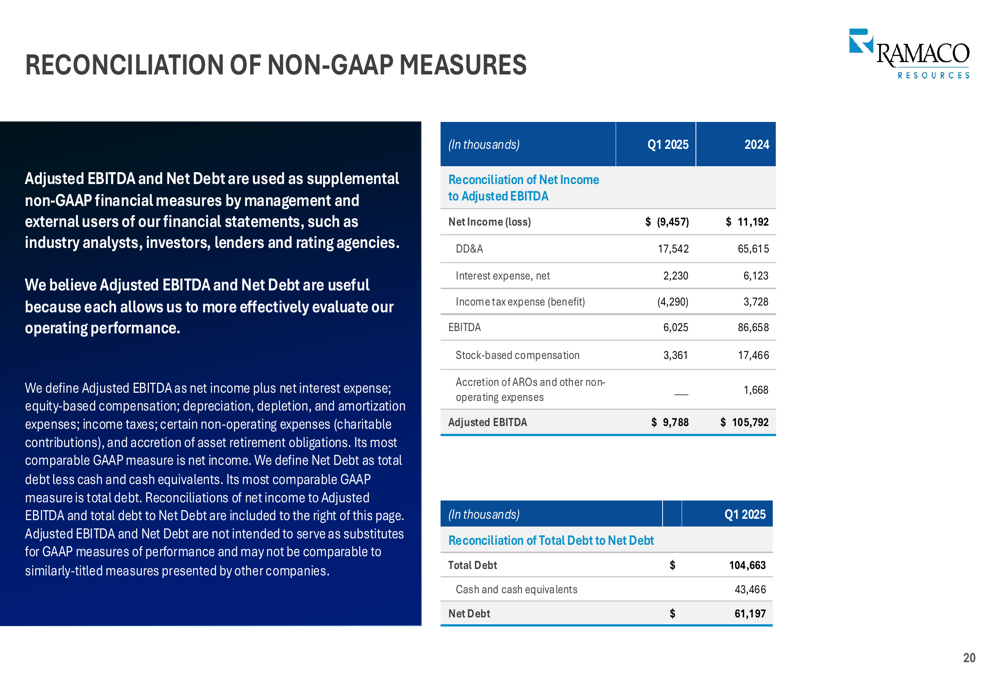

Ramaco Resources, Inc. (NASDAQ:METC) released its first quarter 2025 investor presentation highlighting record coal production and significant cost reductions amid a challenging market environment. The company reported net income of $11 million and adjusted EBITDA of $9.8 million for Q1 2025, while maintaining a strong balance sheet with a net debt to adjusted EBITDA ratio below 0.7x.

The metallurgical coal producer continues to execute its dual growth strategy of expanding coal production while developing rare earth elements and critical minerals at its Brook Mine in Wyoming. This comes as global coking coal markets have shown weakness, with U.S. East Coast indices declining 6% in the first quarter according to previous company statements.

Quarterly Performance Highlights

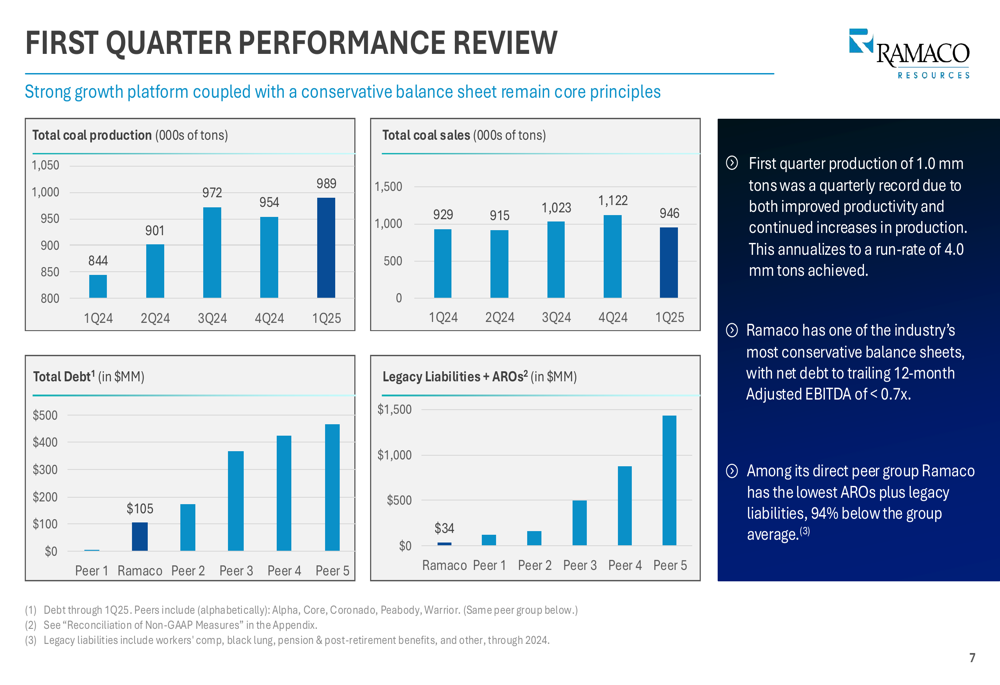

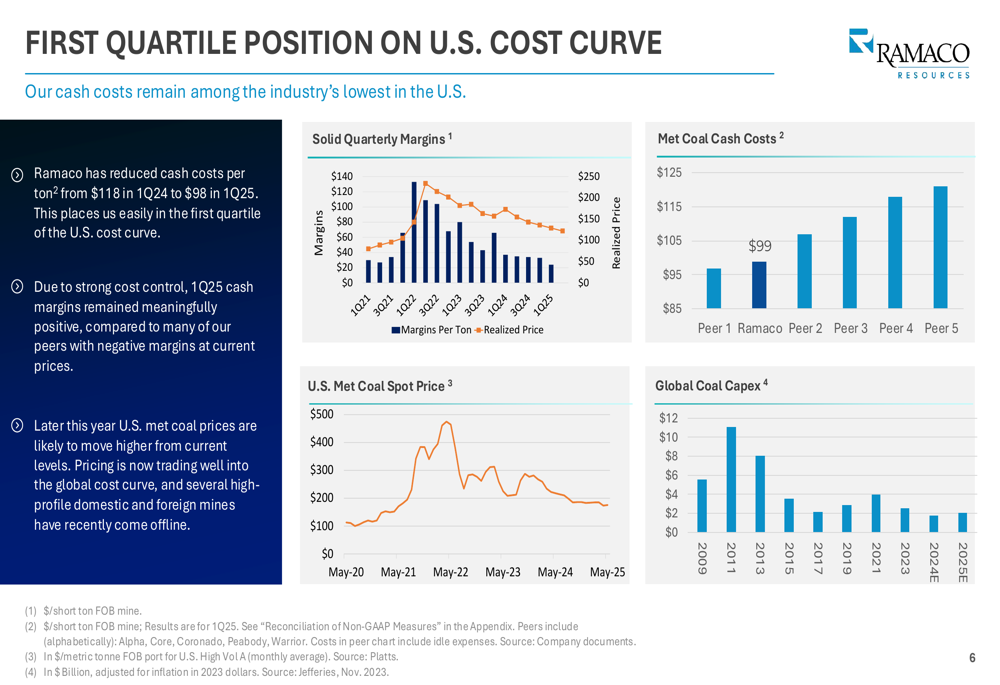

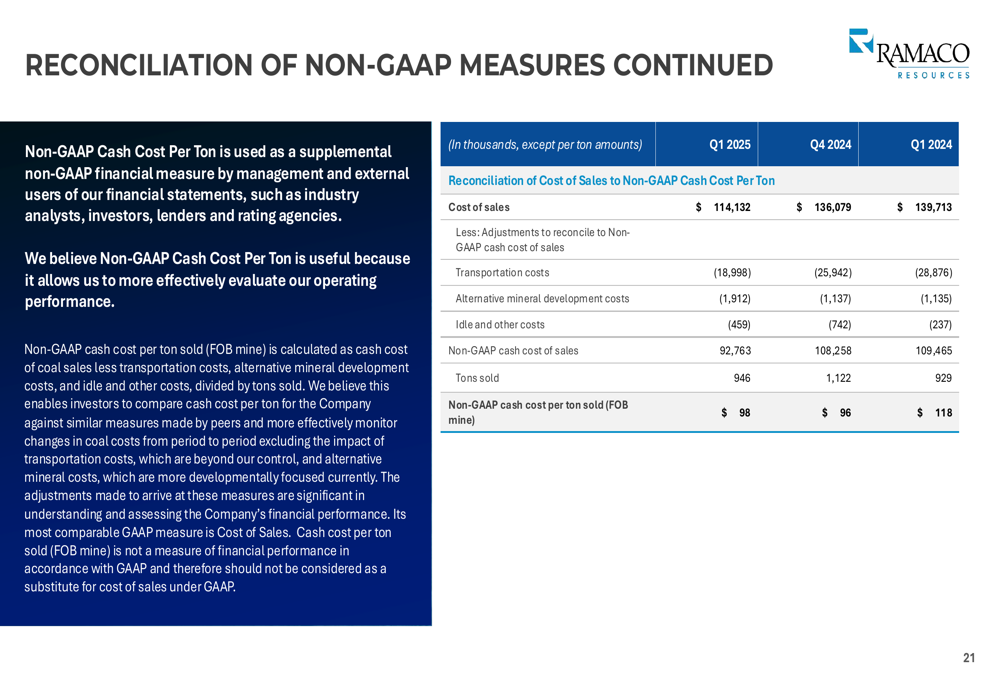

Ramaco achieved record first quarter coal production of 1.0 million tons, demonstrating operational efficiency despite industry headwinds. The company significantly reduced its cash costs per ton from $118 in Q1 2024 to $98 in Q1 2025, positioning it in the first quartile of the U.S. cost curve.

As shown in the following chart of production and cost metrics:

This cost improvement comes at a critical time as Chinese steel exports continue to pressure global steel mill profits. The company’s ability to maintain solid margins while reducing costs reflects its operational discipline and advantageous mining assets.

The company’s first quartile position on the U.S. cost curve is illustrated in this comparison:

Financial Position

Ramaco maintains a strong financial position with total debt of $34 million as of Q1 2025. The company’s net debt stands at approximately $61.2 million, resulting in a net debt to adjusted EBITDA ratio below 0.7x, which provides financial flexibility for its growth initiatives.

The company’s adjusted EBITDA for Q1 2025 was $9.8 million, as detailed in this reconciliation:

Cash costs per ton sold decreased to $98 in Q1 2025 from $118 in Q1 2024, though slightly higher than the $96 reported in Q4 2024. This metric is particularly important as it demonstrates Ramaco’s ability to control costs in a challenging market environment.

2025 Guidance & Outlook

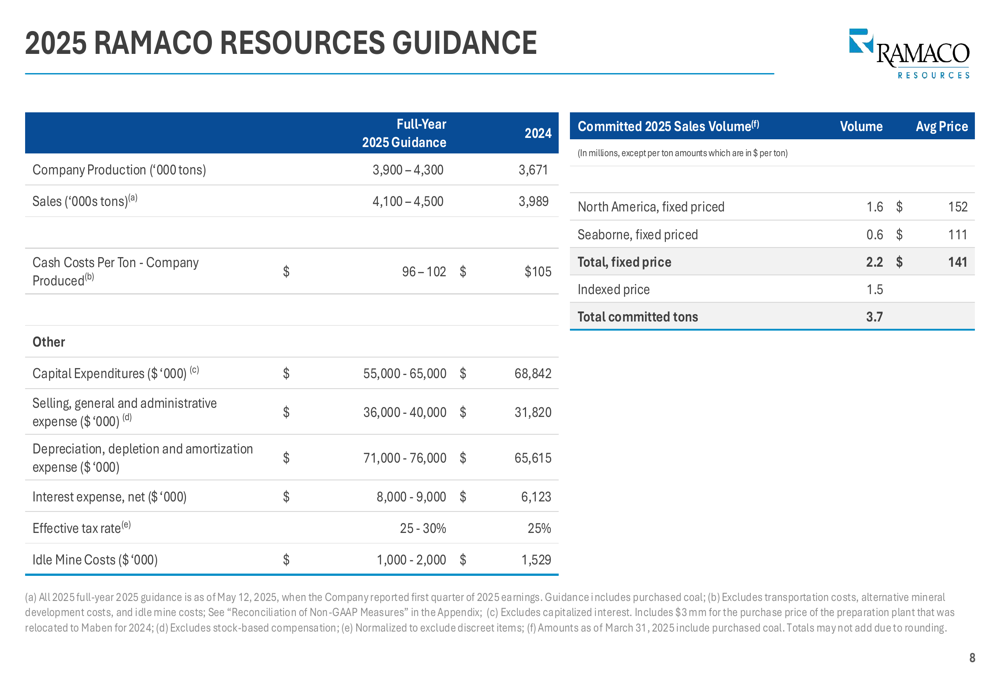

For 2025, Ramaco has provided comprehensive guidance showing continued operational growth and cost management. The company expects production to range between 3.9 and 4.3 million tons, with sales volumes between 4.1 and 4.5 million tons. Cash costs per ton are projected to be $96-102, an improvement from $105 in 2024.

The company has already secured commitments for approximately 3.7 million tons at an average price of $141 per ton for 2025, providing revenue visibility for the year ahead.

Ramaco’s stock closed at $8.99 on May 9, 2025, with a premarket price of $9.03 on May 12, showing relatively stable trading ahead of the presentation release. The company’s shares have traded between $6.30 and $15.32 over the past 52 weeks, reflecting market volatility in the coal sector.

Strategic Initiatives

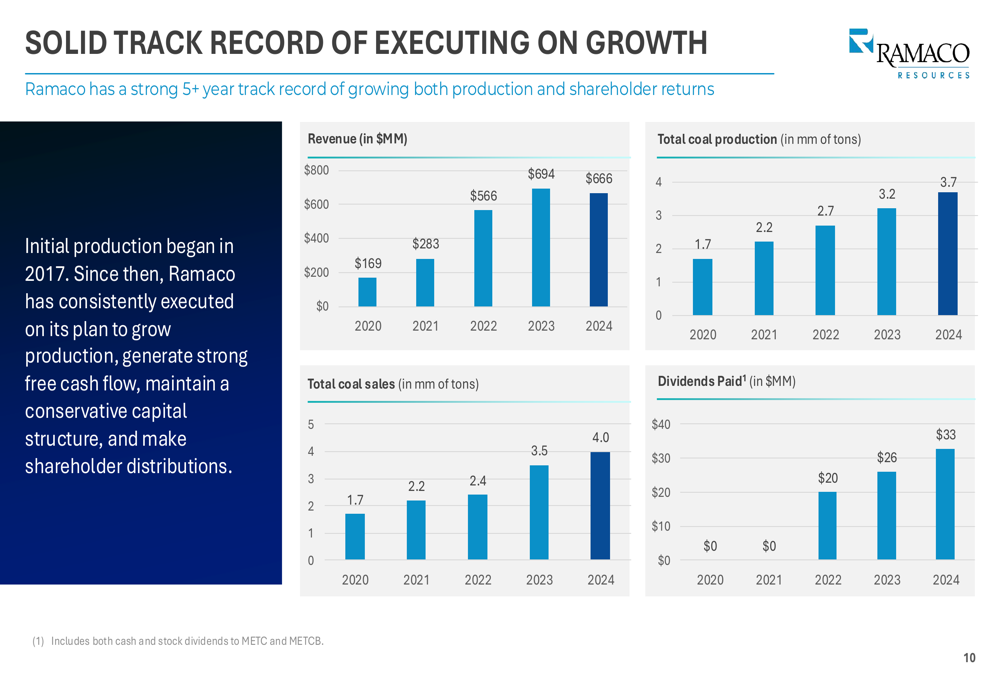

Ramaco has demonstrated consistent growth over recent years, with revenue increasing from $169 million in 2020 to $666 million in 2024, and coal production growing from 1.7 million tons to 3.7 million tons during the same period. The company has also increased its dividend payments from zero in 2020 to $33 million in 2024.

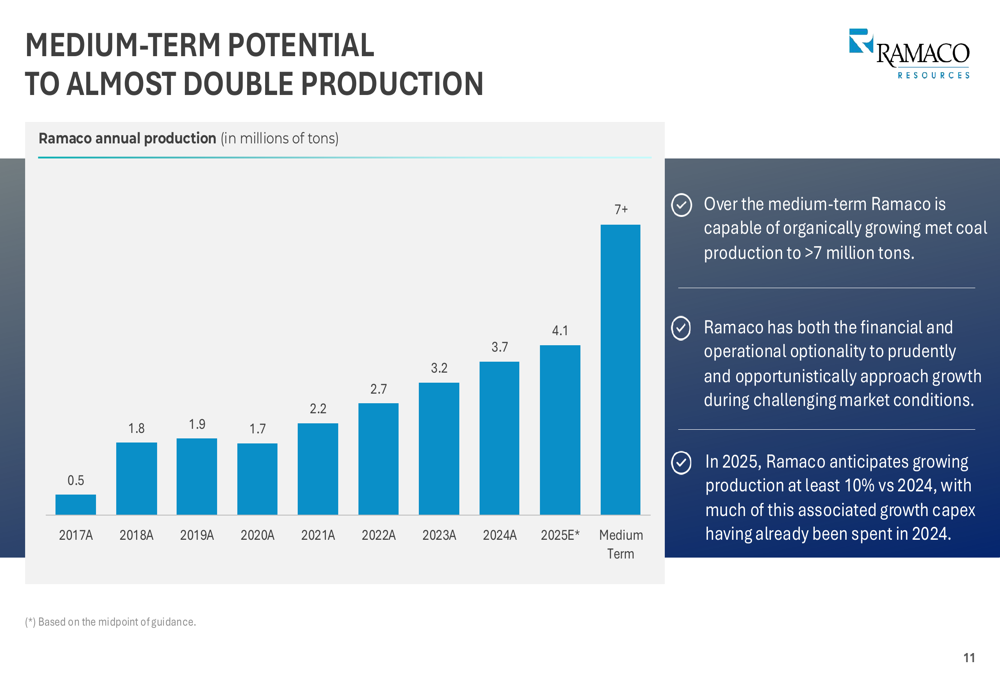

Looking ahead, Ramaco has outlined ambitious growth plans to potentially double its production over the medium term, targeting more than 7 million tons annually. This expansion would represent significant growth from its current production levels.

Rare Earth Elements Development

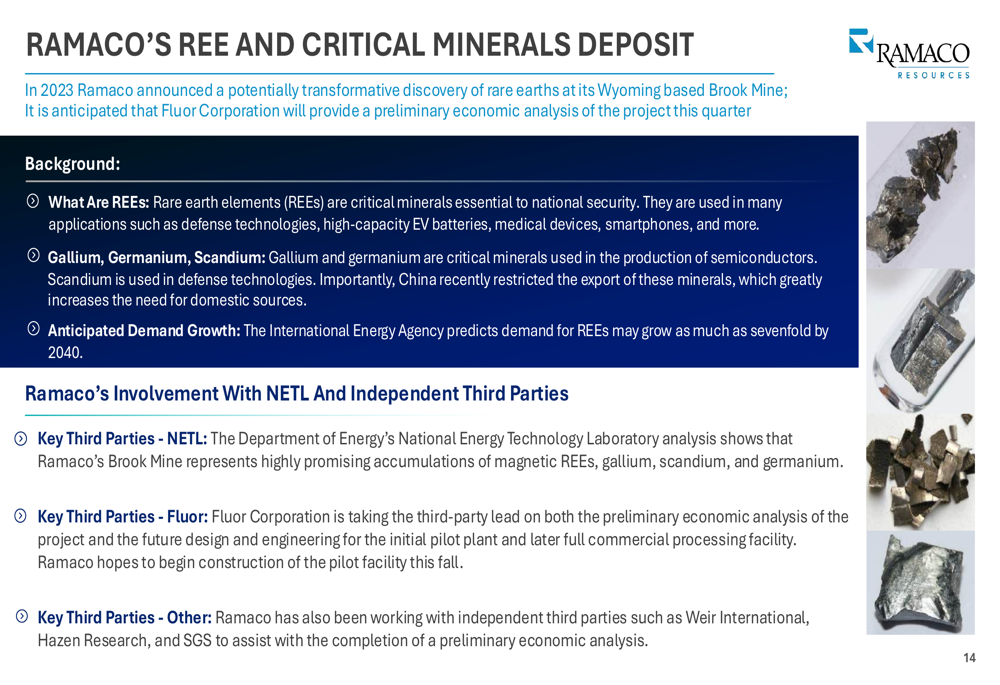

A key strategic focus for Ramaco is the development of its Brook Mine in Wyoming for rare earth elements (REEs) and critical minerals. The company announced this potentially transformative discovery in 2023, with Fluor Corporation (NYSE:FLR) expected to provide a preliminary economic analysis this quarter.

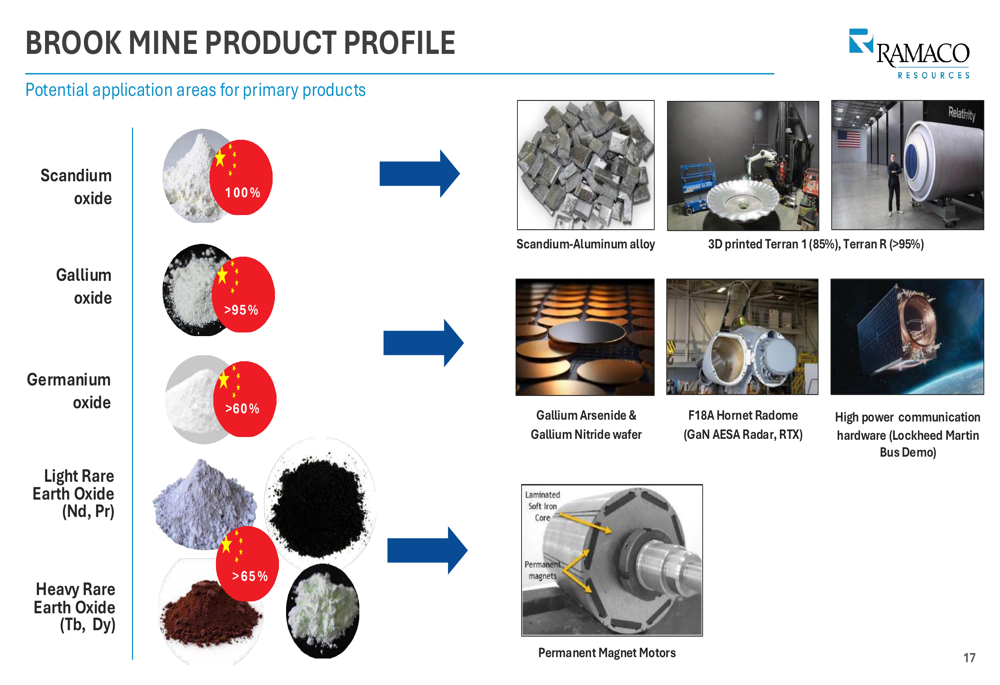

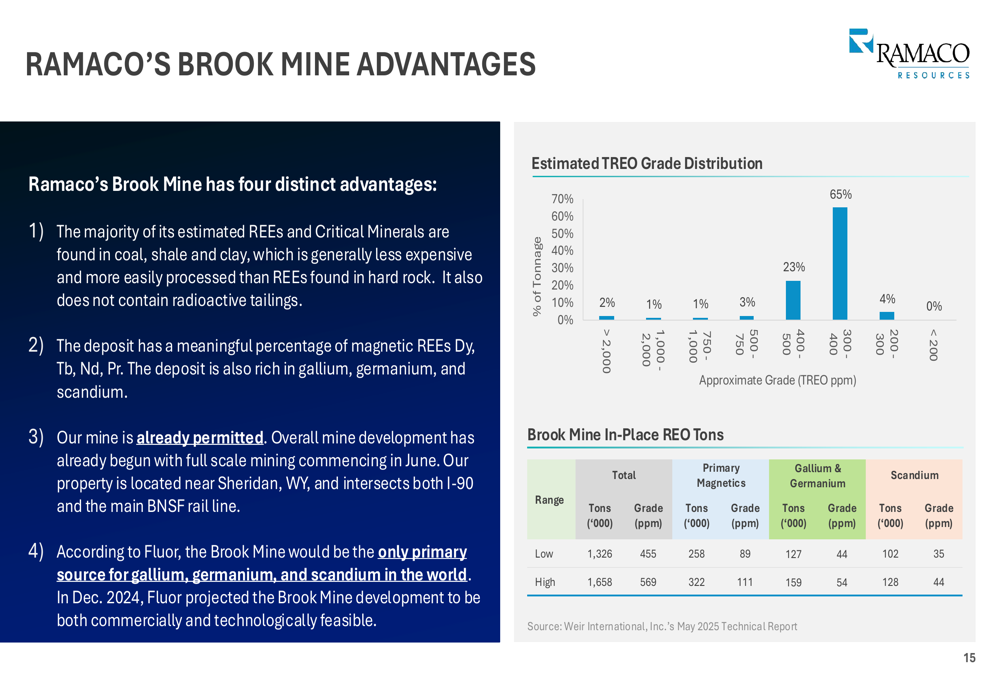

The Brook Mine is positioned as a unique source of critical minerals, with Fluor describing it as potentially the only primary source for gallium, germanium, and scandium in the world. These elements are crucial for advanced technologies and have been subject to export restrictions from China.

The mine’s product profile includes high-value elements with applications in aerospace, defense, and advanced manufacturing. The company highlights that many of these materials have been banned for export by China, creating potential market opportunities.

Ramaco’s Brook Mine advantages include the presence of REEs in coal, shale, and clay, making them potentially easier to process. The mine is already permitted, which could accelerate development timelines compared to greenfield projects.

Forward-Looking Statements

While Ramaco’s presentation paints an optimistic picture of its growth prospects, investors should note that the company faces several challenges. Global coking coal markets have shown weakness, and weather-related operational challenges could impact production in Q1 2025, as mentioned in previous company communications.

The company’s dual strategy of expanding metallurgical coal production while developing rare earth elements represents both an opportunity and execution risk. The Brook Mine’s economic viability remains to be fully demonstrated, with the upcoming Fluor analysis representing a critical milestone.

Nevertheless, Ramaco’s improved cost position, strong contract book for 2025, and potential for both coal production growth and diversification into critical minerals provide multiple avenues for potential value creation in the years ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.