Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

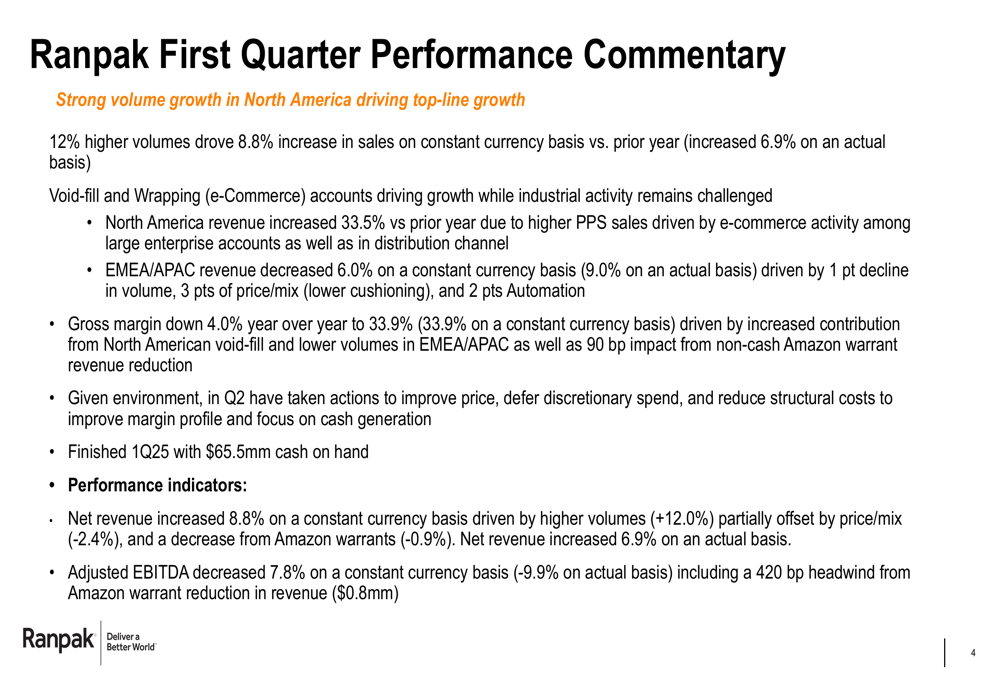

Ranpak Holdings Corp (NYSE:PACK) released its first quarter 2025 earnings presentation on May 6, showing a company experiencing strong volume growth but facing profitability challenges. The sustainable packaging solutions provider reported an 8.8% increase in sales on a constant currency basis, driven primarily by 12% higher volumes, though this was partially offset by negative price/mix effects and Amazon (NASDAQ:AMZN) warrant impacts.

The stock has been under pressure, trading at $4.29 as of May 5, 2025, with a premarket drop of 4.43% to $4.10 following the release, reflecting investor concerns about the company’s declining profitability metrics despite the revenue growth.

Quarterly Performance Highlights

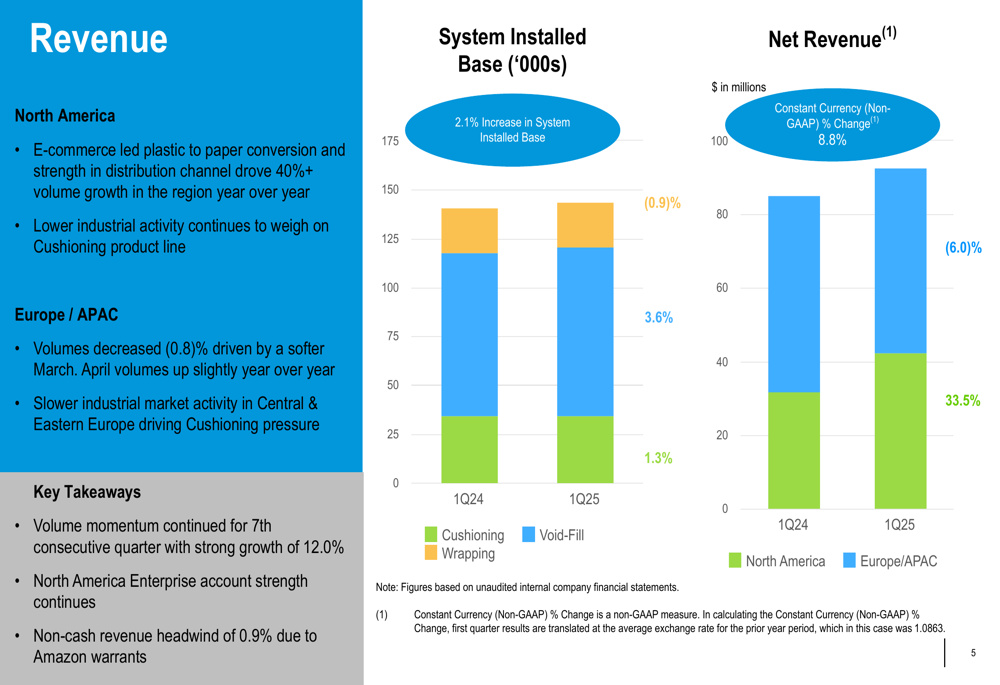

Ranpak’s Q1 2025 results revealed a stark contrast between regional performances. North America showed remarkable strength with a 33.5% revenue increase year-over-year, driven by e-commerce and distribution channel growth exceeding 40%. Meanwhile, Europe and Asia-Pacific regions struggled, with revenue decreasing 6.0% on a constant currency basis.

As shown in the following revenue breakdown chart:

The company’s system installed base grew by 2.1% compared to Q1 2024, indicating continued expansion of Ranpak’s market presence despite challenging conditions in some regions. However, the industrial market activity, particularly in Central and Eastern Europe, continues to put pressure on cushioning products.

The company’s overall performance showed the following key metrics:

Detailed Financial Analysis

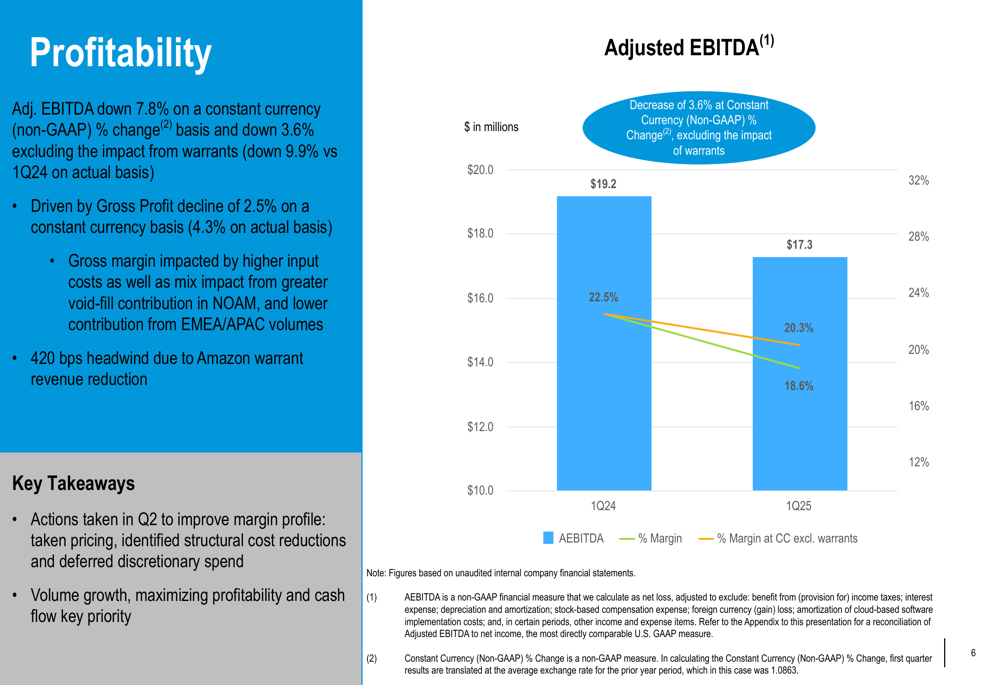

Despite the revenue growth, Ranpak’s profitability metrics declined year-over-year. Adjusted EBITDA decreased by 7.8% on a constant currency basis (9.9% on an actual basis) to $17.3 million, compared to $19.2 million in Q1 2024. The company noted a significant 420 basis point headwind from Amazon warrant revenue reduction, amounting to approximately $0.8 million.

Gross margin declined by 4.0 percentage points year-over-year to 33.9%, impacted by higher input costs and unfavorable product mix. The following chart illustrates the EBITDA trend:

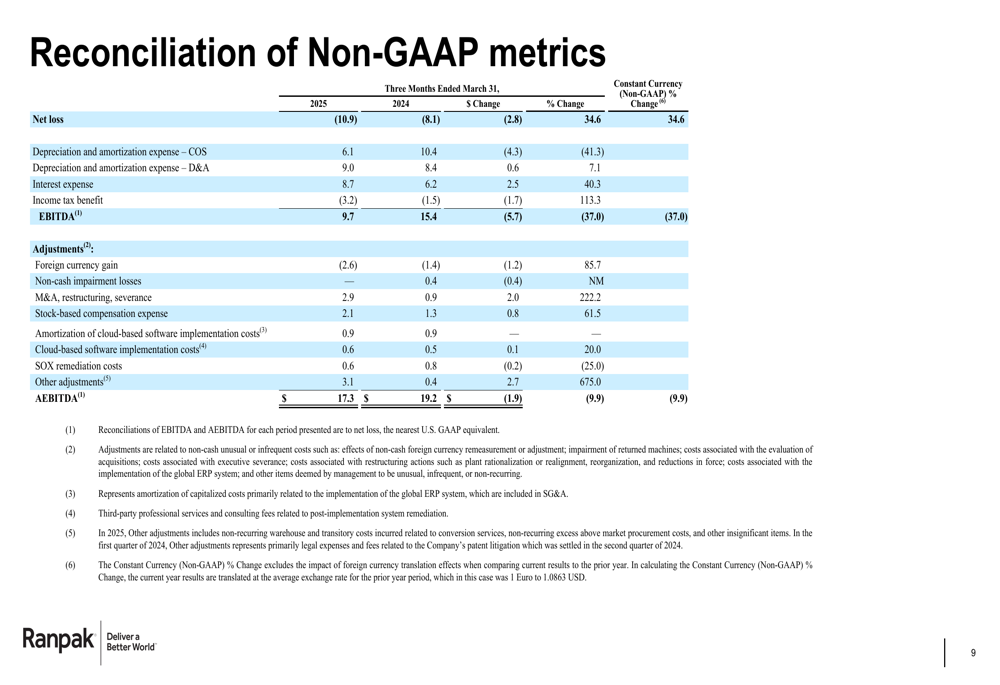

On a GAAP basis, Ranpak reported a net loss of $10.9 million for Q1 2025, compared to a net loss of $8.1 million in the same period last year. This translated to a basic and diluted loss per share of $0.13, versus $0.10 in Q1 2024.

The reconciliation between GAAP and non-GAAP metrics provides further insight into the company’s financial performance:

Ranpak maintained a solid liquidity position, ending the quarter with $65.5 million in cash and no drawings on its revolving credit facility. The company’s net leverage ratio stood at 4.3x as of March 31, 2025, with a bank-adjusted EBITDA leverage ratio of 3.9x per covenant calculation.

The company built paper inventory during the first quarter and expects to convert this to cash in the second half of the year, which should improve its financial position. Ranpak currently has $410 million in U.S. dollar-denominated first lien term loan facilities outstanding, with $4.1 million in principal payments required annually until December 2031.

Forward-Looking Statements

In response to the margin pressure, Ranpak has initiated several actions in the second quarter to improve its financial performance. These include pricing adjustments, deferral of discretionary spending, and structural cost reductions, though specific details were not provided in the presentation.

The company faces continued challenges in the industrial market, particularly in Europe, while the e-commerce sector remains a bright spot. April volumes in Europe/APAC were reported as "up slightly," potentially indicating some stabilization in that region.

These Q1 results may put pressure on Ranpak’s previously announced 2025 guidance of $387-409 million in revenue (representing 5-11% growth) and $88-97 million in adjusted EBITDA. The declining profitability in Q1, despite revenue growth, suggests the company will need its Q2 actions to be effective to meet full-year targets.

The company’s relationship with Amazon appears significant, as evidenced by the warrant-related revenue adjustments. However, the presentation did not provide further details on how this strategic partnership might evolve throughout 2025.

As Ranpak navigates these mixed market conditions, investors will be watching closely to see if management’s actions to improve margins can successfully balance the strong volume growth with improved profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.