Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Rayonier Advanced Materials (NYSE:RYAM) presented its third quarter 2025 financial results on November 5, 2025, characterizing the current year as a "trough" with recovery expected in 2026 and beyond. The company reported revenue of $353 million, down $48 million year-over-year, while operating income improved to $9 million, up $26 million from Q3 2024. Despite the operating income improvement, RYAM missed analyst expectations, with an EPS of -$0.07 compared to the forecasted -$0.02, triggering a significant stock decline of 7.2% in regular trading and a further 10.41% drop in premarket trading.

The presentation focused on framing current challenges as temporary while outlining an ambitious growth strategy centered on high-value Cellulose Specialties and Biomaterials segments. Management emphasized that Q2 2025 marked the low point of the company's performance, with Q3 showing signs of normalization.

Quarterly Performance Highlights

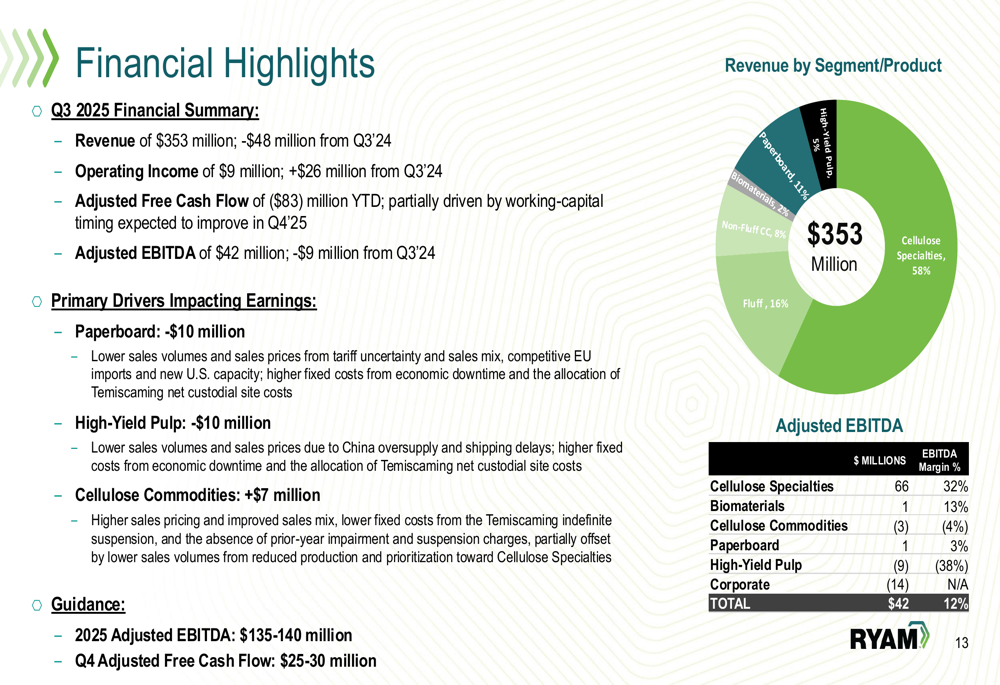

RYAM's Q3 2025 financial performance revealed mixed results across its business segments. The company reported adjusted EBITDA of $42 million, down $9 million from the same period last year, with an EBITDA margin of 12%.

As shown in the following chart of Q3 2025 financial highlights and segment performance:

The Cellulose Specialties segment remained the strongest performer, contributing $66 million in adjusted EBITDA with a 32% margin. This segment represented 58% of total revenue. In contrast, the High-Yield Pulp segment recorded a negative EBITDA of $9 million with a -38% margin, while Cellulose Commodities posted a negative $3 million EBITDA with a -4% margin.

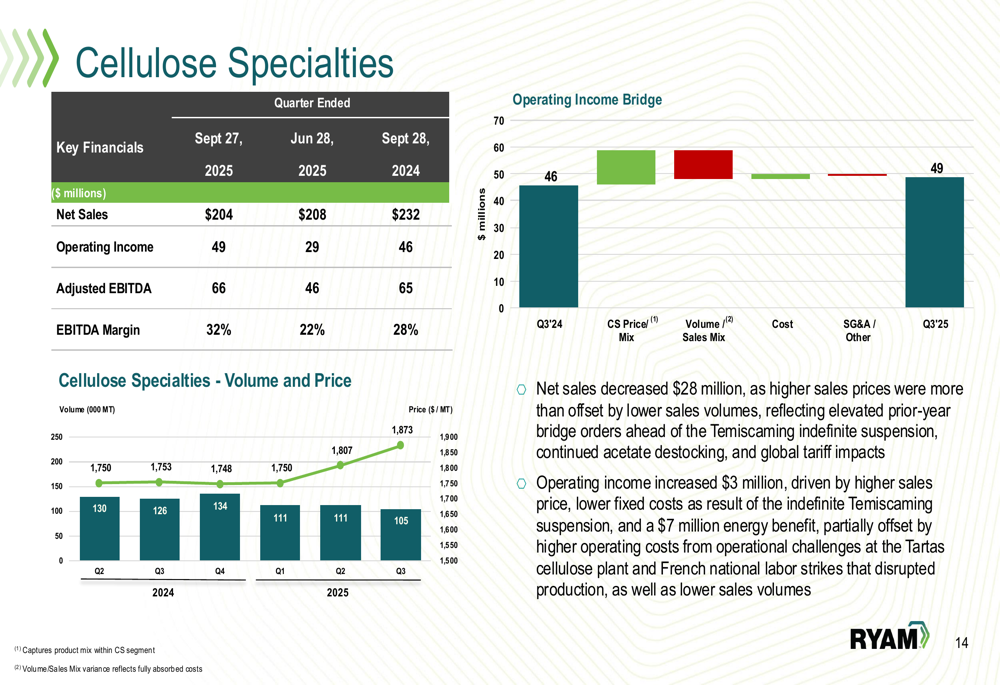

A detailed breakdown of the Cellulose Specialties segment performance shows resilience despite broader market challenges:

The segment generated $204 million in net sales with operating income of $49 million. While net sales decreased by $28 million year-over-year, operating income increased by $3 million, driven by higher sales prices and lower fixed costs.

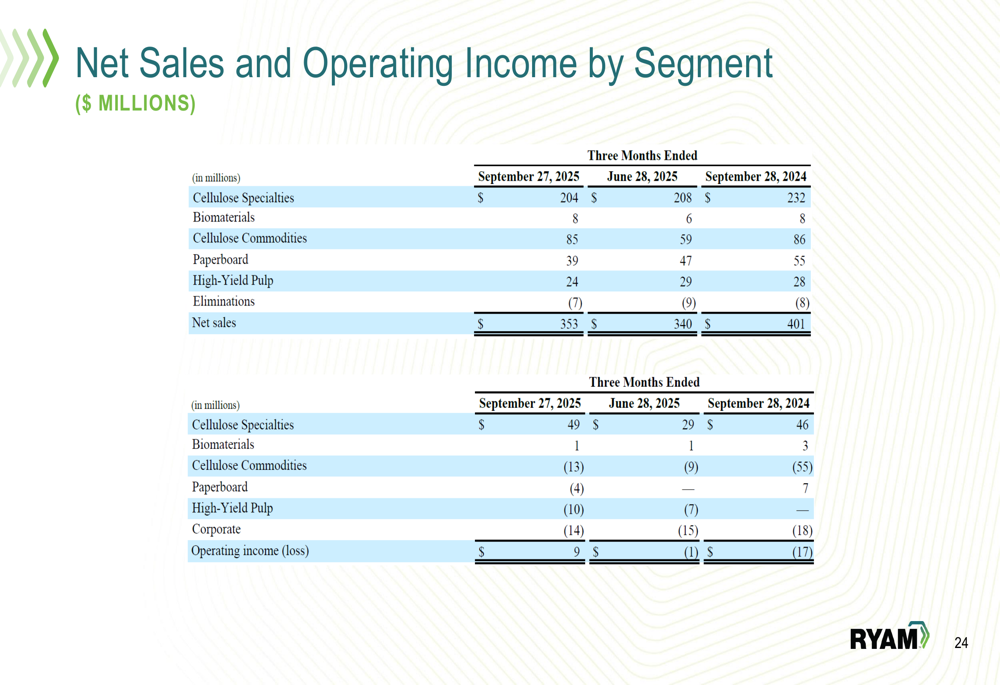

The comprehensive breakdown of sales and operating income across all segments provides further context:

Strategic Initiatives

RYAM outlined a strategic pivot toward becoming a pure-play Cellulose Specialties and Biomaterials company. The plan includes divesting the underperforming Paperboard and High-Yield Pulp businesses, with particular focus on restoring profitability to the Temiscaming site before pursuing divestiture in 2026.

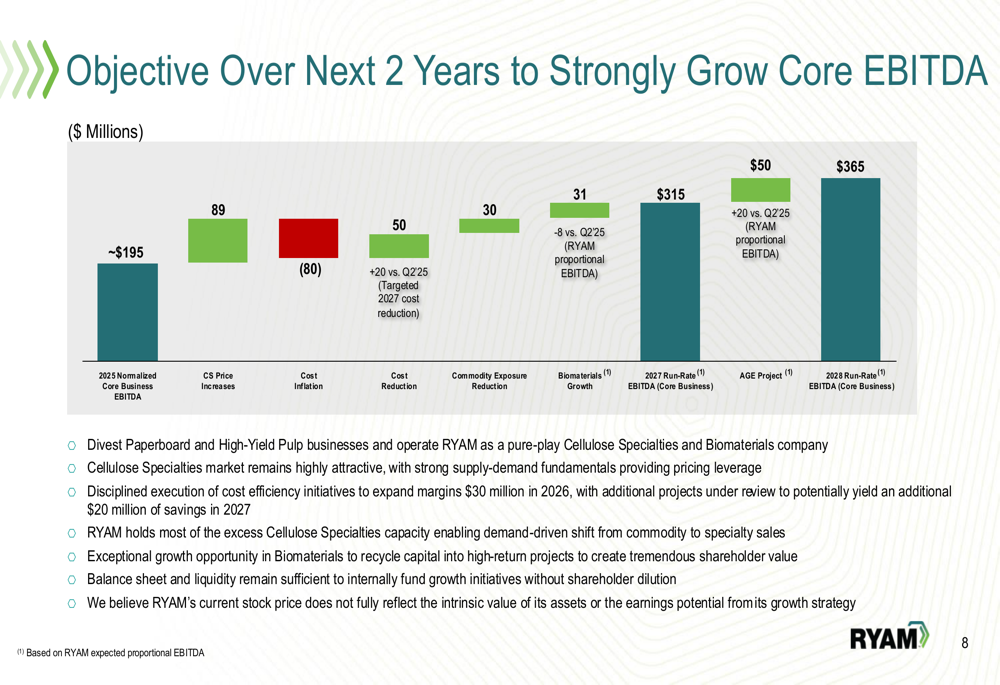

The company presented an ambitious EBITDA growth roadmap, targeting an increase from approximately $195 million normalized EBITDA in 2025 to $365 million run-rate EBITDA by 2028:

This growth strategy relies on several key drivers, including CS price increases ($89 million), cost reduction initiatives ($50 million), commodity exposure reduction ($30 million), and Biomaterials growth ($31 million). The company also highlighted the Altamaha Green Energy (AGE) project, expected to contribute $50 million to EBITDA.

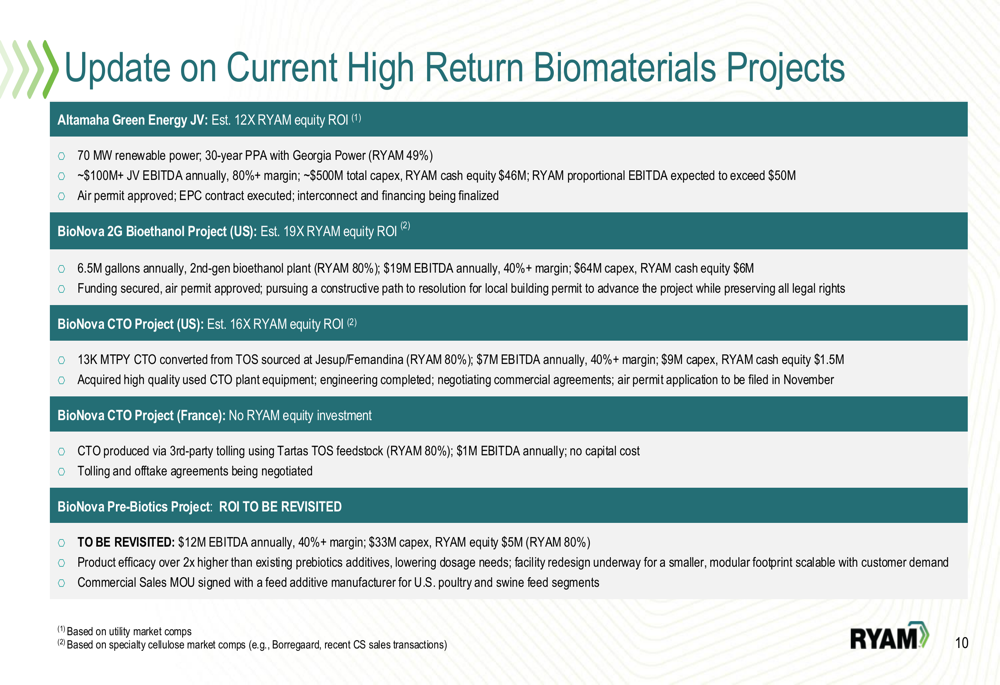

RYAM is advancing several high-return Biomaterials projects that form a critical part of its growth strategy:

Notable projects include the Altamaha Green Energy JV, expected to generate over $100 million in annual JV EBITDA (with RYAM's proportional EBITDA exceeding $50 million), and the BioNova 2G Bioethanol Project, projected to contribute $19 million in annual EBITDA.

Detailed Financial Analysis

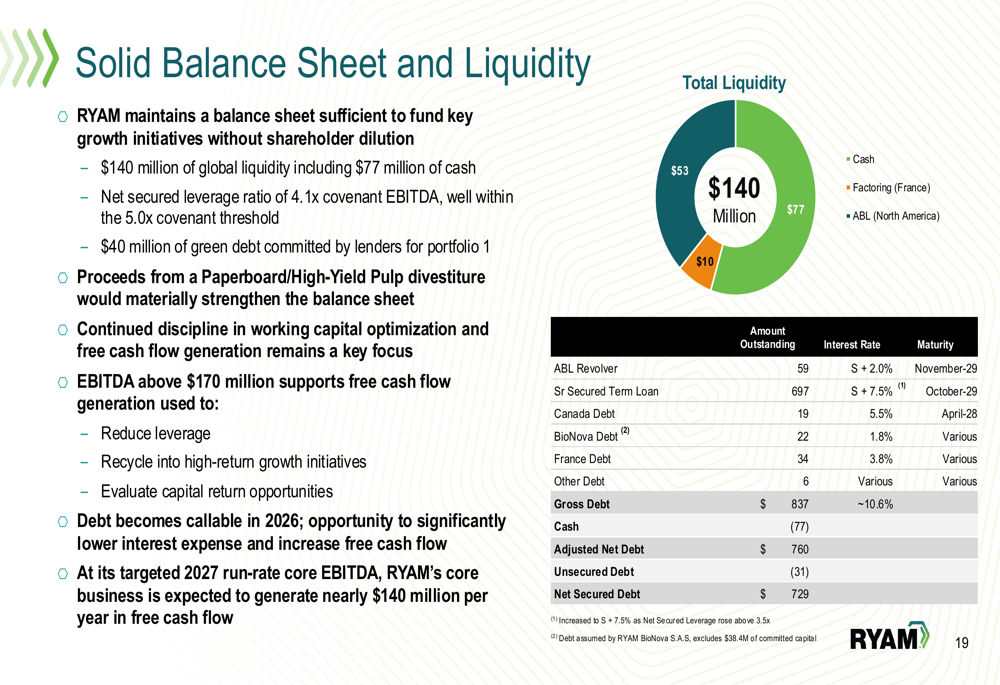

RYAM's balance sheet shows $140 million of global liquidity, including $77 million in cash, against a total debt of $837 million:

The adjusted net debt stands at $760 million, reflecting the company's significant leverage position. This financial structure underscores the importance of successful execution on the company's growth initiatives to improve cash flow generation and debt servicing capacity.

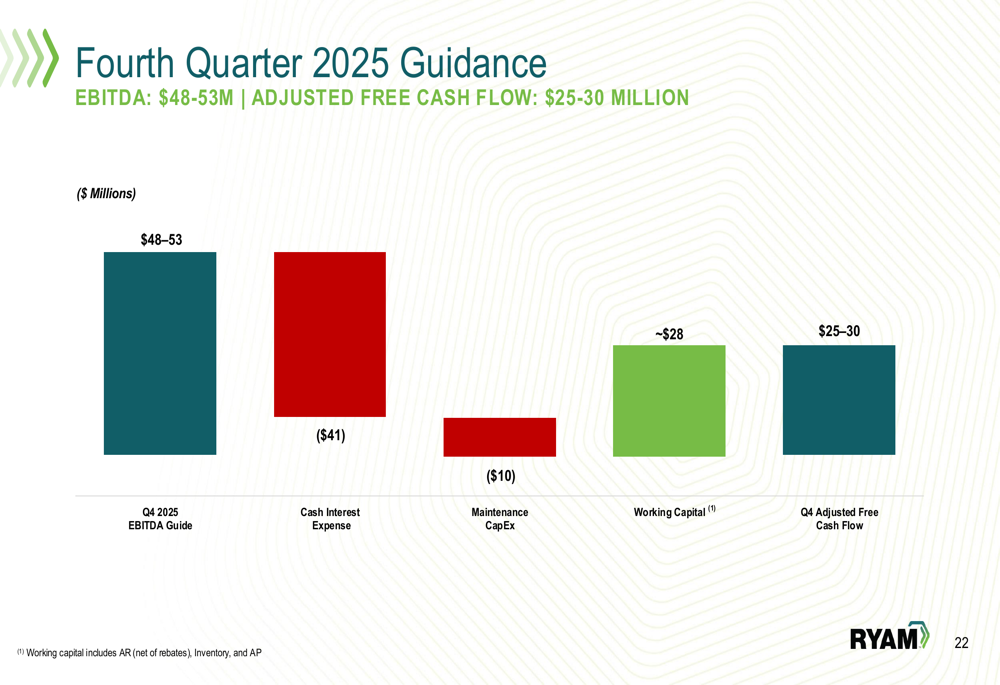

For Q4 2025, RYAM provided the following guidance:

The company expects Q4 2025 EBITDA of $48-53 million and adjusted free cash flow of $25-30 million. The projected improvement in cash flow is primarily driven by working capital improvements of approximately $28 million, partially offset by cash interest expense of $41 million and maintenance capital expenditures of $10 million.

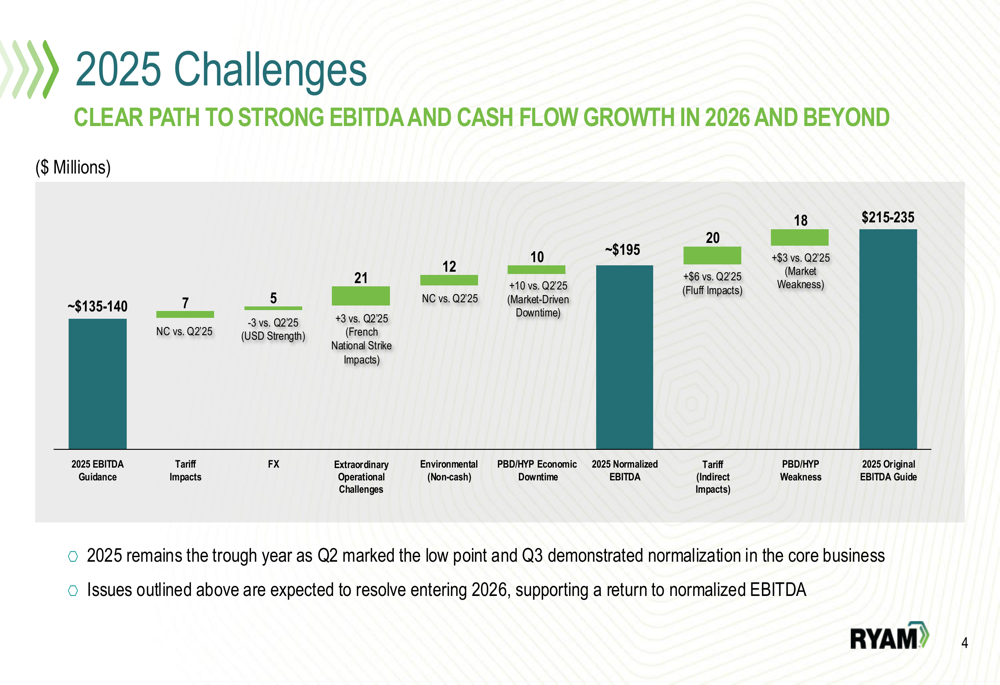

The company identified several factors impacting its 2025 performance, illustrating the path from original EBITDA guidance of $215-235 million to the current guidance of $135-140 million:

Key impacts include tariffs ($27 million total impact), foreign exchange (-$5 million), extraordinary operational challenges ($21 million), environmental non-cash charges ($12 million), and economic downtime in the Paperboard and High-Yield Pulp segments ($10 million).

Forward-Looking Statements

Looking ahead, RYAM's management expressed confidence that 2025 represents a trough year, with recovery expected in 2026 and beyond. The company is targeting significant price increases across Cellulose Specialties grades and implementing cost reduction initiatives to enhance margins.

For the Temiscaming site specifically, RYAM outlined a three-pronged approach to restore profitability:

1. Reducing costs by $10 million annually

2. Improving Paperboard Operational Equipment Efficiency for $10 million annual benefit

3. Realizing $10 million in EBITDA improvement from new product development

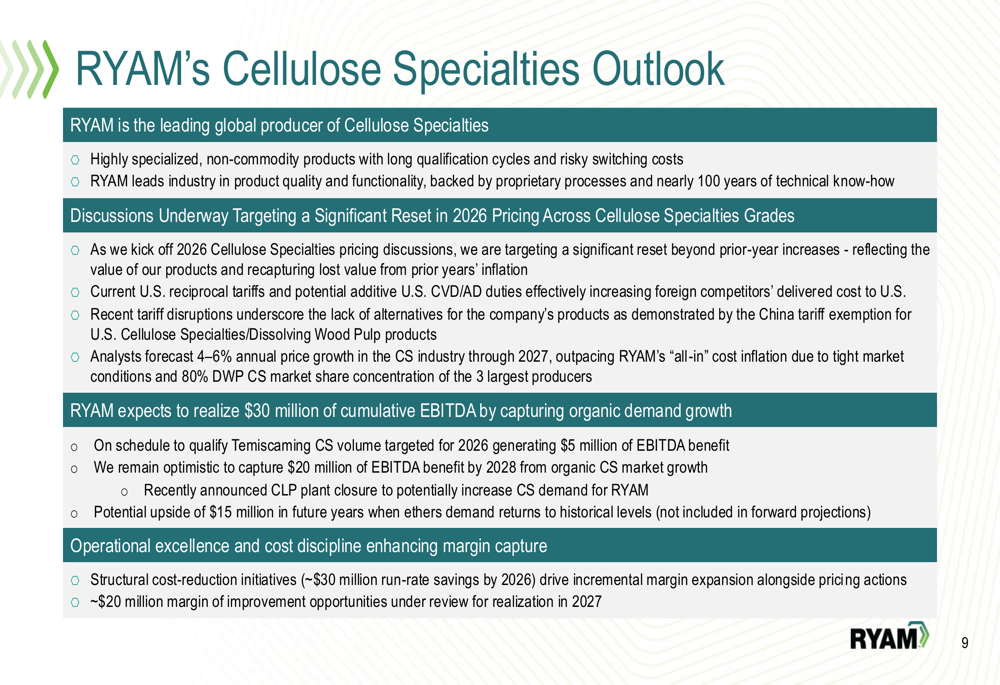

The company's Cellulose Specialties outlook remains positive, with RYAM positioning itself as the leading global producer in this specialized market:

Management emphasized that discussions are underway for a significant reset in 2026 pricing across Cellulose Specialties grades, which is expected to be a major driver of future EBITDA growth.

Despite the optimistic forward-looking statements, investors appear skeptical, as evidenced by the significant stock price decline following the earnings announcement. The market reaction suggests concerns about execution risks and the timeline for recovery, particularly given the magnitude of the miss against analyst expectations for Q3 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.