Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

RBB Bancorp (NASDAQ:RBB) released its second quarter 2025 earnings presentation on July 21, 2025, revealing a significant rebound in profitability after a disappointing first quarter. The bank, which focuses on serving Asian American communities, reported substantial improvements across key financial metrics while maintaining strong capital ratios and continuing to address asset quality concerns.

The bank’s stock closed at $18.26 on July 21, down slightly by 0.38% from the previous session. RBB shares have experienced significant pressure over the past six months, declining 30.6% according to previous earnings reports, with the stock trading between its 52-week range of $14.40 to $25.30.

Quarterly Performance Highlights

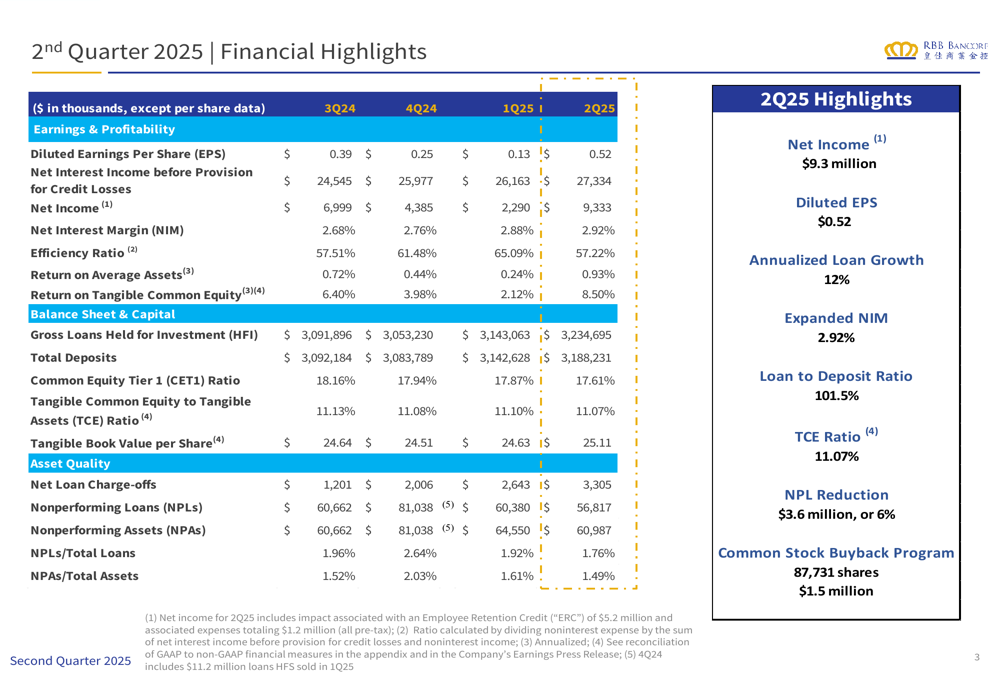

RBB Bancorp’s second quarter results showed marked improvement from the first quarter, with diluted earnings per share jumping to $0.52 from $0.13 in Q1 2025. This represents a significant recovery after the bank missed analyst expectations in the previous quarter, when EPS came in at $0.13 against a forecast of $0.38.

Net income increased to $9.33 million, up substantially from $2.29 million in the first quarter. The bank’s efficiency ratio improved to 57.22% from 65.09%, while return on average assets rose to 0.93% from 0.24%. Return on tangible common equity showed particularly strong improvement, reaching 8.50% compared to just 2.12% in Q1.

As shown in the following comprehensive financial highlights chart:

The bank’s net interest margin (NIM) showed modest improvement, increasing to 2.92% from 2.88% in the previous quarter. This marks the fourth consecutive quarterly increase in NIM, suggesting the bank is successfully managing its interest rate spread despite challenging market conditions.

Detailed Financial Analysis

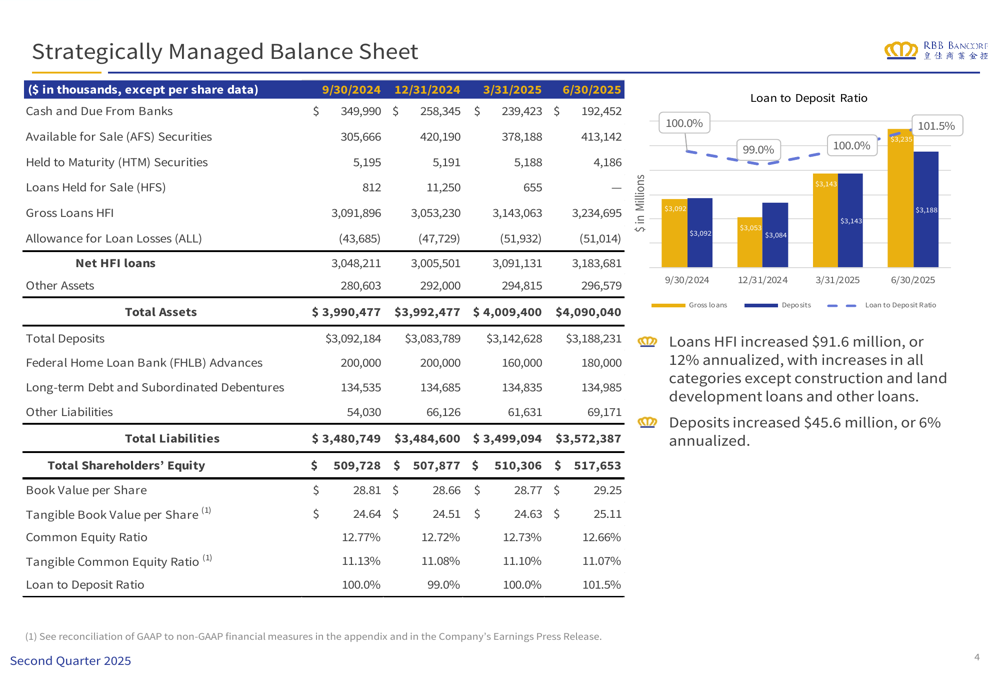

RBB’s balance sheet expanded during the quarter, with total assets increasing to $4.09 billion. The bank reported annualized loan growth of 12%, with gross loans held for investment rising to $3.23 billion. Total (EPA:TTEF) deposits grew at a 6% annualized rate to $3.19 billion, resulting in a loan-to-deposit ratio of 101.5%.

The following chart illustrates the bank’s balance sheet evolution over recent quarters:

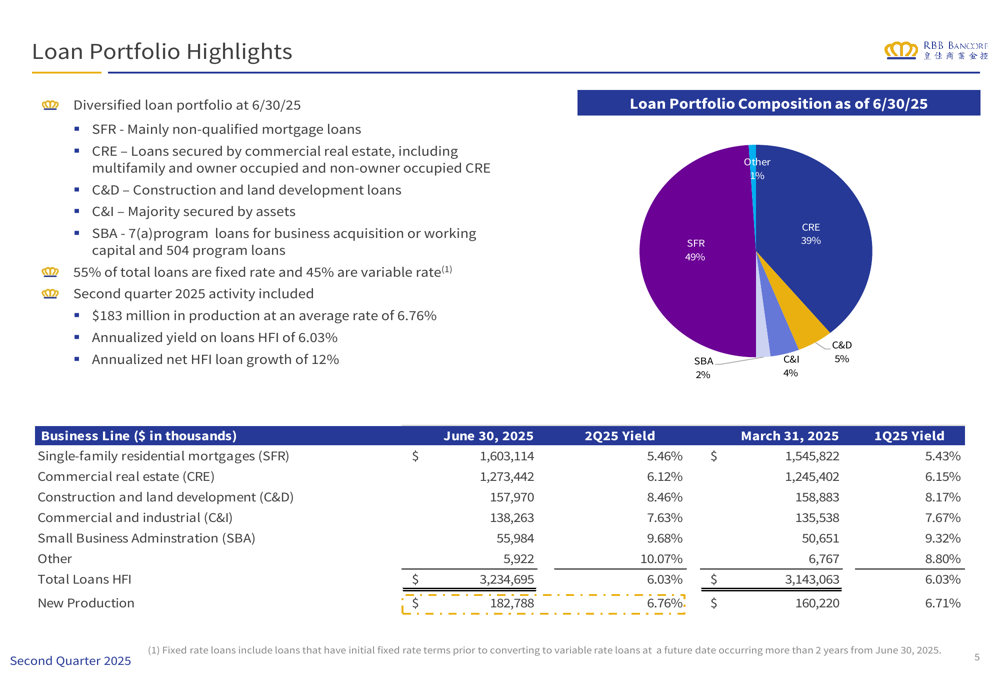

The loan portfolio remains well-diversified, with single-family residential (SFR) mortgages comprising 49% of total loans, followed by commercial real estate (CRE) at 39%. During the second quarter, RBB generated $183 million in new loan production at an average rate of 6.76%, supporting the overall portfolio yield of 6.03%.

The bank’s loan composition and yields are detailed in the following breakdown:

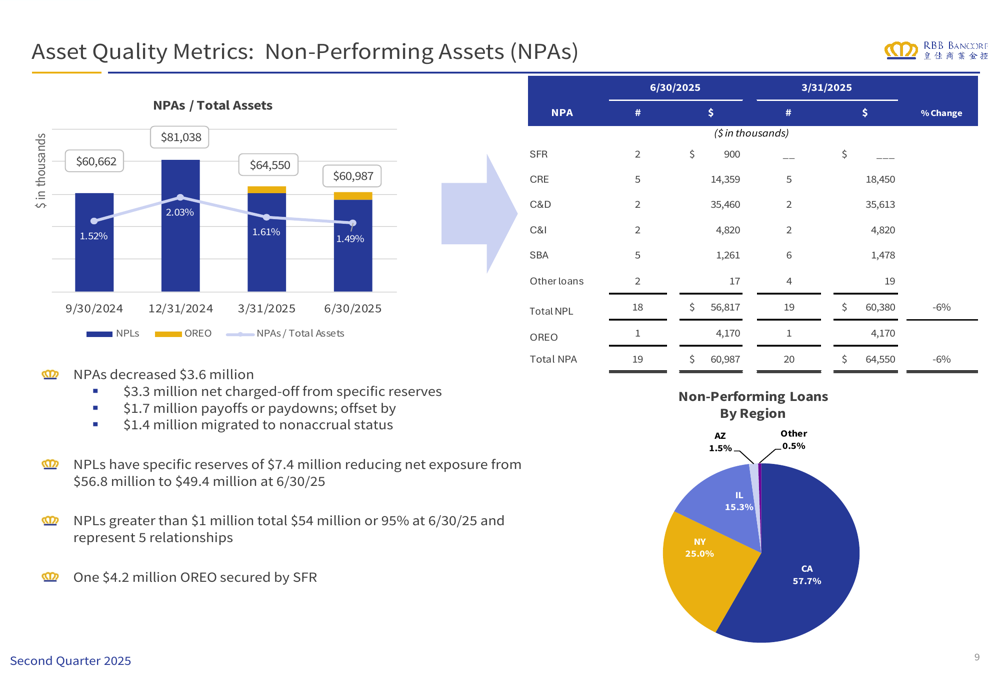

Asset quality showed improvement during the quarter, with non-performing assets (NPAs) decreasing by $3.6 million to $61.0 million, representing 1.49% of total assets, down from 1.61% in the previous quarter. Non-performing loans (NPLs) totaled $56.8 million or 1.76% of total loans, with specific reserves of $7.4 million allocated against these exposures.

The following chart demonstrates the trend in non-performing assets:

The allowance for loan losses decreased by $918,000 during Q2 2025, primarily due to net charge-offs of $3.3 million, partially offset by a provision for loan losses of $2.4 million. The allowance as a percentage of loans held for investment stood at 1.58% at quarter-end, compared to 1.65% at the end of Q1.

Strategic Initiatives

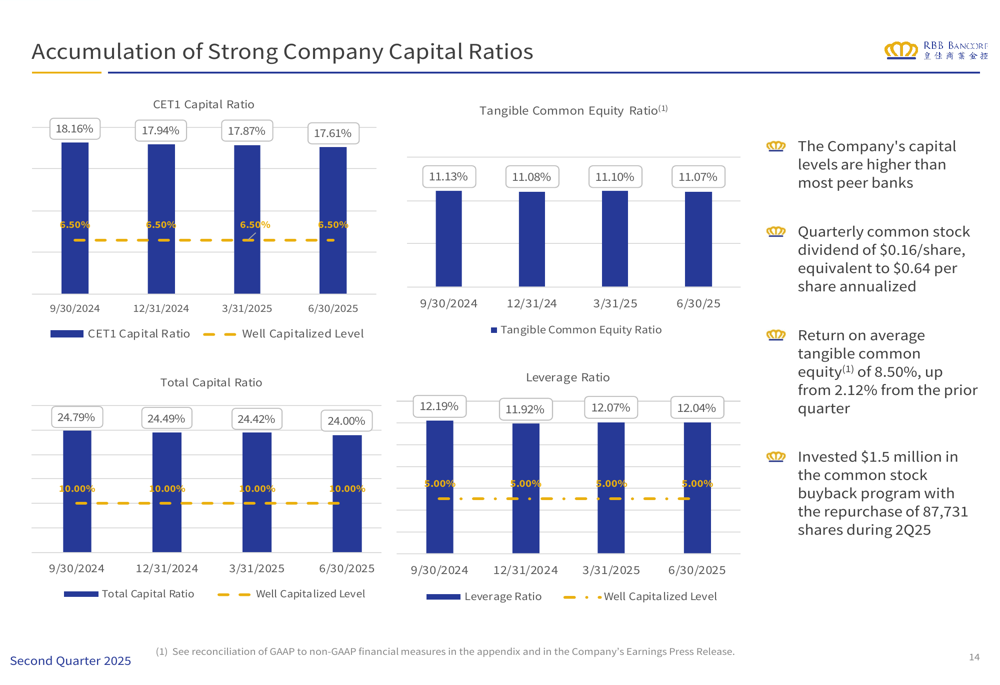

RBB Bancorp continued to focus on capital management during the quarter, maintaining strong capital ratios while returning value to shareholders. The bank declared a quarterly common stock dividend of $0.16 per share and repurchased 87,731 shares for $1.5 million under its buyback program.

The bank’s capital position remains robust, with a CET1 capital ratio of 17.61% and tangible common equity to tangible assets ratio of 11.07%. These metrics significantly exceed regulatory requirements and, according to the presentation, are "higher than most peer banks."

The following chart illustrates RBB’s strong capital position:

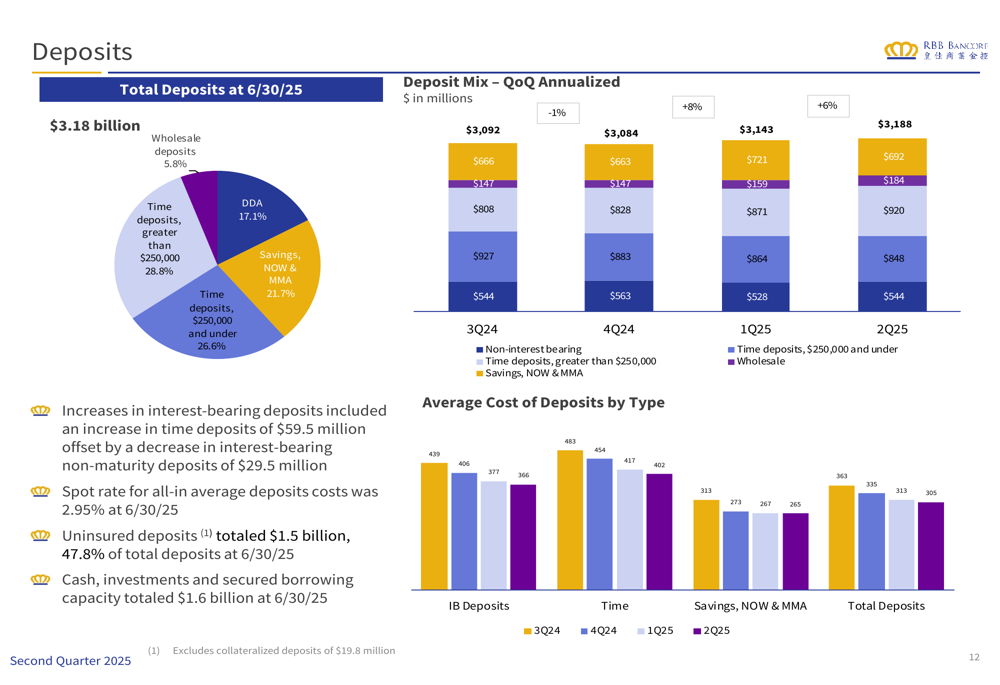

On the deposit front, RBB reported increases in time deposits of $59.5 million, offset by a decrease in interest-bearing non-maturity deposits of $29.5 million. The spot rate for all-in average deposit costs was 2.95% at quarter-end. Uninsured deposits totaled $1.5 billion, representing 47.8% of total deposits.

The bank’s deposit composition and trends are shown in the following chart:

Forward-Looking Statements

While the Q2 presentation doesn’t include specific forward guidance, RBB’s recent earnings call indicated that management expects continued loan growth at a more moderate pace and anticipates further reductions in funding costs. The bank is targeting resolution of non-performing loans by the second half of 2025.

The improvement in asset quality metrics suggests progress in addressing the challenges mentioned by CEO David Morris in the previous quarter, when he noted that "NPLs will continue to be lumpy through 2025." The significant quarter-over-quarter improvement in profitability indicates the bank may be turning a corner after facing headwinds in recent periods.

However, challenges remain, particularly in the bank’s key markets of California and New York, where economic uncertainties persist. The slight increase in special mention and substandard loans during the quarter suggests ongoing credit quality concerns that will require continued monitoring.

With tangible book value per share increasing to $25.11 from $24.63 in Q1, and the stock trading below this level, RBB’s valuation remains at a discount to book value despite the improved quarterly performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.