FTSE 100 today: Edges higher as pound slips; Mitchells & Butlers jumps on results

Introduction & Market Context

REC Silicon ASA (OTC:RECSI) released its third quarter 2025 presentation on November 6, revealing ongoing financial challenges amid difficult market conditions. The silicon materials company, which provides materials for the semiconductor and energy industries, continues to face headwinds from aggressive Chinese competition and delayed growth in key market segments.

The company's stock price fell by 0.74% to $1.205 following the earnings announcement, reflecting investor concerns about its financial position and future prospects. REC Silicon's presentation highlighted the impact of trade uncertainties and subdued demand across its target markets.

Quarterly Performance Highlights

REC Silicon reported negative EBITDA of $7.2 million from continuing operations for Q3 2025, as the company struggles with challenging market conditions and operational costs. Total revenue reached $16.9 million, with silicon gas sales volume decreasing 8.1% compared to the previous quarter.

As shown in the following chart of quarterly silicon gas sales volumes, the company shipped 524 MT in Q3 2025, down from 570 MT in Q2 2025, continuing a generally downward trend from higher volumes seen in 2023 and early 2024:

The Butte operations, which represent the company's primary revenue source, generated $16.8 million in revenue, a 15.1% decrease compared to Q2 2025. Despite the revenue decline, this segment managed to achieve a modest EBITDA contribution of $0.1 million, representing a $0.3 million improvement from the previous quarter's negative result.

The company's financial performance by segment is illustrated in the following earnings summary:

CEO Kurt Levens acknowledged the company's difficult position during the earnings call, stating, "We do not have sufficient cash to meet our debt service and other operating cash flow requirements for the coming year," emphasizing the urgent need for short to midterm funding solutions.

Financial Position and Debt Challenges

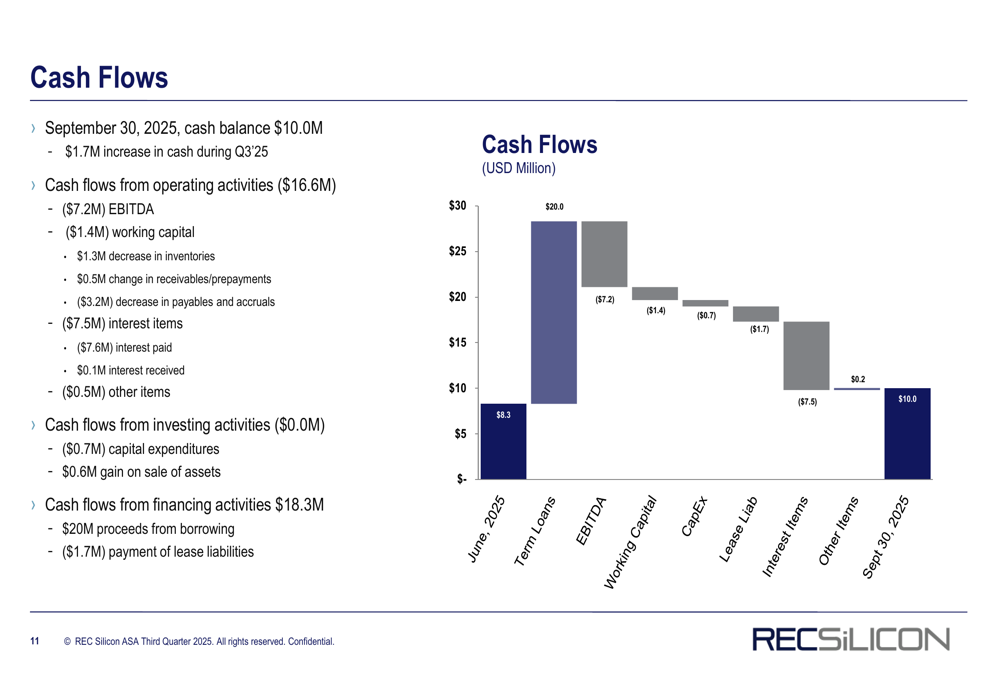

REC Silicon's financial position remains precarious, with a cash balance of $10.0 million as of September 30, 2025. While this represents a $1.7 million increase during Q3, it falls significantly short of addressing the company's substantial debt obligations.

The company's cash flow for the quarter is detailed in the following waterfall chart:

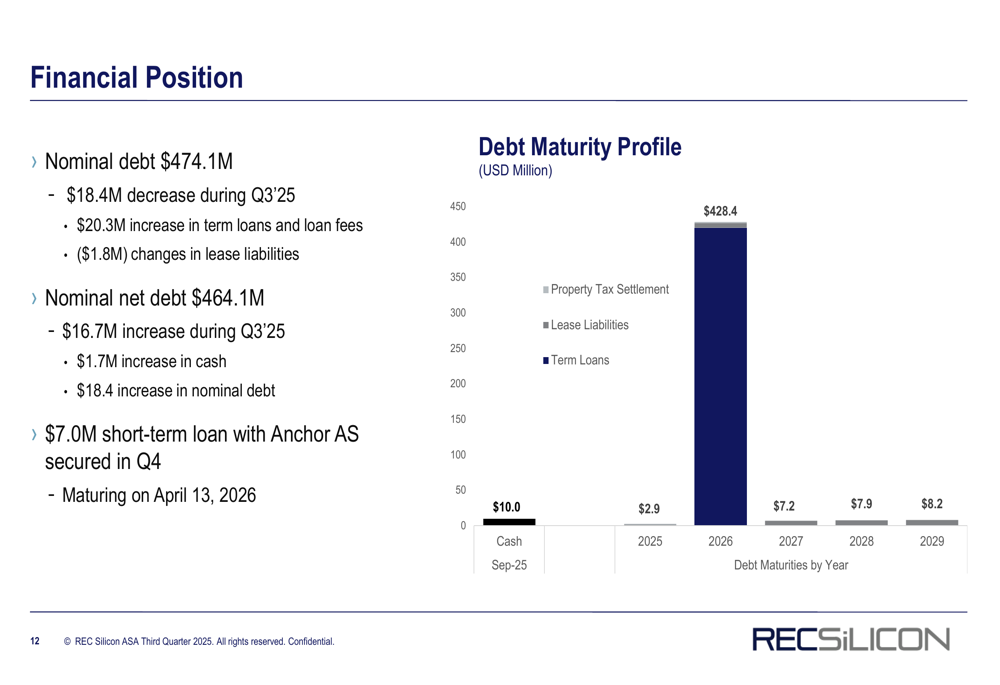

The most pressing financial challenge is the company's debt structure, with nominal debt of $474.1 million and nominal net debt of $464.1 million. Particularly concerning is the debt maturity profile, which shows $428.4 million due in 2026:

To address immediate financing needs, REC Silicon finalized $20.0 million in loans from Hanwha International during the quarter and secured an additional $7.0 million short-term loan with Anchor AS in Q4, maturing in April 2026. However, these measures provide only temporary relief given the scale of the company's debt obligations.

Strategic Initiatives and Cost-Cutting Measures

In response to market challenges and financial pressures, REC Silicon is implementing significant restructuring and cost-reduction initiatives. The company announced plans for approximately 10% workforce reduction in Q4 2025, continuing its efforts to streamline operations.

The company's strategic approach to current market conditions is outlined in the following slide:

Key strategic adjustments include discontinuing Butte polysilicon production and abandoning plans to restart Moses Lake polysilicon operations. Instead, REC Silicon is focusing on optimizing Butte operations, reducing SG&A expenses, and improving baseline silicon gas sales.

The company is also prioritizing the monetization of non-core assets while preserving its positions in semiconductor and flat panel display markets. Management emphasized that core operating assets are not for sale despite financial pressures.

Ownership Changes and Outlook

A significant development during the quarter was the completion of Anchor AS's mandatory offer for REC Silicon shares, resulting in Anchor assuming 60.2% ownership of the company. This follows a voluntary offer launched in May 2025 and completed in July, which initially secured 43.9% of outstanding shares.

Looking forward, REC Silicon provided modest guidance for Q4 2025, targeting silicon gases shipments of approximately 550-600 MT, which would represent a slight improvement over Q3 results. However, the company acknowledged that market conditions remain challenging, with aggressive competition, trade policy uncertainties, and subdued demand continuing to impact performance.

The company summarized its key priorities as follows:

REC Silicon continues to discuss additional financing with Hanwha as well as a more comprehensive restructuring of its term loans. Management emphasized that securing funding for ongoing operations and addressing the looming debt maturities remain top priorities as the company navigates through its financial challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.