TSX up after index logs fresh record high close

Introduction & Market Context

Recursion Pharmaceuticals Inc. (NASDAQ:RXRX) recently presented its Q1 2025 corporate update, highlighting its AI-driven drug discovery platform and pipeline progress against a backdrop of financial challenges. The company’s shares were trading down 4.64% in pre-market at $4.93 following its earnings release, which showed a slight miss on both revenue and EPS expectations.

The presentation comes as Recursion continues to implement its post-Excientia merger strategy, focusing on streamlining operations and prioritizing high-potential programs. With the stock trading closer to its 52-week low of $3.79 than its high of $12.36, the company is working to convince investors that its technology platform can deliver long-term value despite near-term financial headwinds.

Strategic Pipeline Focus

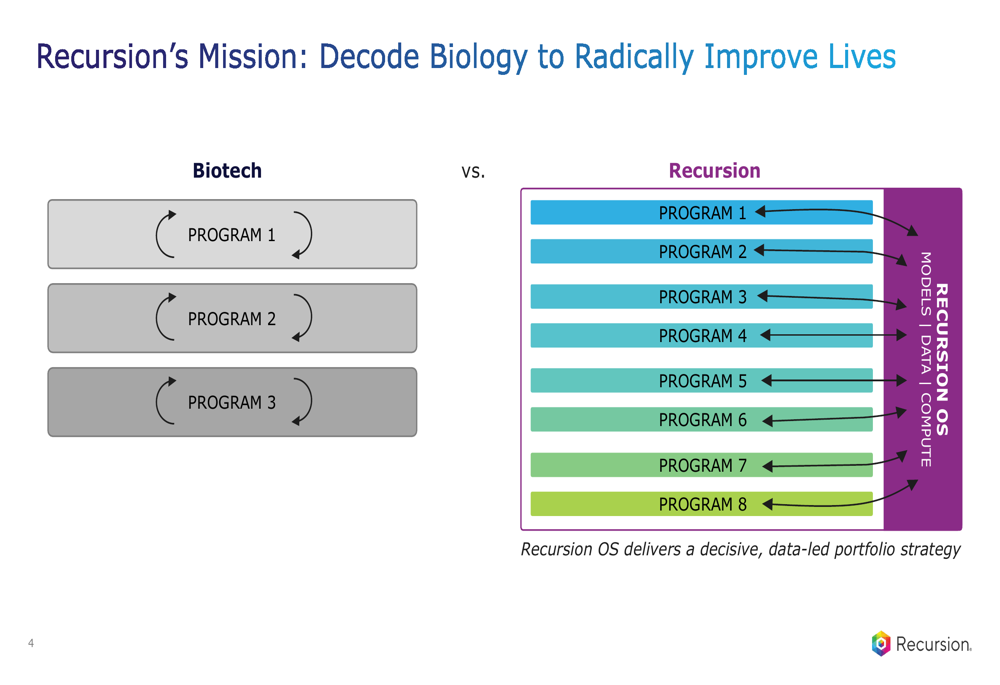

Recursion’s presentation emphasized its differentiated approach compared to traditional biotech companies. While conventional biotechs typically advance one program at a time through a linear development process, Recursion leverages its operating system to simultaneously progress multiple programs with greater efficiency.

As shown in the following comparison between traditional biotech and Recursion’s approach:

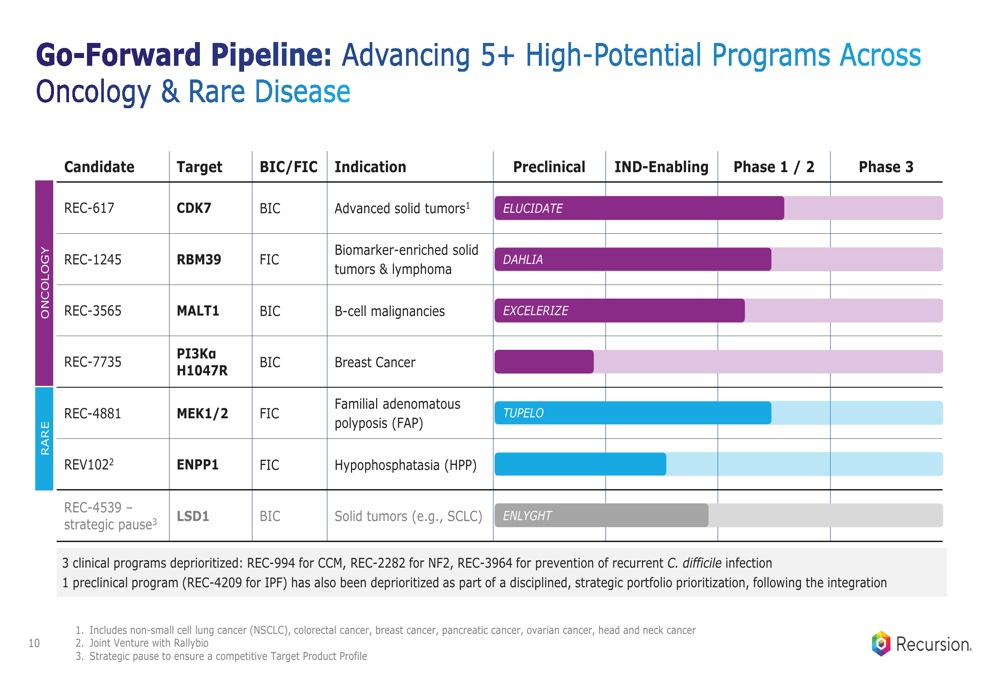

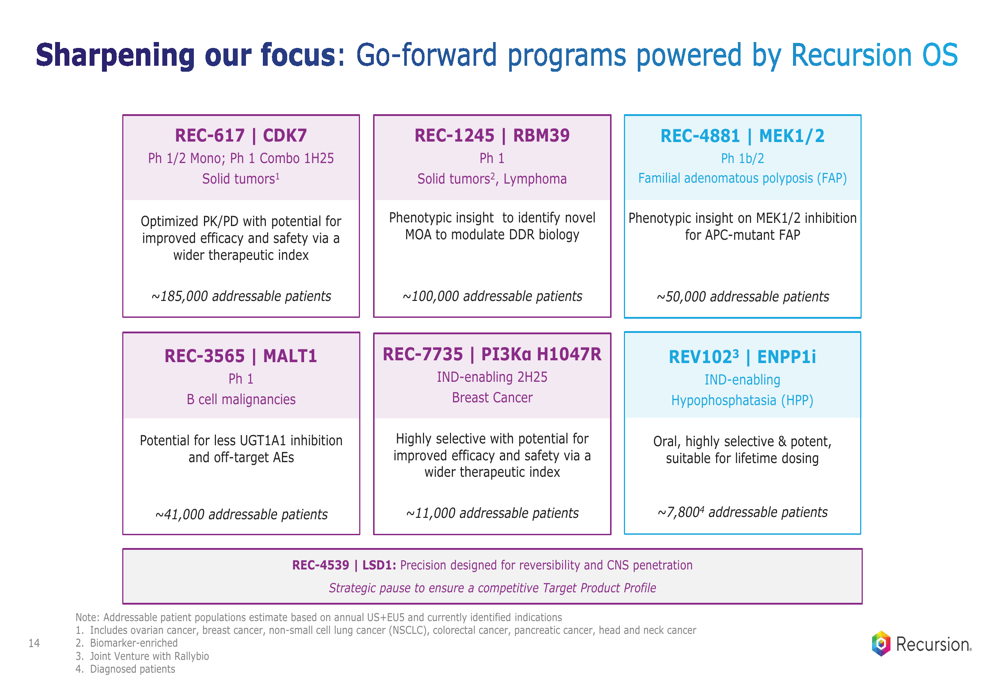

The company has sharpened its focus following the Excientia merger, prioritizing programs with the highest potential for success. Recursion’s pipeline now centers on oncology and rare diseases, with seven key programs at various stages of development. The strategy aims to deliver near and long-term impact while maintaining financial discipline in an uncertain macroeconomic environment.

Recursion’s go-forward pipeline includes promising candidates targeting conditions with significant unmet needs:

The pipeline details reveal substantial addressable patient populations for each program, with the company targeting both first-in-class and best-in-class molecules:

Platform Technology Advantages

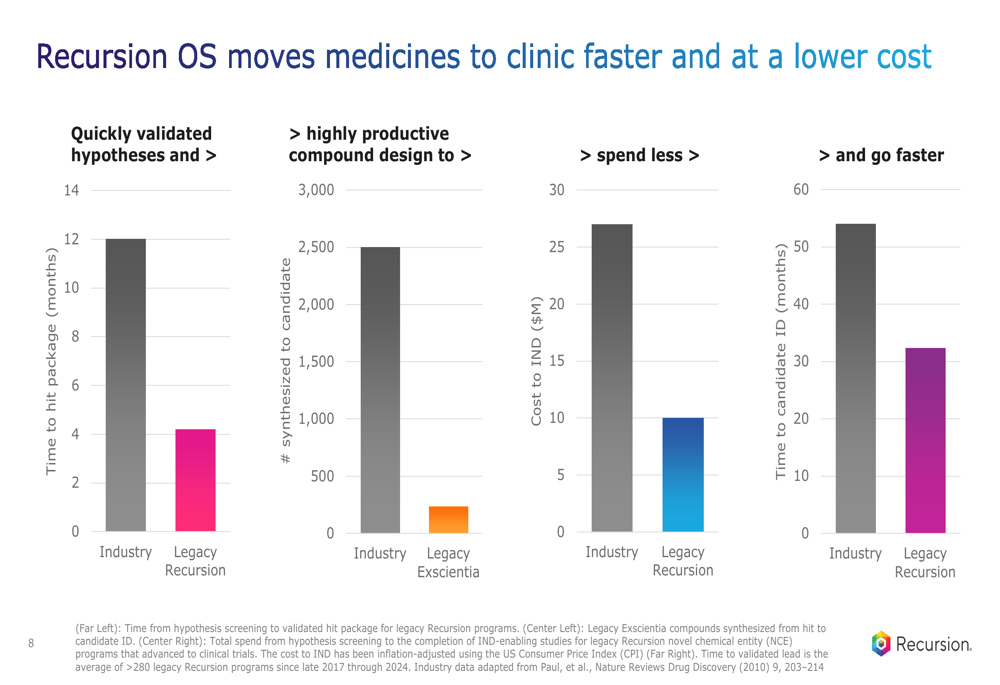

A core element of Recursion’s value proposition is its Recursion OS platform, which has evolved from version 0.1 to 2.0. The company claims significant advantages in speed and cost compared to industry standards, potentially providing a competitive edge in drug development.

The following chart illustrates Recursion’s claimed advantages in hypothesis validation, compound design efficiency, cost, and development timelines:

These efficiency metrics are particularly important given the company’s current financial position. With $509 million in cash as reported in the Q1 earnings release, Recursion projects runway through mid-2027, but improving development economics could extend this timeline or accelerate value creation.

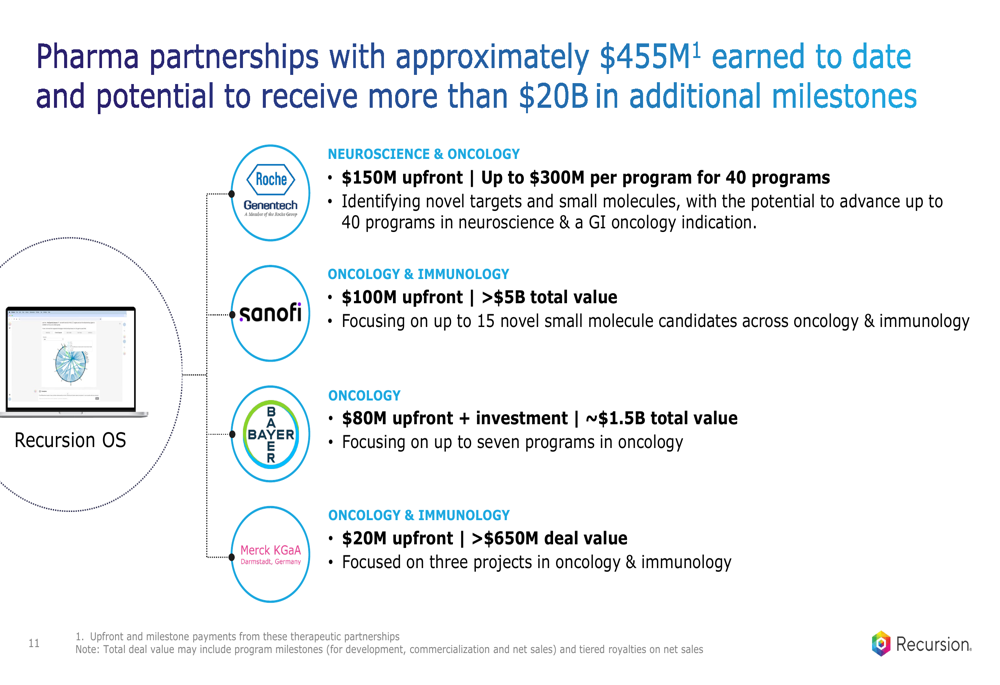

The company has leveraged its platform to secure significant pharmaceutical partnerships, generating approximately $455 million to date with potential for over $20 billion in additional milestone payments:

Key Program Highlights

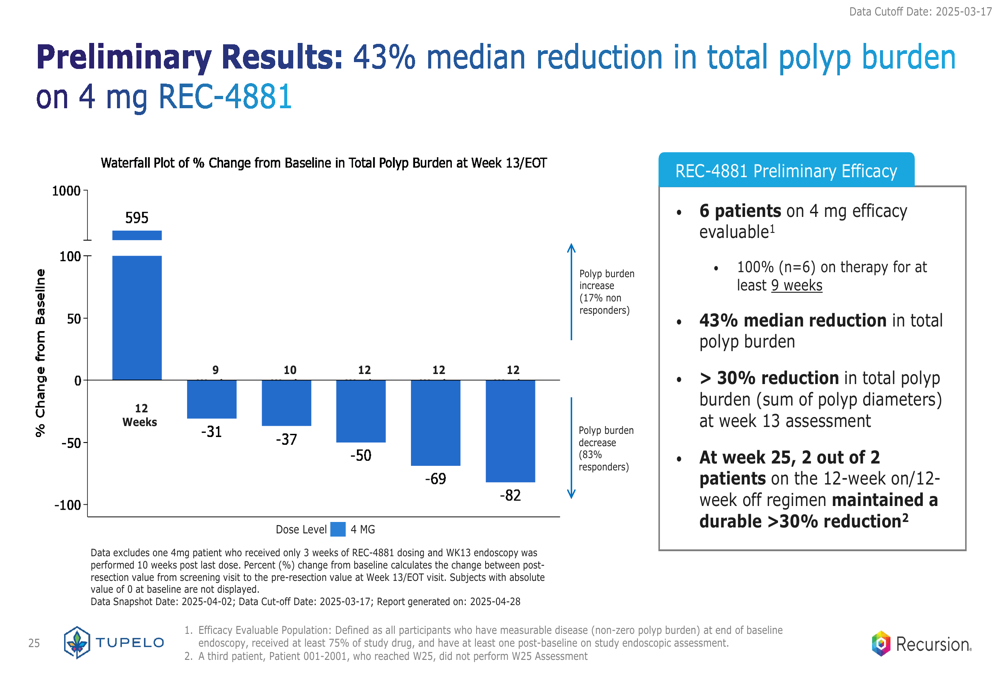

Recursion highlighted several promising programs in its presentation, with particular emphasis on REC-4881 for familial adenomatous polyposis (FAP), a rare disease with no approved systemic therapies.

Preliminary efficacy results for REC-4881 showed a 43% median reduction in total polyp burden at the 4mg dose level, with all evaluated patients showing clinical benefit:

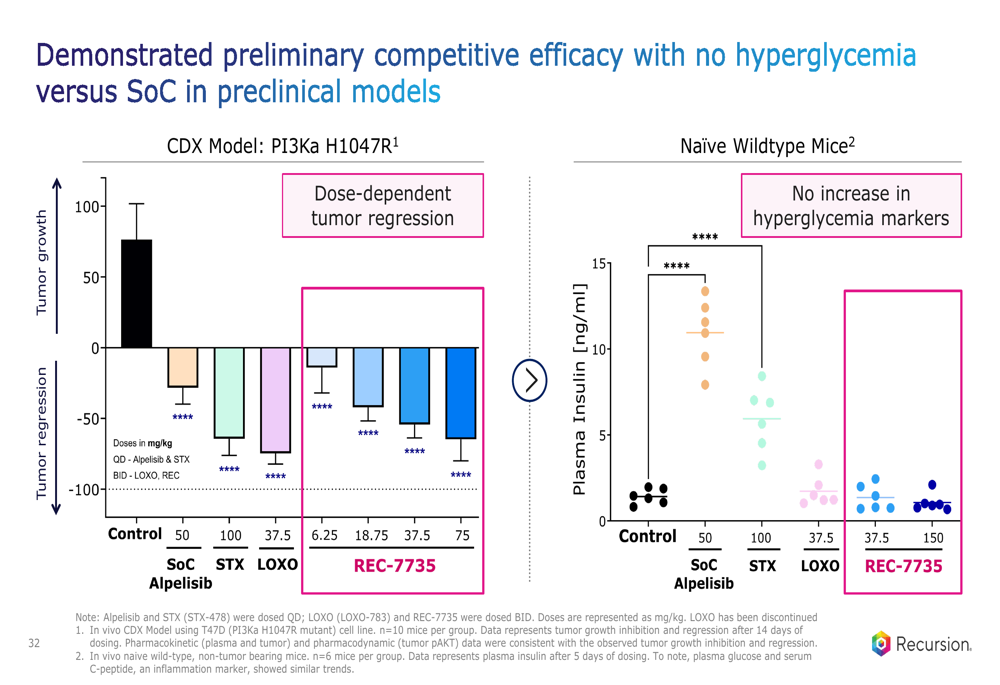

Another highlighted program is REC-7735, a PI3Kα H1047R inhibitor for breast cancer, which demonstrated strong preclinical efficacy compared to competitors:

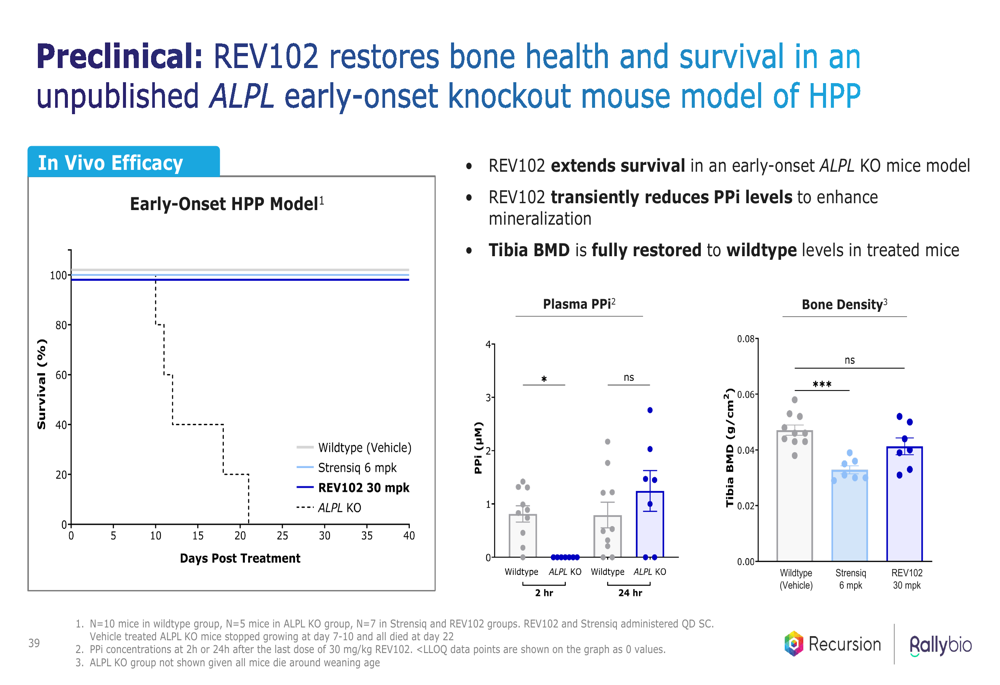

For REV102, an ENPP1 inhibitor targeting hypophosphatasia (HPP), preclinical data showed significant survival benefits and improvement in bone phenotypes:

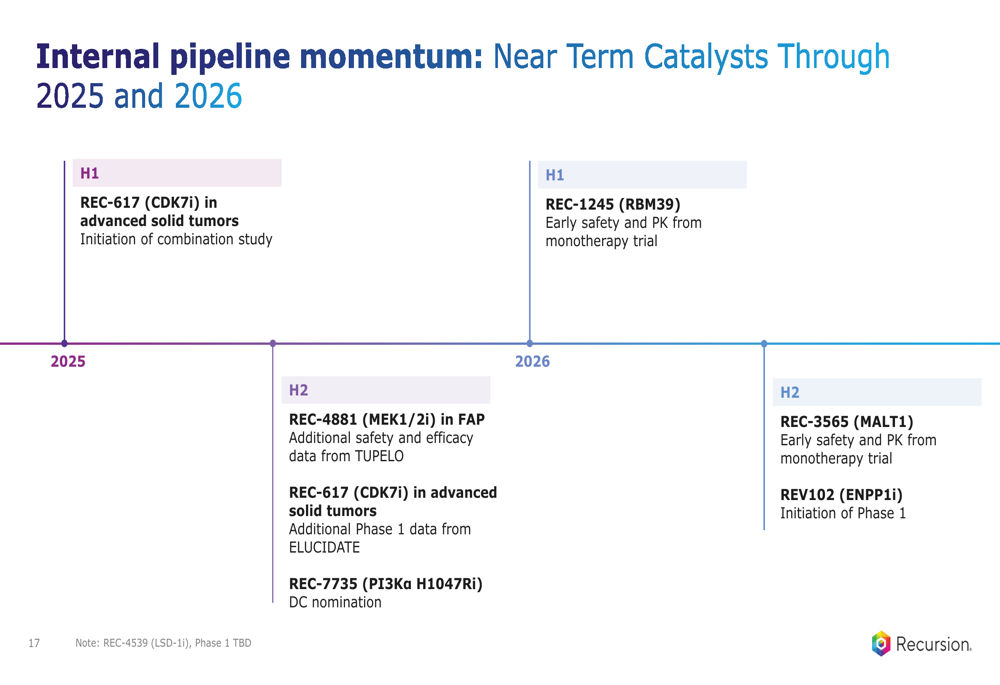

The company outlined several near-term catalysts expected in 2025-2026, which could potentially drive stock performance if positive:

Financial Position & Outlook

Despite the pipeline progress highlighted in the presentation, Recursion’s Q1 2025 financial results revealed ongoing challenges. The company reported revenue of $14.75 million, slightly below the forecast of $14.98 million, and an EPS of -$0.50, missing expectations by $0.01.

The stock’s 35.52% decline over the past year reflects investor concerns about the path to profitability. However, the company has taken steps to reduce its cash burn, reporting $118 million in operational cash burn for Q1 2025, and analysts project 26% revenue growth for FY2025.

CEO Chris Gibson expressed confidence in the company’s position as a leader in the tech-bio space during the earnings call, while CFO Ben Taylor emphasized operational efficiency improvements. The company’s strategic focus on high-potential programs and platform development aims to balance near-term financial constraints with long-term value creation.

For investors, the key question remains whether Recursion’s technological advantages and pipeline progress will translate into financial success before its cash reserves are depleted. The upcoming catalysts in 2025-2026 will be critical in determining whether the company can reverse its stock’s downward trend and deliver on the promise of its AI-driven approach to drug discovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.