Qantas shares slide to 6-mth low as airline trims revenue outlook

Introduction & Market Context

Redeia Corporacion SA (BME:REE) presented its first half 2025 financial results on July 30, 2025, revealing modest growth that fell short of analyst expectations. The Spanish grid operator’s stock has declined 3.43% to €15.78 following the presentation, reflecting investor concerns about the company’s performance and ongoing regulatory investigations.

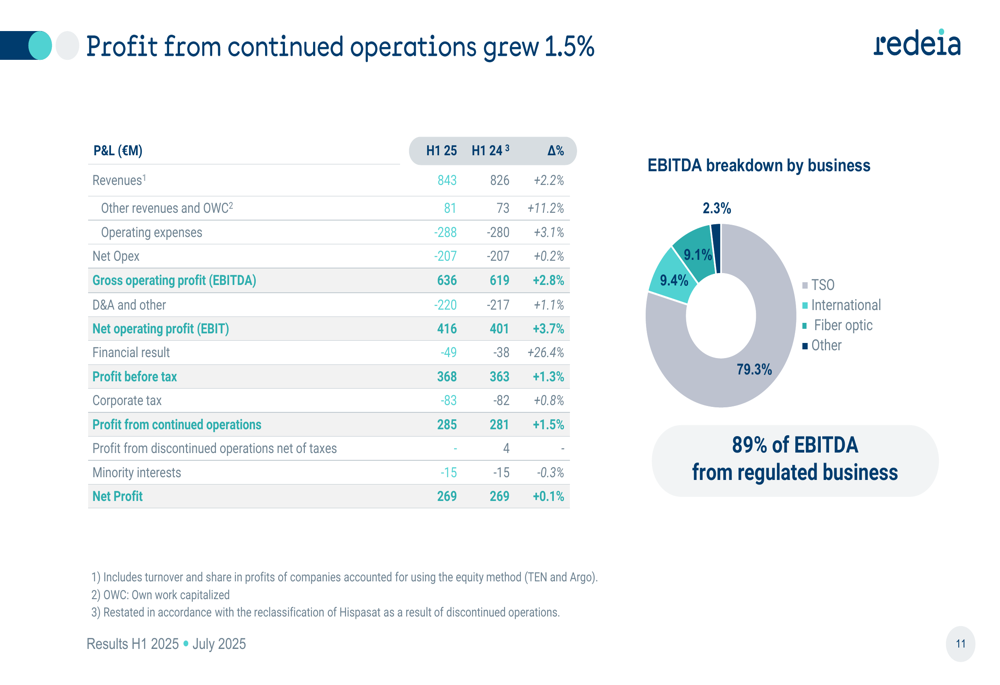

The company reported stable net profit of €269 million for H1 2025, unchanged from the same period last year, while revenue grew by 2.2% to €843 million. However, these results missed analyst forecasts, with earnings per share of €0.23 falling 6.66% below the expected €0.2464.

Quarterly Performance Highlights

Redeia’s financial performance showed incremental improvement in key metrics despite falling short of market expectations. Revenue increased 2.2% year-over-year to €843 million, primarily driven by the company’s Transmission System Operator (TSO) segment, which grew by 3.4%.

As shown in the following profit breakdown:

EBITDA rose 2.8% to €636 million, with 79.3% coming from the TSO business. The company’s international operations and fiber optic segments contributed 9.4% and 9.1% to EBITDA respectively, though both segments experienced slight revenue declines compared to H1 2024. Overall, 89% of the company’s EBITDA came from regulated business.

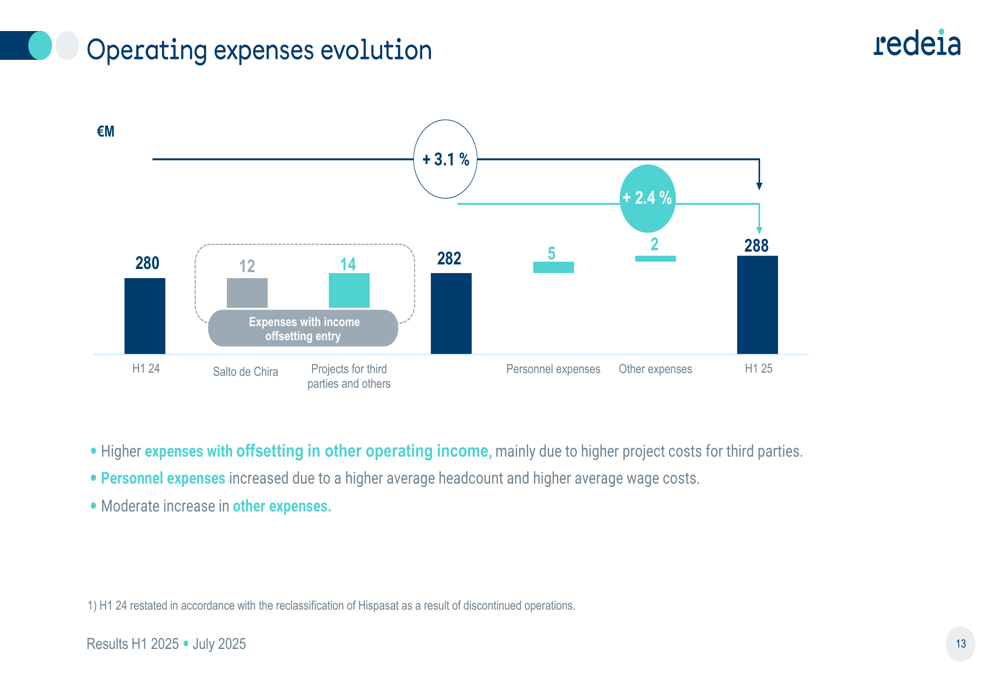

Operating expenses increased by 3.1% to €288 million, driven by costs related to the Salto de Chira project and higher personnel expenses due to increased headcount. This expense growth partially offset revenue gains, as illustrated in the following chart:

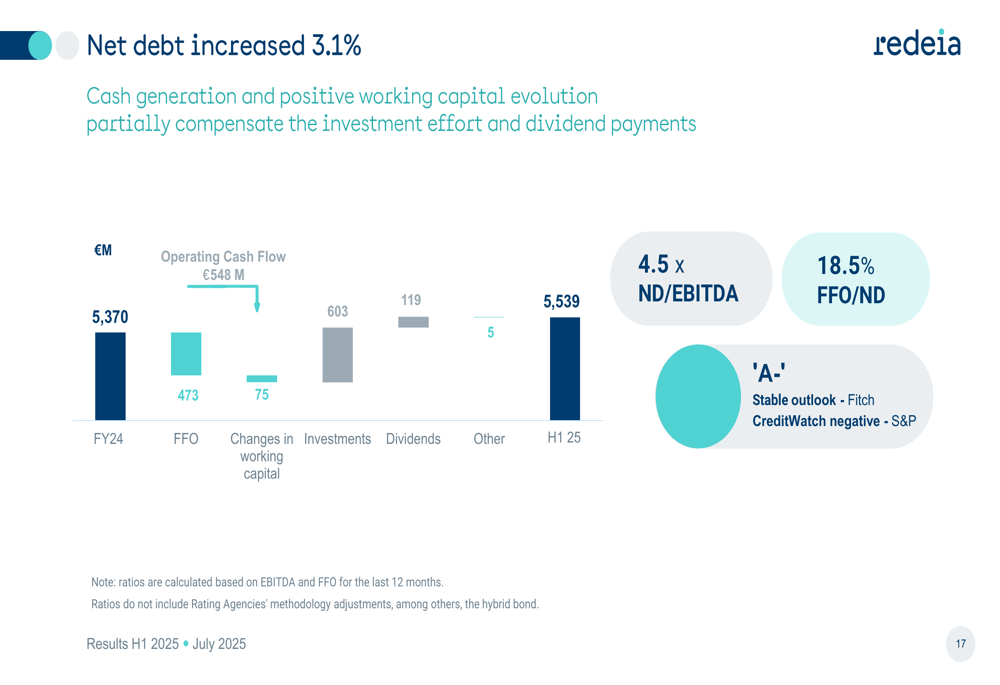

The company’s net debt rose to €5,539 million, up 3.1% from €5,370 million at the end of 2024. This increase was attributed to significant investment activities, though partially offset by positive cash generation and working capital evolution.

Strategic Initiatives & Regulatory Developments

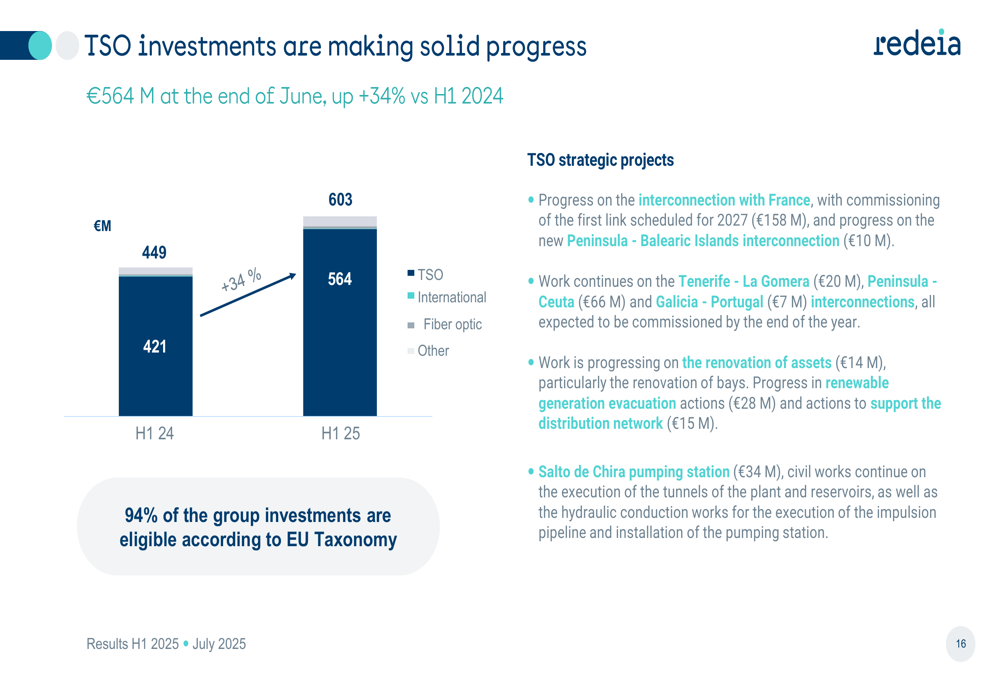

Redeia continues to pursue an aggressive investment strategy, with TSO investments reaching €564 million in H1 2025, a 34% increase compared to the same period last year. The company emphasized that 94% of its investments are eligible under EU Taxonomy guidelines, underscoring its commitment to sustainable development.

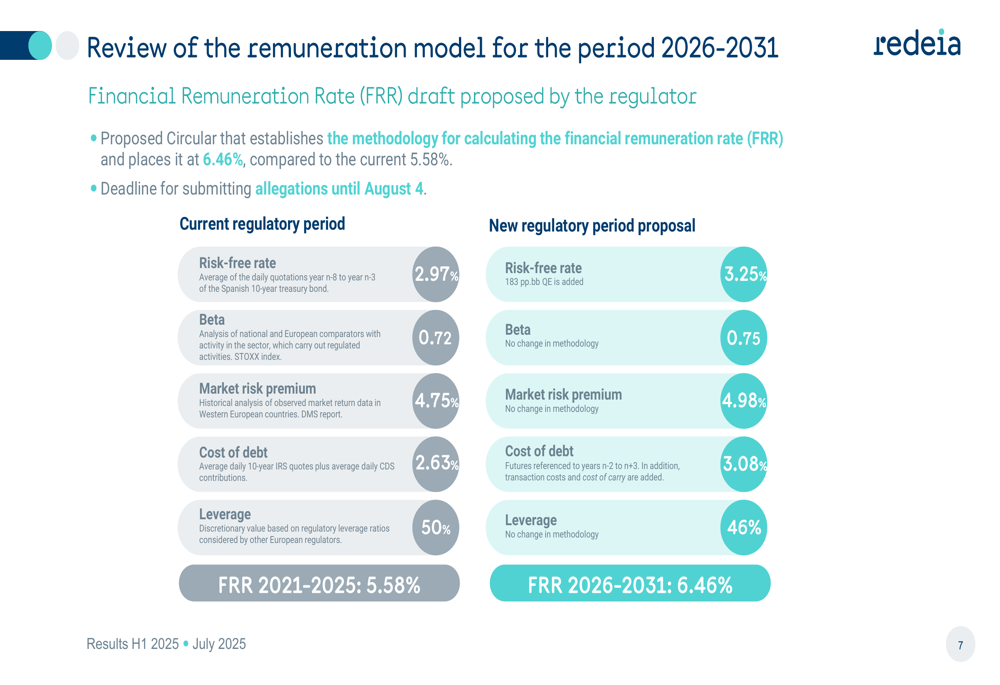

A significant regulatory development is the proposed new Financial Remuneration Rate (FRR) for the 2026-2031 period. The methodology under consideration would increase the FRR to 6.46% from the current 5.58%, potentially improving Redeia’s future financial outlook.

The company is also progressing with the divestment of its Hispasat satellite business, with the transaction expected to close in Q4 2025. Additionally, Redeia secured significant financing support, including two tranches of loans from the European Investment Bank totaling €550 million for strategic projects.

Operational Challenges

A notable operational challenge for Redeia was the April 28 incident in its transmission grid. While the company reported swift restoration of supply, investigations by the CNMC and the National Court are ongoing. Management stated that no provision has been recorded in the interim financial statements, asserting that Red Eléctrica acted in accordance with current regulations.

The company has outlined several recommendations to strengthen the electricity system following the incident, including increased voltage control capabilities, enhanced system oscillation damping, and revised overvoltage function settings. These recommendations have led to the approval of additional investments totaling €750 million, bringing the total planned investment to €8,203 million.

Financial Structure & Outlook

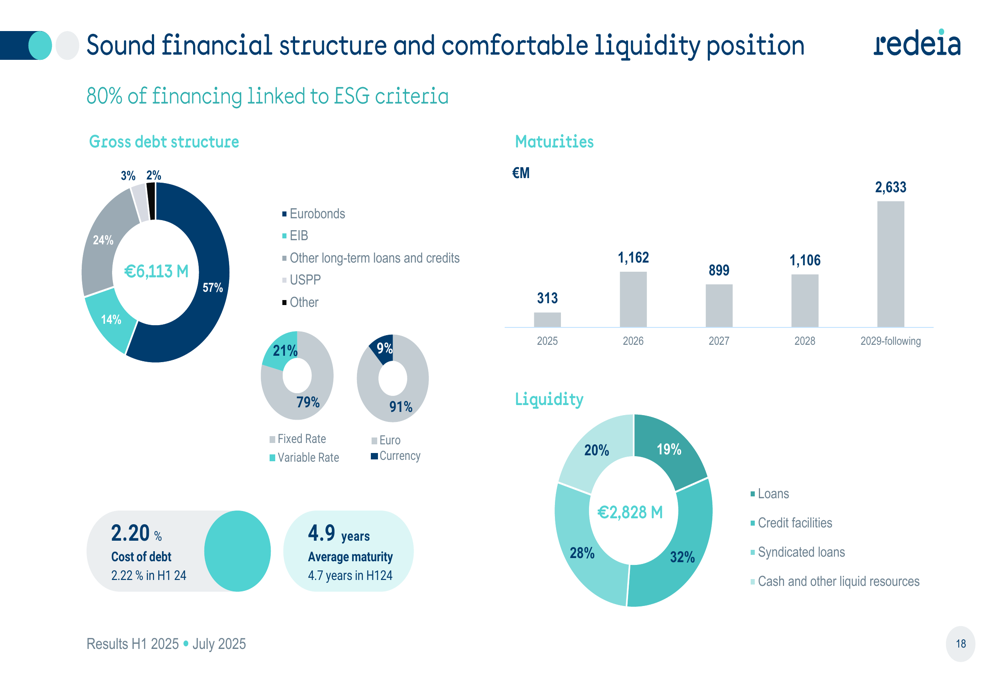

Redeia maintains a diversified financial structure with 80% of its financing linked to ESG criteria. The company’s average debt maturity stands at 4.9 years, with a cost of debt of 2.20%, slightly improved from 2.22% in H1 2024.

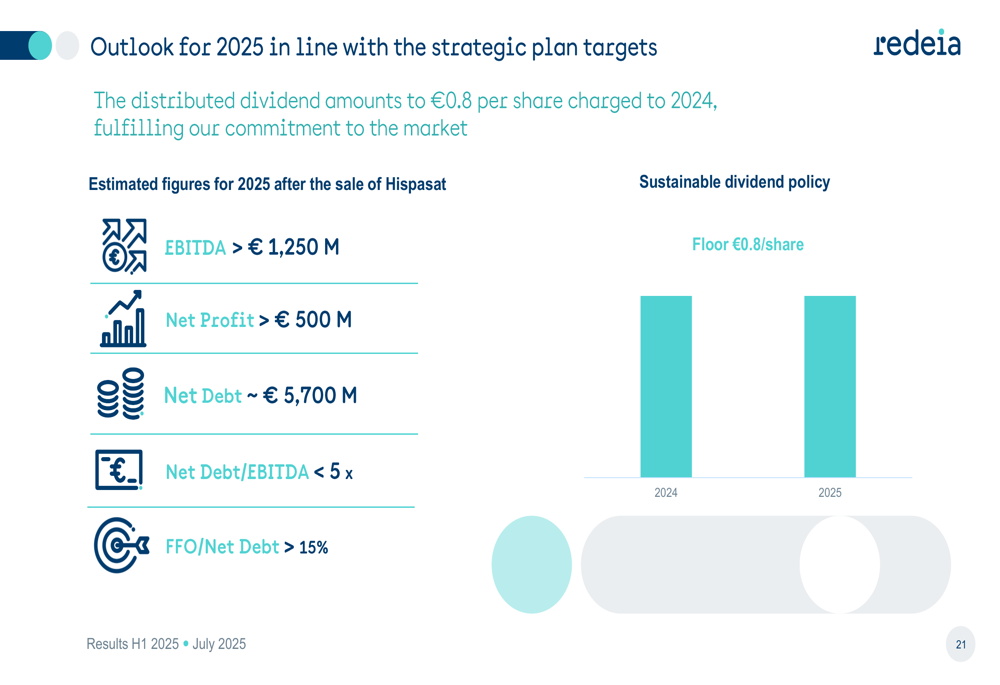

Looking ahead to the full year 2025, Redeia projects EBITDA to exceed €1,250 million and net profit to surpass €500 million after the sale of Hispasat. Net debt is expected to reach approximately €5,700 million, with a net debt to EBITDA ratio below 5x.

The company confirmed its dividend policy with a floor of €0.8 per share, noting that it has already distributed a dividend of €0.6 per share on July 8, 2025.

Analyst Perspectives

Market reaction to Redeia’s results has been negative, with the stock trading closer to its 52-week low of €15.69. Analysts have expressed concerns about the company’s ability to meet its full-year targets given the underperformance in the first half.

The credit rating outlook presents another challenge, with S&P placing the company on CreditWatch negative, though Fitch maintains an ’A-’ rating with a stable outlook. This divergence reflects uncertainty about Redeia’s ability to manage its increasing debt load while pursuing ambitious investment plans.

Despite these concerns, some analysts view the proposed higher remuneration rate for 2026-2031 as a potential catalyst for improved performance in the medium term, provided the company can successfully navigate current operational and financial challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.